Art Berman Newsletter: August 2020 (2020-7)

Things are looking bleak for oil markets in early September 2020. WTI fell below $40 today and Brent is not far behind at a little more than $42..

There’s nothing much different from earlier this week or any time in the last month. What’s different is that an equities sell-off has reminded markets of all the uncertainties underlying oil prices.

The economy is a disaster by any objective measure. U.S. unemployment checks stopped a few weeks ago and tens of millions of Americans don’t have enough money to pay their bills. Coronavirus hasn’t gone away and it is improbable that a vaccine will be generally available in 2020. Americans are protesting and looting in the streets.

Nothing apart from the Federal Reserve Bank seems to holding the center from falling apart.

The oil demand recovery is only a recovery if you believe that April was as bad as things can get. The most encouraging part of oil markets is that U.S. comparative inventory has fallen consistently now for six weeks and the oil surplus has been reduced by nearly a third from its highest level in mid-July. I am also encouraged by the slow but incremental increase in diesel consumption because that is the barometer of the economy.

Based on everything that I know about comparative inventory and oil markets, prices should be moving toward $50 or $55 but this time, I don’t think that will happen. Coronavirus has plunged the world into a chasm of uncertainty that has not existed since 2008. Anything could happen and there is more risk to the downside than to the upside.

What concerns me most is what will happen when markets realize that U.S. oil production will fall to levels not seen since the early 2000s.

I have described this in my recent post “Stop Expecting Oil and the Economy to Recover.” I would like use this newsletter to explain why this drastic production decline is unavoidable.

Leads and Lags From Price Signal to Increasing Production

Rig count is a good way to predict future oil production as long as the proper leads and lags are incorporated.

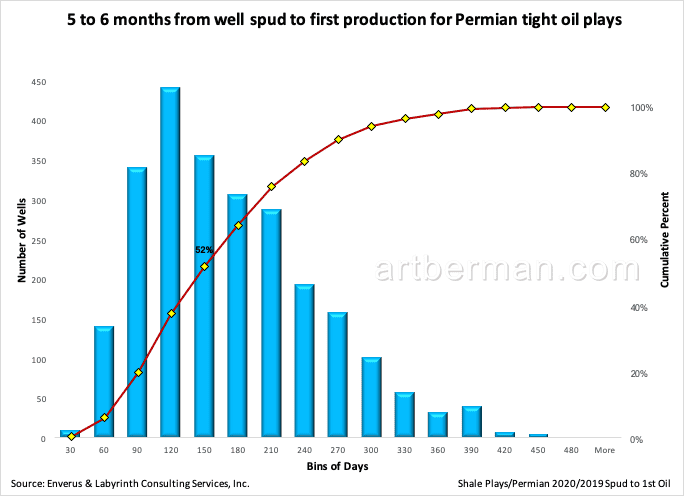

It takes a month or two between an upward price signal and a signed contract for a drilling rig. It takes another 5-6 months from starting a well to first production for tight oil wells (Figure 3). With pad drilling, usually all wells on the pad must be drilled before bringing in a crew to frack the wells.

Source: Enverus and Labyrinth Consulting Services, Inc.

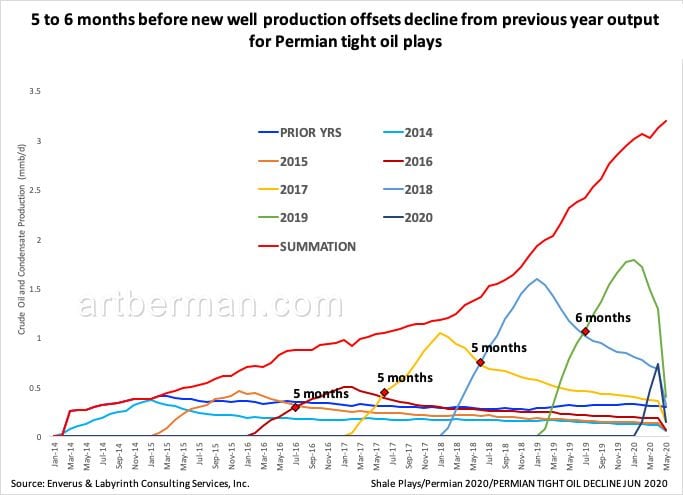

Figure 4 shows the production histories of wells with first production in successive years from 2014 through 2020. Each vintaged year increases to a maximum and then declines.

The key point is that it takes five to six months before first production from new wells offsets declining output from previous years’ well.

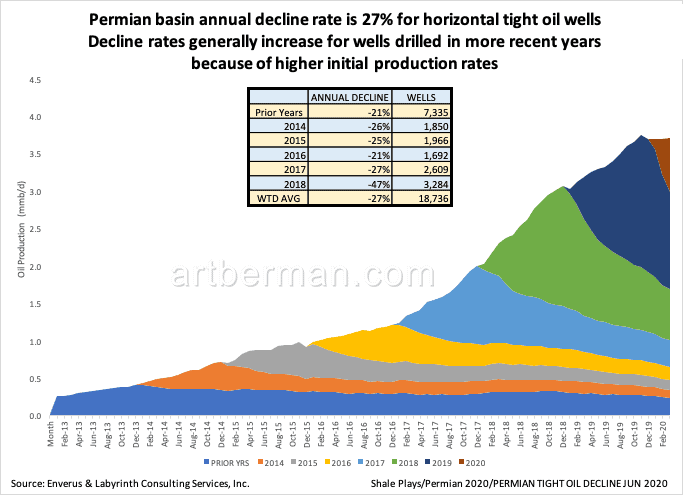

Figure 2 is what has become a fairly standard way to represent vintaged decline rates. That means grouping wells by their year of first production, normalizing those production histories, and observing their group natural decline rate without the complication of adding new wells from subsequent vintaged years.

High decline rates are generally acknowledged for tight oil wells but this allows us to see how those decline rates change over time. In Figure 2, for example, we see that rates have increased from 21% to 47% between 2016 and 2018. That is because completion methods have improved so newer wells produce at higher early rates but their estimated ultimate recoveries have not increased.

Decline rates generally increase for wells drilled in more recent years

because of higher initial production rates.

Source: Enverus and Labyrinth Consulting Services, Inc.

In Figure 3, I have deconstructed those vintaged group declines and shown them as separate curves instead of stacked as they are in Figure 2. The important observation is that it takes five or six months from first production until a new group of wells begins to offset the decline of the previous year production group.

for Permian tight oil plays.

Source: Enverus and Labyrinth Consulting Services, Inc.

So, it takes a month or two between increased price and a rig contract. It takes another 5 or 6 months to drill and complete all the wells on a drilling pad. It then takes another 5 or 6 months from first production before new wells offset declining output from older wells. Add it all together and it takes at least a year between an upward price signal and enough new production to maintain or increases tight oil output.

The End of American Energy Dominance

What I have described here are the details behind the assertions made in my recent post about the inevitability of U.S. oil production decline.

Tight oil is the the foundation of U.S. energy dominance. The U.S. has always been a major oil producer but it moved into the top tier of oil super powers as tight oil boosted output from about 5 mmb/d to more than 12 mmb/d between 2008 and 2019.

World crude and condensate production fell an astonishing 10.8 mmb/d from 82.5 to 71.7 mmb/d from April to June of this year. About 30% of that decline was from U.S. output and a little more than half of the U.S. decline was from tight oil.

U.S. tight oil accounted for 83% of growth in world production over the decade 2009 to 2019. A renewed and increased reduction in tight oil output would mean that world supply would stop growing.

U.S. production may be 50% lower by mid-2021 than at year-end 2019. The implications for U.S. geopolitical power and balance of payments are staggering.

At the same time, it is likely that world oil supply and demand will fall in together if the global economy continues to contract. In that case, lower U.S. and world production may not provoke anything more than a relative decline in world living standard.

No one ever has a clear vision of the future and humans have a terrible record predicting even near-term outcomes. It does seem, however, that uncertainty has rarely been higher. Whatever happens, I am confident that energy will be the economy as much in the future as it has always been. Understanding oil markets has never been more important.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

What was the US demand for oil at the end of 2019 and what is it now? Are we going to import due production decline? Thanks

U.S. consumption was 20.6 mmb/d at the end of 2019 and is now 17.9 mmm/d.

Best,

Art

As a long time reader and first-time subscriber, what are the general actionable areas in which to invest in the upcoming world of $100+ oil? Integrated majors? Do suppliers like Pipe companies, drillers, domestic producers whose assets are being bought for pennies on the dollar?

Bob,

First, thanks for subscribing.

As I wrote in the Newsletter, “Based on everything that I know about comparative inventory and oil markets, prices should be moving toward $50 or $55 but this time, I don’t think that will happen. Coronavirus has plunged the world into a chasm of uncertainty that has not existed since 2008. Anything could happen and there is more risk to the downside than to the upside.”

That is obviously a relatively short- to medium-term view. You are right to conclude that a supply deficit is likely as long as demand recovers and that is not given in my mind.

I am not an investment advisor but looking at performance, Chevron and ConocoPhillips have done quite well through these dark times. For international companies, I admire Total and Equinor.

All the best,

Art