A Natural Gas Price Play is Wishful Thinking

Lower tight oil production should mean lower associated gas production so U.S. natural gas prices should rise, right? That is the conventional wisdom. Too bad it is mostly wishful thinking.

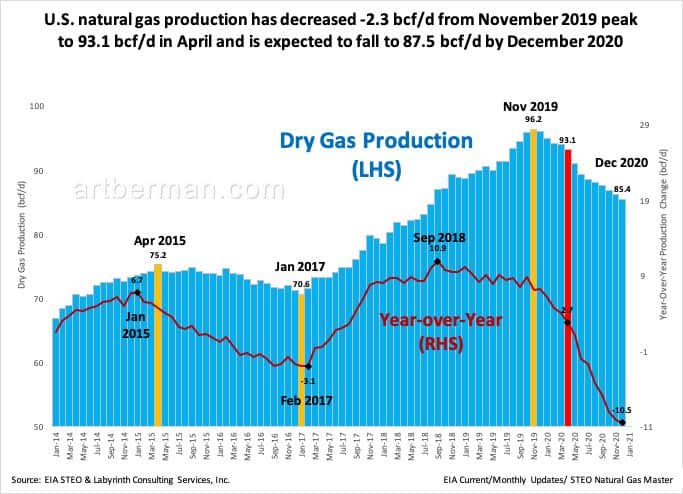

U.S. gas production has already fallen more than 2 bcf/d from the November 2019 peak of 96 bcf/d to 93 bcf/d in April (Figure 1). It is expected to decrease another 7.7 bcc/d by December to 85 bcf/d so that sounds like there might be a supply deficit and higher gas prices.

to 93.1 bcf/d in April and is expected to fall to 87.5 bcf/d by December 2020.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

The problem with that thinking is that it ignores consumption and the resulting supply-demand balance.

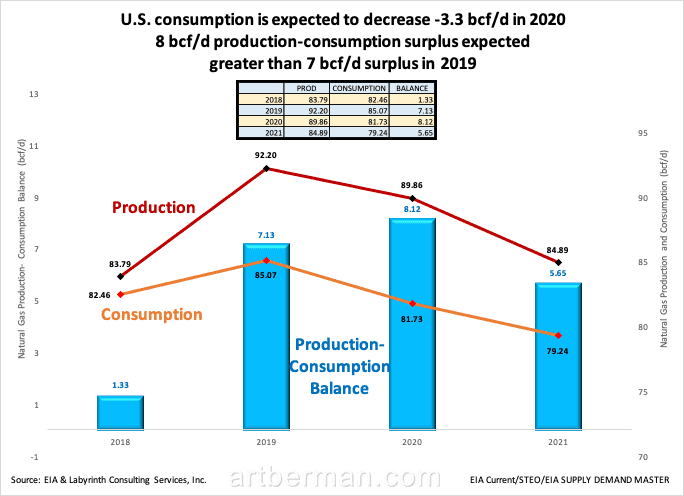

Consumption is expected to decrease 3.3 bcf/d in 2020 compared to 2019 (Figure 2).

8 bcf/d production-consumption surplus expected

greater than 7 bcf/d surplus in 2019.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

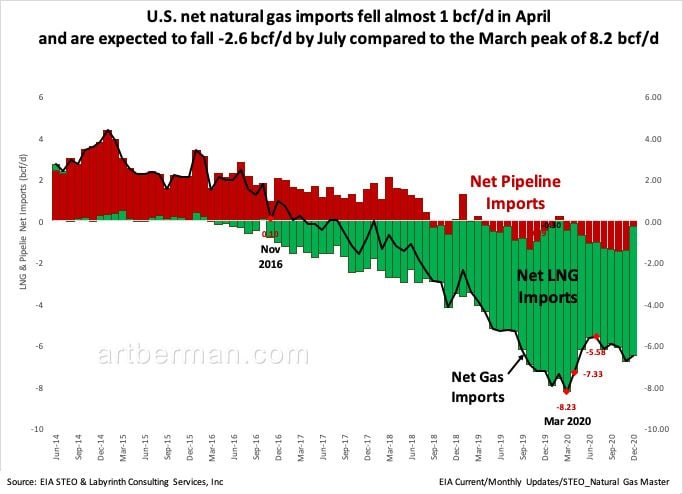

That is not, however, the whole picture because the U.S. became a net exporter of gas in 2016 and these volumes are part of demand. LNG (liquefied natural gas) and pipeline exports fell about 1 bcf/d in April from the March 2020 peak of 8 bcf/d (Figure 3). Exports are expected to continue to decrease to about 5.6 bcf/d in July before increasing again. This is because of low foreign gas prices from decreased demand from Covid-19 economic slow-downs.

Decreased exports mean more domestic supply.

and are expected to fall -2.6 bcf/d by July compared to the March peak of 8.2 bcf/d.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

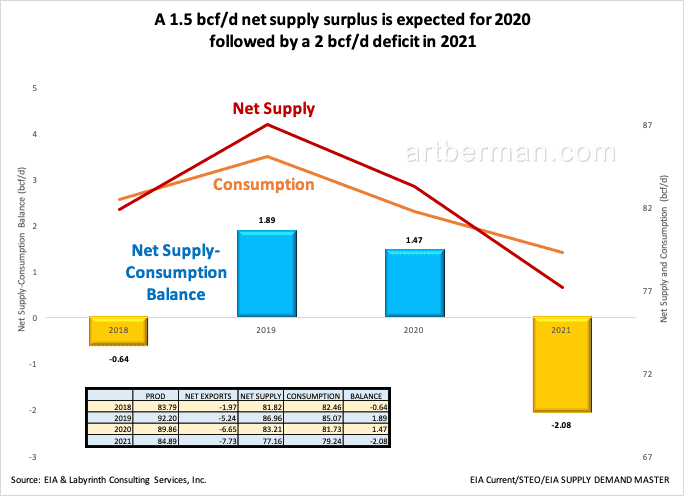

Production minus exports is “net supply.” Net supply differs only slightly from demand because it does not include movements into and out of primary storage.

A supply surplus of about 1.5 bcf/d is expected in 2020 based on the difference between net supply and consumption (Figure 4). The forecast for 2021, however, appears to be a very different story with an implied supply deficit of about 2 bcf/d.

followed by a 2 bcf/d deficit in 2021.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

That suggests that a long bet on natural gas for 2021 might be a reasonable play. The problem is that 2021 is a long time from now and I have little confidence in EIA’s forecast that far into the future.

I believe that its consumption and net export forecasts are optimistic. Gas prices have collapsed in Europe and Asia and the effect of Coronavirus on the global economy is far from certain.

Figure 5 shows gas production, net supply and seasonally-adjusted consumption. This is important because seasonal variation in gas usage storage changes is extreme.

Looked at from this perspective, it is clear that any potential net supply deficit occurs in the second half of 2021. Most of that period is during the summer and fall when gas demand is typically low. Only November and December 2021 fall into the winter heating season and the gap between supply and consumption decreases with increased production levels.

Any supply deficit easily resolved by decreasing export allowables.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

U.S. Department of Energy (DOE) approvals for gas export are provisional. Approvals are subject to review and may be revoked if export “will not be consistent with the public interest.” In the unlikely event that domestic supply became tight, relatively small adjustments of export allowable volumes would provide a simple remedy.

My guess is that market forces will minimize or eliminate any gas supply deficit without DOE intervention. Despite my implied criticism of the far end of EIA’s gas forecast, spot gas prices never reach $3.10 in any month of the forecast. That hardly reflects concern about adequate supply.

I am not suggesting that there is no possibility of a gas-price play in 2021. There is always considerable uncertainty about weather and the pace of economic recovery from coronavirus shutdowns. These could surprise either to the positive or to the negative for gas supply and demand.

The point is that lower production of associated gas does not logically result in a supply deficit. Markets are more complex than that.

Conventional wisdom is, after all, called conventional for a reason.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

[…] June 2020, I […]

I have seen several ‘experts’ pounding the table now, telling people to invest in natural gas, some even suggest daily triple leverage natural gas play (UGAZ), I think that is suicidal.

Anyone who wants real professional advice should stick to the real expert such as Art Berman.

Chee,

I don’t understand why experts think natural gas or LNG is a good bet. I’ve never understood LNG.

Best,

Art

Why are you projecting 2021 consumption drops?

It’s EIA’s projection.

Thanks for another great analysis/article I’ve been studying the Marcellus/Utica supply and outlook and am concluding industry will have no trouble keeping current pace of supply for another decade or more. But not at prices less then $2.50/MMBtu. The Marcellus Tier 1 targets are certainly diminishing and Utica wells – which can equal Marcellus Tier 1 – cost considerably more due to increasing depth. Natural gas plays elsewhere in the country are less prolific and so if Marcellus/Utica struggles at <$2.50, these most definitely will too. So FWIW, I see a long term price needing to be higher than current strip to keep supplies adequate,

Tom,

Thanks for those comments and information. I recently did an evaluation of Haynesville EUR and economics and was surprised to find that wells drilled in 2016-19 break-even at around $2/mmBtu.

All the best,

Art