Art Berman Newsletter: August 2022 (2022-7)

Markets never move in a perfect straight line, and protracted selloffs include plenty of invigorating rallies. That’s what John Authers wrote in the Washington Post this week about the stock market but it applies equally to oil.

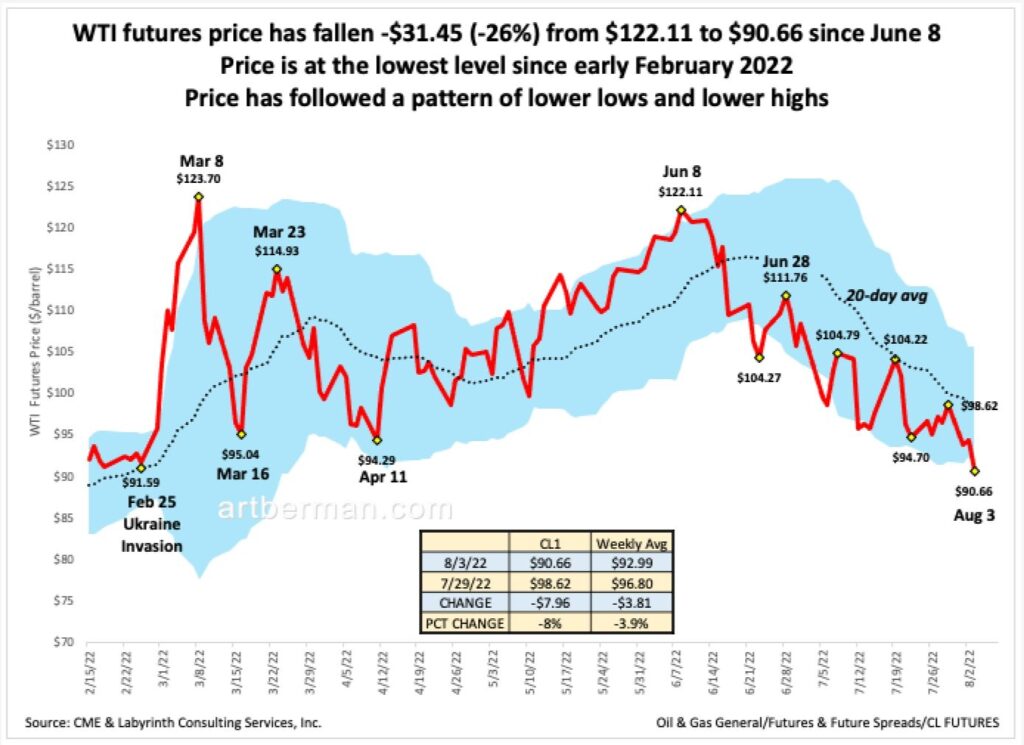

WTI futures price has fallen -$31.45 (-26%) from $122.11 to $90.66 since June 8 (Figure 1). It is at the lowest level since early February 2022. Its descent has included some hopeful rallies but overall, prices have been characterized by lower highs and lower lows. That’s a discouraging signal that requires no expertise in charting patterns. It is also notable that none of those rallies has exceeded the 20-day simple moving average (the dotted black line).

Most market pundits, however, believe that this pattern is an aberration. They point out almost daily what we all know namely, that there is a tug-of-war going on between signs of global economic weakness or recession and tight physical markets.

Last week, ING’s Warren Patterson wrote,”There are clear supply issues facing the market, which will keep the oil balance tight.”

Energy Aspects’ Amrita Sen stated that “the crude market hasn’t been this tight for a very long time,” but that was in mid-June 2021. The message hasn’t changed in more than a year. How is that helpful?

The problem is that the paradigm has changed and analysts don’t see it.

Paradigm Change

Thomas Kuhn popularized the idea of a paradigm in The Structure of Scientific Revolutions. A paradigm is a matrix of shared beliefs that explains certain patterns within a complex system for a time. Once a paradigm is generally accepted, new information is fitted into its preformed, conceptual framework and alternative explanations are strongly resisted. A new model only emerges after the persistent failure of the ruling paradigm to explain new information.

The current oil-market paradigm emerged from the period of rapid economic expansion following World War II. It was predicated on an almost unlimited supply of relatively cheap oil. The oil-price shocks of 1974 through 1980 nearly upended the model. A return to cheaper oil over the following two decades, however, seemed to re-validate the ruling paradigm. Added emphasis was thereafter made for the effect of price on supply and demand largely through the introduction of futures markets in 1978.

The paradigm was again threatened by high oil prices from 2005 through 2014 but again, lower prices through much of the period before 2022 saved it from failure.

The oil and energy crisis of 2022 has again challenged the ruling theory but the analysis and explanations have not yet changed. This is why analysts keep repeating the same message. Many of us suspect that a new threshold has been crossed where the old rules don’t apply but most keep hoping for a return to normal—perhaps after the Ukraine War is over.

Beginning of the End of the Oil Age

The correlation between oil consumption and economic activity (GDP) is well known (Figure 2, courtesy of Simon Michaux). Countries that use more oil have greater productivity and, therefore, higher GDP.

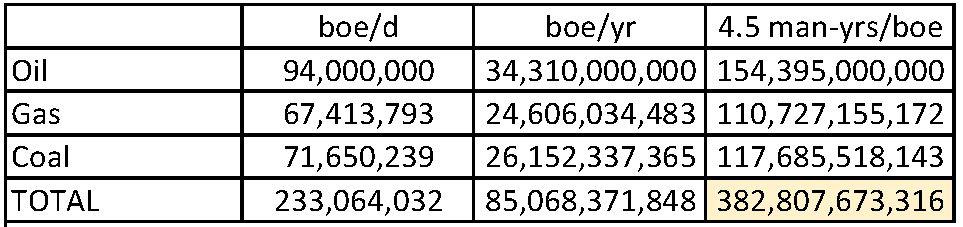

That is because a barrel of oil contains approximately 4.5 man-years of work. No other energy source comes close. Oil has 80% more energy per-unit volume than coal and 150% more than wood. Another way to think about this is that the world has more than 150 billion oil slaves working 24 hours per day (Table 1). No wonder human slavery went out of business! This is a key element of the ruling oil paradigm even though few people actually understand its magnitude.

The truth is that significant cracks in the paradigm’s armor emerged during the first oil shocks. Oil use began to decline from 48% of total world energy consumption after 1977 apparently because of high oil prices (Figure 3). This was the beginning of the end of the oil age.

Despite lower prices, however, oil’s proportion of energy consumption continued to decline through the mid-1990s to 38%. After a brief resurgence to 40% in 2005 and another to 37% in 2017, relative oil use continued to decrease.

The problem is compounded because per-capita oil consumption has been flat since since 1985 (Figure 4). That means that individual worker productivity is not growing as it did before the oil shocks. It is only because we have so many oil slaves that the problem is not worse.

Economy Dissociated from Work

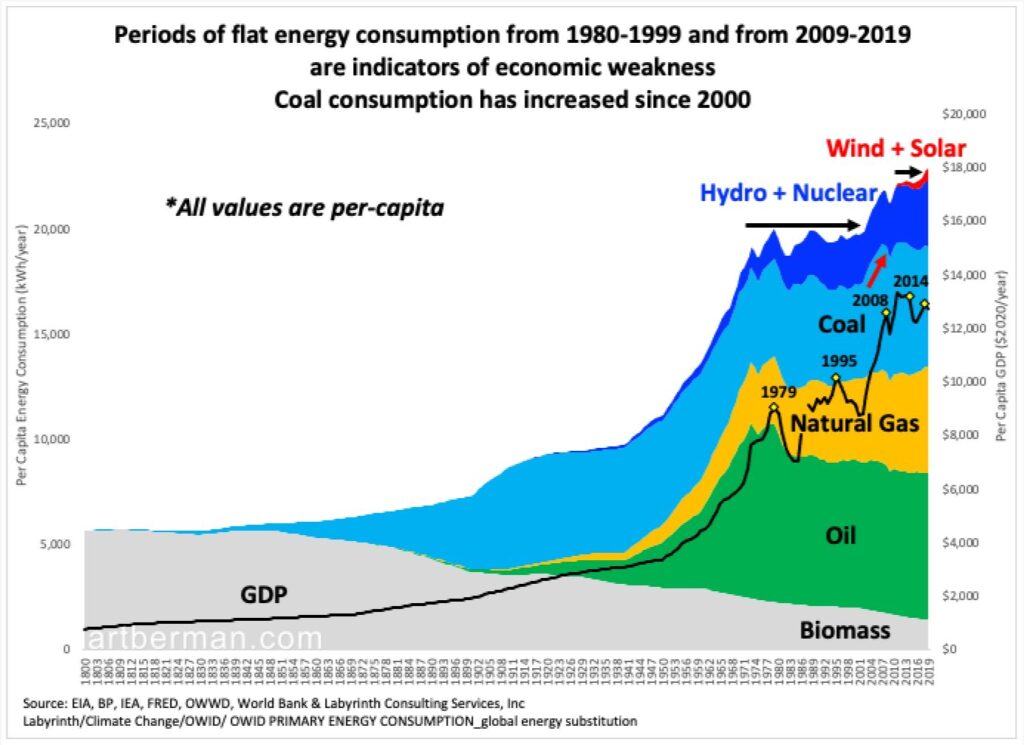

An obvious explanation for why declining relative oil use was not more problematic is that other forms of energy filled gaps left by declining oil consumption. Coal, natural gas, nuclear and hydroelectric power increased markedly during the 1970s and 1980s (Figure 5). Per-capita total energy consumption, however, was as flat as oil use through the end of the 20th century.

In the early 2000s, coal consumption ramped up dramatically as the economies of China, India and other developing countries grew. Following the 2008 Financial Collapse, world energy consumption flattened again.

Figure 5. Periods of flat energy consumption from 1980-1999 and from 2009-2019 are indicators of economic weakness. Coal consumption has increased since 2000. Source: EIA, BP, IEA, FRED, OWWD, World Bank & Labyrinth Consulting Services, Inc.

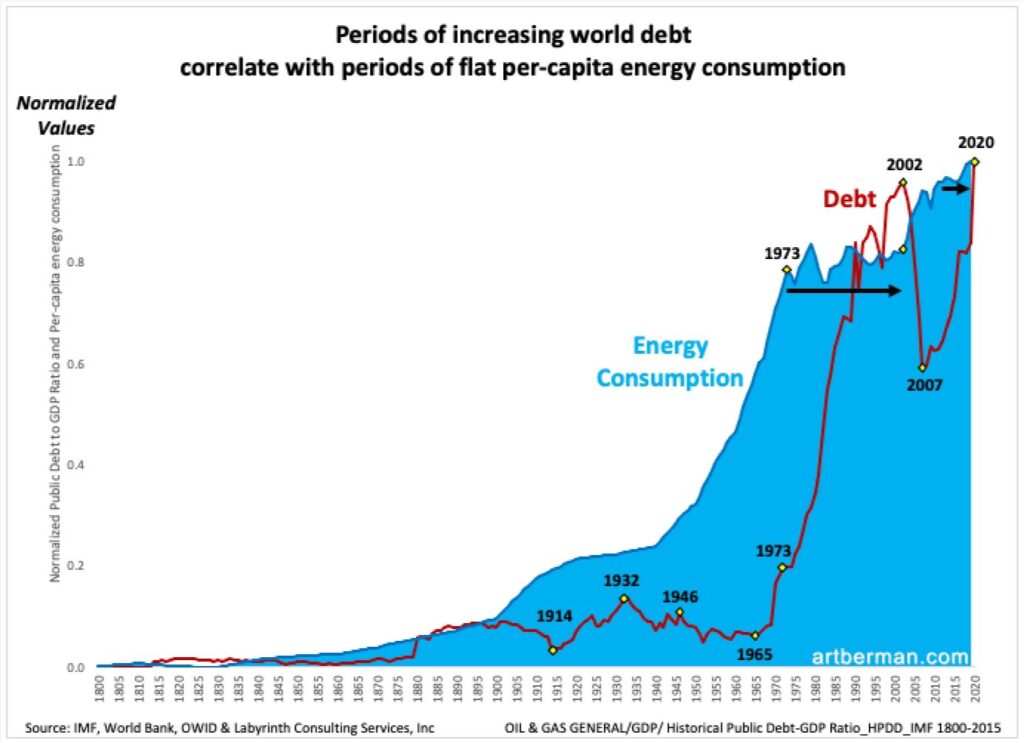

Another factor that disguised these productivity changes was debt. Figure 6 shows that world public debt increased sharply beginning in the mid-1960s and accelerated during the oil price shocks of the 1970s and 1980s. It further shows that the highest debt levels corresponded to periods of flat per-capita energy consumption. In other words, debt was used to boost spending and GDP disguising the stagnation of worker productivity from energy consumption.

Parts of the economy were increasingly dissociated from work—the real economy—and progressively more focused on financial transactions—the fiat economy. In the fiat economy, capital could be created out of thin air and money could be multiplied through leveraged financial transactions that involved no physical product.

This phenomenon is commonly described as the decoupling of the economy from energy consumption. It is commonly cited as an explanation for peak oil demand at some time in the relatively near future. It is sometimes called the energy intensity of GDP or the amount of oil use needed to generate a dollar of GDP.

Figure 7 shows this concept taken to its absurd limit. Energy, not oil, intensity is plotted along with total world energy consumption. The amount of energy needed for a dollar of GDP increase has declined since at least 1970. This suggests that GDP can increase using less energy every year. That is the economic equivalent of a perpetual motion machine. If that is true, then why does world energy consumption continue to increase?

It only makes sense if the fiat economy has thoroughly distorted GDP through debt and monetary policy following the oil-price shocks 50 years ago.

The Real Energy Paradigm

A substantial portion of the global economy is synthetic. It is supported by massive debt and leveraged investments in some sector that requires little energy and, therefore, little work. At some time, part of this economy will contract or collapse reverting to something approaching the real economy.

That is a crucial perspective for those who analyze and invest in energy.

Analysts have paid lip service to a supply and demand model for at least 50 years. It has served investors poorly because demand has almost always been given precedence over supply. That’s a problem because oil markets have been supply-constrained since price discovery through futures trading was established nearly 45 years ago. Markets have little control over demand but price can be used to modulate drilling.

There is always concern about demand destruction when oil prices move higher but history shows that supply destruction is at least as important. In fact, supply decreased more than demand during the oil-price shocks after 1973. More than 21 mmb/d were removed from world markets because of lower supply compared with 15 mmb/d from lower demand since 1974.

The world thinks it’s in an energy crisis today and indeed there are shortages in some places. Mainstream analysts explain that it is because of a decade of industry under-investment, resurgent demand after the 2020 pandemic, and the Ukraine War. Those are all factors but the underlying problem is investor hesitancy to fund aggressive drilling programs since about mid-2018. Despite record cash flow in recent quarters, few public companies are willing to undertake those campaigns without investor support.

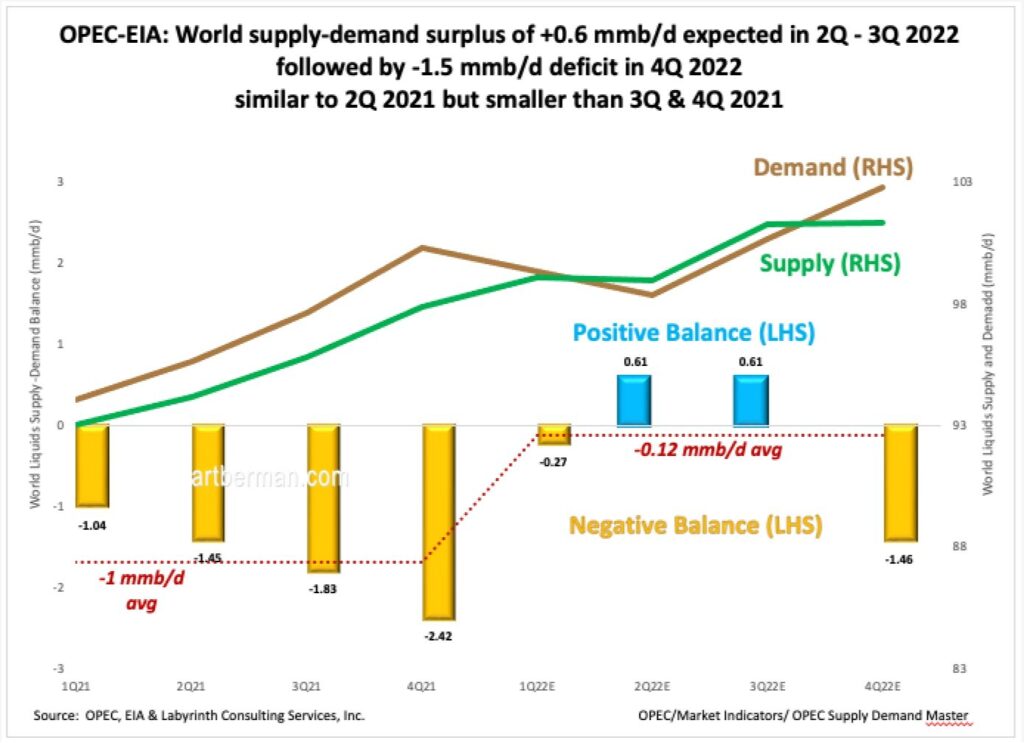

Meanwhile, the short-term is characterized by adequate oil supply despite the daily analyst chorus of comments about tight physical supply. The world has a supply surplus of about +0.6 mmb/d through the third quarter of 2022 (Figure 7). A deficit of approximately -1.5 mmb/d is expected in the fourth quarter but I doubt it will be that large given the underlying weakness of the global economy. Even if the expected deficit materializes, it will be similar to deficits in 2021 that failed to result in extraordinarily high oil prices.

The world thinks that an energy transition is underway but fails to understand that transitions are additive. The relative percent of fuels changes but volumes rarely decrease. The world uses, for example, as much biomass today as in 1800. Nor is there any likelihood that this transition will take 30 years instead of the century or longer period for earlier transitions.

Most people think the economy runs on money. It runs on energy. Energy is the economy. Money is a claim on the work that comes from energy and debt is a lien on future energy.

The world is undergoing an energy crisis more fundamental than the simple shortage happening today in Europe. A shortage can be remedied.

The economic growth and prosperity after World War II was because of the extraordinary productivity increase from converting to an oil-based society. That lasted for roughly a generation. The oil-price shock of 1974 changed everything by ending the rapid economic expansion made possible by cheap oil.

“From 1950 to 1973 the Western European economic product had nearly tripled, and the US GDP had more than doubled in that single generation. Between 1973 and 1975 the global economic growth rate dropped about 90 percent…A second wave of oil price rises…led to…another 90 percent decline in the global rate of economic growth between 1979 and 1982.”

Vaclav Smil, The Way The World Works (2022)

I am deeply concerned about climate change but I don’t think it is the biggest problem that the world faces in the next decade. It is a symptom of the much larger problem of overshoot—humans using natural resources and polluting at rates beyond the planet’s capacity to recover.

As per-capita oil consumption declined following the initial oil shocks, the world became progressively poorer. Debt was used to smooth over this problem and to extend the illusion of growth. GDP kept growing because it excludes the cost of material production.

The real crisis today is the economic expression of the reality that energy is the economy. As living standards fall, mass immigration and civil unrest will probably increase. The oil age has been ending for 50 years and there is no substitute. Wind, solar and nuclear only address electric power generation which accounts for only 18% of world energy consumption. Even if we could magically transform 100% of electric power to non-fossil energy sources, this would not address the other 72% of energy use that society needs.

The world is not running out of oil but it takes capital and time to increase supply. World oil production most recently peaked in November 2018 at 102.2 mmb/d of total liquids (Figure 10). It is unlikely to regain that level at any time over the next several years. Complaining about government policy or industry under-investment is not helpful. We should just accept that this is our near-term reality.

The medium- to long-term should be increasingly affected by limited supply growth. The market will send price signals to producers based on its sense of medium-term supply urgency. Prices will rally until inflation and a fragile economy end the rally. This is the dialectic that I expect will dominate oil markets in 2022 and probably beyond. There is great opportunity for those who understand this pattern.

These themes are playing against a backdrop of massive global debt load and the imaginary recovery from the economic closures of 2020 and 2021.

Price formation in oil markets is all about supply and inventories are part of supply. Old-paradigm analysts believe that oil demand must revert to ever-higher levels which supply simply cannot meet. In fact, the opposite is true. The correct oil paradigm is supply-driven and price-constrained.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

A most important newsletter! (Not that the others are not). A brilliant use of data to debunk an old paradigm and move forward.

Thank you for your comment.

All the best,

Art

Hello Art:

I’ve been trading commodities for 50 years, and these markets take the cake as far as analysis is concerned.

Are you in general agreement with Jeff Curries research?

https://smartermarkets.media/summer-playlist-episode-1-jeff-currie/

Interesting Times!!

Doug Edwards

Doug,

I admire Jeff’s insight and agree with most of his observations. I still place him in the category of old-paradigm analysts because he cannot see a world in which lower supply leads to lower instead of higher prices.

All the best,

Art