Art Berman Newsletter: September 2020 (2020-8)

U.S. oil inventories have fallen every week for two months yet prices are falling. Weak demand is the explanation from analysts and journalists yet I doubt that most of them could explain what demand is and how it differs from consumption.

Analysts fret about demand but markets focus on ensuring adequate supply at the lowest possible price. Oil company share price correlates with oil price so lower prices eventually affect capital available to drill and complete wells. Supply, therefore, can be increased with higher price and decreased with lower price. Demand is more complex and difficult to modulate so instead, markets use price as leverage to control supply.

In practice, supply and demand are less important than the supply-demand balance. If supply is adequate, and supply and demand decreased together as they have since March, markets remain well-supplied because the balance is unchanged. When markets are well-supplied, price is flat although waves of investor sentiment move it up or down within range boundaries. That is what we are seeing now.

The supply-demand paradigm, in fact, grossly understates supply. That is because it does not account for inventory. It includes movements in and out of storage but ignores the historical cumulative volume already in storage.

Supply and demand accounting is a quick-look overview of the oil market. It provides a present period analysis that may accurately reflect physical market transactions but is ultimately incomplete. It is similar to a current quarter financial statement. It accurately reflects changes since the last quarter but does not include sunk costs—that is capital spent in previous quarters or expenses that were previously written down. In the case of oil supply and demand, excluding storage is quite a sunk-cost equivalent.

Astute analysts have noted for years what they call “missing barrels.” Goehring and Rozencwajg believe that these are because of understated demand but that is not correct. Missing barrels are inherent in the supply-demand accounting method that ignores inventory and only considers present period transactions.

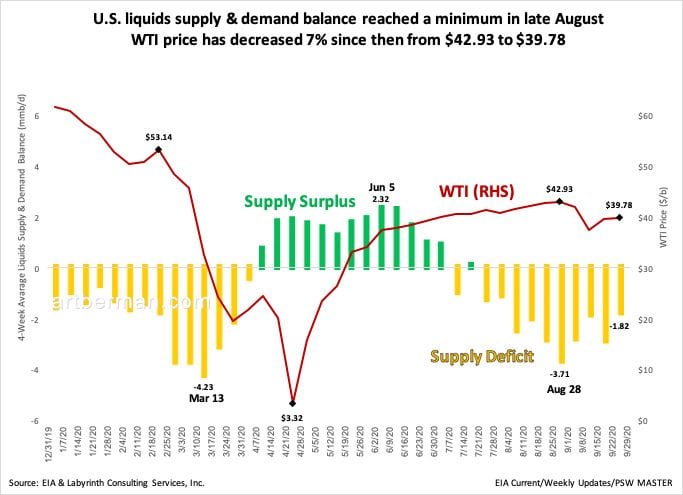

Figure 1 shows U.S. supply-demand balance for 2020. There is a fair correlation between WTI price and the supply-demand balance but some obvious problems as well. That is partly because supply includes oxygenated fuels, natural gas plant liquids and refinery gain that are not important factors in price formation. These have averaged 6.9 mmb/d so far in 2020—that is 27% of what is considered “oil” in global supply-demand accounting!

WTI price has decreased 7% since then from $42.93 to $39.78.

Source: EIA and Labyrinth Consulting Services, Inc.

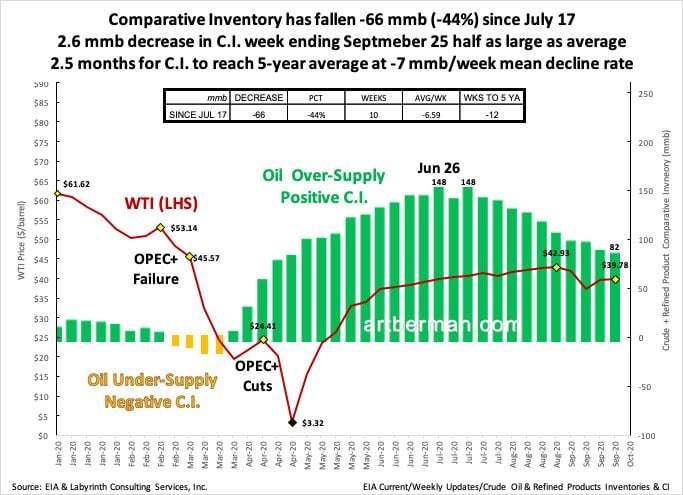

Figure 2 shows U.S. comparative inventory over the same period. It also has problems. That is mostly because oil prices recovered from near-zero despite growing comparative inventory.

2.6 mmb decrease in C.I. week ending Septmeber 25 half as large as average.

2.5 months for C.I. to reach 5-year average at -7 mmb/week mean decline rate.

Source: EIA and Labyrinth Consulting Services, Inc.

Both methods are incomplete but the contrast between the two is stark and obvious. Supply and demand suggests that oil prices should be sky-high with a deficit of 2 to 4 mmb/d.

Comparative inventory suggests that a considerable supply overhand is putting a ceiling on prices—a compelling explanation for current pricing.

U.S. supply and demand is difficult and messy to determine correctly even though the necessary inputs and outputs are publicly available thanks to the EIA. Global supply and demand is little more than a guess because much of the data is simply unavailable or unreliable.

A spectrum of information is needed to arrive at a reasonably robust understanding of oil markets and pricing. I don’t place much value in supply and demand but most analysts would probably disagree.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts