Oil Prices and Demand are not Returning to Normal

Oil prices and demand are not returning to normal.

Prices have increased since late April because there was no place to go from a negative price but up. We are near the end of a rally whose ceiling will be in the low $40-range for the foreseeable future.

The Big Short

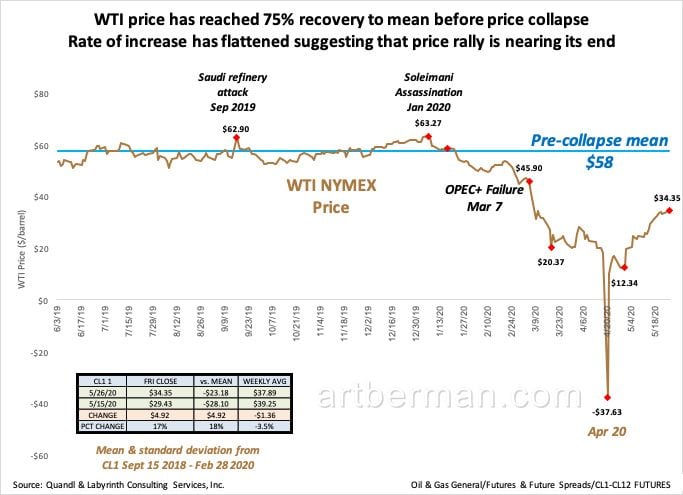

WTI price fell to -$37 on April 20 and has recovered to $34 over that last 5 weeks (Figure 1). Negative prices resulted from a one-day short squeeze. The May contract was expiring & no oil storage was available. Those who waited to sell their contracts had to pay those who held storage to take physical delivery of the oil.

Prices are approaching 75% recovery to the $58 mean before the price collapse in March. That calculation starts at $12.34 since the negative price was an anomaly and gives a false measure of the recovery.

The rate of price increase has flattened and price has fallen more than $1.50 from yesterday’s settle of $34.35 at this writing. The rally is nearing its end.

Rate of increase has flattened suggesting that price rally is nearing its end.

Source: Quandl and Labyrinth Consulting Services, Inc.

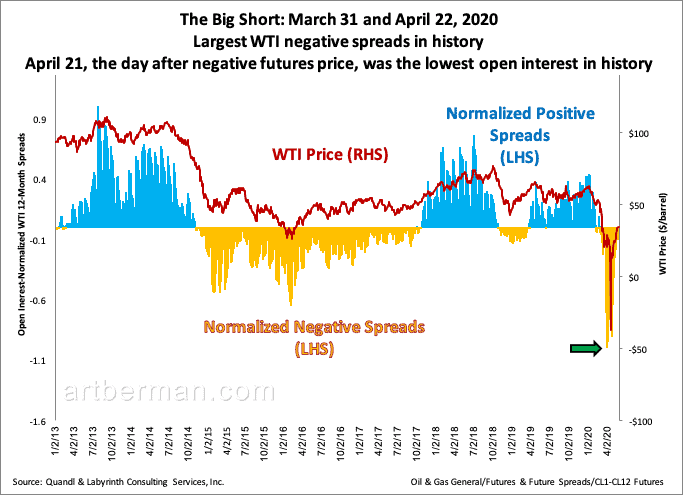

Negative prices were the headline in April but the negative spread was the story.

WTI 12-month spreads reached the most negative levels in history between March 31 and April 21 (Figure 2). Shorting oil after the OPEC+ meeting disaster in early March was some of the easiest free money ever made. The short-covering rally that followed negative oil prices was a classic no-brainer, not to be mistaken with something meaningful. Been down so long, it looks like up to me.

Largest WTI negative spreads in history

April 21, the day after negative futures price, was the lowest open interest in history.

Source: Quandl and Labyrinth Consulting Services, Inc.

There’s been a lot of discussion about negative oil prices and whether there was some sort of manipulation that led to it. Investors noticed.

WTI open interest the day after negative prices was the lowest in history. Weak open interest and trading volumes have characterized the futures market since then. Investors are voting no confidence with their feet. I hope the Chicago Mercantile Exchange is paying attention.

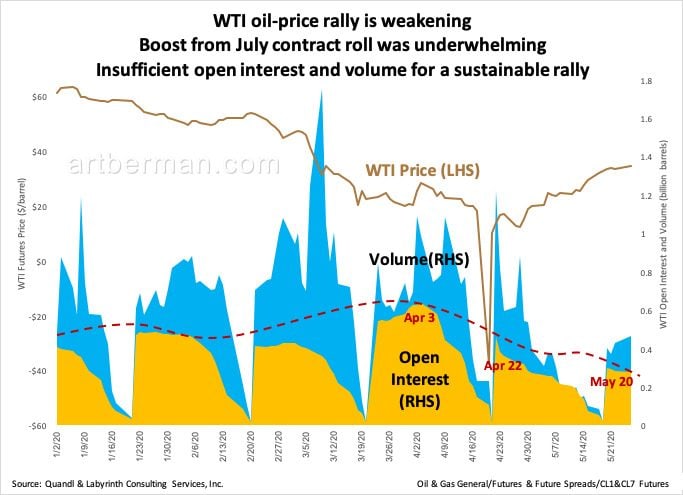

Open interest rises and falls with every contract expiration. Open interest in 2020 peaked around April 3 (Figure 2). The June contract roll on April 22 was characterized by a lower net interest-bounce than in the previous month. The boost from the July roll on May 20 was even lower. This combined with lower trading volumes, and the flattening of prices are evidence that this price rally is almost over.

Boost from July contract roll was underwhelming.

Insufficient open interest and volume for a sustainable rally.

Source: Quandl and Labyrinth Consulting Services, Inc.

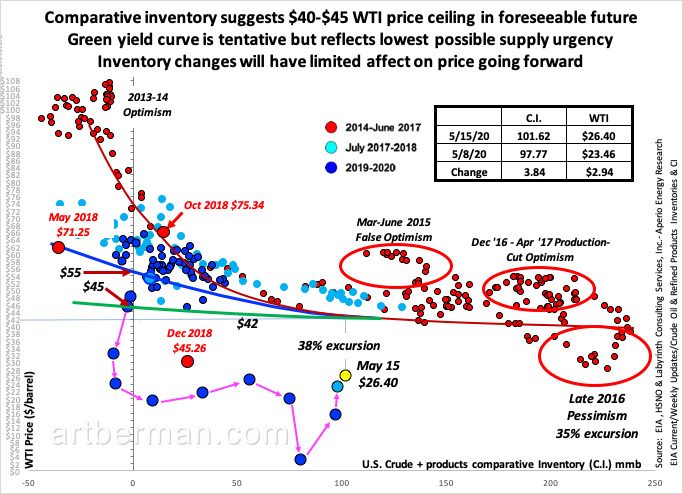

Comparative Inventory is the Key to Price Formation

Comparative inventory (C.I.) is the key to understanding price formation. It is the best way to identify price trends and to anticipate future price movements.

C.I. is the difference between current storage levels of crude oil plus a select group of refined products, and their 5-year average for the same weekly time period. Because it is a year-over-year calculation, it normalizes seasonal variations in production, consumption and refinery utilization.

The yield curve that results from cross plotting C.I. vs oil price offers a structure for organizing seemingly random variations in oil prices. The yield curve has provided a useful solution for the complex market forces that determine price formation since inventory data was first published by the EIA in the 1990s.

Supply drives oil markets and price is the signal to producers to increase or decrease drilling to ensure adequate supply. Demand matters but supply can be adjusted relatively quickly. We have seen that in recent weeks as producers have shut in wells in response to extraordinarily low oil prices. The storage crisis that most analysts believed was certain did not happen. Markets are not always right but they are ruthlessly efficient.

The present yield curve shown in green below in Figure 3 is tentative since prices are still in considerable flux. It assumes the lowest possible supply urgency based on the lowest price signals the market has ever sent. Because the yield curve is nearly flat, price will not change much with inventory fluctuations. That is why prices fell so far, so quickly. It is also why they are unlikely to rise much farther.

WTI will probably not exceed $40-$45 per barrel until markets re-price oil upward because of an increased sense of supply urgency. As long as prices are below the yield curve, there is little potential for a return to pre-collapse prices in the mid-$50 range.

Green yield curve is tentative but reflects lowest possible supply urgency.

Inventory changes will have limited affect on price going forward.

Source: EIA and Labyrinth Consulting Services, Inc.

An L-Shaped Recovery

I don’t believe that most people have come to terms with the reality of oil markets going forward. The Covid-19 economic shut-down was not a switch that was turned off and now is turned on as economies begin to open.

Almost 40 million Americans have filed unemployment claims since the end of February. The Chairman of the U.S. Federal Reserve Board expects that to increase and for GDP (gross domestic product) to fall as much as 30% in the second quarter of 2020. Jobs and economic output will not return quickly. A profound re-structuring of the economy must happen first.

U.S. unemployment benefits will expire in July unless Congress extends the payment period and this will mean greater hardship and less spending.

“Seventy-five percent of Americans have seen their income cut by at least 25%. These are the seeds of social unrest.”

Danielle DiMartino Booth, Quill Intelligence

DiMartino Booth’s comment seems exaggerated but it notionally reflects the reality that recovery optimists appear to ignore; namely, that even people with jobs probably aren’t making the same amount as they were before the Covid-19 shutdowns. Only about 40% of Americans have enough savings to cover 3 months of living expenses.

U.S. oil consumption has improved since mid-April but remains about 20% less than normal for this time of year. Most of that increase is from gasoline use and that is skewed by the fact that almost no one is using public transportation.

The harsh truth is that if tens of millions of people have no jobs to go to, gasoline consumption cannot recover to early 2020 levels. The latest Apple mobility data indicates that global driving is about 32% less than the early 2020 baseline.

The world has been on OPEC+ life support since production cuts began in late 2016. That is why when Saudi refineries were bombed in August 2019, prices only spiked for a few days. Markets yawned because there was plenty of spare supply.

Now, OPEC+ has had to cut almost 10 mmb/d and prices have barely recovered into the $30 range. Markets know that the world has plenty of oil supply and that any talk of a balanced market or physical shortages are completely artificial.

With somewhat higher oil prices, U.S. tight oil producers are talking about reactivating shut in wells. Russian leaders are looking forward to the July end of the latest OPEC+ production cut agreement. Floating storage is estimated at around 200 mmb and term structure no longer justifies the cost of storage.

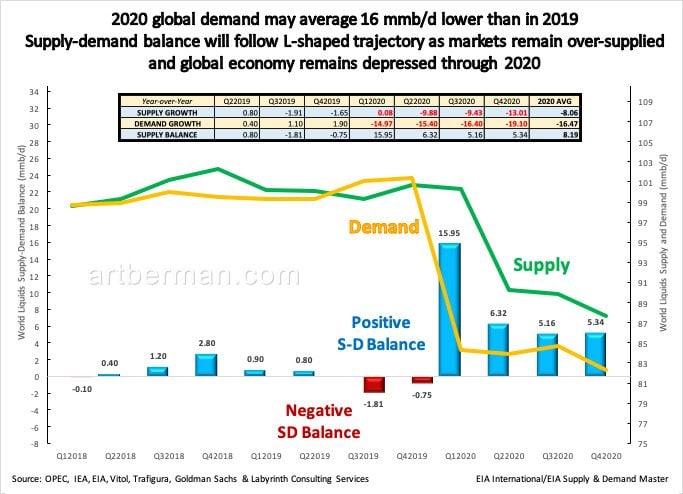

The International Energy Agency and OPEC expect 2020 world demand to be about 9 mmb/d less than in 2019. Those forecasts feature a V-shaped demand recovery that strikes me as either naively optimistic or wantonly patronizing to its funders’ expectations.

Neither agency forecasts supply but EIA data indicates supply will average about 5.5 mmb/d less than in 2020. It at least suggests more of a U-shaped supply recovery.

Considering all of the facts and reasonable extrapolations summarized in this post, I expect an L-shaped recovery in oil supply and demand (Figure 4). This is more of a thought experiment than a forecast because uncertainty is extreme. The supply and demand lines in the figure are meant to be probabilistic trend lines. I expect a most-likely case for 2020 in which supply will fall by about 8 mmb/d and demand, about 16 mmb/d.

Whether you accept my hypothesis or prefer one of the international agencies’, the differences are only a question of degree. The world will be over-supplied with oil in 2020.

Producers will be forced to cut production because of low price and low demand

Supply-demand balance will follow L-shaped trajectory as markets remain over-supplied

Many of you have written saying that my observations and data are compelling but that you are more optimistic than I am.

I appreciate those comments and will close this post by saying that science and scientific analysis are about neither optimism nor pessimism. Science is founded on observation and description. Patterns are identified and questions are asked to provoke a hypothesis that can be tested with further observation and description.

People naturally want to know what caused things to be the way they are. That is not, however, the aim of science. Science seeks to anticipate the most probable future configuration of things based on patterns identified and tested in the present. That may disappoint some of you whose conception of science is from television or movies.

You have told me that the patterns that I observe and describe seem right to you. You just don’t like the consequences of my explanations.

We are witnessing a momentous transformation of the world economy. Covid-19 was the trigger but the forces it is disrupting have been developing for a long time. Chief among those is the debt undertaken to perpetuate economic growth when common sense indicated it should have slowed or ended decades ago.

Energy is the economy and oil is the most important part of energy today. It is not surprising that oil should be the proverbial canary in the coal mine for the rest of the economy.

Oil prices are not returning to normal. Neither is the economy.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Today, similar to every day since mid-April, CME Group, the world’s largest derivatives exchange, lists WCS (Western Canada Select) and Edmonton Sweet Synthetic (NE2) at negative numbers far into next year. There are NO OPEN CONTRACTS, or in fact, any interest shown at all. This suggests that Alberta’s Tar Sands have no future at all. I have been stating this for years now.

In what business fantasy world does increasing the supply of high-cost, lowest quality bitumen, in a market already flooded with low-cost, high-quality crude, lead to increased demand and higher prices for Alberta bitumen?

Nobody in the world considers Canada to be a reliable source of energy as a mere wink from Houston will lead to immediate cutoff of all overseas supplies from Canada. Make no mistake, the US will continue to dominate all sources of crude in the Americas. The use of the term ‘landlocked’ is remarkably stupid as it merely means Canada has the longest undefended border with the world’s largest energy market. Alberta’s crude flows without the presence of two carrier battle fleets, expensive shipment through the Southern Ocean or Atlantic hurricanes, or threats from terror, rebellion, or war of any kind.

The Saudis have paid for refinery construction all the way from Pakistan to China expressly to secure reliable demand for their crude. The marketing plan for Trans Mountain has Jim Kenney, Andrew Scheer, and Stephen Harper pushing a battered shopping cart to the end of the pier. They stand there dirty and desperate with a large cardboard sign reading, ‘Will ship crappy bitumen anywhere for food’.

Richard,

I don’t know much about WCS or Edmonton futures but heavy oil from Canada is crucial to U.S. refiners in order to blend with lighter U.S. grades. Also disagree that no one considers Canada aa reliable source of energy. Canada has been the principal source of U.S. imported oil for a long time.

All the best,

Art

Thank you Art for your great work, many traders now believe that Oil will retrace to 40 in June – Aug period and continue higher to 45 towards end of 2020. Based on that they link energy names like chevron , BP,…. etc to much higher upside from current share prices. Do you agree with that view? Another question where I can find a reliable chart that shows oil prices and traded volumes.

$40-$45 is the range that comparative inventory suggest for oil pricing today based on stock levels. Chevron has the best stock price performance and BP has a lot of debt that concerns me.

I can make a chart of volume vs oil price for you. Here is an example:

Please contact my business manager and he will discuss the specifics: [email protected]

All the best,

Art

It is not the ‘price’, but rather the little remaining physical oil available in the ground – what matters!

The transition of the ownership of Iraq’s oil into the hands of armed militias – is smoothly-ongoing since the US has invaded the country in 2003.

That process is now almost achieved.

One may think the unrest in Minneapolis in the last few days was a substantial and scary.

Watch the video below – it demonstrates how the Militias are conditioning the population to their incoming, unmasked, undisguised control of 4.5+ million barrel p/d of gold-grade oil – by firing hills of live ammunition in the air, almost randomly – raining on the city of Basrah – bullets…

The reason behind the now-regular event, they claim, is that – they are fighting each other!

The end result is that the population are made scared to death, more than willing to relinquish all their national oil, exchanging it with their lives – if they manage, no matter how that means living in an Energy-less life, back into the pre-industrial age.

When the Militias will finally get the entire oil exportation in their hands, will price charts go up?

No. The 4.5+ million barrel will be taken off of all charts, as they’ll be traded smuggled by the Energy black market – priceless.

They may appear on formal charts coming from Fracking, from the UK, Alaska or from newly discovered fields.

I invite Art to devise a novel calculus for the energy market that tries quantifying these new social-Darwinism dynamics and their impact on the global hydrocarbons market in the coming decades.

When I first traveled to Kuwait as a boy, it took my father a little more than an hour to drive the family from Basrah to the centre of Kuwait!

The oil-rich Abadan in Iran is few tens of kilometres from my grandfather’s house in Basrah, too.

OPEC turning an OPEM[ilitias] – is in-sight!

https://www.youtube.com/watch?v=l5lEYPG06LU

The world is a great stage full of heroes and villains. It has never been different.

I am a scientist who observes who likes to try to explain things. I am not an activist.

I’m not clear about what you are asking of me but think is more than what I do.

All the best,

Art

Thank Art for your quick response

Interesting analysis Art. Thanks for the insight

Good to hear from you, Marc.

All the best,

Art

..It is all about oil

Syrian oil being forcefully put into the hands of the international black energy market…

Local observers fear that soon nobody will be able to tell if oil supplies coming through the black energy market are bigger than those coming into the audited market – which makes any report on Energy, no matter who is releasing it – not worth the ink written with.

And who blames them after watching the video clip below;

(Sorry, the clip is not English-narrated but one can have an idea from the images – lakes and lakes of crude oil are traded at the gun point – transported outside the country mixed with blood, while the media is claiming demand for oil is crashing!)

https://www.youtube.com/watch?v=MIewVwEc3OE

I don’t understand the basis of your comment but I assure you that the volume of oil produced in Syria is insufficient to affect world oil prices.

All the best,

Art

Do you think current prices could threaten the social/political stability of major oil exporting countries (eg. Saudi Arabia, UAE, Russia etc). Would political upheaval in any of these countries have much affect on oil prices? I looks like based on your article that there is a huge oversupply in any event.

David,

I see considerable potential for unrest because of low oil prices and economic desperation from the global depression. It’s hard to know where this may happen but geopolitical stress would result in higher oil prices exacerbating economic hardship for many in the world.

Best,

Art

[…] Oil Prices and Demand are not Returning to Normal May 27, 2020 […]

Not pleasant, but unfortunately an honest synthesis of the evidence we have. Admirable job.

Agree.

Art