Art Berman Newsletter: April 2020 (2020-3)

This Price Rally Will End in Tears

Oil prices have increased more than $62 over the last two weeks–the biggest price rally in history.

WTI futures price closed at -$37.63 on April 20 and today price is almost $25. Analysts are jabbering about a bull market and tight oil company share prices are about 85% higher on average than 2020 lows. It feels strange to talk about a rally when prices are only approaching the mid $20 range.

There is nothing to celebrate and everything to suspect about this rally. Some states are opening for business and that’s good but layoffs and bankruptcies are climbing and by the way, so are Coronavirus cases and deaths. I want to be optimistic but data has not yet allowed me change my views in my recent post Game Over for Oil, The Economy is Next.

This rally will end in tears like every other rally since mid-2014. That doesn’t mean there isn’t money to be made on stocks, futures or commodities but perspective is required to understand the risks.

A Supply-Constrained Market

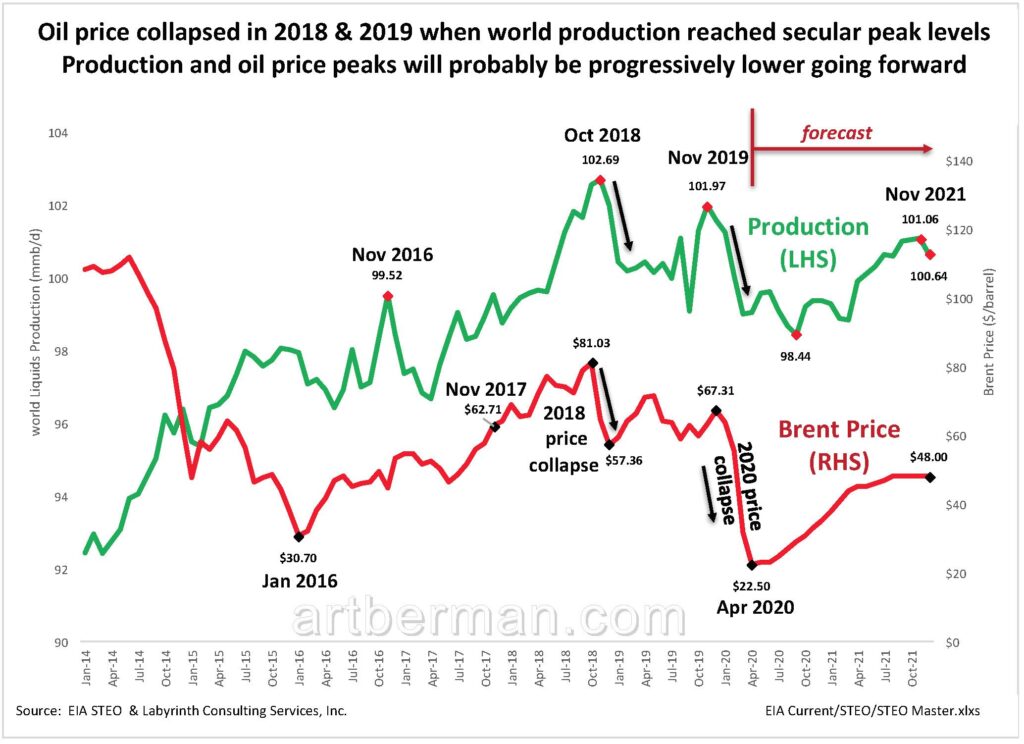

World prices collapsed in 2014-16 because of over-supply and the end of QE (quantitative easing) liquidity. In the darkest hours of early 2016 when Brent fell to almost $30 per barrel, investors began pouring money into E&P companies, especially tight oil players in the United States. Production increased although most of it was uneconomic until prices finally breached $60 in November 2017.

Source: EIA STEO and Labyrinth Consulting Services, Inc.

Most analysts believe that demand drives oil markets. I believe markets have been supply-constrained since 2008. That means that producers will continue to increase supply as long as oil price growth persists–regardless of the cost of extraction or the condition of their balance sheets—until capital is denied by credit markets.

It is, therefore, supply more than demand that drives oil markets. Even now, with demand at historic lows, all eyes are on supply—OPEC+ supply cuts and the shutting in of tight oil wells in the U.S. I’m not saying that demand doesn’t matter but markets use price to signal either more or less drilling to producers depending on supply urgency.

The 2018 price collapse was a turning point for modern oil markets. The U.S. announced withdrawal from the Iran nuclear pact in April 2018. It further disclosed its intent to put full oil-export sanctions on Iran by October. OPEC producers ramped up output anticipating Iran’s 4.5 million barrels per day to disappear.

President Trump stunned the world when he announced waivers for eight countries in early November. Brent prices promptly collapsed from $81 to $57 by late December as fourth quarter 2018 supply surplus exceeded all levels that had crushed oil prices from 2014 through 2016.

As soon as prices began to rise, the supply-constrained market re-asserted itself but the importance of this price collapse was not lost on investors. Managed money drastically reduced its bets and open interest fell to record lows. Investors fled from E&P stocks and outside capital evaporated.

Future Rallies Will Reach Lower Highs and Lower Lows

The world has been on OPEC+ life support since production cuts began in late 2016. That is why when Saudi refineries were bombed in August 2019, prices only spiked for a few days. Markets yawned because there was plenty of spare supply.

The last price rally during late 2019 needed the triple buzz of another OPEC+ cut, the U.S.-China trade deal and the assassination of Iranian General Soleimani—yet Brent prices failed to reach even $70 per barrel.

Oil prices were collapsing in January when Coronavirus began affecting Chinese demand. The disastrous Saudi-Russian decision to increase production and to cut prices in March accelerated the plunge. The spread of the virus to the rest of the world by late March and resulting economic closures sent prices to the lowest levels in modern history.

I like forecasts like Figure 1 not because I believe them but because they provide succinct summaries of present thinking about how things may develop. EIA expects oil prices to recover in 2020 and early 2021. Despite otherwise terrible oil prices, the supply-constrained model suggests that producers will once again increase oil supply to a lower secular peak in late 2021. You can figure out the rest–more price collapses to progressively lower levels followed by production increases to correspondingly lower peaks.

That is perhaps the best-case scenario.

The U.S. has never before faced shutting in such a large number of producing wells. Closing—or ‘killing”— a well is always a risky proposition. It’s not as simple as turning a valve. A special rig must be brought to the wellsite. Heavy fluid—or “mud”—is pumped into the hole to stop the flow of oil and gas. Changing the pressure regime that radically leads to great uncertainty. Then, a metal plug must be cemented into the hole to stop the flow of fluid. The mud penetrates the reservoir and may cause permanent formation damage. Metal pipe and equipment left in the hole may corrode while the well is shut in.

When the well is ready to be re-opened, another rig must be used. The cement is drilled out and the plug removed along with the heavy mud. Then, you wait and hope that the well flows again.

Bringing back shut in wells may require well treatment, re-perforation and possibly re-fracking. That will mean time and potentially considerable expense. After the last price collapse, frack crews were not available to meet demand for 12-24 months. Not only did laid off crews need to be re-assembled or newly hired but stacked equipment needed substantial refurbishment.

In perfect economic times, all of this creates uncertainty and delays. In an economic depression, there may simply not be the money or the will for it. I do not, therefore, expect October 2018 production levels to be regained for many years and possibly not ever.

Much Lower Oil Prices Inevitable

Despite the present optimism about prices, there is still no place to store oil, the world economy is a disaster and Coronavirus is not going away. That means that oil prices will probably crash again sooner than later. Many independent oil companies will declare bankruptcy in coming months.

The majors will struggle to pay dividends and will not risk shareholder revolt by acquiring zombie companies at any price. Refineries will close and supply of diesel critical to heavy transport will be increasingly uncertain. The owner of failed E&Ps and refineries will be the U.S. government.

The best case is that we will see lower production peaks followed by price collapses to progressively lower levels through the 2020s.

The worst case is that coronavirus re-closes the economy and the financial system collapses.

The most likely case is for another economic closure in which extreme measures by the U.S. Treasury prevents financial collapse. Much lower oil prices are inevitable in all scenarios once the false optimism of the present oil rally is recognized.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Great insights. Total contrast to the headline grabbing nonsense out there. Subscription is totally worth it. I will certainly recommend this to anyone interested in #OIL.

Thanks!

All the best,

Art

Thanks for your keen insight and experience, great context+detail to what we all look at so closely. Much appreciated.

Thanks for joining our website and purchasing a subscription

Thank you Art, I am new subscriber and wanted to know your latest views, taking into consideration the current spike in crude prices.

Ahassan,

The current price rally is losing momentum. The price spike that you mention is because oil has been grossly under-priced since March. The market is not wrong but rather, has been sending a strong signal to producers to shut in their wells. Success in this effort has caused markets to raise prices toward the comparative inventory yield curve. So the rally is more of a partial correction back to where prices should be.

I recommend that you subscribe to my Comparative Inventory & Oil Storage Report. It is a weekly product that goes into much more detail than my blog and twitter posts. It is only $10/week for an annual subscription: https://www.artberman.com/plans/comparative-inventory-packages/

All the best,

Art