Why Is Anyone Celebrating $33 Oil?

Oil prices have recovered to almost $33 and already some analysts are declaring this a “relentless oil price rally.” Reality check: that is $3 more than the WTI weekly average at the bottom of the last price crash in 2016.

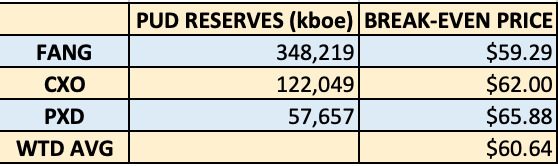

Permian basin independents Concho, Diamondback and Pioneer need about $60 to break even according to their recent SEC 10-K filings. Hedging doesn’t offer anything more than about $37 two years out.

I don’t know about you but I’m going to leave the champagne in the refrigerator for awhile.

Some of the current optimism comes from a slightly less pessimistic forecast for world demand destruction by the International Energy Agency than they had a month ago. Instead of demand growth falling 9.3 mmb/d in 2020, IEA now thinks it may only fall 8.6 mmb/d.

I will try to curb my enthusiasm.

For IEA’s forecast to happen, global demand must continue to rise from ashes and supply must continue to drop. That’s a pretty tall order for a world that is locked in an economic depression that will almost certainly last beyond 2020.

“We are in an outright depression & won’t recover for a long time…Those who expect recovery this year are delusional because many of the job losses will be permanent & probably half of small businesses will fail.”

Dave Rosenberg, Chief Economist & Strategist, Rosenberg Research & Associates, Toronto

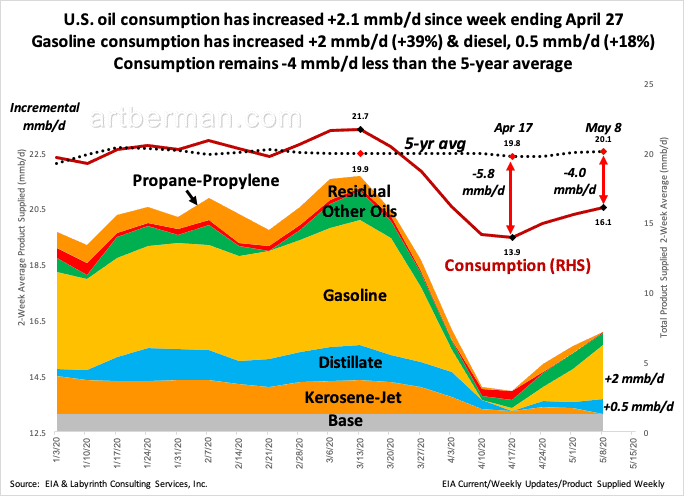

U.S. Consumption is Recovering

Now the good news : U.S. consumption has increased 2.1 mmb/d from its lowest level in mid-April (Figure 1). Most of the increase is in gasoline consumption. Activity is increasing and people are driving more. Diesel use is also rising and that’s encouraging because it suggests that more goods that require truck, train or ship transport are being ordered. Kerosene-jet fuel use, however, has never been lower than the week ending May 8.

Source: EIA and Labyrinth Consulting Services, Inc.

I have to wonder what the increased gasoline is being used for with so many stores and businesses closed. My guess is that people are using their cars to go everywhere. Buses, trains and subways are operating on a limited basis and who wants to take the risk of getting sick on public transportation?

Diesel use has increased half as much as gasoline as a percent and that suggests that half of the gasoline increase is just people avoiding public transport and not really a sign of an exuberant economic re-opening.

The bad news about the consumption increase is that it’s still 4 mmb/d (20%) less than the 5-year average for the first week in May.

And that is the problem for the economic recovery. Unemployment is probably 20% when the official 15% is adjusted for those not looking for work or who just haven’t filed a claim. The economy may be officially open but the number of people losing their jobs is increasing. We’re operating on an 80% economy and that may seem optimistic by the end of the year.

Why Is Anyone Celebrating $33 Oil?

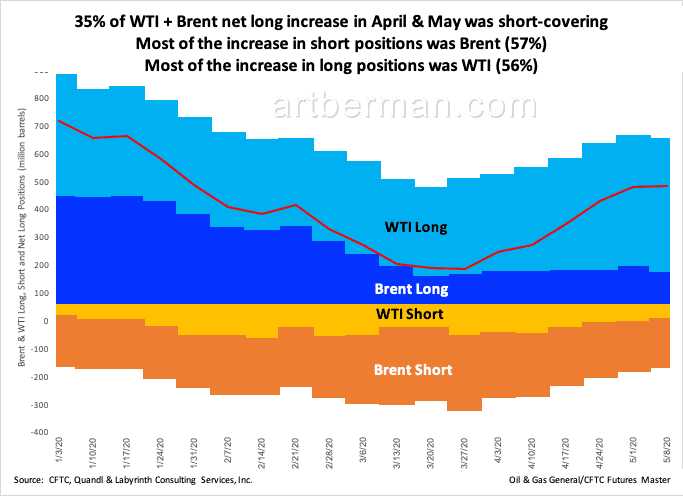

Whenever a rally’s growth is strong regardless of its starting point, it tells you that the market was short—really short. Brent and WTI net long positions confirm that.

Thirty-five percent of WTI + Brent net long increase in April and May was from short-covering (Figure 2). Brent accounted for most of the increase in short positions since late March and most of the increase in long positions was from WTI.

Why are markets more pessimistic about Brent price upside than they are about WTI? Some of it is probably because WTI prices fell so much lower than Brent in April.

It is worth remembering that OPEC’s basket price is less than $25 at this writing.

Source: CFTC, Quandl and Labyrinth Consulting Services, Inc.

The main reason for celebrating $33 WTI is because that price is almost three times higher than the $11 average futures price in the second half of April. The comparative inventory yield curve indicates that WTI should be priced at about $42 based on last week’s oil storage volumes so there’s room for the rally to continue.

But to what end? The top independent producers in the Permian basin need more than $60 wellhead price to break even (Table 1). This is based on their own future cash flow statements in their latest 10-K filings with the Securities and Exchange Commission.

Source: Company 10-K filings for 2019 and Labyrinth Consulting Services, Inc.

Analysts can use all the sleight-of-hand available to show that somehow these companies are cash flow positive on a point-forward basis. The data in Table 1, however, is the reality that they told the U.S. government in February.

Anyone who is enthusiastic about $33 oil needs to think about that.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Thank you very much for your article. Just wonder what you think about OXY. It’s also a major player in Permian basin. To my knowledge, OXY has a lower break-even price compared with FANG, CXO and PXD.

Fuying,

I haven’t done a detailed evaluation of the Permian basin plays for awhile but I doubt OXY’s break-even is lower than the others you mentioned. Everyone is losing money these days anyway.

Best,

Art

Since 2003, Iraq is in chronic grid power shortage.

Most of the 17 GWh it generates is consumed by the vast oil extraction and export operation, which leaves the population in the dark, especially during the 9 months-long extremely harsh summer. Life in Iraq today is mostly a pre-Edison age-style.

Some estimate the gap of shortage is of no less than 50 GWh.

There are billions of other humans that have never enjoyed a grid power, since Edison and still.

Demand for Energy never drops down. What might go down is figures of poor Energy Audits.

Prices are man-made. Energy is a property of Physics,

“Any move by an energy system to re-organise itself for less energy consumption will cause it consuming even more energy than if it abandoned that re-organisation”.

Re-tooling the industrial base for ventilators, producing and broadcasting more news briefs and campaigns, masks for the entire population, vaccines, stay-home enforcement, etc – will consume energy far exceeds all the energy saved by grounding the airline fleets, restricted driving, etc.

This pandemic might be an opportunity to gravitate nations toward – who next joins Iraq back into the pre-industrial age, and then stays there – another Iraq.