Art Berman Newsletter: January 2023 (2023-1)

Many analysts imagine that oil markets are returning to normal after a rough second half of 2022. That means higher prices but price is only a measure of efficiency, and higher prices mean the market is failing its customers.

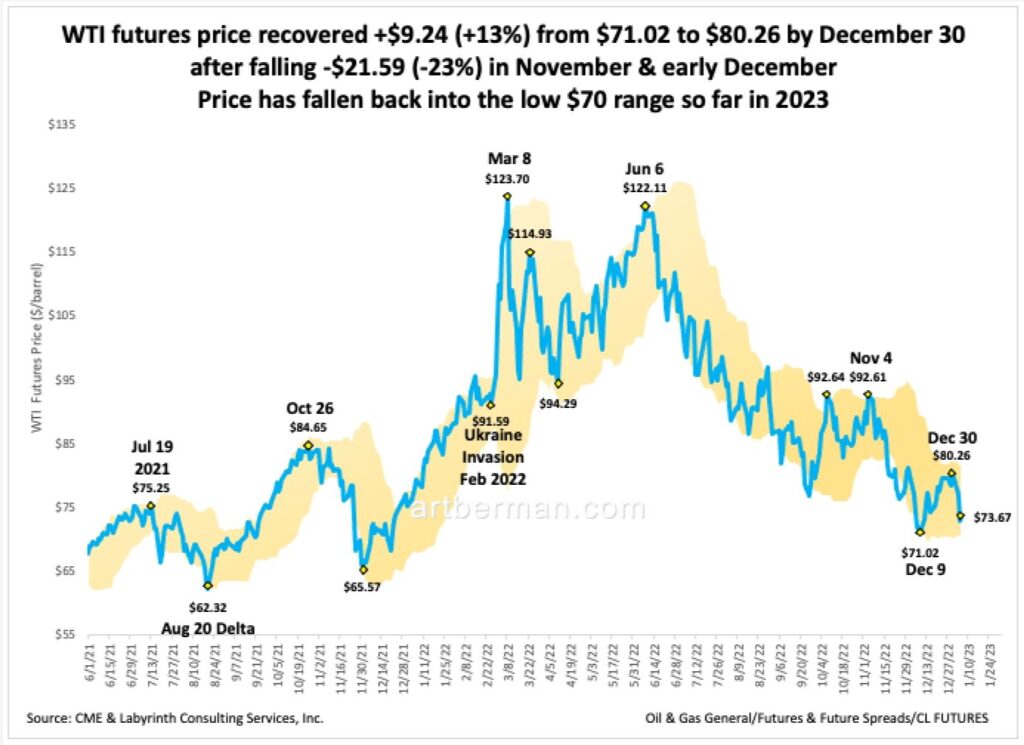

WTI price rose to $124 after Russia invaded Ukraine in February 2022 (Figure 1) but fell to $71 by early December 2022. It rose to $80 by year-end but has fallen back into the low $70 range so far in 2023. In other words, price returned to pre-Ukraine invasion levels averaging $77 in December. If that’s normal, then I agree.

The problem, of course, is that nothing has been very normal for several years. The world experienced a series of systemic shocks that began with the global pandemic in early 2020. The highest inflation rates in decades—especially in the United States and in Europe—have resulted in monetary tightening. China’s economy has slowed with COVID lockdowns and the effects of the Ukraine War have affected supply chains and increased food and energy prices around the world.

In August, French President Emmanuel Macron stated this succinctly and eloquently:

“What we are currently living through is a kind of major tipping point or a great upheaval … we are living the end of what could have seemed an era of abundance…the end of the abundance of products of technologies that seemed always available.”

Last week, Daniel Yergin described what happened to oil markets in 2022:

“Europe’s ban on Russian oil, combined with the U.S.-generated “cap” on Russian oil prices, marks the end of the global oil market. In its place is a partitioned market whose borders are shaped by not only economics and logistics but also geopolitical strategy.”

He under-stated things. The global oil market is fragmenting but also, the world order that has existed since the end of World War II is ending.

A Joint Statement by China and Russia in early February 2022 called for “constructing a community of common destiny for mankind.”

“The sides call for the establishment of a new kind of relationships between world powers…They reaffirm that the new inter-State relations between Russia and China are superior to political and military alliances of the Cold War era. Friendship between the two States has no limits…The sides oppose further enlargement of NATO and call on the North Atlantic Alliance to abandon its ideologized cold war approaches.”

Russia and China declared the beginning of a new world order. Twenty days later, Russia began its invasion of Ukraine.

This created extraordinary market dislocations that pushed energy, grain and fertilizer prices to 10-year highs. The western press gloats about Russia’s military failures but this conflict is more about establishing a new world order than it is about conquering Ukraine. Look who is on Russia’s side from an oil perspective—OPEC+ and China at the very least. That’s more than 50% of global oil supply.

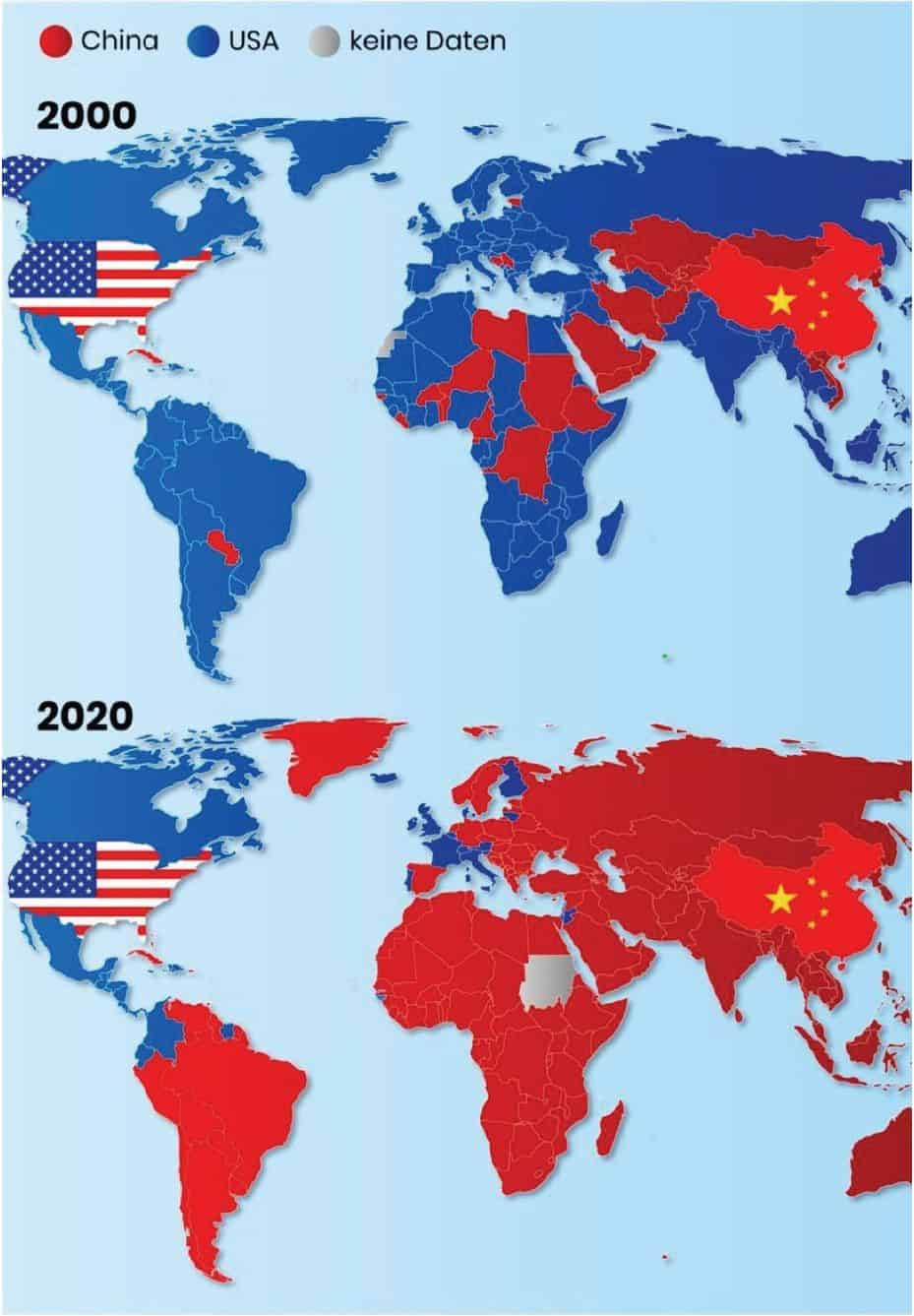

Figure 2 shows the change in trade since 2020 with the United States (blue), and with China (red). Felix Zulauf commented on this map that,

“It’s a completely different world…When you look at the world map…in the year 2000…the world was blue….When you look at the map today, all of Asia is red. Africa is red. South America is red. More than half of Europe is red. And what’s left is Great Britain, US, Canada, Mexico, and maybe the Netherlands—and that’s it.”

The reason the US and its Allies won WWII was because of better access to petroleum than its enemies. That, at least, was the conclusion of a study by Herbert Feist in 1944 which greatly influenced President Roosevelt’s understanding of the strategic importance of oil.

“The outstanding feature of oil geography is that, while the demand for oil is world-wide, the great sources of supply are few and separated…[The] basic policy task must be that our country and its armed forces be able to count in wartime on broad supply wherever these forces require it with least military risk and with minimum burdensome obligations.”

That was part of the reason that Roosevelt met with Abdul Aziz Ibn Saud on the aircraft carrier USS Quincy as he returned from Yalta. Even though the U.S. was oil-independent and by far the largest producer in the world in 1945, Roosevelt recognized that energy security was the basis of U.S. power. He agreed to guarantee Saudi national security in exchange for Saudi Arabia providing the United States with oil security.

That was the keystone of U.S. foreign policy for the next 58 years until George W. Bush destroyed it in 2003 by occupying Iraq. This upset the Middle East balance of power by giving greater influence to Iran. Subsequent mis-steps by the Obama administration increased Iran’s reach and allowed Russia to become a serious player on Iran’s side.

Obama further undermined what Roosevelt had acheived by abandoning traditional allies Saudi Arabia, Israel and Egypt. He thought that the U.S. no longer needed Saudi Arabia because of the shale revolution.

Trump partied with Saudi royalty but further undermined policy by telling the Saudis what to do. He did nothing when Saudi refineries were bombed in 2019—not even a phone call to say we felt for our partners. He managed energy security like a Manhattan slumlord. Biden continues the energy-blind Obama approach.

U.S. relations got so bad with Saudi Arabia that Crown Prince Mohammed bin Salman would not return phone calls from President Biden in early 2022. Felix Zulauf noted that “the Saudis used to be an ally of the US, which is not the case anymore. The Saudis are closer to China these days than to the US. So, the whole equation is much more fragile than it used to be. That’s a different setup.”

Just after Russia invaded Ukraine, Dan Yergin remarked,

“Energy security fell off the table in the United States as we became self-sufficient…It was like amnesia.”

Putin is not an original thinker but a consummate pragmatist. He has watched the US’s descent into energy blindness. Europe just followed the money.

Putin chose his moment to invade Ukraine cleverly. US production was down 2 mmb/d with Covid, and European countries had taken on massive levels of debt to survive the pandemic. He calculated that withholding energy would stoke inflation and make that debt unmanageable not to mention the social welfare bills to subsidize higher energy prices.

Russia and China have an informal confederation of nations who have had it with western dominance. Collectively they have the natural resources, means of production and cheap labor force to win.

Let the U.S. exhaust itself and drain its strategic petroleum reserve fighting high energy prices and defending Ukraine. Let Europe bury itself in debt as it subsidizes the electric bills for its citizens and abandons its climate goals in order to generate power.

“In December, the German grid was among the dirtiest in the developed world burning coal as its primary fuel…The speed with which they were able to bring back…old coal plants is really phenomenal…but they spent almost $0.5 trillion on this effort.”

Doomberg

Framing the Ukraine conflict about winning and losing understates what is really happening. This is about energy, the basis of the world economy. This is not a war that the west can won from an energy and demographic perspective. Let’s not forget that Vladimir Putin’s PhD dissertation was Mineral and Raw Materials Resources and the Development Strategy for the Russian Economy. He probably knows more about energy than all of the leaders of NATO combined.

A competing petroyuan reserve currency seems likely later in the decade. Credit Suisse analyst Zoltan Pozsar believes that this was the purpose of Xi Jinping’s recent meeting with Saudi Arabia and the GCC in December. He wrote in a note to clients that Xi “wants to rewrite the rules of the global energy market.”

Rana Faroohar explained the significance of these developments in a recent article:

“That would mark a massive shift in the global energy trade…China would not only dramatically increase imports from GCC countries, but work towards “all-dimensional energy co-operation.” This could potentially involve joint exploration and production in places such as the South China Sea, as well as investments in refineries, chemicals and plastics. Beijing’s hope is that all of it will be paid for in renminbi, on the Shanghai Petroleum and Natural Gas Exchange, as early as 2025.”

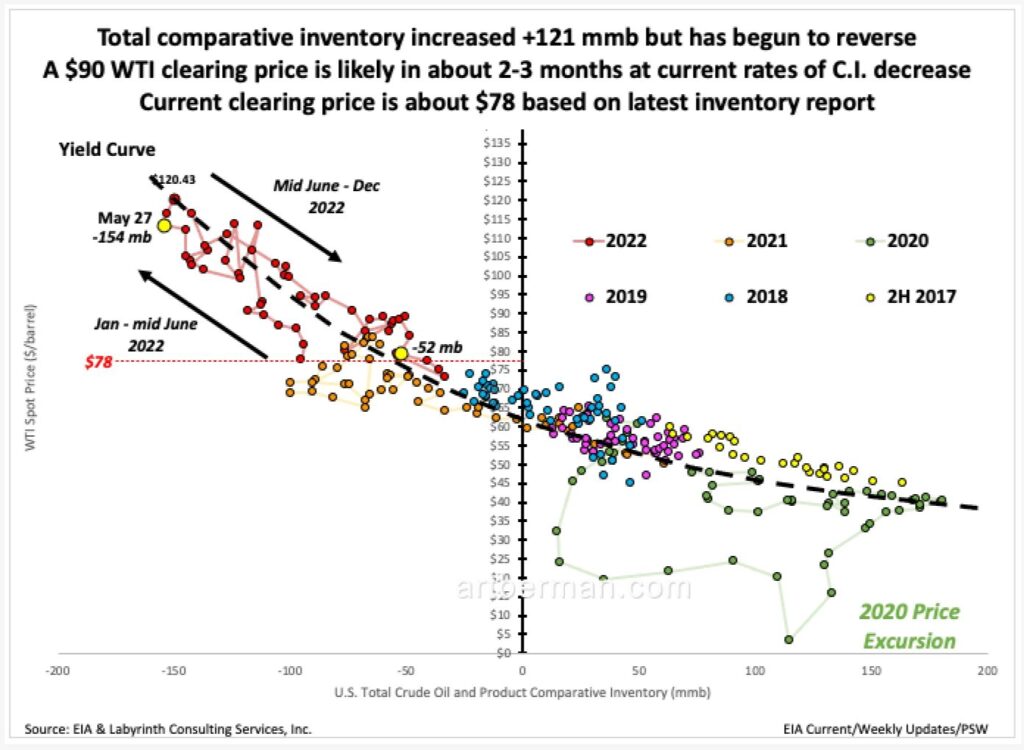

If oil price is all that matters, WTI is likely to move toward $90—and Brent a few dollars higher—some time in the first or second quarter of 2023. U.S. comparative inventory has begun to decrease again following its long increase in the second half of 2022. (Figure 3).

Based on the dashed black yield curve, WTI’s market-clearing price at current inventory levels is about $78 as of the EIA’s oil storage report published on January 5, 2023. The ending of U.S. SPR releases should result in a C.I. shift into greater supply deficit. Assuming that this proceeds at a similar rate as C.I. has increased since May, it should take about 2 to 3 months for WTI to reach $90 per barrel.

The problem with this—and all other forecasts—is that it assumes that prices will follow the patterns of the last 30 years. That is not given because of the fragmentation of the global market.

More importantly, oil price is not all that matters. It is a reflection and derivative of how effectively producers are meeting the world’s energy needs. A well-connected world with relatively few political and economic conflicts is what the market prefers.

From that perspective, high price is a failing grade. Those who celebrate high oil prices—the oil bulls—either do not understand this or are so selfishly motivated that they don’t care if the world is in trouble as long as they are making money.

Energy is the economy and oil is the most important part of energy today. When oil markets are stressed as they have been in 2022, problems with the global economy and broader markets are not far behind.

Morgan Stanley co-President Ted Pick summarized this a few months ago:

“It’s an extraordinary moment; we have our first pandemic in 100 years. We have our first invasion in Europe in 75 years. And we have our first inflation around the world in 40 years. When you look at the combination, the intersection of the pandemic, of the war, of the inflation, it signals paradigm shift, the end of 15 years of financial repression and the next era to come…Global markets may have reached a structural inflection point—an end to the era of ample liquidity, low inflation, and low interest rates that followed the 2008–2009 global financial crisis.”

Rana Faroohar insightfully captured the present state of world energy,

“On Valentine’s Day in 1945, US president Franklin Delano Roosevelt met Saudi King Abdul Aziz Ibn Saud on the American cruiser USS Quincy. It was the beginning of one of the most important geopolitical alliances of the past 70 years, in which US security in the Middle East was bartered for oil pegged in dollars.

“But times change, and 2023 may be remembered as the year that this grand bargain began to shift, as a new world energy order between China and the Middle East took shape.”

The 2020 global pandemic was a watershed event that completed a paradigm change for oil markets that began with the Financial Collapse of 2008. Key components of this shift are greater debt levels and the energy-blind expectation that fossil fuels can be quickly replaced by renewables. That left Europe unprepared after Russia invaded Ukraine. These forces are now breaking western economies.

That is the goal of those aligned against the old world order.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts