Art Berman Newsletter: June 2021 (2021-5)

WTI futures price reached the highest level in more than two-and-a-half years this week. That should be good for the oil industry but the headlines proclaim that the age of oil is over.

The International Energy Agency dropped a bomb on May 17 with a report called “Net Zero by 2050: A Roadmap for the Global Energy Sector.” It calls for an end to approvals for all new oil and gas fields, and coal mines and plants in 2021.

“We do not need any more investments in new oil, gas and coal projects.”

Fatih Birol, Executive Director International Energy Agency

A week later, there were three announcements that some said would change the oil and gas industry forever.

A Dutch court ordered Shell to cut total emissions by 45% within 10 years. On the same day, ExxonMobil activist investors added three of their own climate-friendly nominees to ExxonMobil’s board after warning that the producer faced an “existential risk” from its fossil fuel focus. In a similar move, Chevron investors forced that company to set more stringent emission targets on the petroleum products that it sells.

Climate and environmental industry lobbyists declared May 26 “Black Wednesday.” It would forever be remembered, they said, as the day when everything changed for Big Oil. These stinging defeats mean that the days of big oil infamy are now over.

“Wow. We’re clearly witnessing the beginning of the end of the fossil fuel era. They’re starting to panic. Let’s speed up the process.”

Greta Thunberg

The truth is that absolutely nothing has changed because of the Black Wednesday announcements or because of IEA’s report. To borrow the language of the IEA roadmap, these are simply a few new milestones along the energy-blind detour to nowhere. Holman Jenkins described it as a case of “activists substituting crowd-pleasing potshots at ‘big oil’ for the climate policy victories they haven’t won.”

But the oil industry has much bigger problems than some clashes with investors and courts about climate policy and emission levels. The substantial threat to oil companies is limited access to capital because of poor financial performance.

Investors have been painfully clear about what needs to change: better cash flow statements and less emphasis on growth. The companies have delivered but the investors have not reciprocated with capital. That’s because the new E&P business model that they demanded is unattractive to them!

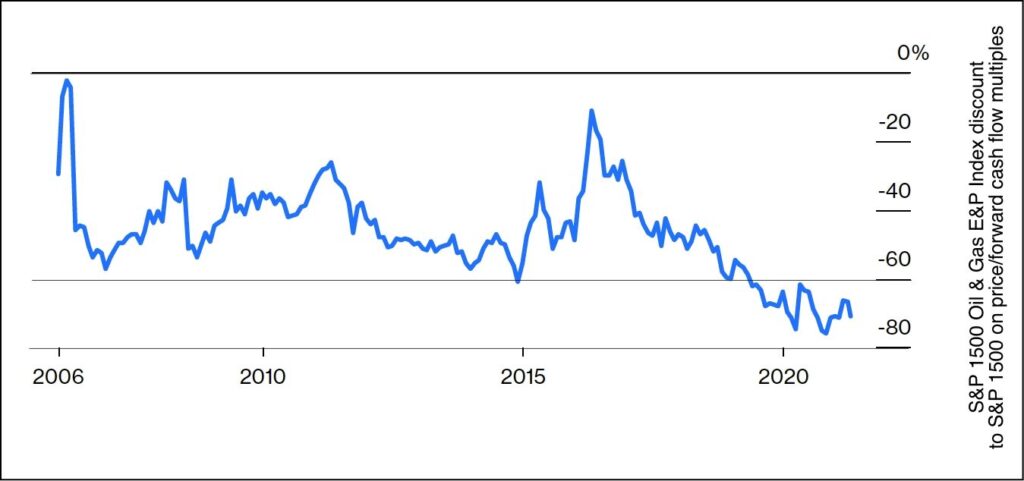

Energy stocks are having a great year so far in 2021. Share prices are beating the broader market by more than 25% but investors aren’t impressed. In fact, oil and gas companies multiples are discounted about -70% compared to the broader S&P 1500 (Figure 2).

Figure 2. Oil and gas companies multiples are discounted about -70% compared to the broader S&P 1500. Source: Bloomberg and Labyrinth Consulting Services, Inc.That’s because companies aren’t spending enough money to have a growth story.

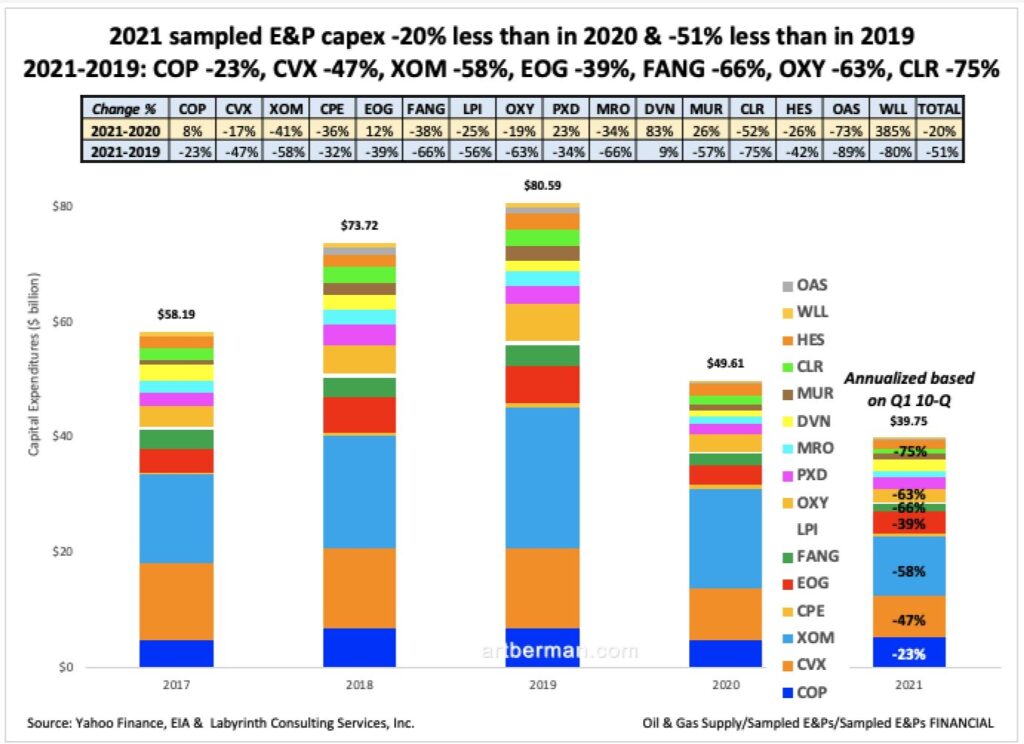

Figure 3 shows full-year capital expenditures (capex) for the oil-directed E&Ps that I follow. 2021 was annualized from first quarter data using historical ratios of first quarter-to-full year amounts.

Capex is likely to be about -20% less than in 2020 and -50% less than in 2019. The table shows those comparisons for each company but only Conoco (COP), EOG, Pioneer (PXD), Devon (DVN) and Whiting (WLL) plan to spend more money on drilling in 2021 than in 2020.

U.S. oil production fell -935 kb/d from 12.25 to 11.3 mmb/d in 2020. If companies spend -20% less on drilling in 2021, they will be lucky to maintain much less grow production levels regardless of technology, cost reductions or increased reliance on drilled, uncompleted wells.

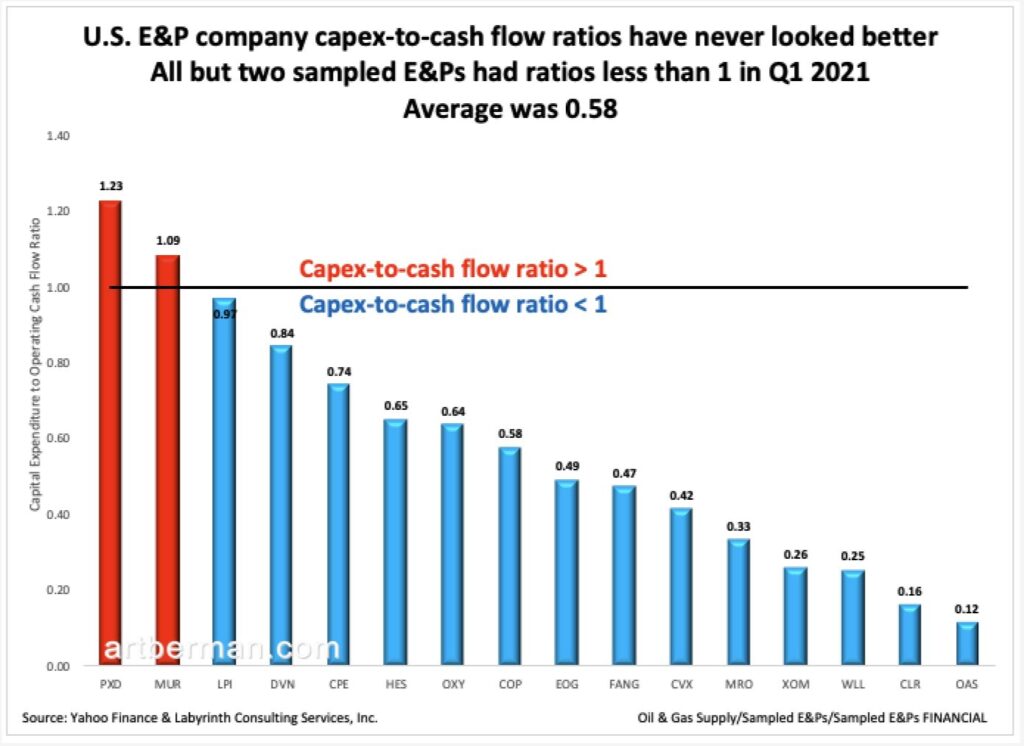

Investors have been telling oil companies that they need to show cash flow instead of growth as a pre-requisite for renewed investment.

Capex-to-cash flow ratios have never looked better. All but two sampled E&Ps had ratios less than 1.0 in Q1 2021 and the average was 0.58. That means that companies are making more money than they are spending. Isn’t that exactly what investors have been demanding?

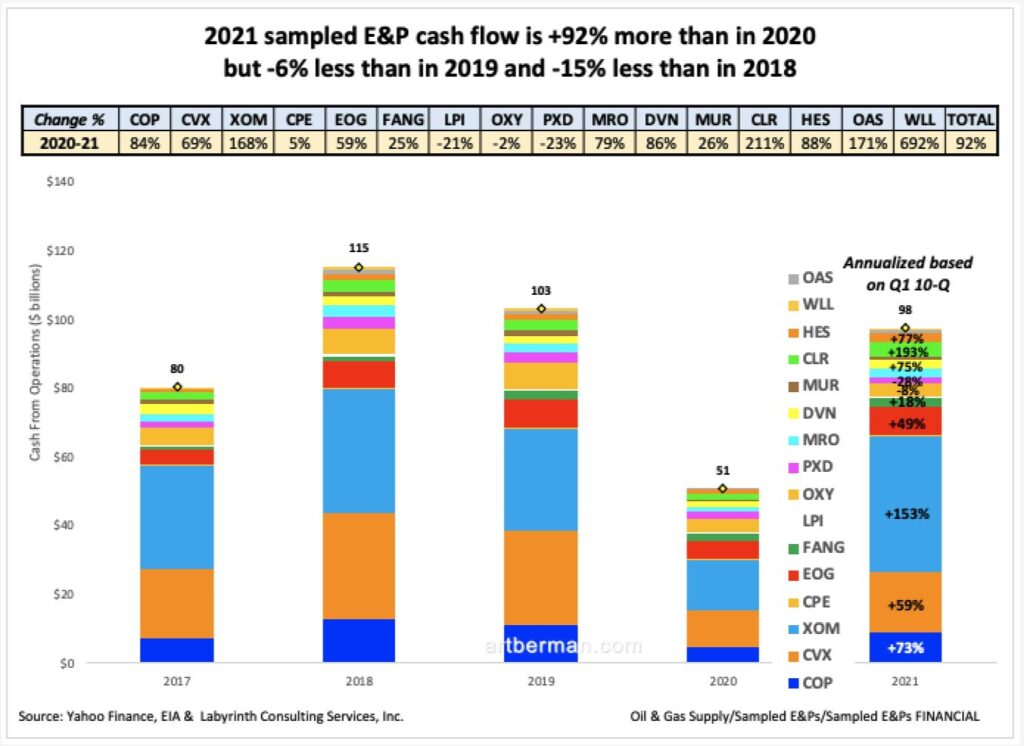

Figure 5 shows full-year cash flow with first quarter 2021 data annualized using historical ratios of first quarter-to-full year amounts.

2021 cash flow is likely to be more than +90% more than in 2020 but -6% less than in 2019 and -15% less than in 2018. Investors may acknowledge the improvement but are not excited enough to give money to oil companies to grow.

U.S. oil production growth over the last decade was enabled by almost unlimited credit. Oil prices reached more than $140 per barrel in 2008 because markets felt strong and appropriate urgency about global supply.

World production was flat from 2004 through 2011 (Figure 6). Conventional, deep water and oil sand plays could not be developed fast enough to offset depletion of older fields. Crude oil and condensate was stuck at about 74 mmb/d. Demand was growing especially in Asia and prices were exceptionally high (despite an interruption during the 2008 Financial Collapse) from 2003 until the middle of 2014 as markets signaled producers to drill.

Tight oil development was only possible because of stable, high oil prices and the easy money monetary and banking policies that followed the 2008 crash.

Figure 6. Flat world production led to 2003-2014 oil super-cycle. Tight oil added 10 mmb/d of supply and ended the super-cycle. 2020-21 lower output not a supply problem but artificial from OPEC cuts & less drilling. Source: EIA, Cansim, Enverus & Labyrinth Consulting Services, Inc.

Tight oil delivered the supply that markets demanded but piled up a mountain of debt in the process. When prices collapsed in 2014, the cash flow from high prices dissolved but the debt remained. The second tight oil boom from 2016 until the Covid economic collapse in 2020 provided similar credit benefits to a more select group of E&Ps than during the first.

Investors became disaffected with tight oil some time in mid-2018. Their complaint was lack of cash flow and too much debt. Capital availability contracted. Climate concern was less of a factor than it is today.

E&Ps emerged from the 2020 collapse even more deeper in debt and almost completely cut off from outside capital.

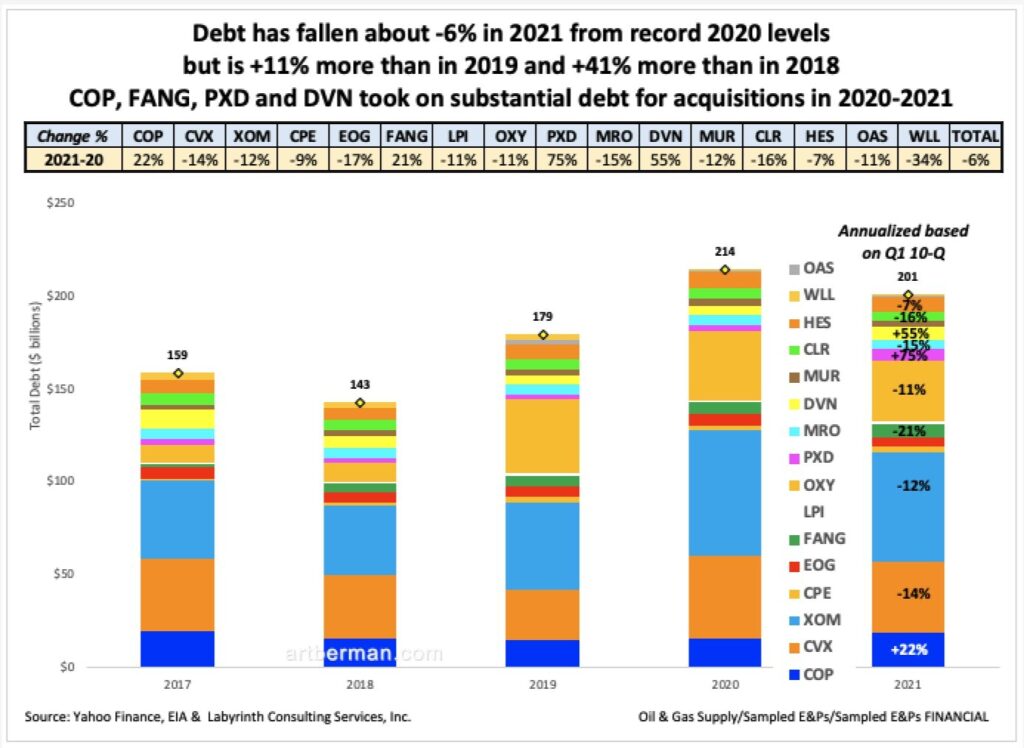

Figure 7 shows that 2020 debt was about +20% higher than it had been in 2019. Companies struggled to reduce that burden but appear poised to end 2021 about -6% lower than in 2020. And yet, 2021 debt will be about +19% higher than it was in 2019 and +41% more than in 2018.

The 2021 debt picture is complicated by the fact that several of the sampled E&Ps acquired other companies thus increasing debt offsetting decreases by their peers. Notably, Chevron bought Concho, Diamondback bought QEP and Guidon, Pioneer bought Parsley and Double Point, and Devon bought WPX. Notably, although not in 2021, Oxy’s purchase of Anadarko in 2020 greatly increased its debt load.

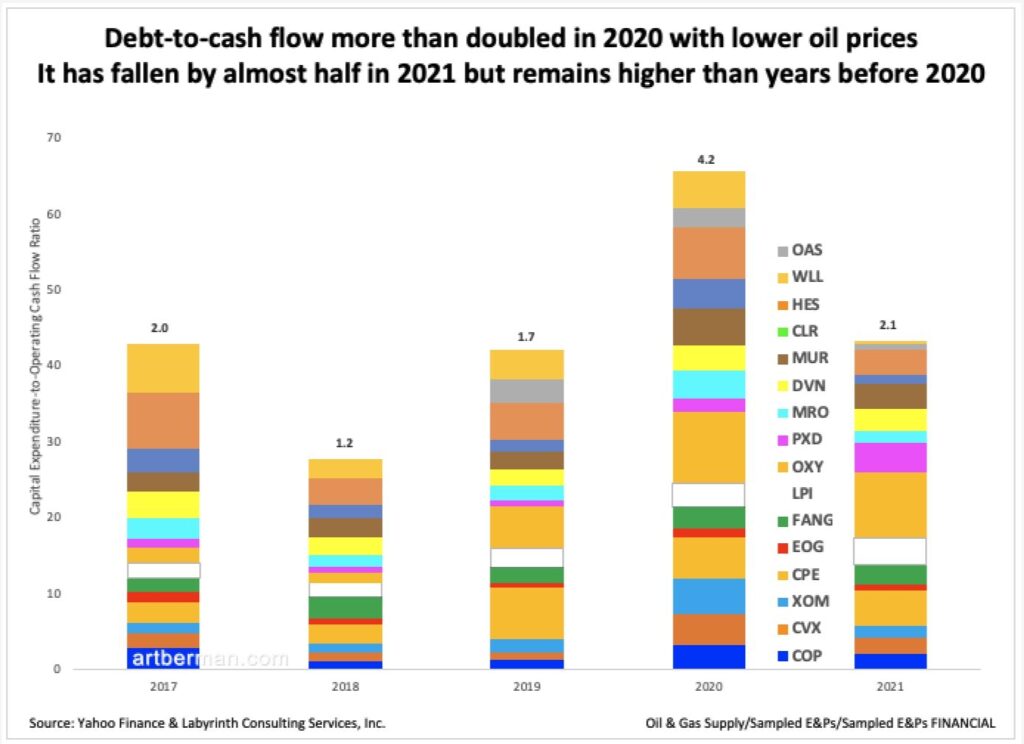

In the glory years, investors didn’t care so much about debt but were somewhat sensitive to debt-to-cash from operations ratios since that is a measure of how long it might take to pay down debt.

Debt-to-cash flow more than doubled in 2020 as cash from operations plummeted with low oil prices and companies added debt to survive that worst of all years in the U.S. oil business (Figure 8). The ratio increased from 1.7 in 2019 to 4.2 in 2020.

2021 is projected to be a far better year with debt-to-cash flow falling to 2.1 but that remains higher than in all years shown before 2020.

I have observed and written about the love affair between investors and shale companies for 15 years. I was among shale’s strongest critics because of their obsession with growth at the expense of cash flow and manageable debt. Investors were steadfast in their infatuation with these companies until they weren’t.

What happened that made them fall out of love?

The answer is fairly straight-forward: investors weren’t making the kind of money that they did during the second shale boom.

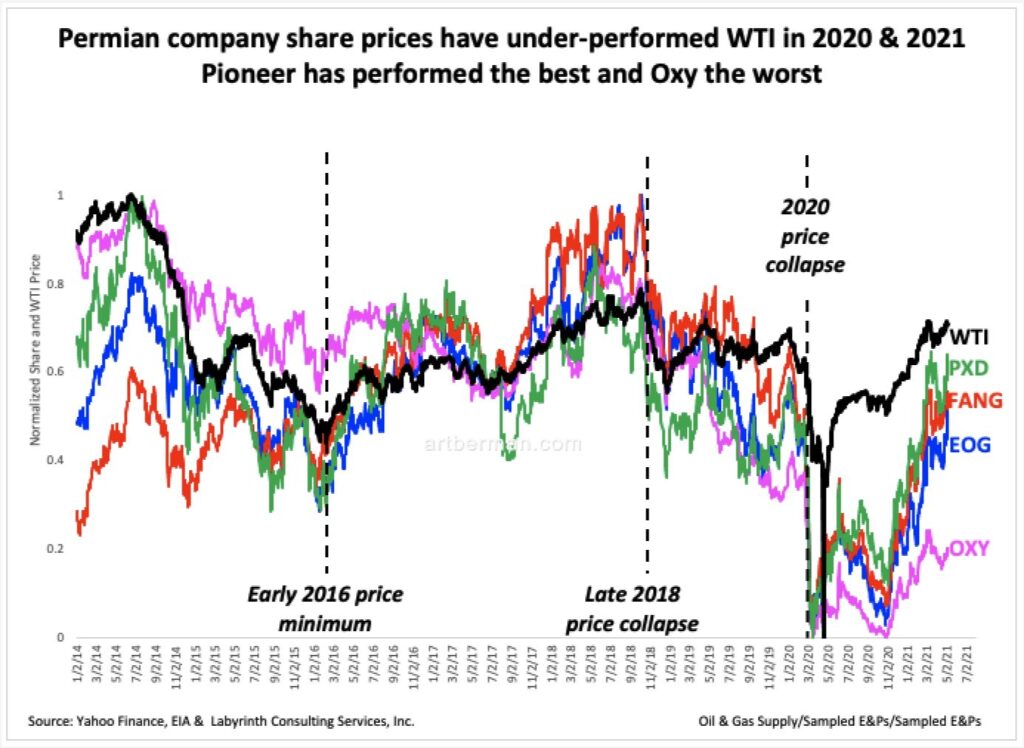

I have normalized company share prices and WTI spot price for four of the relatively pure Permian players in Figure 9: Pioneer (PXD), Diamondback (FANG), EOG and OXY. It shows that share prices for all of the companies out-performed WTI for much of the period between the early 2016 WTI price minimum and the late 2018 WTI price collapse. In 2019 and the first few months of 2020, most companies under-performed WTI. Since March of 2020, all have significantly under-performed WTI although prices have improved in recent months.

Investors didn’t care a bit about negative cash flow when oil prices were in the toilet in 2016 and companies were going bankrupt. That’s because oil prices could only go higher. Smart capitalists were not investing in the companies but rather, were playing their stock or collecting a coupon on their bonds. Free cash flow was not part of their calculus. Neither was debt.

The stock play was better than casino gambling. WTI price almost tripled from $26 in early 2016 to $76 by late 2018. Buying and selling tight oil company stocks was a great way to ride that wave without the risks of commodity trading. An investor who bought shares of tight oil companies in 2016 and held them until late 2018 would have made an average profit of 181%. By moving in and out of stocks during higher frequency price fluctuation, even greater profits were possible.

Investor flight began when oil prices approached and then, exceeded the cost of the marginal barrel–about $60 per barrel for WTI. That happened in the last two quarters of 2018. No more free money. Then, prices collapsed in November 2018 and investors were out.

Why didn’t investors return after April 2020 when prices reached historical lows? Some did but the enthusiasm and momentum was gone from the plays. Investors had moved on and probably had started to believe their own stories about cash flow and debt. Perhaps more importantly, the tide of public opinion about climate change and ESG had shifted. Oil plays were passé.

The companies have demonstrated discipline balancing profits and growth, are cash-flow positive, and have debt-to-cash flow ratios within reasonable limits. Spot WTI is near $70 per barrel but U.S. output slipped below 11 mmb/d this week.

Investors demanded fiscal & growth discipline from tight oil. Tight oil delivered but investors are uninterested because there’s no growth story. Bait-and-switch.

I am surprised that the same executives who masterfully peddled the dream of Saudi America have now tacitly conceded defeat to green energy. The eight largest publicly traded oil and gas companies have announced plans for net-zero carbon emissions and some have stated plans to transform themselves into renewable energy companies. None, however, have pushed back against the green tide and made the obvious case for oil and gas as the central component for economic growth and political power.

I believe that climate change is a threat to the environment and perhaps even to human civilization. Many thoughtful people disagree and doubt that it is a crisis. Public opinion about climate change, however, is a threat to the future of the oil and gas industry.

The global transition to a petroleum-based economy was responsible for the growth and prosperity of the last 75 years. The momentum today for a transition to an electric-based, decarbonized economy will unavoidably result in an end of economic growth.

It is pointless to debate whether climate change is real or is an emergency, or whether it is because of natural forces or human activity. That train left the station while people were arguing in the parking lot. I do not advocate a position. I recommend that investors position themselves based on what I have described.

Much of the net zero emission discussion today is based on profound energy blindness. I am betting that oil and gas supply will become a more pressing near-term emergency than climate change over the next few years.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Thanks for the reply, I am thinking about RIG and the Russian arctic. However you cut the cake, time is running out.

Is offshore drilling worth a deeper look?

Everything is worth a deeper look. I believe that most of the reserves are known although there will be more discoveries of smaller fields. That, at least, is the history of plays.

Best,

Art

excellent info – thanks