The Misunderstanding of Oil Underinvestment

Analysts are sounding the alarm that oil industry underinvestment is responsible for higher oil prices. Their concern is based on a misunderstanding of how the oil business works.

In fact, the level of oil investment over the last several years has been exactly right based on market price and investor expectations. The oil business is not a service industry nor is it part of the Consumer Protection Agency.

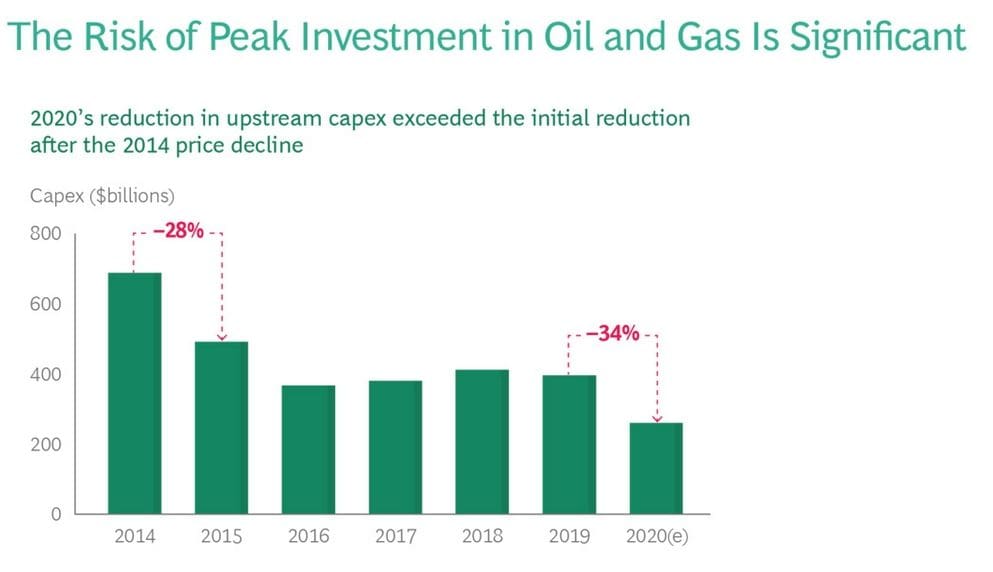

The logic behind the case for underinvestment is as follows: because industry capex fell after 2014, and fell again in 2020, and because there is now a supply shortage, industry is to blame for underinvesting (Figure 1).

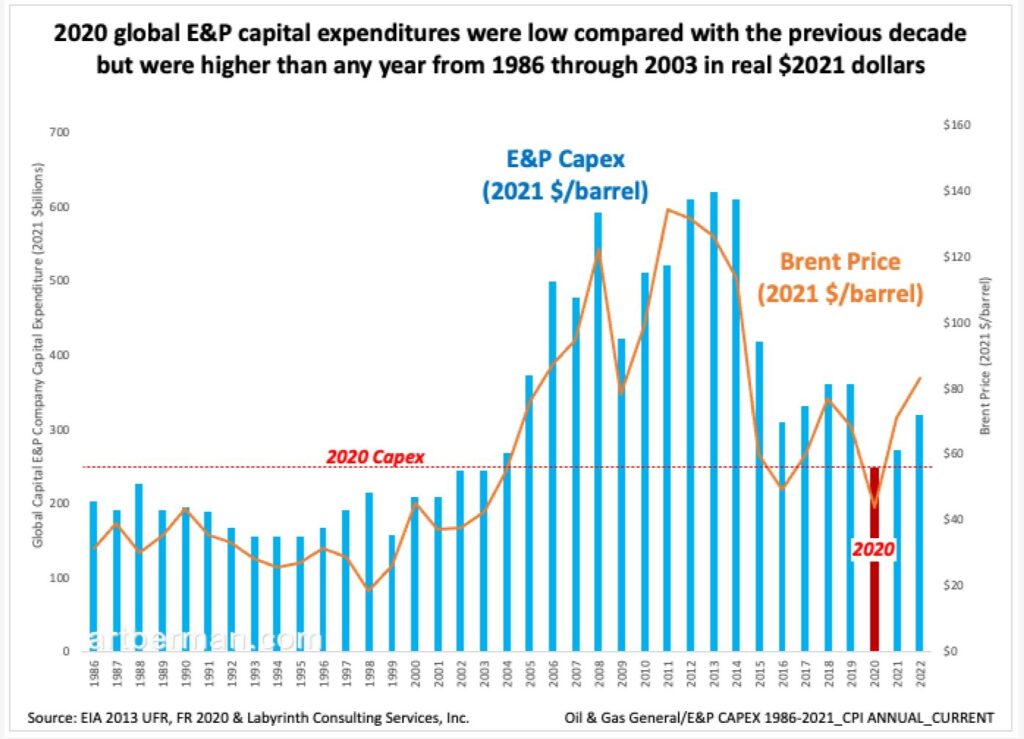

This argument fails to acknowledge that 2006 through 2014 was the longest period of high prices and capital expenditures in the history of oil markets (Figure 2). Over-supply and collapse of prices after 2014 did not justify as much capex as before, nor was there any reason to expect higher prices until very recently—remember ‘lower for longer’? To compare the last few years to 2014 results in a distorted perspective of the present.

If an oil company decides to drill a well today, most of its reserves will be produced at prices two to five years from now. No one knows what those may be. That is why oil is a risky business. Periods of major capital investment are based reasonable expectation of multi-year high oil prices and that has only happened twice during the last fifty years.

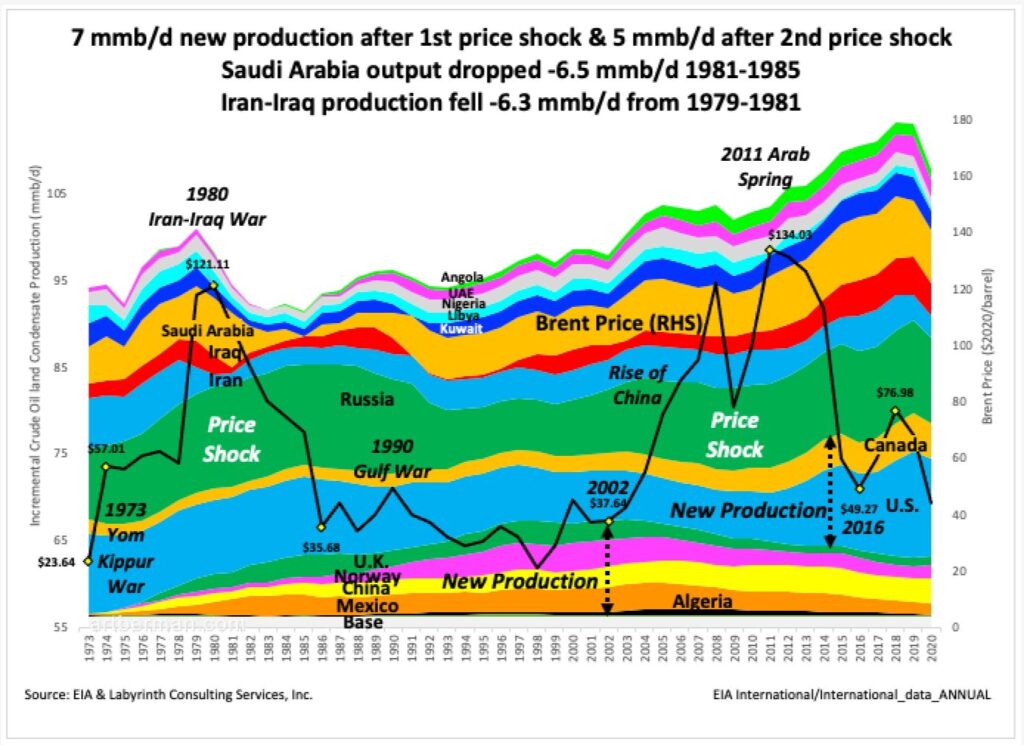

The first oil shortage and price shock began with the Yom Kippur War in 1973 when Brent was $24 per barrel in 2020 dollars (Figure 3). Price increased to $121 by 1980 when more than 6 mmb/d were removed from the market because of the Iran-Iraq War. The shock ended when oil prices fell to $36 in 1986 when supply exceeded demand.

Investment based on higher oil prices from 1974 to 1986 led to 7 mmb/d of new production from the North Sea, China and Mexico (wedge at bottom on Figure 3). But that’s only half of the story. Saudi Arabia’s output dropped 6.5 mmb/d from 1981 through 1985 as it tried to accommodate both new supply and demand destruction from high oil prices (gold fill in upper left part of Figure 3).

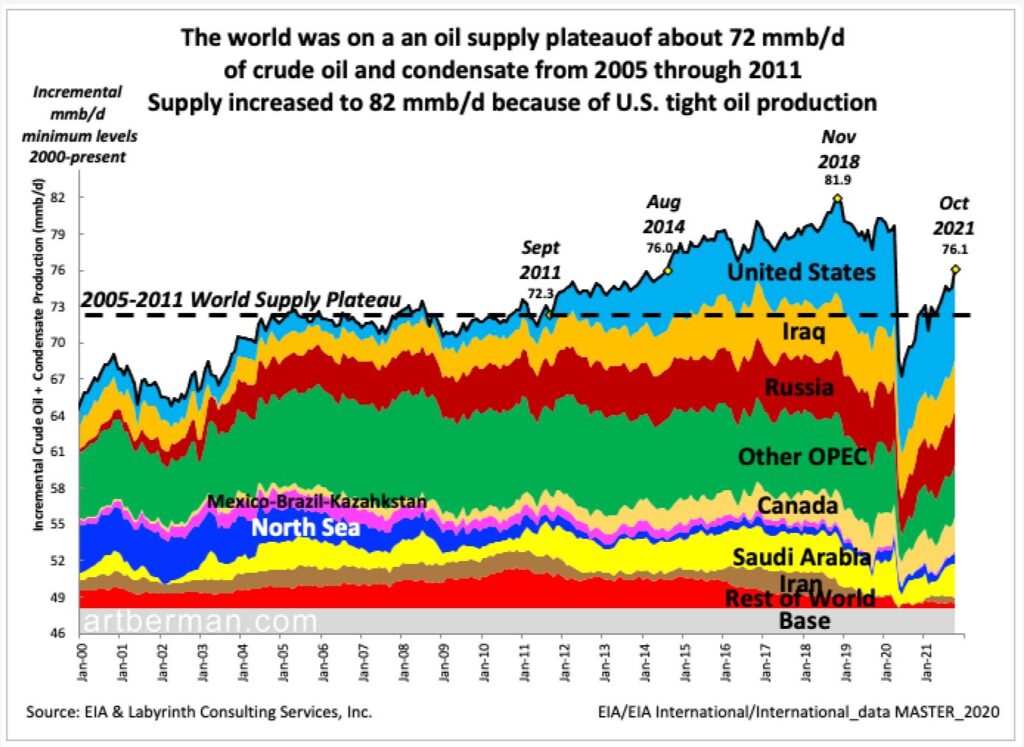

The second oil-price shock began in about 2002 when price was $38 and peaked in 2011 when it reached $134. Price increased initially because of rising demand from China but flat world output from 2005 through 2011 (Figure 4). It peaked in 2011 when 1.5 mmb/d of Libyan oil was removed from the market during that country’s civil war (cyan fill in upper right of Figure 3). The shock ended when prices collapsed from over-supply in 2014 and fell to $49 by 2016.

Almost 5 mmb/d of new unconventional production was added after 2011 from the United States and Canada thanks to massive capital flows based on expectation of prolonged high oil prices (light blue in upper right of Figure 4).

There is always concern about demand destruction when oil prices are high but history shows that supply destruction is at least as important as demand destruction. In fact, supply decreased more than demand during the oil-price shocks after 1973 (Figure 5). More than 21 mmb/d were removed from world markets because of lower supply compared with 15 mmb/d from lower demand since 1974 (see table in Figure 5).

Should oil companies be expected to maintain high production levels when demand is low as a public service to consumers?

The main takeaway from the last 50 years is that investment level is largely outside the control of oil companies. Instead, capital from credit markets is the controlling factor. Since 2014, credit for drilling has contracted and investors have demanded more emphasis on profit margins than on production growth.

An energy shortage began in 2021. The causes are complex but a lower-for-longer complacency about the abundance of relatively cheap oil was part of it. So was the energy-blind idea that oil and gas had a limited future and would soon be replaced by electric power from solar panels and wind turbines. The shortage has worsened in 2022 because of the war in Ukraine and the resulting likelihood of energy supply interruptions from Russia.

The third oil-price shock has begun. It will probably last a decade or more if the past is any guide to the future.

If shortage leads to a period of consistently higher prices, outside capital will probably become available for drilling as it was from 2002 to 2014. Those who do not understand how the oil business works may blame underinvestment for the emerging oil shortage but reduced capital supply from credit markets is the main reason.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Brilliant analysis, Art! You never cease to amaze.

Regards,

Jonathan

Hey Art,

Another really great article. Very nice work. This should be required reading in congress …. well, I believe in unicorns too.

Always a real pleasure to see your thought.

Respectfully,

Bill DeMis

Thanks, Bill.

Other than the author’s conclusion “…reduced capital supply…” I not only agree with the relevant data, but argued the same points of “…deja vu forseasoned executives…” who experienced prior price spikes that were followed by price declines resulting in loss of jobs and bankruptcies. However, there has never been more capital available in the credit markets with the tightest yield spreads in history.

great note as always

this is take 3 for me