Art Berman Newsletter: January 2022 (2021-12)

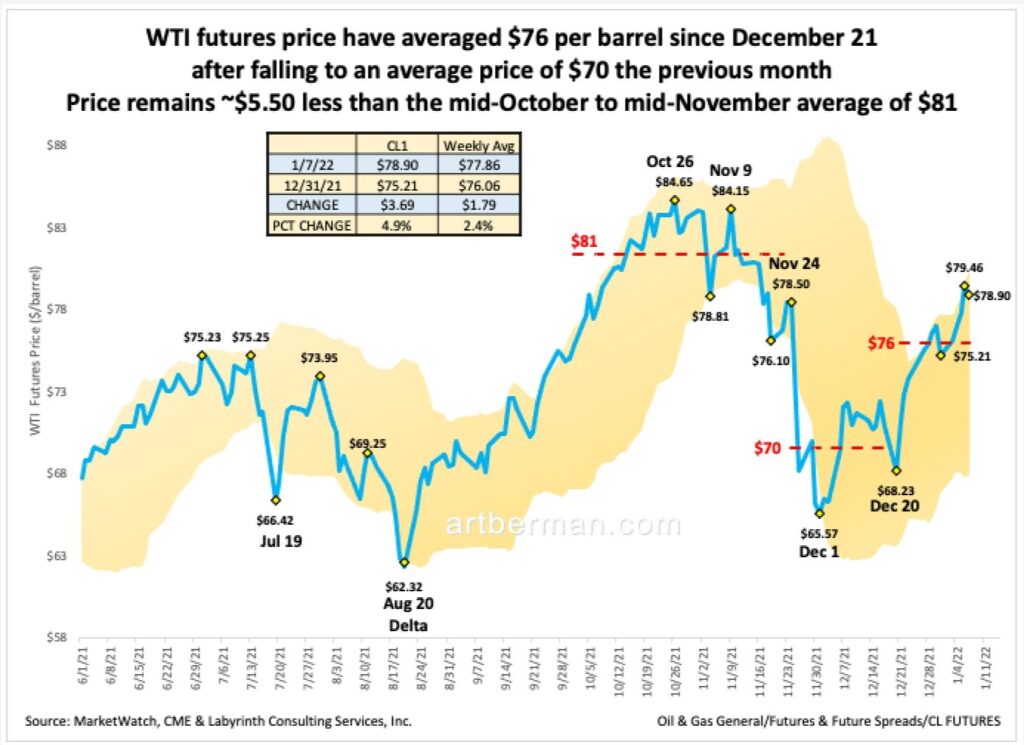

WTI prices have rallied to almost $80 per barrel and seem likely to move higher. Futures prices have averaged $76 per barrel since December 21 after falling to an average price of $70 the previous month (Figure 1). Price remains ~$5.50 less than the mid-October to mid-November average of $81.

Prices have returned to the upper Bollinger band limit (yellow shaded area in Figure 1) for the first time since mid-October. The bands represent two standard deviations around the 20-day moving average price. Prices at the upper limit may mean a slowing rate of price growth. On the other hand, prices remained at the upper Bollinger limit from mid-September through mid-October during the long rally from $72 to $80 per barrel.

Mainstream interpretations explain lower November-December prices by releases from strategic petroleum reserves and demand concerns about the omicron Covid variant. The late December and January rally is similarly explained by reduced demand concerns from omicron and supply outages in Kazakhstan, Libya, Nigeria and North America. Both scenarios are occurring against a backdrop of resurgent demand for and lagging supply of energy.

Those are all relevant factors but they also describe business-as-usual in world oil markets. Mainstream interpretations fail to acknowledge that a new paradigm is emerging—one that takes into account an energy transition that has no historical analogue.

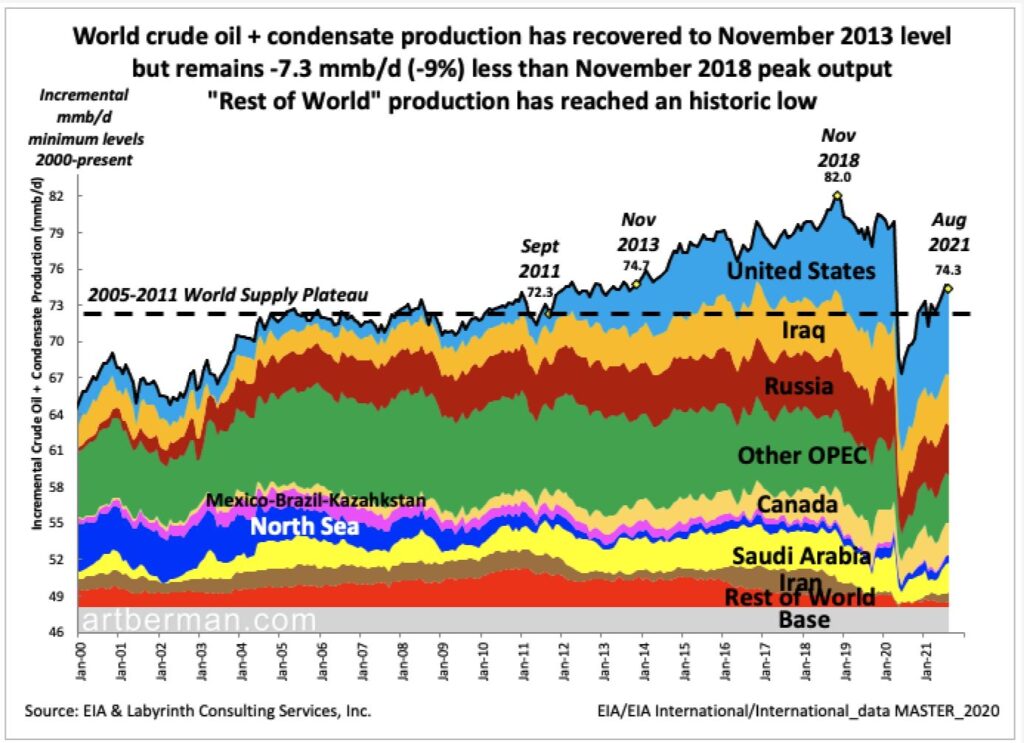

World crude oil and condensate production has recovered to the November 2013 level of about 74 mmb/d but remains -7.3 mmb/d (-9%) less than November 2018 peak output of 82 mmb/d (Figure 2). “Rest of World” production has reached an historic low.

The 2005-2011 world supply plateau shown in Figure 2 was the principal reason for high oil prices that led to development of tight oil in the United States. All meaningful supply growth since 2005 has been from the U.S. and specifically from tight oil plays.

World crude and condensate production dropped 13.2 mmb/d (16%) from November 2019 through June 2020. It has since increased about 8 mmb/d (+11%) back to near the 2005-2011 plateau. This change in supply is critical for understanding current market pricing.

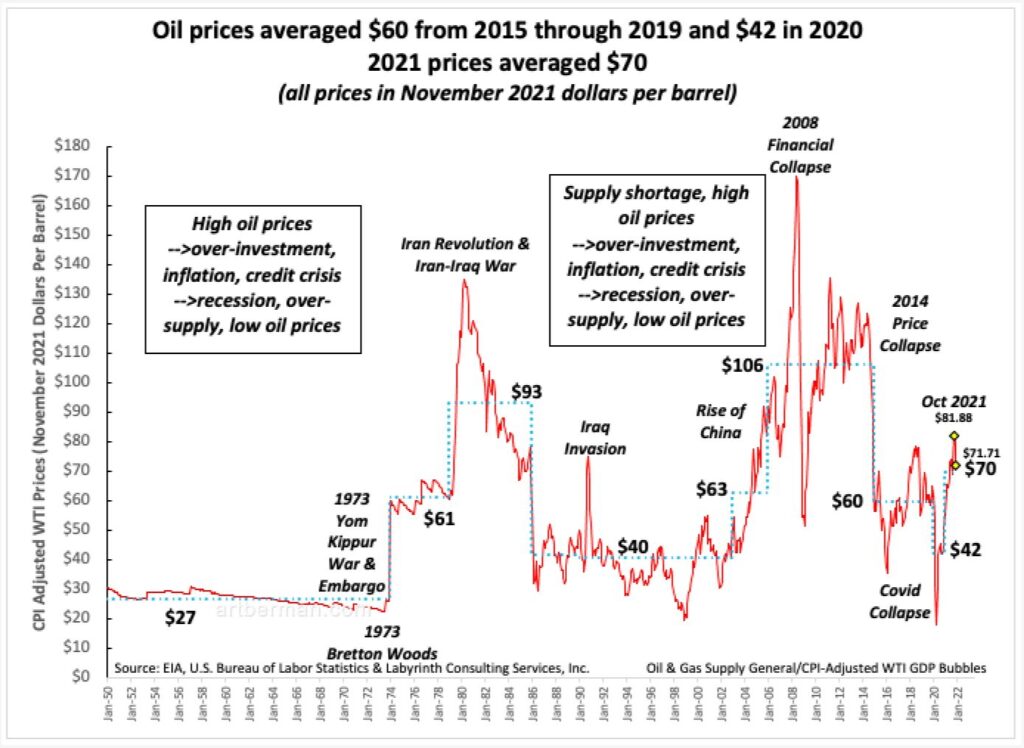

WTI averaged $60 per barrel from 2015 through 2019 and $42 in 2020 all in CPI-adjusted dollars (Figure 3). 2021 prices averaged $70.

Prices averaged $106 per barrel from January 2006 through December 2014 and this is surely what bullish analysts have in mind as they point out the lack of oil investment and call for an impending super-cycle for commodities.

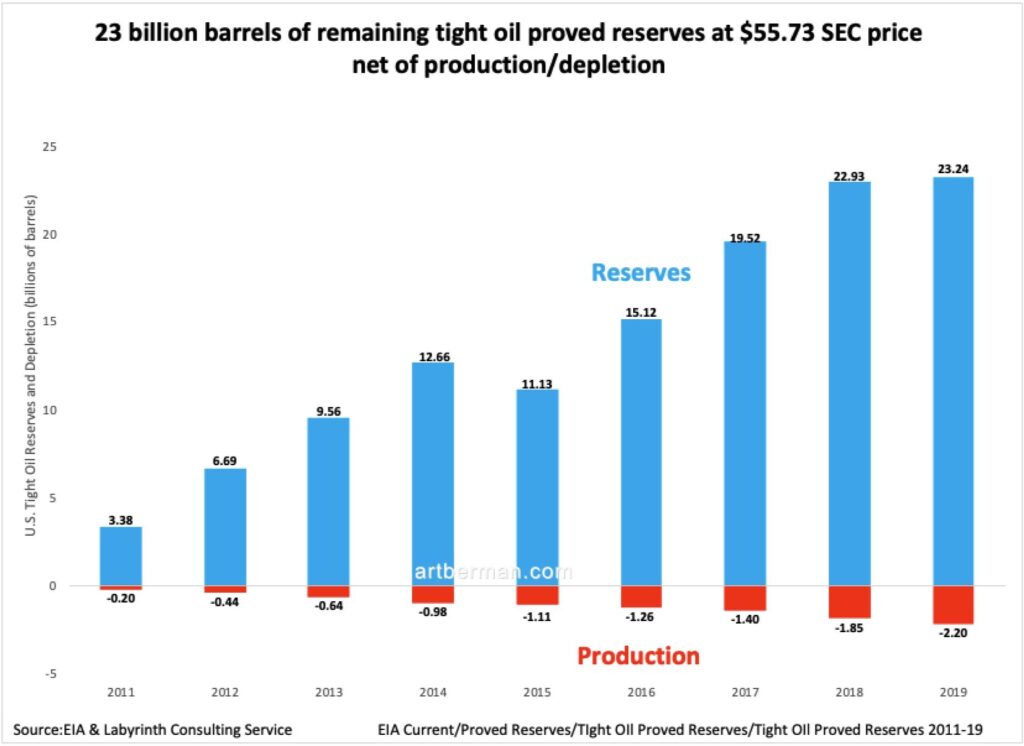

Many of the same analysts assume that U.S. shale plays have limited growth potential but proved reserves tell a different story. EIA’s latest data indicates that there are about 23 billion barrels of tight oil proved reserves at an SEC price of $55.73 (Figure 4). The most recent Dallas Federal Reserve survey of 92 oil and gas executive indicates that most companies can break even at about $50 per barrel.

The production/depletion rates shown in Figure 4 suggest about 10 years of remaining reserves. That may not seem like a lot but 10 years of reserves-over-production has been the standard number for my entire career. One may argue that new reserves are not or will not be found at previous levels but that argument has been around for most of my career also.

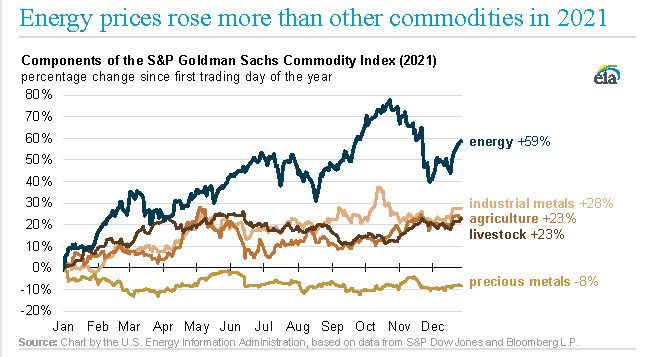

Figure 5 shows the energy prices performed better than all other commodities in Goldman Sachs’ Commodity Index for 2021. This does not mean that investors will rush back to oil companies with new capital but some will especially if prices remain relatively high or move higher.

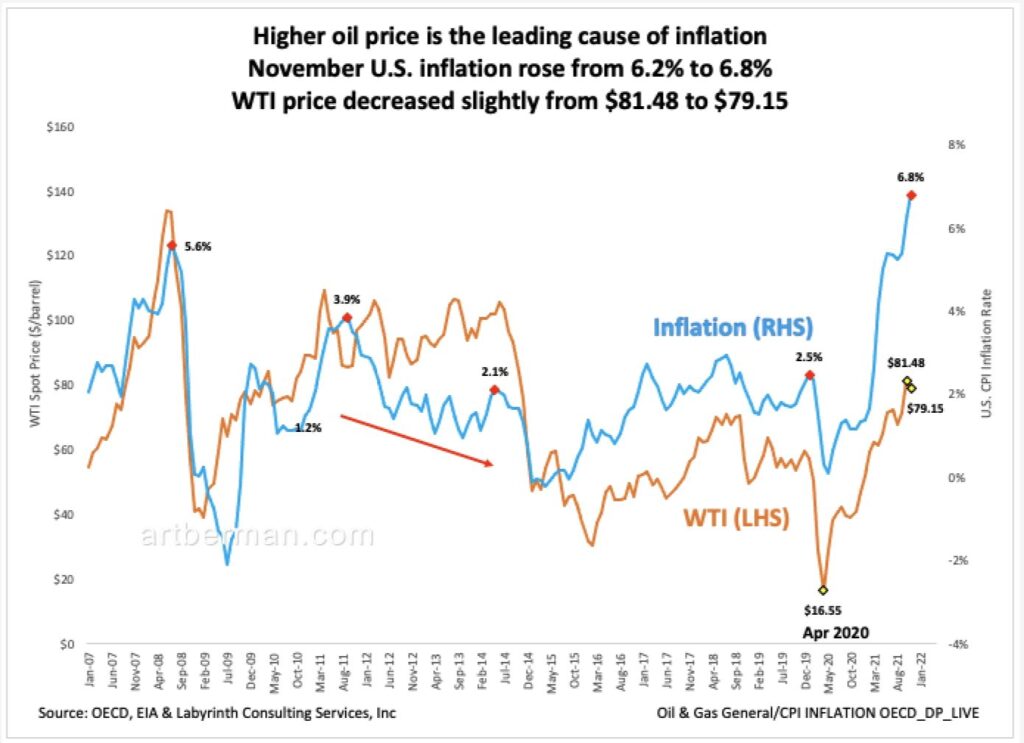

On the other hand, U.S. inflation has increased to 6.8% (Figure 6). That is the highest level since June 1982. As economists debate whether or not inflation is transitory, I look at the solid correlation between inflation and oil price and conclude that it is as transitory as relatively high oil prices. In other words, it is here to stay unless oil price falls.

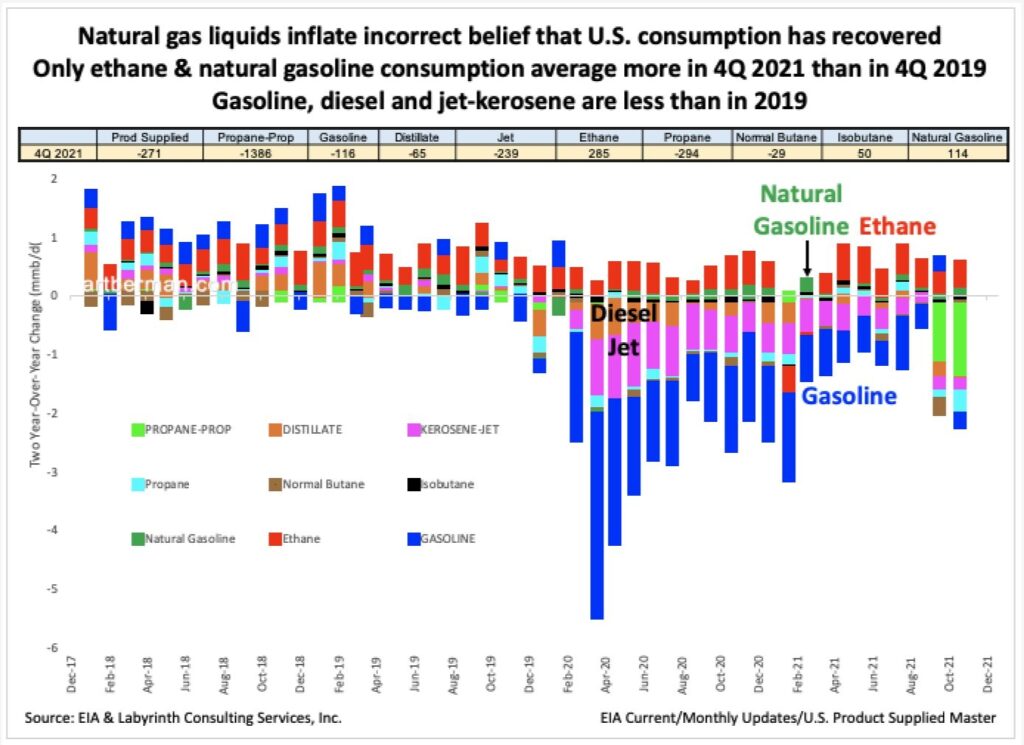

Figure 7 shows two year-over-year U.S. consumption data for key refined products in order to compare recent levels with those before the Covid pandemic. The data is clear. Although gasoline, diesel and jet consumption are recovering, they lag 2019 levels. The popular belief that consumption has recovered is biased by increased natural gas liquids consumption. The leading sources for this are ethane and natural gasoline, both of which come from natural gas and not from oil production.

Inflation is affecting most consumers and they will cut back where they can. Gasoline is among the first discretionary cuts that consumers make. Driving a little less is fairly painless especially in a changed work and commuting paradigm.

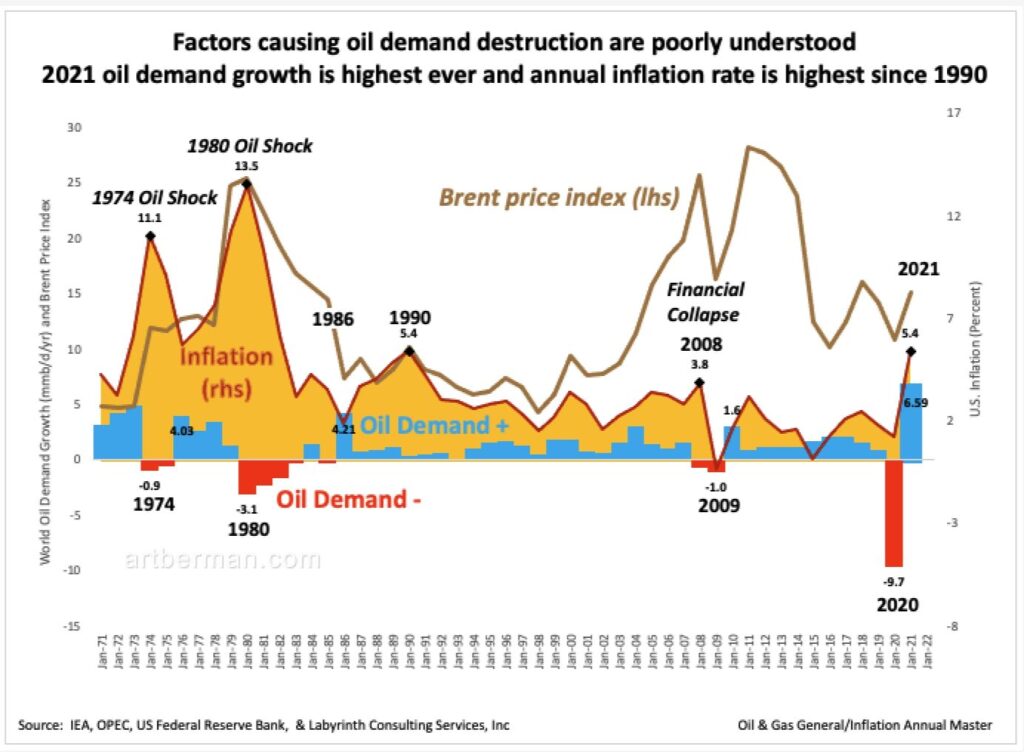

Although the factors controlling oil demand destruction are complex, there is an empirical correlation between inflation rate and oil demand destruction (Figure 8). The 1974 through 1980 oil shocks were accompanied by record global inflation rates of more than 11%. Oil demand decreased by more than 3 mmb/d in 1980 when Brent price reached $128 in 2021 dollars.

Surprisingly, inflation only increased about 0.5% above its 10-year average in 2008 and fell to a record low in 2009 following inflation-adjusted Brent price of $167 per barrel. Oil demand destruction was only about 1 mmb/d and inflation remained relatively low despite $110 average real Brent price from 2010 through 2014. I suspect that anomalous period reflected the financial vs. economic basis for the 2008 Collapse and monetary policies that favored affordability and spending.

Demand destruction approached 10 mmb/d in 2020. That had little to do with inflation and everything to do with the closure of the world economy. The practically unavoidable resurgence in oil and material demand has resulted in the highest inflation in 30 years. An inflation surge of almost 1.5% in October and November 2021 accompanied $82.50 average Brent price.

The mainstream explanation—that Covid-related demand concerns caused lower oil prices in December—ignores this data. Demand destruction was an important factor in that price decline.

China’s “common prosperity” economic reforms are another potentially critical factor going forward. Premier Xi Jinping has greatly restricted China’s booming technology, real estate, education and entertainment industries in order to reduce income inequality.

This has already led to lower economic growth and has profound implications for China’s demand for oil. At the same time, China has not escaped higher energy prices.

“It will have pretty substantial external implications and those might play out for years to come,” noted Michael Pettis, a Senior Fellow at the Carnegie-Tsinghua Center and professor of finance at Peking University.

What is happening today inside China has great deflationary potential across world markets but is seldom mentioned by oil analysts.

The short-term is dominated by adequate oil supply despite the daily analyst catechism of tight physical supply. The medium- to long-term is increasingly affected by limited supply growth.

These themes are playing against a backdrop of massive global debt load and the imaginary recovery from the economic closures of 2020 and 2021.

Meanwhile, an energy transition is underway that finds no irony in moving from the most productive fossil energy sources to substantially less-productive renewable sources. Nor is there any sense of the historical unlikelihood of making this transition in 30 years instead of the century or longer period for earlier transitions.

Old paradigm analysts believe that oil demand must revert to ever-higher levels which supply simply cannot meet. They cannot fathom a reality in which demand constrained by prices near the upper limit of affordability adjusts to oil supply limited by investors who see a finite future for oil.

The market will send price signals to producers based on its sense of medium-term supply urgency. Prices will rally until inflation and a fragile economy end the rally. This is the dialectic that I expect will dominate oil markets in 2022 and probably beyond. There is great opportunity for those who understand this pattern.

Ronald Reagan said the future belongs to the brave. I suspect that it has always belonged to those with sufficient clarity to recognize a new paradigm when they see it.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Thanks for the response.

Doug

The analysis is crystal clear. one question.Why on earth would Texas banks reload and lend to the Tigh Oil people after the bust of the last three years and the likelihood of waffling prices for the foreseeable furute?

All bets off in a Middle East problem.

Doug Edwards

Doug,

Because banks need to make money. They make money when they lend money.

Best,

Art