Art Berman Newsletter: June 2020 (2020-5)

Highlights

- Oil prices are converging on a secular mean in the $40 to $45 range for WTI.

- The rate of comparative inventory increase appears to be slowing.

- Rig count weekly decrease appears to be slowing.

- WTI will probably fluctuate in the $40 to $45 range in coming weeks and months.

- Rig counts should increase later in 2020 and prices should move up to $50 to $60 per barrel some time in 2021.

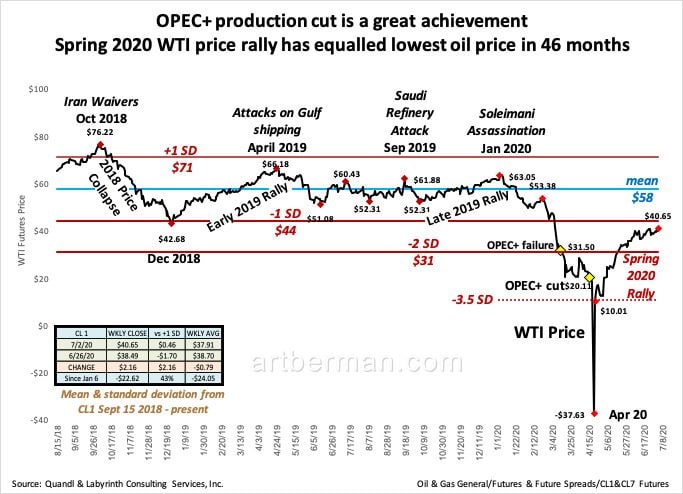

Oil Prices Have Stabilized

Oil prices have been in extraordinary flux falling from $53 to -$37 and back again to $41 per barrel (Figure 1). Even excluding the negative oil price on April 20, WTI reached 3.5 standard deviations below the 3-year mean of $58 in April. It is almost impossible to anticipate where a rally from those low levels will end.

Spring 2020 WTI price rally has equalled lowest oil price in 46 months.

Source: Quandl and Labyrinth Consulting Services, Inc.

Nevertheless, I have maintained since April that $40-$45 would be that level based on comparative inventory. Figure 1 shows clearly that prices are converging on the range that I anticipated. They may briefly exceed $45 and fall below $35 in coming weeks and months as the price discovery process proceeds. On a monthly average, I expect that $40 to $45 will be the WTI price range for the rest of 2020 barring a serious supply interruption.

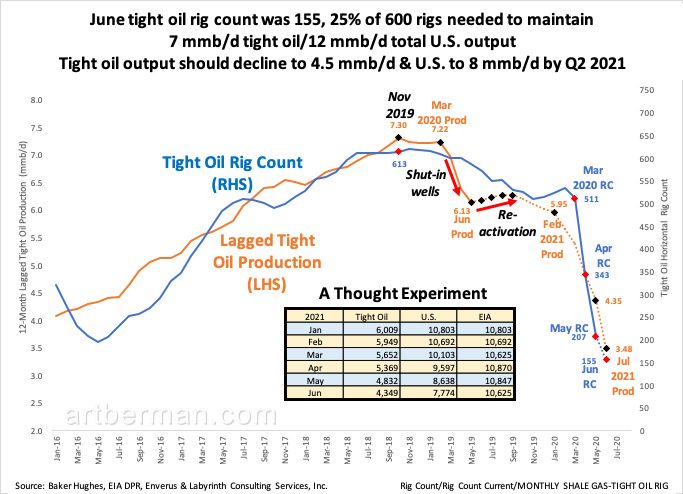

U. S. Supply Will Decline Next Year

The U.S. tight oil rig count is now 155 (Figure 2). That is about 25% of what is needed to maintain tight oil production at 7 mmb/d and U.S. total output at 12 mmb/d. That means that tight oil will irreversibly fall to less than 5 mmb/d and U.S. to less than 8 mmb/d by mid-2021.

The considerable lags and leads mean that production decline cannot be expected to reverse until well into 2021 assuming that it starts to increase immediately. That won’t happen because of constrained budgets and low oil prices.

Tight oil output should decline to 4.5 mmb/d & U.S. to 8 mmb/d by Q2 2021.

Source: Baker Hughes, EIA DPR, Enverus & Labyrinth Consulting Services, Inc.

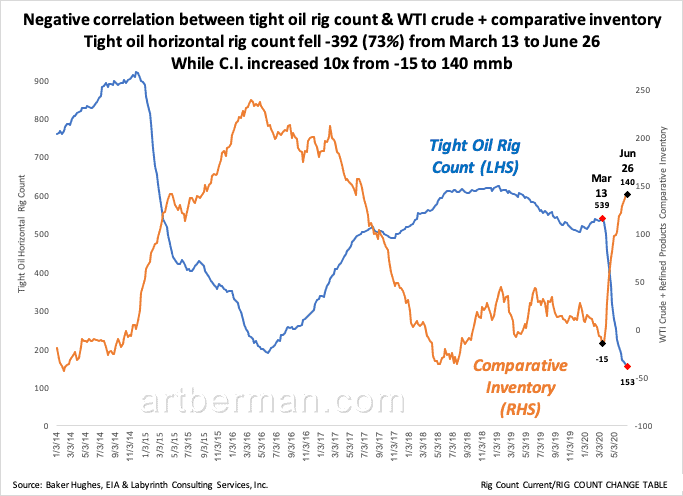

It is impossible to predict when rig count might begin increasing again. Empirically, there is a negative correlation between tight oil rig count & WTI crude + comparative inventory (Figure 3). Tight oil horizontal rig count fell -392 (73%) from March 13 to June 26 while C.I. increased 10-fold from -15 to 140 mmb. Outside capital was available after the 2014-2016 oil-price collapse that may not be available this time. At the very least, rig count won’t begin to reverse until U.S. storage begins to decline and that has not happened yet.

The implications of plunging rig counts are enormous not only for U.S. but also for world oil supply since tight oil has accounted for all of global growth since 2010. There are clearly huge uncertainties between now and mid-2021. The largest among these is a global economic depression caused largely by the Covid-19 epidemic.

There is a low probability that the pandemic will end or be under control any time soon.

“I’m not sure that the influenza analogy applies anymore…Right now, I don’t see this slowing down into summer or end of fall. I don’t think we’re going to see one, two and three waves. I think we’re going to see one very, very difficult forest fire of cases.”

Dr. Michael Osterholm, Director, Center for Infectious Disease Research and Policy at the University of Minnesota

Its toll on economic activity and human life will be far greater than many predict and what is advertised by politicians. If Dr. Osterholm is correct, the drop in oil supply may consistent with the decrease in supply that the horizontal rig count indicates. If, on the other hand, oil-demand and economic activity recover according to the mainstream view, supply will become tight and prices should increase.

For now we see through a glass, darkly

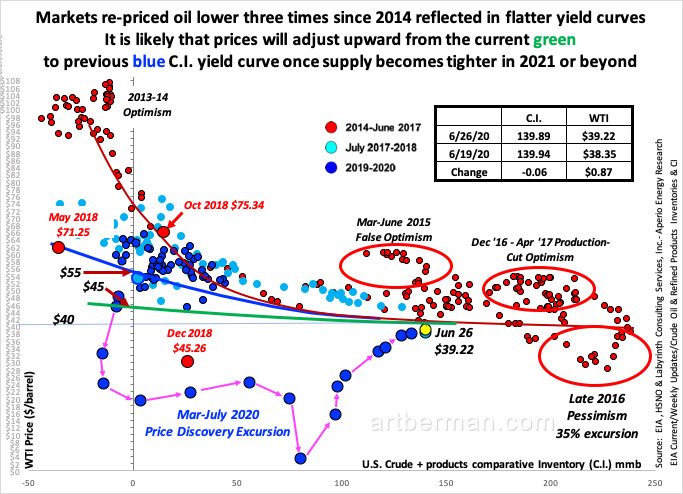

Markets re-priced WTI lower three times since 2014 reflected in flatter comparative inventory yield curves (Figure 4). It is likely that prices will adjust upward from the current green to previous blue C.I. yield curve once supply becomes tighter in 2021 or beyond.

It is likely that prices will adjust upward from the current green

to previous blue C.I. yield curve once supply becomes tighter in 2021 or beyond.

Source: EIA and Labyrinth Consulting Services, Inc.

Most analysts agree that it is foolish to predict oil prices. This is true for the short-term daily or weekly fluctuations. Once a baseline is established from price discovery following market disruption, price formation is fundamentally rational and systematic until the next secular change. I expect WTI to largely follow the blue yield curve in Figure 4 for as long as surplus inventories dominate oil markets.

Price, inventories, rig counts, supply and demand are all related in complex response relationships. Knowing the appropriate ways to measure and analyze those interrelated components is critical to understanding the dynamics of price formation.

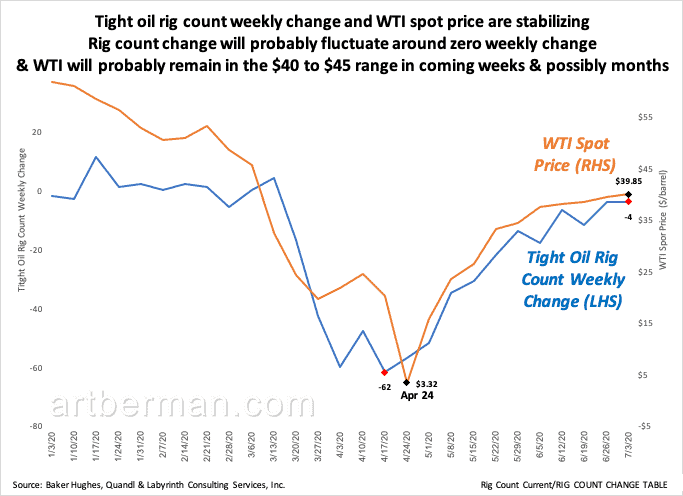

U.S. tight oil rig count weekly change appears to be stabilizing. Not surprisingly, the rate of WTI spot price change is also decreasing (Figure 5).

Rig count change will probably fluctuate around zero weekly change

& WTI will probably remain in the $40 to $45 range in coming weeks & possibly months.

Source: Baker Hughes, Quandl & Labyrinth Consulting Services, Inc.

This supports my expectation that WTI prices should average $40 to $45/barrel in coming weeks and possibly months. When C.I. decreases enough to persuade markets that a secular change has occurred, rig counts will increase and prices should move back to the blue yield curve and average $50 to $60 per barrel.

It would be foolish to predict when that may occur. I doubt it will be in 2020.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts