Art Berman Newsletter: October 2022 (2022-9)

OPEC+ cut production by 2 mmb/d.

This seems inconsistent with the chorus of analysts who have been hyperventilating about tight supply and under-investment for at least a year. If supply is so tight, why is a production cut a good idea?

“It doesn’t make sense, all things being equal, that oil prices would fall below what they were before the war because there’s a shortage.”

Anna Rathbun, chief investment officer at CBIZ Investment Advisory Services

Meanwhile Goldman Sachs and Bank of America expect Brent to average $100 in the fourth quarter of 2022 because the market is “critically tight.”

“The potential for oil prices to explode to the upside is increasing, particularly if you don’t get Iran.”

Jeff Currie, Goldman Sachs

In order to average $100, Brent would probably have to be $110 or more in November and December unless current price levels increase soon and stay high. The risk for investors is that these investment banks may just be trying to cover their bad bets on a commodity super-cycle or the revenge of the old economy made last year or early in the Ukraine War.

The problem with this thinking is that it the ignores systemic risks of higher oil prices on the global economy, and it ignores history.

Abdulaziz bin Salman’s August Comments

Saudi oil minister Abdulaziz bin Salman moved markets in August when he suggested that OPEC+ may need to make output cuts for the first time since it withheld 9.7 mmb/d in March 2020.

“OPEC+ has the commitment, flexibility and the means within the existing mechanisms of the ‘Declaration of Cooperation’ to deal with such challenges including cutting production at any time and in different forms.”

Abdulaziz bin Salman

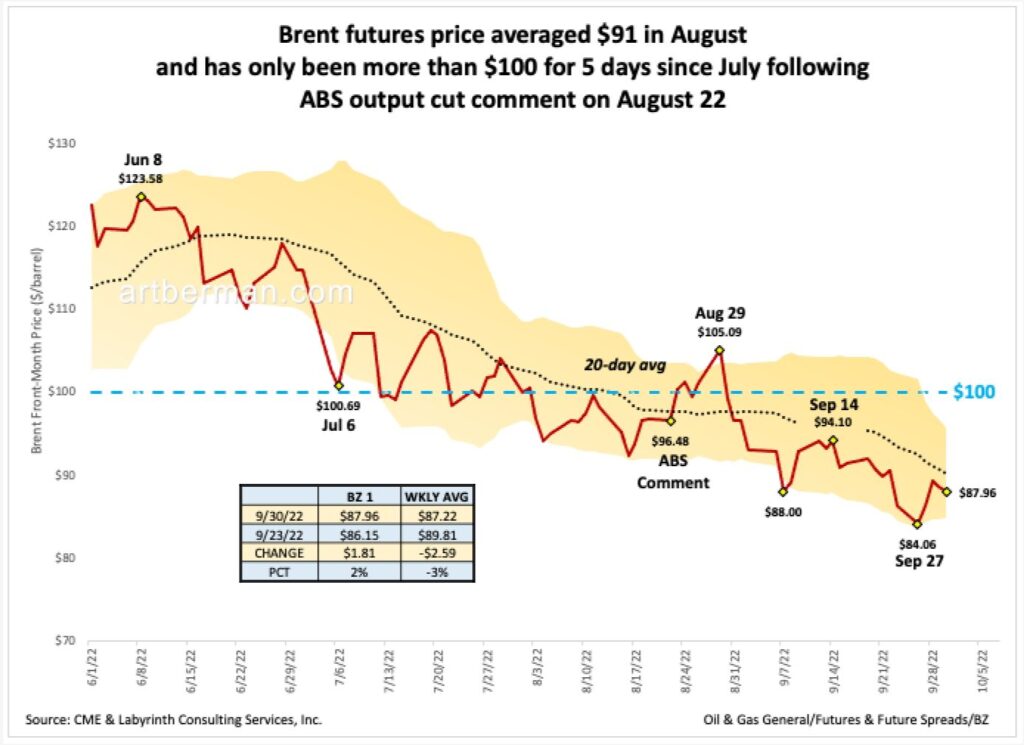

In the week following those comments, Brent futures price increased $8.61 (+9%) reaching more than $105 per barrel. No previous rally from early June through mid-August exceeded the 20-day average price (dotted black line in Figure 1). At the same time, Brent averaged $91 in August so higher prices following a November production cut are certainly possible.

Figure 1. Brent futures price averaged $91 in August and has only been more than $100 for 5 days since July following ABS output cut comment on August 23. Source: CME & Labyrinth Consulting Services, Inc.

Comparative Inventory

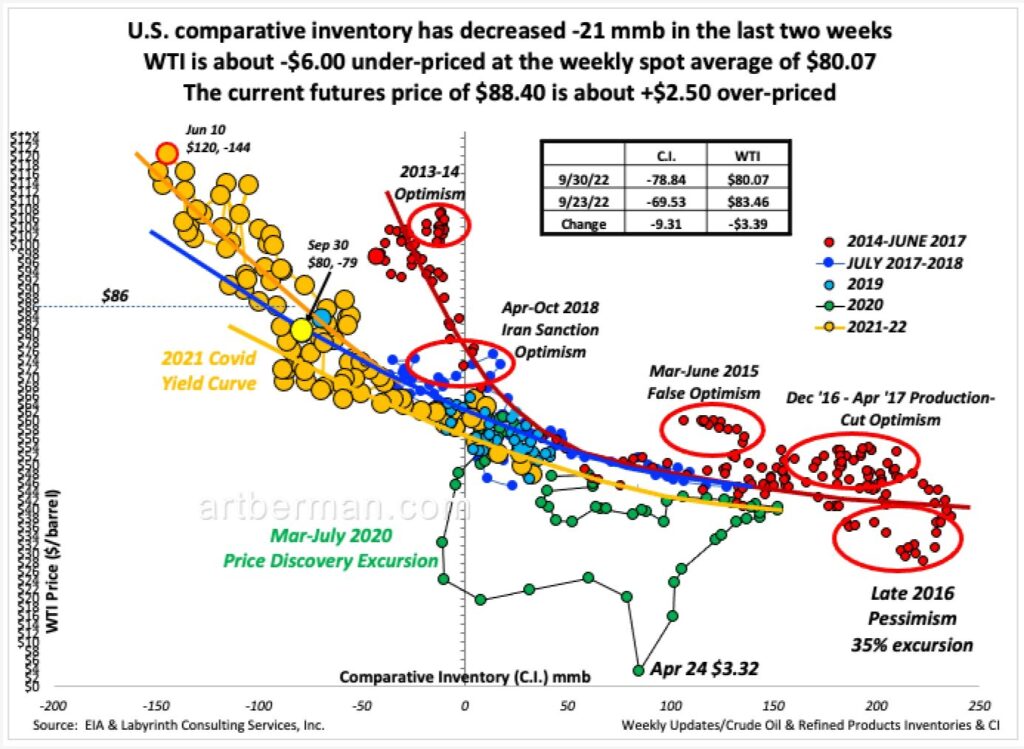

Comparative inventory is the best way to evaluate how likely $100 fourth quarter average Brent price may be. What has to happen to inventories for oil price to increase to that level?

Figure 2 shows comparative inventory for U.S. crude oil plus select refined products versus WTI spot price. The orange line is the yield curve that describes price vs volume data for 2021 and 2022.

C.I. has increased +70 mmb (+47%) since June 10 and has only decreased during three of sixteen weeks since then. That’s a strong and consistent trend.

At the same time, C.I. has decreased -21 mmb in the last two weeks. WTI is about -$6.00 under-priced at the weekly spot average of $80.07 but this morning’s (October 5) futures price of about $88 is +$2.00 over-priced.

If comparative inventory continues to decrease, it is likely that WTI would have moved higher without an OPEC+ production cut. A WTI price of $93 should translate to a Brent price of $100 so it’s reasonable that Goldman and Bank of America are right about $100 Brent.

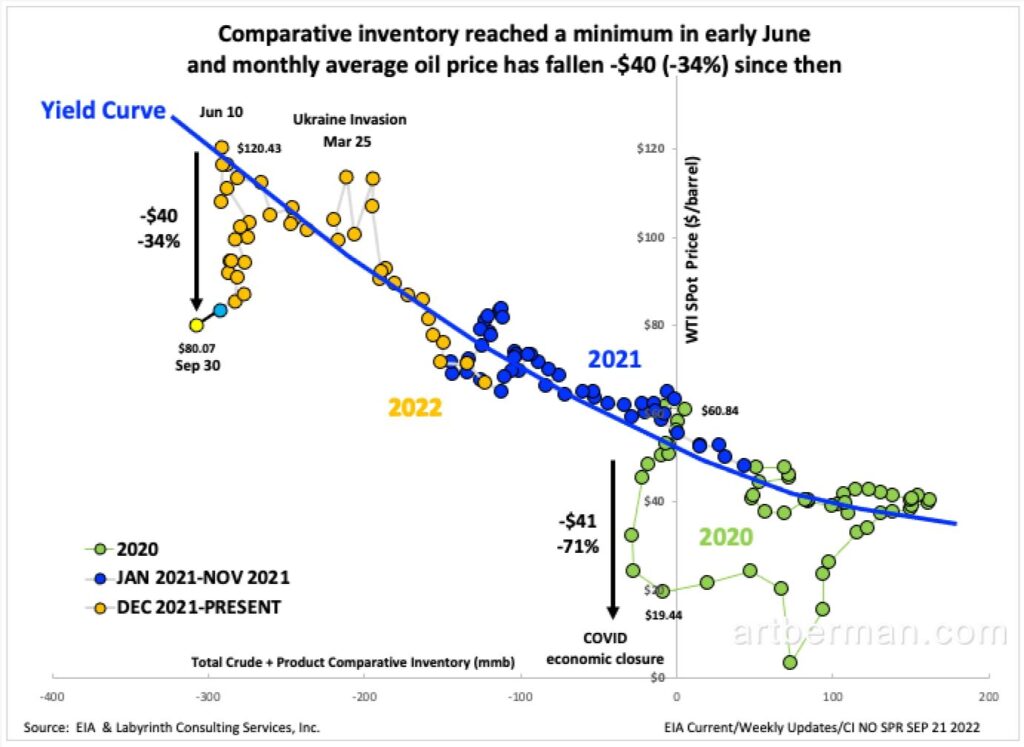

It’s fair to ask how much releases from the strategic petroleum reserve have contributed to comparative inventory.

In Figure 3, I show C.I. including the strategic petroleum reserve versus WTI spot price to fully account for the effect of releases since late 2021.

C.I. reached a minimum in June and neither moved much lower or higher until the last two weeks. Price has fallen about $40 or 34%. That pattern looks similar to what happened in the first quarter of 2020 when the COVID pandemic slowed and eventually closed the global economy. The COVID percent of decrease was greater but the comparison is still sobering.

This suggests that the market doesn’t agree with a $100 oil-price forecast despite what fundamentals indicate.

Gloomy and More Uncertain

The International Monetary Fund’s July 2022 World Economic Update was subtitled “Gloomy and More Uncertain.”

“The baseline forecast is for growth to slow from 6.1 percent last year to 3.2 percent in 2022…The risks to the outlook are overwhelmingly tilted to the downside.”

IMF

The world has experienced a series of systemic shocks that began with the global pandemic in 2020. The highest inflation rates in decades—especially in the United States and in Europe—have resulted in monetary tightening. China’s economy has slowed with COVID lockdowns and the effects of the Ukraine War have had affected supply chains and prices around the world for food and energy.

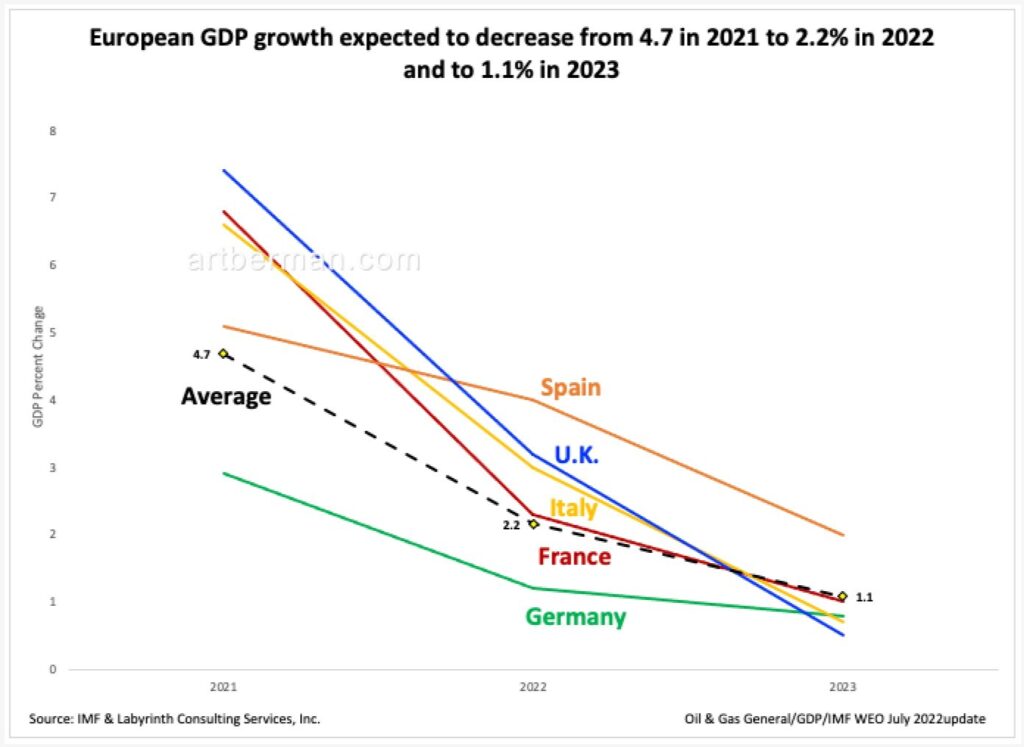

Europe is at the center of current global economic concerns. European GDP growth is projected to decrease from 4.7% in 2021 to 2.2% in 2022, and to 1.1% in 2023 (Figure 4). The U.K. and Italy are expected to have the sharpest declines.

These projections seem quite optimistic. I would be surprised to see any GDP growth in 2022.

Emerging market debt is equally troubling. The IMF notes that 60% of low income countries are either in or at high risk of government debt distress. That’s an increase from about 25% 10 years ago. As central banks raise borrowing costs, the declining value of developing countries’ currency will likely cause economic distress, reduce demand, and result in potential recession for countries with dollar-denominated debt.

This reminds me of what happened when the U.S. raised interest rates in the early 1980s under Federal Reserve Chairman Paul Volcker. Many emerging-market economies went into a depression.

Reduced economic activity and weak demand for oil led to $35 average oil prices (in 2022 dollars) from 1986 through 2002 (Figure 5). 2022 inflation is the highest since the oil shocks

An OPEC+ production cut will amplify the world’s economic problems because it will raise oil prices at least for the short term and ensure tight central bank policies.

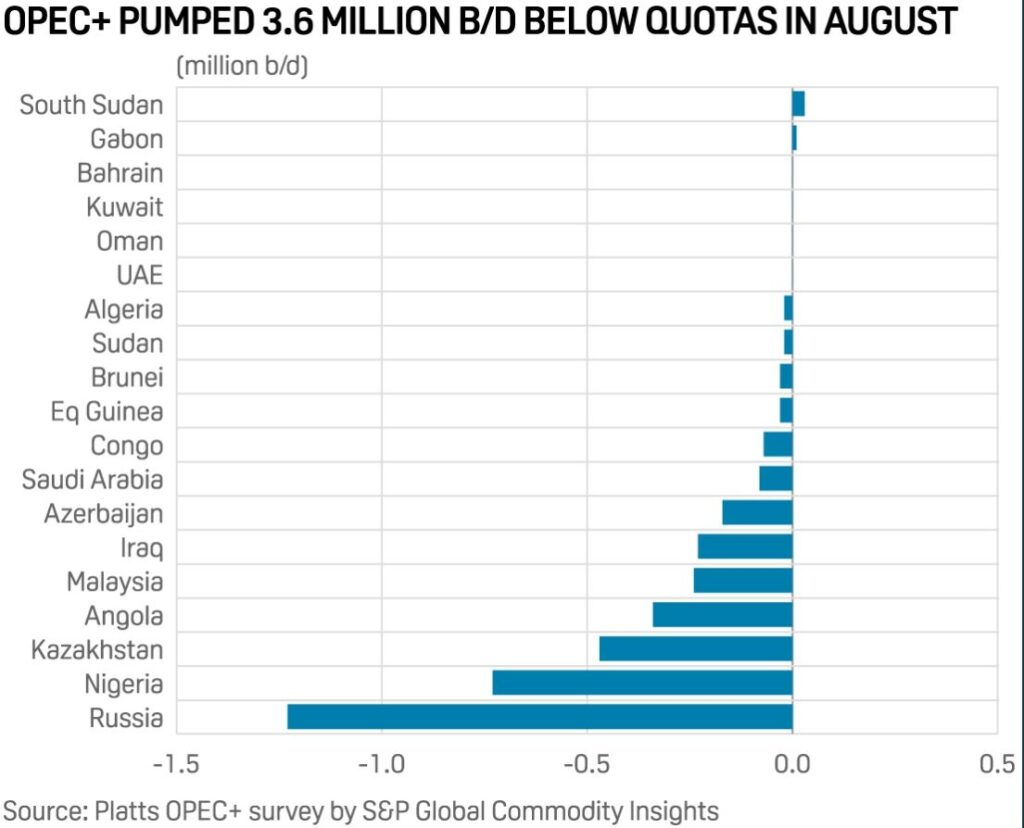

Why did OPEC cut production when it can’t deliver on its output quotas already? It pumped 3.6 million barrels per day below quotas in August (Figure 6).

OPEC+’s intent seems to be bigger profits as long as the resulting price rally lasts. The timing certainly suggests it is also meant to deliver much-needed cash to Russia. It will, moreover, poke Biden, the U.S. and NATO in the eye. This is part of the new world order and we should expect more to come.

OPEC’s record has been dismal trying to manage oil markets over the last decade.

That’s because markets cannot be managed. Oil is the largest commodity market in the world. It may be nudged by those with enough oil or money but not for very long. The opportunities for unintended consequences are great.

OPEC+ completely misjudged the market when it chose not to act in November 2014 and in March 2020. The results were disastrous.

Oil is a complex part of a complex system. Trying to play God with the world’s master resource is an arrogant fool’s errand.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts