Art Berman Newsletter: April 2022 (2022-3)

Oil prices plunged following the announcement that the U.S. will release 1 mmb/d from its Strategic Petroleum Reserve (SPR) over the next 6 months.

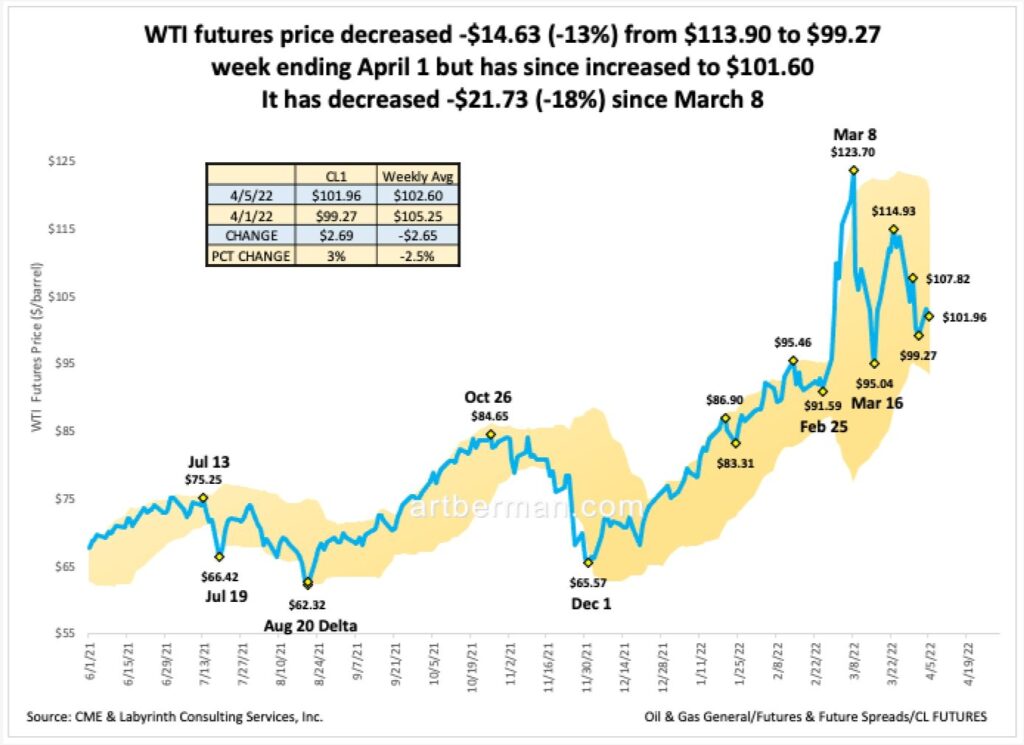

WTI fell from its early March high of $124 to $99 last Friday April 1. Since then, it has increased to $101.96 (Figure 1) but is trading below $100 today, April 6. Most of the recent decrease came from deflation of the approximate $15 of Ukraine war risk premium. Comparative inventory indicates that the “correct” WTI price at present inventory levels is about $91 per barrel.

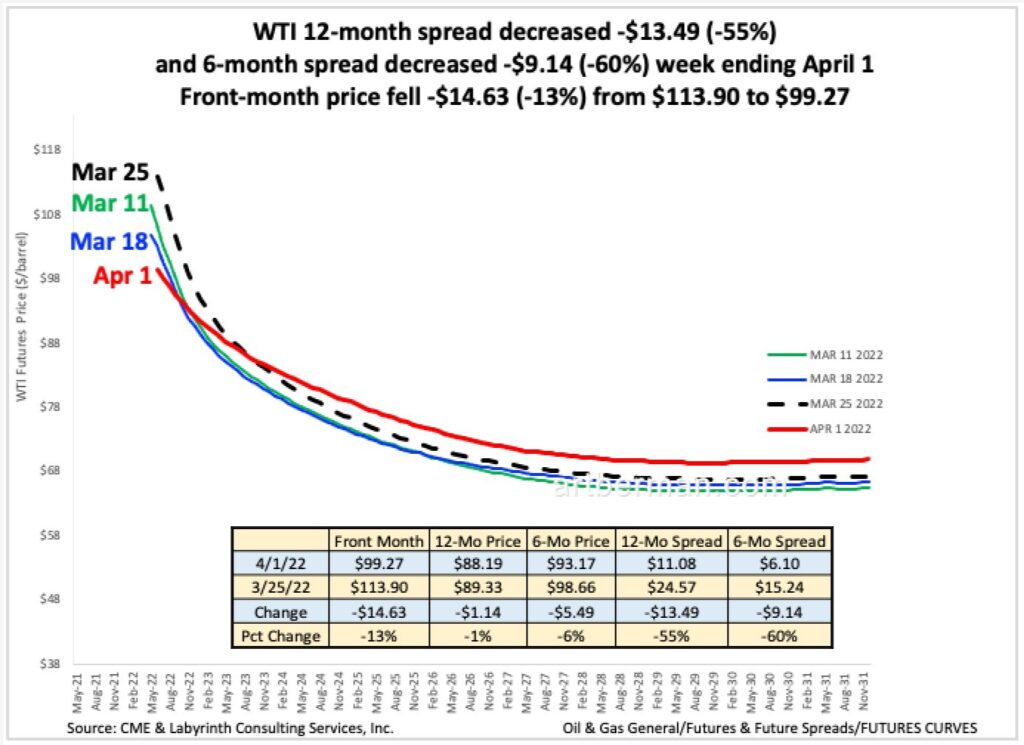

The calendar spreads for futures contracts eased dramatically. WTI 12-month spread decreased $13.49 (-55%) and the 6-month spread decreased -$9.14 (-60%) for the week ending April 1 (Figure 2). The term structure remains backwardated—the market is willing to pay more for oil today than in the future—but its slope is considerably flatter than in recent weeks. That means that supply urgency has relaxed at least for now.

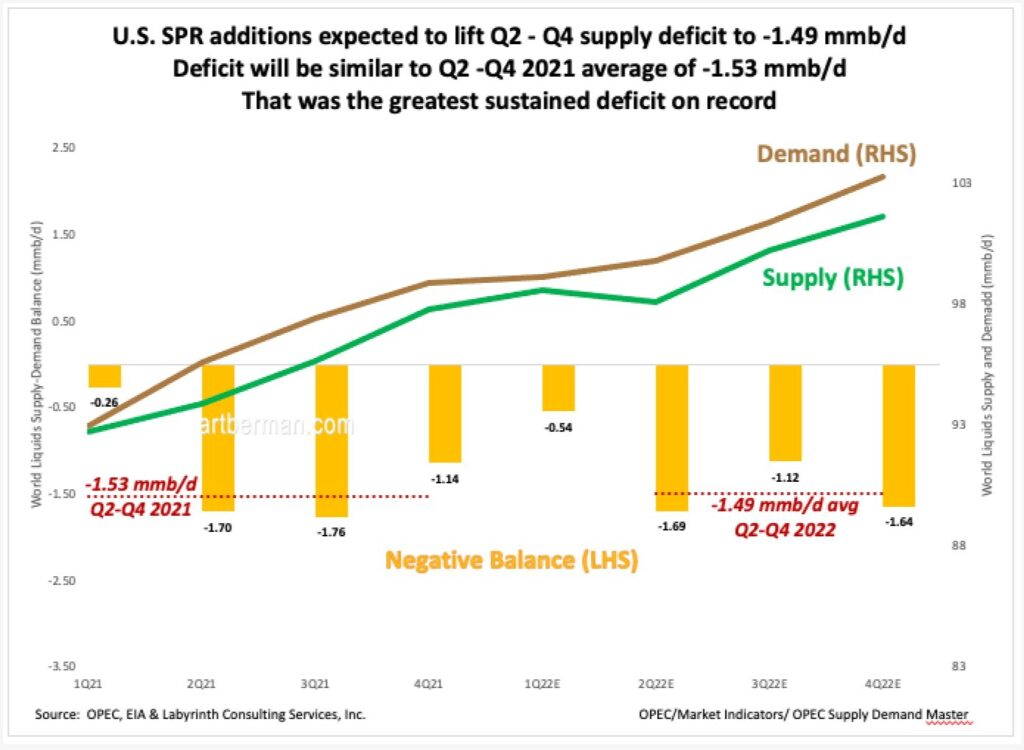

Although their effect is substantial, the SPR releases will do no more than to maintain the world supply-demand deficit at about the same level that it was in the last three quarters of 2021—the greatest sustained deficit on record (Figure 3). Without the releases, the estimated deficit for the rest of 2022 could be 2.5 mmb/d. Needless to say, this and the estimate in Figure 3 are conjectural but based on plausible expectations about Russian export levels.

Oil price is on a balance beam with supply urgency on one side and short-term remedies on the other. World oil and gas supply was tight before the Ukraine conflict began. Now, it seems likely that the world will experience the third major oil shock in the last 75 years.

The most wildly optimistic outcome from U.S. releases would be to offset lower Russian exports. It is unlikely even in that case that oil prices will fall much below present levels of about $100 for WTI and $110 for Brent. That is because the releases are only for six months and do nothing to change the market’s sense of supply urgency beyond the third quarter of 2022.

Today, Goldman Sachs’ Jeff Currie noted that “Every producer with the exception of UAE and Saudi Arabia is producing less today than they were in January 2020…The supply constraints are severe. Throw in the Russian shock on top of it [and]…this is a real shortage.”

The only remedy for high oil prices seems to be an economic recession.

Former U.S. Federal Reserve Governor Lawrence Lindsey said this week, “I do think we’re going to have a recession, probably in the next quarter.” His comments were directed at inflation and the extreme measures the central bank will have to take to counter it.

Others suggest that the inverted Treasury bond yield signals a recession. Last weekend, John Mauldin wrote about the yield curve, “I like to compare it to a fever—not serious in itself, but a sign you have an infection or some other ailment. An inverted yield curve means something is wrong in our economic body.”

My focus on the global petroleum system suggests other reasons for recessionary concerns. Diesel is the life blood of the global economy. Ships, trucks and trains run on diesel so these industries are direct indicators of the economic body.

FreightWaves CEO Craig Fuller recently wrote an article titled “Just 3 years after 2019’s trucking bloodbath, another is on the way.” He believes that demand for freight trucking has weakened because inflation is affecting consumer demand for goods. The Dow Jones Transportation Average fell nearly 5% last Friday in one of the index’s worst single-day performances in recent history.

At the same time, the war in Ukraine has thrown the world shipping industry into chaos. Elizabeth Braw of American Enterprise Institute stated in March that “All of that is happening, and it’s leaving all these vessels traveling around the world with cargo already on board, with crew already on board, leaving them in complete no man’s land…Shipping accounts for 90% of trade…If shipping can’t continue as it has been working until now, then we will see a reduction in economic activity.”

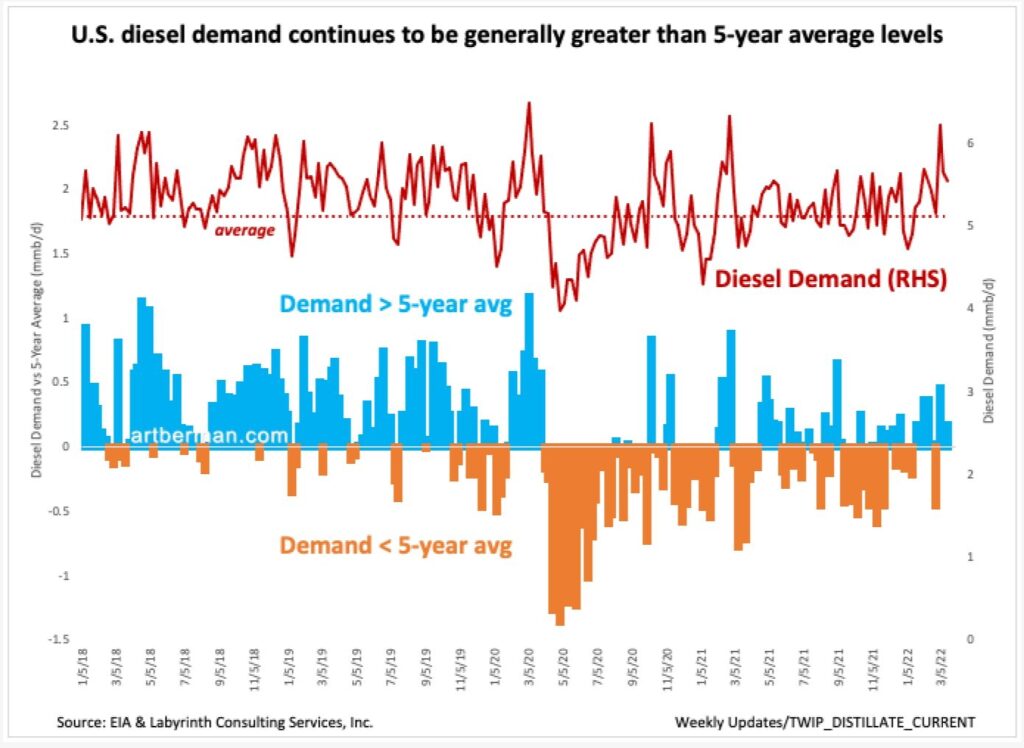

U.S. transport fuel costs have increased 34% in 2022 and yet diesel demand continues to be greater than the 5-year average suggesting that the economy remains relatively strong (Figure 4).

There is little sign of lower gasoline demand either. It seems that consumers are buying less gasoline with each fill-up but visiting the gas station more frequently. That is good news but it is hard to imagine that this trend will continue for long.

This suggests that additional factors are in play. Some say that those include stronger savings after the pandemic and pent-up demand—whatever that is.

I suspected that there may be a lag between oil price increase and a demand response. I normalized crude, diesel and gasoline prices in Figure 5 but found no indication of a lag effect. Monthly average diesel and gasoline prices largely track changes in WTI price.

Whenever oil prices reach levels approaching $100 per barrel, analysts inevitably start talking about demand destruction. Higher energy prices result in higher prices for foods, plastics and metals, often beyond what many buyers can afford. Bloomberg wrote last week, “that’s forcing consumers to cut back and, if the trend grows, may tip economies already buffeted by pandemic and war back into recession.

Many believe that there is some threshold energy price that triggers demand destruction in the broader economy. I have seen estimates that range from $80 to $150 per barrel. I don’t believe that it is that simple and appreciate the wisdom in Morgan Stanley’s remark that “the price at which demand destruction kicks in can be fiendishly difficult to estimate.”

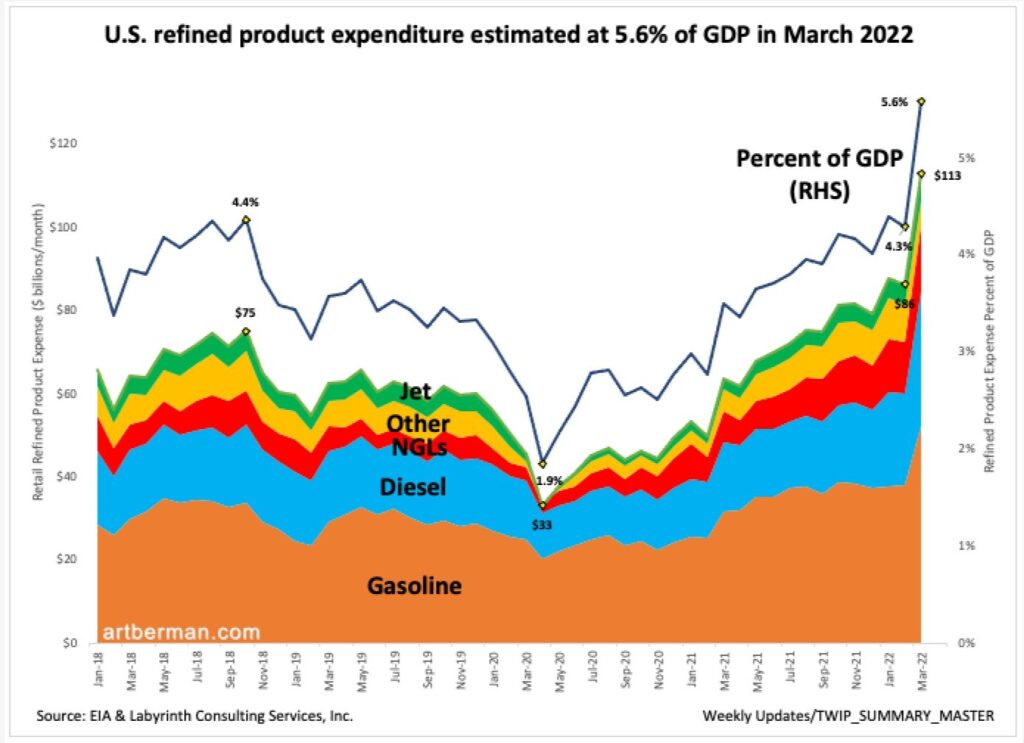

I analyzed U.S. refined product expenditures from January 2018 through March 2022. Figure 6 shows that the present ratio of these costs to U.S. GDP is about 5.6%. That this is the highest level in the period evaluated and the sharp increase in March is notable.

Mauldin’s yield curve comment seems apropos to this measure also: something is wrong in our economic body.

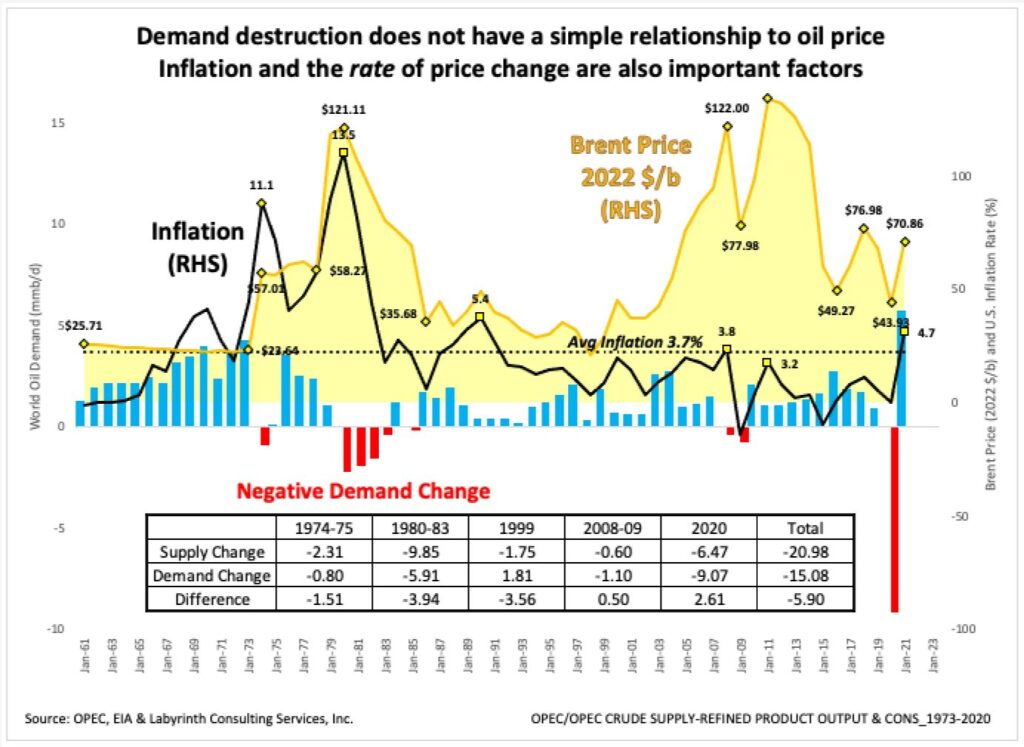

Inflation and the rate of price change are important factors that are only indirectly accounted for by comparing energy expenditures to GDP.

Figure 7 shows inflation, Brent oil price in $2022 dollars and changes in world oil demand. It suggests that rates of change in price and inflation may be more important than their absolute values.

Analysts are obsessed with demand destruction but history shows that supply destruction is at least as important as demand destruction. In fact, supply decreased more than demand during the oil-price shocks after 1973 (Figure 8). More than 21 mmb/d were removed from world markets because of lower supply compared with 15 mmb/d from lower demand since 1974 (see table in Figure 8).

Analysts have been sounding the alarm that oil industry underinvestment is responsible for higher oil prices. Lately, investors are included in the blame game.

Whether you look at absolute prices, the backwardation, producer stock prices or inven tory levels, all the normal market signals are screaming for more oil. This in turn requires more upstream capital spending. Unfortunately, ESG pressures are serving as a block, preventing capital from entering the oil market and preventing it from balancing.

Goehring and Rozencwajg

These concerns are based partly on a misunderstanding of how the oil business works.

In fact, the level of oil investment over the last several years has been exactly right based on market price and investor expectations. The oil business is not a service industry nor is it part of the Consumer Protection Agency.

The third oil-price shock has begun. Peak oil has come back to haunt us.

Shale plays bought the world another decade of supply beyond what anyone imagined twenty years ago. Those plays are far from depleted but enthusiasm for oil is. Energy-blind fantasies about windmills and solar arrays have replaced reality for many activists and world leaders.

The energy shortage that began in 2021 has accelerated in 2022 because of the war in Ukraine and the resulting likelihood of energy supply interruptions from Russia. It is unclear if a balance can be found between earth’s ecosystem and the hard requirements of human systems that rely on energy. The requisite for that possibility is acknowledgement that alternatives to fossil energy are not nearly ready to meet those requirements.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Art, won’t the shale oil independent fill in some of this gap…?? It seems at these prices there is a temptation to get a portion of the production going again?

Don Bruce