Art Berman Newsletter: June 2022 (2022-5)

Oil supply cannot meet rebounding demand. Oil markets are surging again now that China’s Covid lockdowns are ending.

WTI had climbed from $66 in early December to $92 by late February (Figure 1). Then, Russia’s invasion of Ukraine drove price to almost $124 in early March. China’s March through May lockdowns cooled oil’s 2022 rally and depressed prices into the $90 range. Now, with that in the past, prices have increased to almost $120.

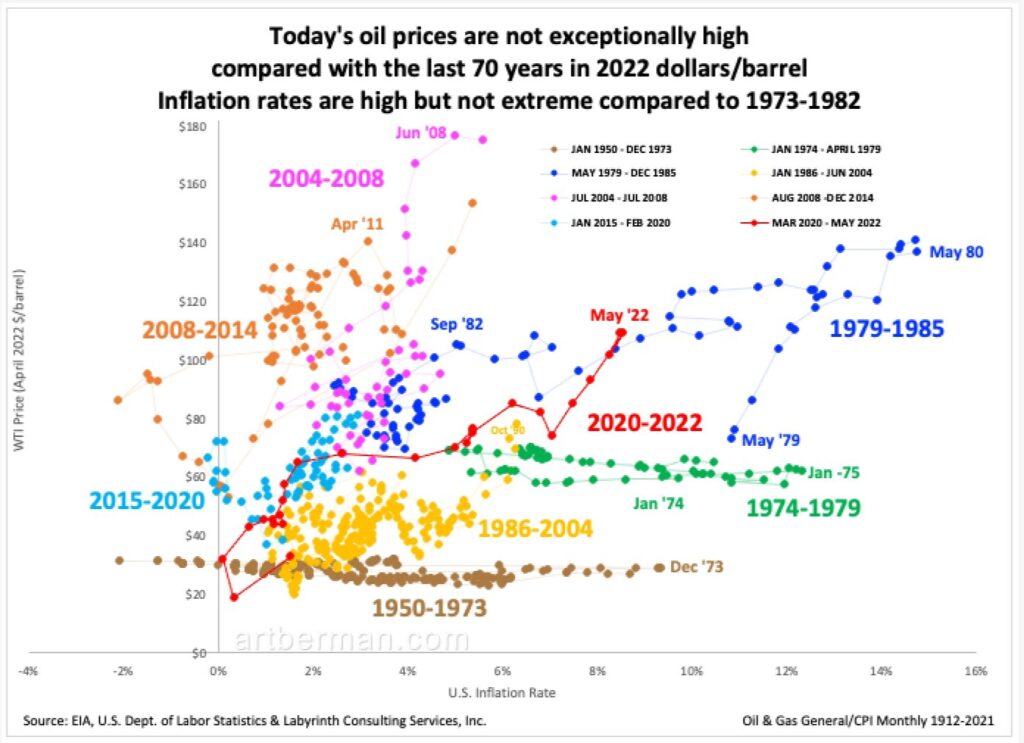

WTI spot price has averaged $100 per barrel so far in 2022. That’s a lot higher than it has been for the last eight years but it’s not that high compared with earlier periods. The May average WTI price of $110 was 27% lower than the 1980 and 2011 price peaks in 2022 dollars (Figure 2). It was 38% less than the 2008 peak.

Inflation has re-entered public consciousness after more than a decade in the shadows. As the world recovers from the pandemic, the price of everything has increased.

Figure 3 shows the same data as in Figure 2 but cross-plotted rather than as a time series. It emphasizes that today’s oil prices are not exceptionally high compared with the last 70 years in 2022 dollars/barrel. It further underscores that while inflation rates are high they are not extreme compared to 1979-1985.

The flat brown data points reflect the Texas Railroad Commission’s artificial control of world oil prices until U.S. production peaked in 1970 and market forces took over.

Some analysts believe that the upper limits of oil price are unconstrained by past history because circumstances are so different today after the pandemic and a decade of exploration and production under-investment. They see the 2004-2008 data (magenta in figure 3) and find no reason that prices should not reach similar levels in 2023.

They may be right based on supply limitations but the demand side of things is considerably different today. The early 2000s were characterized by the rise of China as the world’s largest consumer of imported oil. Today, China’s growth has reached a more mature level, Covid lockdowns notwithstanding.

The price of oil and inflation have tracked one another as closely as is anything in the real world for the last decade-and-a-half (Figure 4). What’s different today is that inflation is substantially higher than at any other time in that period. It is, in fact, at the highest level since late 1981 (Figure 2).

Figure 4. Strong correlation between U.S. inflation and WTI oil price. Source: EIA, U.S. Dept. of Labor Statistics & Labyrinth Consulting Services, Inc.It is understandable that inflation baffles the consumer. It is more difficult to explain why many economists don’t see the correlation between energy prices and inflation.

Goldman Sachs’ Damien Courvalin recently noted in an interview that “supply elasticity is close to nil.” When asked about recession concerns he said, “The output gap is tighter in energy than anywhere else in the economy.” Responding to a direct question about demand destruction, he stated that a $125 per barrel might slow price growth but implied that there was room to move higher than that threshold.

Analysts sometimes refer to demand destruction but are rarely as direct as Courvalin, but his response still leaves me wanting something more substantial.

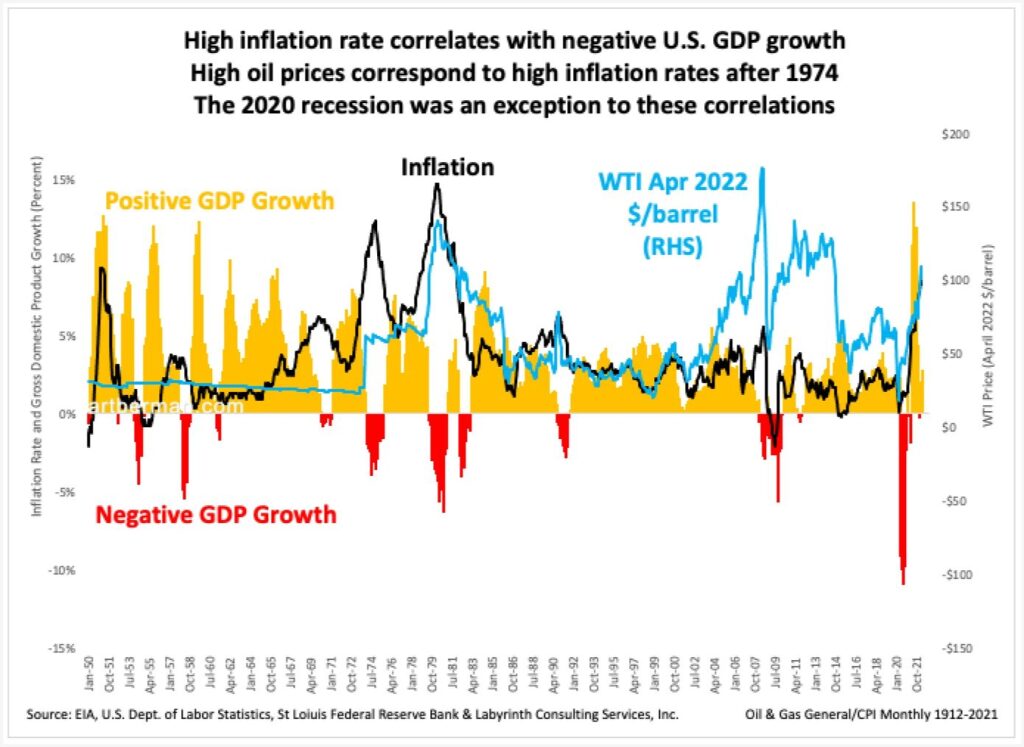

Figure 5 shows inflation and WTI price but adds the economic dimension of GDP (gross domestic product) growth. Periods of high inflation rate correlate with negative U.S. GDP growth. High oil prices correspond to high inflation rates after 1974 although the 2020 recession was an exception to these correlations.

The implications of Figure 5 are chilling. The rate of 2021 and 2022 inflation growth is only comparable to the period of oil shocks in the 1970s and early 1980s. Those correspond to negative GDP growth. Economists may explain this differently but it seems obvious that sharply higher oil prices were probably the main factor behind inflation then and now.

Let’s now return to the question of demand destruction. U.S. oil consumption has fallen in every period of inflation increase since 1970 (Figure 6).

Consumption fell more than 1 mmb/d during the first oil shock from 1972 through 1976. It dropped almost 4 mmb/d during the second oil shock from 1976 through 1983, and it fell 2 mmb/d in 2008-2009.

Consumption is not the same as demand because demand includes exports. It is, however, a reasonable proxy for long-term demand because the U.S. did not become a significant exporter of refined products until about 2010 and was not an exporter of crude oil until 2016. At the very least, U.S. consumption reflects domestic demand by the biggest consumer and the largest economy in the world.

The onset of & degree of demand destruction varies for each U.S. oil price-inflation cycle as do the onsets of price increase and inflation but demand destruction occurs within every cycle since 1972 (Figure 7).

The significance of this chart cannot be over-stated. History does not give us a clear map showing when demand destruction will occur and how long it will last. It does, however, indicate that the extraordinary increase in oil price and inflation over the last 18 months will almost certainly reduce oil demand by a substantial amount.

The data suggest that demand may decrease by 500 – 750 kb/d annually for two to three years. This may begin in a few months or some time next year. It is always possible that this time is different from the last 75 years but I doubt it. Add to that that lower or negative GDP growth accompanies higher oil prices, and lower demand looks increasingly probable.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

A needed perspective on the demand side. Demand is the tricky part so thanks for taking a stab at it.

Thanks!