Art Berman Newsletter: October 2021 (2021-9)

“This market is on fire. The only way is up. The market is hungry for oil. There’s quite a chance of reaching $100 a barrel.”

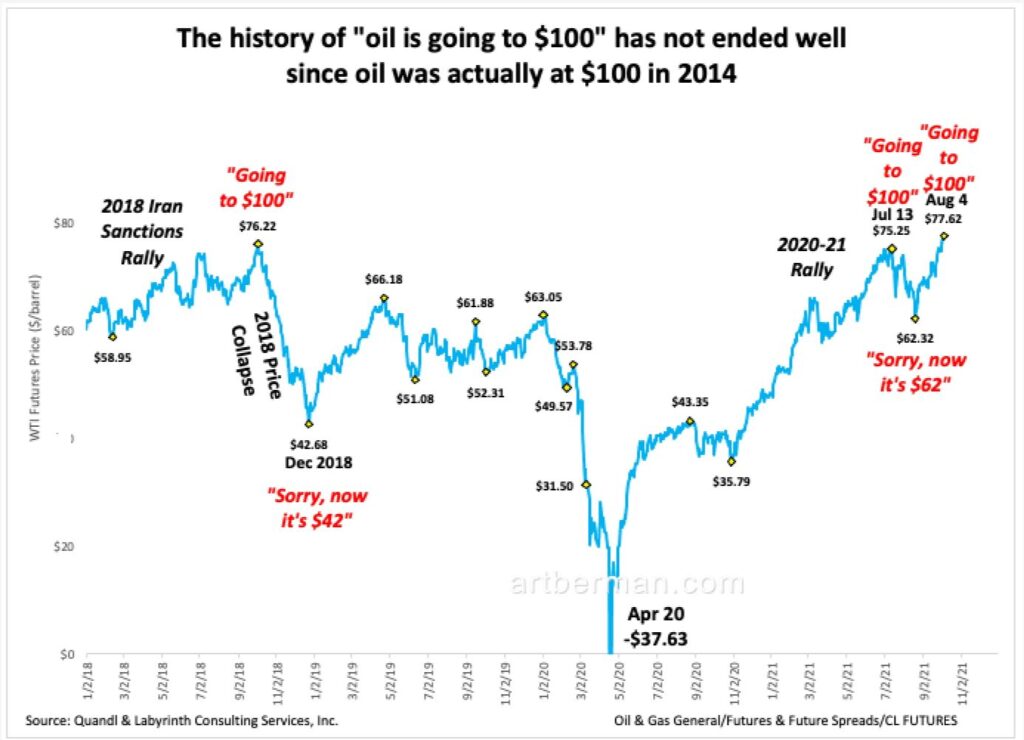

I wrote that sarcastically three months ago in the July 2021 Newsletter. WTI price was $75.25 the last time analysts proclaimed $100 oil just around the corner in mid-July (Figure 1). It fell three times after that to $62.32 by August 20. Now, it has reached a multi-year high of $77.62 following the OPEC+ announcement on October 4 to hold production steady and, of course, analysts are certain that oil is going to $100.

The same claims were made during the 2018 Iran sanctions price rally when oil reached its last high of $76.22 in early October, 2018. By late December, prices had collapsed to $42.68.

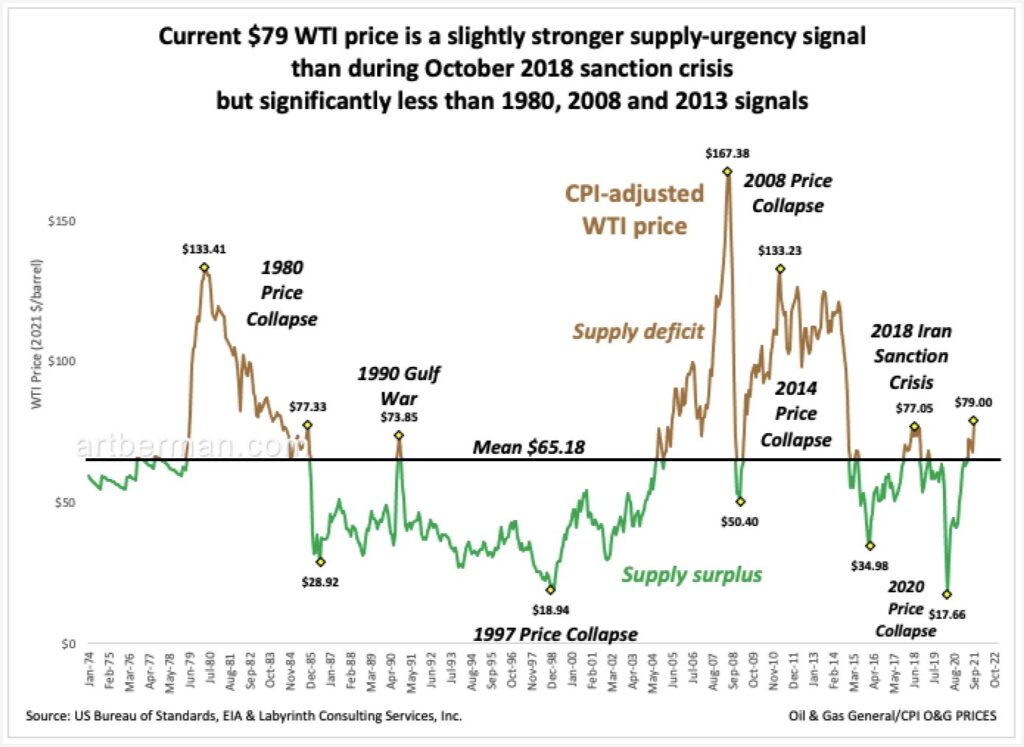

The truth is that the history of “oil is going to $100” has not ended well since oil was actually $100 in 2014. Figure 2 shows inflation-adjusted WTI prices and key historical events from 1974 to the present. The current WTI futures price of about $79 per barrel represents only a slightly stronger supply-urgency signal than the price at the peak of the 2018 Iran sanctions crisis. It is significantly less than previous supply-urgency signals in 1980. 2008 and 2013.

Lacking this context, Bank of America has raised its price forecast to $100 per barrel (Figure 3).

Goldman Sachs has raised its Brent forecast from $80 to $90 per barrel. The investment bank stated that “global stocks are being depleted at a rate of about 4.5m b/d — the fastest draw on record — and inventory could fall to its lowest level since 2013 by the end of the year.”

In July, Goldman’s Jeff Currie made a similar case for $80 oil by late August which obviously wasn’t correct.

Have oil fundamentals really changed since July or is this just another case of analysts blowing smoke?

Many of the arguments today are similar to those before—surging oil demand, flat U.S. shale production, and industry under-investment among them. On the other hand, some things have changed.

A major hurricane disrupted oil and gas production in the Gulf of Mexico more than any storm in decades. A natural gas shortage in Europe has pushed gas prices to record highs and may increase oil demand as some consumers switch from gas to heating oil. A coal shortage in China has forced electric power cutbacks to some industries. Filling stations in the U.K. are out of fuel as supply chain disruptions and labor disruptions are affecting markets and economic activity worldwide.

Hurricane in Gulf of Mexico

Oil and natural gas prices began to increase in the U.S. when the National Hurricane Center stated the likelihood that a powerful new storm in the Caribbean would enter the Gulf of Mexico. WTI increased from $62 on August 20 to $69 by the time Hurricane Ida made landfall in Louisiana.

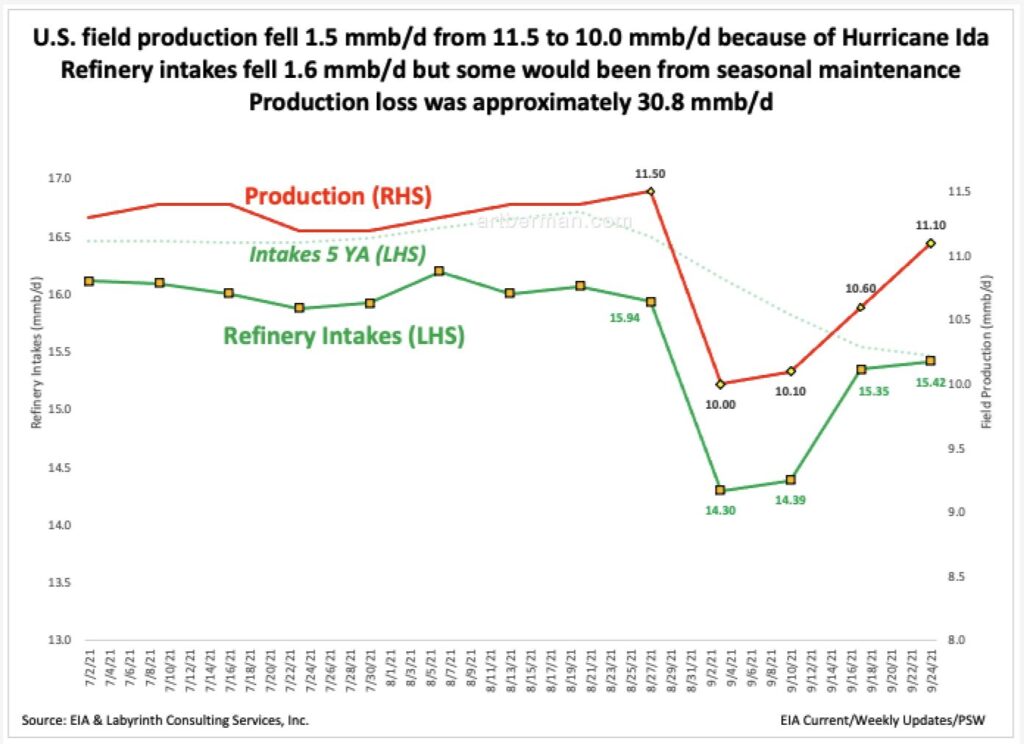

U.S. field production fell 1.5 mmb/d from 11.5 to 10.0 mmb/d (Figure 4). Refinery intakes fell 1.6 mmb/d but some of that decline was from seasonal maintenance—note that the 5-year average dotted, green line in Figure 4 was already decreasing. The total production loss is estimated at approximately about 31 mmb.

Tropical storm Nicholas further disrupted refining and onshore facilities in Louisiana in mid-September.

Once the damage was assessed, prices rose to $73. It now seems that 200 to 250 kb/d of production will probably remain off line until the first quarter of 2021.

Disruption from Hurricane Ida continues to impair approximately 540 mmbcf/d of gas production from the Gulf of Mexico. That’s an improvement of 340 mmbc/d from a week ago when 880 mmcd/d was offline.

Natural Gas Shortage

U.S. gas spot price reached $6.37 per mmBtu this week. That’s +$4.45 (+232%) higher than a year ago. Even before Ida, prices for the first half of September were +$2.81 (+57%) higher than a year ago. A hot summer has been a factor for higher prices but the main reason that gas prices are higher is because gas exports are nearly three times higher than last summer.

Last summer, gas exports decreased from 9 bcf/d in March to only 4.5 bcf/d in July because of low demand in the early months of the pandemic. Exports for August 2021 were more than 12 bcf/d. In other words, there is approximately 7.5 bcf/d more demand for gas this summer than there was a year ago. That’s why inventories are low and prices are high.

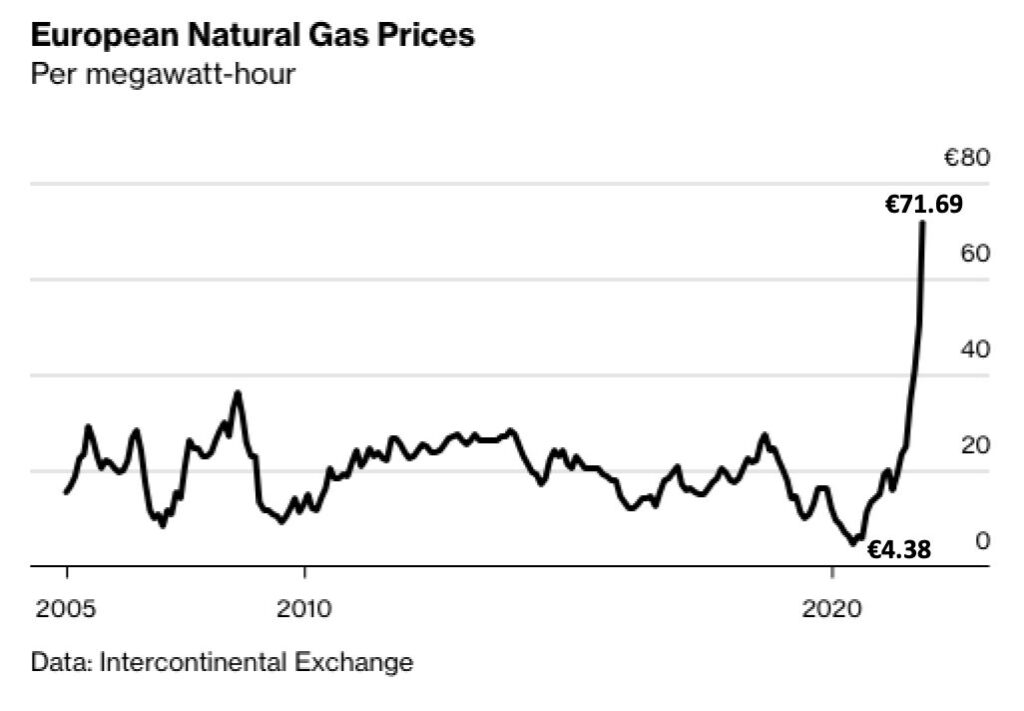

Meanwhile, a serious natural gas shortage has developed in Europe. Its origins are complex but chiefly lie in a naive belief that gas and coal could be readily be replaced by renewable sources. Gas prices are now above $20/mmBtu in most of Europe and electricity prices have resulting electricity prices have increased 16-fold (Figure 5).

Three large fertilizer plants have closed and electric power plants to have been forced to produce less electricity. A slew of industries that include steel, food processing and hospital supply are experiencing the effects of carbon dioxide shortages and higher prices for everything that depends on natural gas for its manufacture and distribution.

Welcome to the Energy Transition.

Coal Shortages

The futures price for Australia’s Newcastle thermal coal—the Asian benchmark—has increased from about $100 per tonne in June to $270 per tonne in early October (Figure 6).

Meanwhile, coal prices in Europe are at record levels because of lower wind output, record-high natural gas prices and nuclear plant seasonal maintenance outages. Europe’s carbon tariffs have further added to coal’s cost. Rotterdam coal futures for January 2022 delivery have risen from about $90 per tonne in June to $254 per tonne today.

The simple explanation for tight supply and high prices is that rapid recovery from the Covid pandemic has put unexpected pressure on supply. Ongoing Covid lockdowns and sick workers in mines combined with similar problems for coal transport resulted in shortages. While all of that is true, it does not fully explain the shortage.

It is a confluence of inter-related factors and feedback loops that typically describe complex systems like energy.

China produces half of all the coal mined in the world but it relies on imports to meet its growing demand for electric power. Last November, it placed an embargo on coal imports from Australia. This was the complicated culmination of poor relations between the mostly foreign-owned Australian coal industry and its east Asian customer.

China turned to other sources for its coal including Indonesia. That left less coal for other buyers like India—the world’s second largest coal importer—and Europe. Record rain in Indonesia, however, has limited shipments so, like Europe, China began using natural gas for power generation further inflating the global price for that commodity. On the other hand, India and Brazil are now buying more coal from Australia following the rupture of its trade with China.

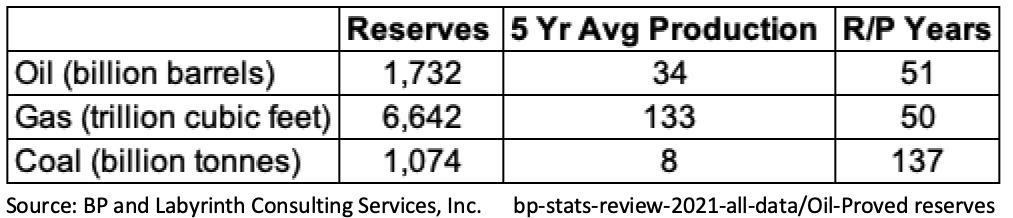

The world is not running out of coal. Based on proved reserves and the 5-year average production rate there are roughly 137 years of coal left in the world (Table 1). That’s about 2.75 times longer than for oil or natural gas. The method R/P (reserves divided by production) is coarse but the comparison is clear: there’s a lot more coal left in the world than oil or gas. The present problem with coal supply is logistical.

China Power Shortage and Evergrande

With coal in tight supply, many Chinese power producers are outbidding European buyers for liquefied natural gas cargoes in preparation for winter before spot prices increase further. Many who cannot switch to gas have curtailed power production. The government fixes consumer prices so at some wholesale price threshold, producers lose less money by not producing electricity than by producing it. That means less electric power for industries since households receive preferential treatment from the state.

In the middle of this energy crisis, the government has chosen to further curtail power allotment to industries that are the biggest carbon emitters. It’s unclear if this is a way to save face because the supply is simply not there, or if it is indeed a plan motivated by environmental quality. Target industries include fertilizer, steel, aluminum and chemicals. The result is reduced economic activity.

Goldman Sachs recently downgraded China’s growth forecast for the second half of the year largely because of the power crisis writing, “Recent sharp cuts to production in a range of high-energy-intensity industries add to the already significant downside pressures in the growth outlook.” Its forecast for 3.2% fourth quarter growth—down from its earlier forecast of 4.1%—would be China’s lowest since the second quarter of 2020, when the country was early in recovery from pandemic lockdowns.

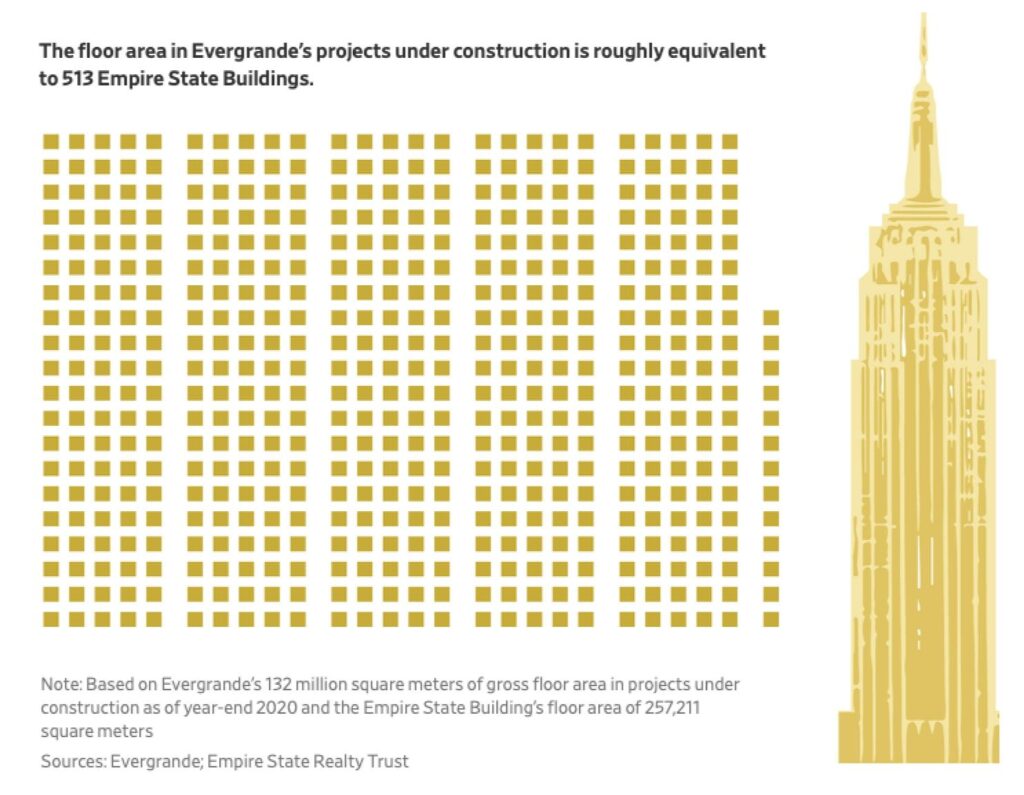

At the same time, the Evergrande debacle is unfolding. Evergrande is the largest real estate developer in China (Figure 7). It benefited from the $1.6 trillion government infrastructure spending over the last decade that has resulted in a massive real-estate bubble. This includes the “superblock”cities with no inhabitants.

Lauren Teixeira wrote in 2019 that “superblock planning…was irresistible to Chinese officials, who could quickly expand the housing supply and generate a massive amount of tax revenue in the process.”

Last weekend, John Mauldin summarized it this way: “The key point here: Evergrande-like development in China wasn’t just capitalism doing its thing. It was capitalism facilitated by government officials for their own purposes. Beijing wanted social order and local officials wanted revenue. The housing projects helped deliver both.”

Evergrande missed a payment this month on part of its staggering $300 billion debt and it doesn’t look like the government is going to do much to help. Some analysts fear that the fallout from Evergrande maybe a “Lehmann Brothers moment” but it is more likely to be initially limited to China. Its deflationary effects, however, will almost certainly spread throughout the global economy.

Supply Chains

If you’ve tried to rent a car, good luck. There aren’t any because there aren’t enough semiconductors to make new cars to replace those sold during the height of the pandemic because of no demand.

There are approximately seventy container ships anchored off the Port of Los Angeles because there aren’t enough dock workers to unload them or enough truck drivers to take the delivered goods to buyers. There’s a gasoline and diesel shortage in the U.K. not for lack of fuel but for lack of truck drivers to deliver fuel from refineries to filling stations (Figure 8).

The list goes on. These shortages are not born of scarcity. They are blamed on supply chain breakdowns. We assume that the problem is because of Covid and that things will go back to normal once the pandemic is over. Thoughtful people realize that although the supply chain problems will slowly improve, nothing is going back to the way it was before Covid.

Amy Davidson Sorkin recently wrote, “Americans are not facing Soviet-style empty shelves, or having to scrap for the basics. In aggregate, we are hardly in a condition of scarcity. Still, supply-chain trouble suggests that something is off with the way we’re operating in the world, and that we don’t yet know the extent of our vulnerabilities. The issues can also be a serious impediment to a broader economic recovery.”

Covid-19 exposed the long-standing problem of relying on the lowest-cost producer for supplies that are critical for national security. Beginning in the 1970s, American manufacturing was progressively dismantled in favor of cheaper suppliers in places like China and India. The market place is efficient but does not always work in the public interest. Prices went down and a just-in-time economy developed but nothing was done to ensure domestic supplies in the event that just-in-time wasn’t.

Is Oil Going to $100?

It is bizarre that analysts promoting a bull oil thesis seem to ignore China. It is, after all, the world’s largest oil importer and its economic growth and energy consumption have dominated world demand for most of the last 20 years. High oil prices are unacceptable to China. It has used its cash power to manipulate world oil prices by either buying crude or selling cheap refined products for several years. Its recent release of crude from its strategic petroleum reserve was the prelude to its power and Evergrande crises.

Jeff Currie says that oil prices are set to “explode to the upside” regardless of what happens to gas prices. He says that markets have come from of a period of pricing demand recovery after Covid to now pricing scarcity. He argues that production outages from Hurricane Ida have fully offset OPEC+ supply increases to date and that markets are already in a supply-demand deficit. He further states that the “demand hit” from the Delta variant was smaller than most expected.

Bank of America’s Francisco Blanch said this week that, “Oil demand is coming back from mobility…but it’s also coming with natural gas prices rising so fast & creating substitution back into oil.” He didn’t explain what he meant by that. Let me be generous and say that this may happen on a small scale for heating oil during the winter but for now it is purely speculative and certainly is not affecting present oil prices. Nevertheless, Bank of America later raised is Brent estimate to $100 per barrel.

JP Morgan Chase wrote in a note to clients that gas is so expensive in some places that switching to refined products could increase global demand by 900 kb/d.

That’s a lovely idea but it has little practical application outside of consumers or power plants that can switch between heating oil and natural gas. It’s not as if many can substitute natural gas for gasoline or diesel in their car or truck.

Right now it certainly feels like these analysts may be right about much higher oil prices but I remain skeptical. Oil markets are tight and prices are higher right now because of hurricane disruption in the U.S. Gulf of Mexico but this is temporary. Similarly, the gas crisis in Europe is serious but ultimately also temporary. The OPEC+ meeting earlier this week had a huge effect but history suggests that this will fade.

The world has a lot more oil and gas than it is likely to need for at least the next few years. Europe got caught with its energy pants down and things will get difficult if the winter is colder-than-normal but the shortage is because of bad planning and not resource scarcity. Russia’s Nordstream 2 gas pipeline is completed and will begin delivering 5 to 6 bcf/d to Germany. That won’t solve Europe’s problem this winter but it will help.

It is tempting to think that $90 is the next stop on the way to $100 oil. Then, there’s China.

Oil market sentiment seems to reflect a belief we’re back to the heady days from 2011 through mid-2014 but I believe that those days are gone for oil. Investors fled after the price collapse in late 2018 and haven’t returned. Underinvestment has been a mainstay for bullish arguments since late 2014 but scarcity has not yet materialized. Shortages because of supply-chain disruptions are not the same as resource scarcity.

Qontigo’s Olivier d’Assier who is watching the rout in East Asian equity markets, astutely noted yesterday that, “The economy isn’t back to normal…but markets have behaved as if things were back to normal.”

Inflation is a threat to the economic recovery and I believe that it has at least as much to do with high oil prices as it does the many causes discussed by economists. Similarly, Pimco’s Erin Browne said the the current energy crisis is a real inflation “risk that is being underestimated by the market right now.”

I have little doubt that today’s gas, coal and, to a lesser extent, oil shortages will fuel market sentiment and oil prices for the coming weeks and months. If oil is going to $100 as some think and others hope, inflation will soar. If that happens, I fear for our fragile economic recovery and for oil demand.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts