Oil Storage-Comparative Inventory Report – Example

WTI will average less than $20 in May

WTI remains grossly under-priced. That sends the strongest possible signal to producers to shut in their wells. Oil prices will remain depressed until there is evidence for lower production levels in the near term. Do not expect WTI to reach $40/barrel any time soon and probably not in 2020 on any sustainable basis.

The world is experiencing an historic decrease in demand from virus-related closure of economic activity. Markets, however, always focus on supply. Price is the lever that raises or lowers production. As long as supply and demand are in relative balance, the demand matters little to the market.

Figure 1 shows the comparative inventory-WTI yield curve with the latest data point in yellow marked April 24. The magenta arrows indicate the descent of oil prices since the early March failure of OPEC+ to cut production and the subsequent Covid-19 economic closure. The green line “yield curve” suggests that the marginal barrel price is $45 at the 5-year average

Source: EIA and Labyrinth Consulting Services, Inc.

The flat trajectory of the yield curve means that large changes in storage volumes will result in relatively small changes in price. That is why prices fell so quickly to such low levels in March: markets enforced a new yield curve that was lower and flatter than the previous blue trend.

The correct price for WTI based on comparative inventory is about $44–simply follow the vertical line up from the yellow data point to the yield curve, and trace a horizontal line to the y-axis to read this value.

The market is shorting oil price in a huge way. It’s message may be summarized as follows:

“There is so much supply relative to demand that I will only pay you $10 for what we both know is worth $44. Take it or leave it. Come back and see me when supply is much lower and we’ll discuss a somewhat higher price then.”

I expect prices to move upward toward and possibly into the $20 range in May.

Filling storage will result in massive well shut-ins

The likelihood that U.S. storage will reach capacity is what will force producers to shut in their wells. Despite misleading headlines in the press, storage is not full but all space for storage is leased. For many companies, that means that there is no place to put their oil if they can’t sell it. Larger companies either have their own refineries or have long-term contracts with refiners and are, therefore, less constrained.

U.S. storage will not reach capacity for about 3 months at current fill rates but Cushing is another story; it will probably be full in another 3 weeks (Figure 2). Because Cushing is the pricing point, WTI will be especially sensitive to fill levels.

Source: EIA and Labyrinth Consulting Services, Inc.

Despite WTI breaching $20 briefly today (Friday, May 1), that was a Friday futures or sentiment-based anomaly. Until markets see storage trends level off or decline, prices should stay below $20 on a weekly average basis. It is worth noting that fill rates have decreased over the last 4 weeks.

Companies are already shutting in production. ExxonMobil, Chevron and ConocoPhillips plan to cut U.S. production by 660 kb/d by the end of June. Smaller companies without the same access to pipelines and refineries will be cutting more severely. I expect that April production will be 15-20% less than in March and that total U.S. production will fall to less than 6 mmb/d by the end of June (Figure 3).

Source: Baker Hughes, EIA DPR, Drilling Info and Labyrinth Consulting Services, Inc.

Consumption and Refinery Intakes are Crashing

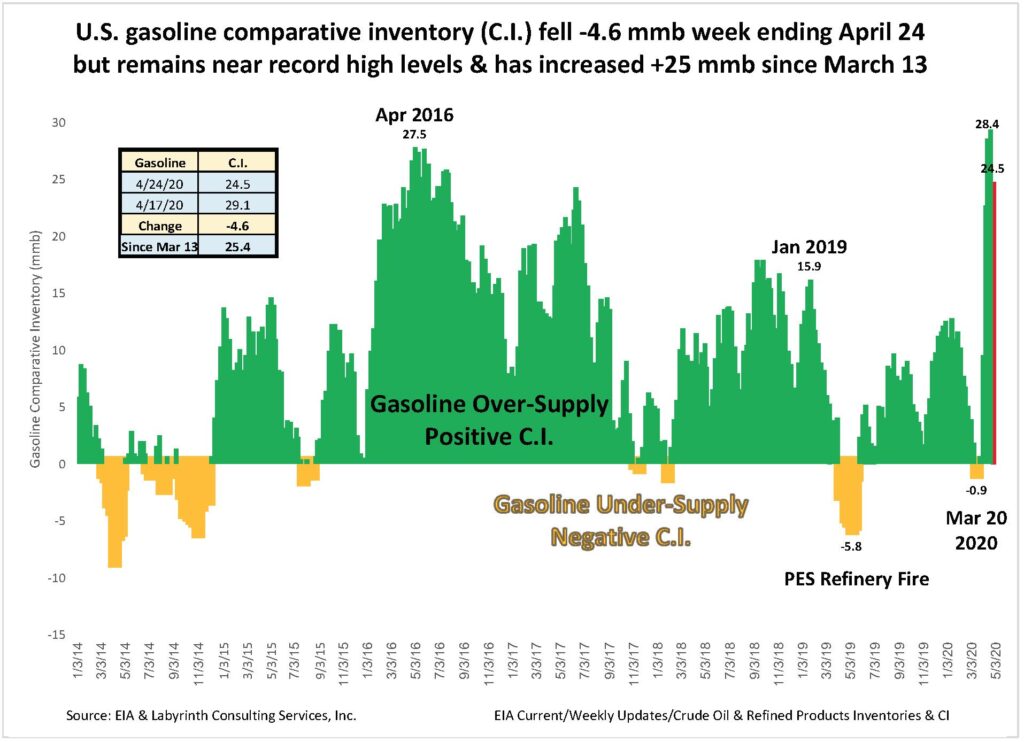

Investors got excited that gasoline stocks and comparative inventory fell -4.6 mmb this week (Figure 4). That does not change the fact that current C.I. is near record levels or that it has increased 25 mmb since March 13.

Source: EIA and Labyrinth Consulting Services, Inc.

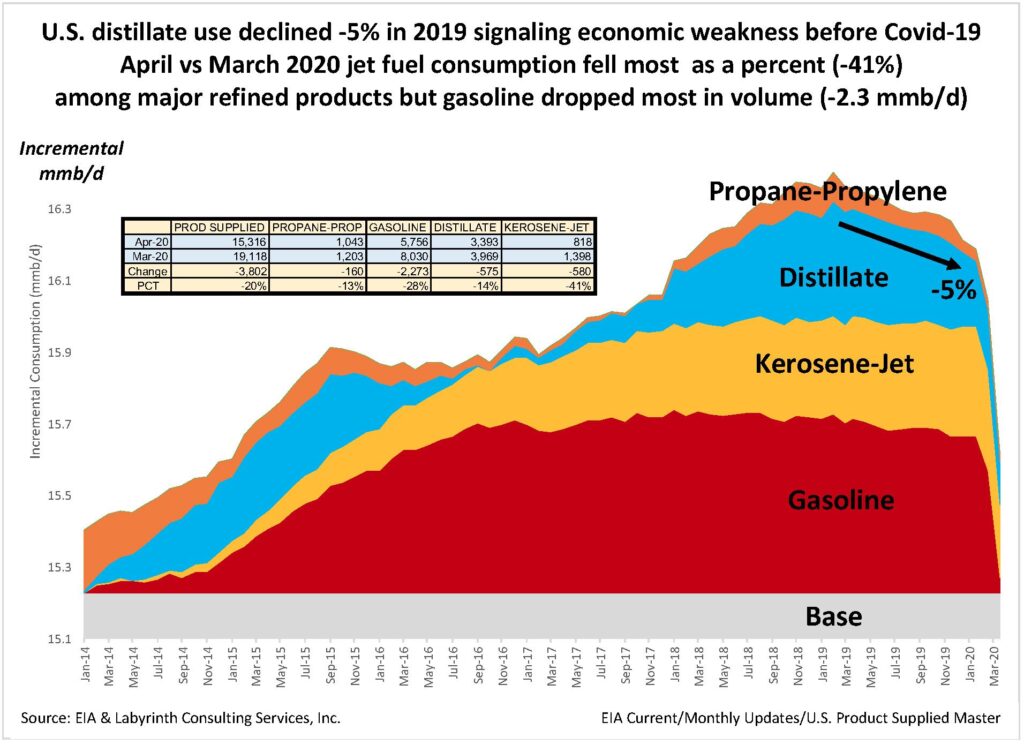

Nor does it affect the larger effect of decreased refined product demand. Overall consumption decreased 20% (-3.8 mmb/d) in April (Figure 5). Jet fuel use declined the most as a percent (-41%) but gasoline fell the most in volume at -2.3 mmb/d.

Source: EIA and Labyrinth Consulting Services, Inc.

The 5% decrease in distillate consumption in 2019 is particularly troubling. Distillate or diesel use is not ordinarily affected by price the way that gasoline is. That is because most gasoline use is personal and, therefore, somewhat discretionary. Diesel is used for heavy transportation–ships, trucks and trains–and when it declines it is usually because of decreased orders for durable goods. The implication is clearly economic weakness and this was occurring before the virus-related economic shutdown.

The key factors affecting this week’s storage report were higher consumption and refinery intakes (Figure 6). Consumption rose 1.7 mmb/d (11.6 mmb/week) and refinery intakes were 0.3 mmb/d (2.3 mmb/week) higher.

Source: EIA and Labyrinth Consulting Services, Inc.

Although that is positive, it is against the bleak backdrop of sharply lower consumption and refinery intakes. Estimated April U.S. petroleum consumption was 4 mmb/d (-21%) less than in March and 4.8 mmb/d (23%) lower year-over-year (Figure 7).

and -4.8 mmb/d (-23%) lower year-over-year.

Source: EIA and Labyrinth Consulting Services, Inc.

Similarly, refinery intakes were 3.4 mmb/d lower than the week ending March 20 and -3.7 mmb/d lower than a year ago (Figure 8).

and -4.8 mmb/d (-23%) lower year-over-year.

Source: EIA and Labyrinth Consulting Services, Inc.

The Worst is Not Over

After WTI’s descent into negative prices, WTI’s recovery to nearly $20 seems to offer a sense of relative calm.I see nothing calming in the data.

Oil traders are engaged in price discovery as they always and appropriately are. They will continue until they cannot find a counter-party on the other side of the trade and then, they will “follow the tape” in the opposite direction.

As Cushing continues to fill and approaches capacity, WTI price will probably crash back to $10 or lower. I hope that I am wrong.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts