Art Berman Newsletter: March 2022 (2022-2)

The price of energy has moved from high to higher with the Russian invasion of Ukraine. Traders and shipping companies are unwilling to take Russian oil.

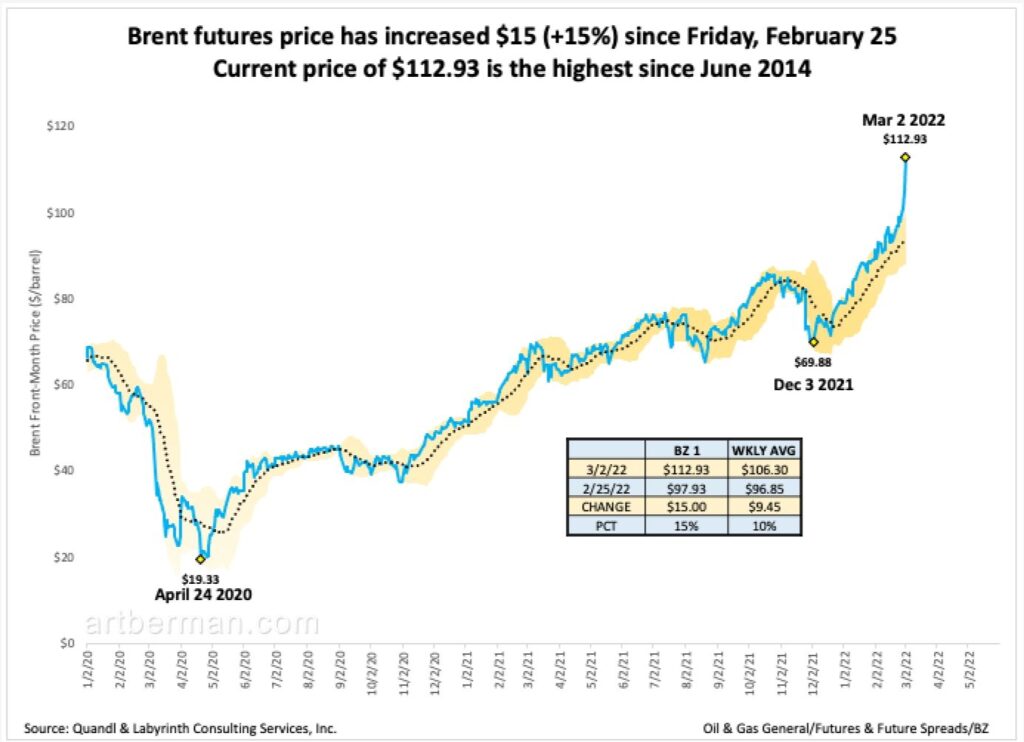

Brent futures price closed at almost $113 on March 2. Price has increased $15 (+15%) since Russia invaded Ukraine last week (Figure 1). The current price of $112.93 is the highest since June 2014.

Russia produced 10.6 mmb/d of crude oil and condensate in January—only the U.S. produced more at 11.6 mmb/d. Europe gets about 25% (2.5 mmb/d) of its oil from Russia and most Russian crude trade is currently frozen because of sanctions, freight interruptions and wider political risks.

Ural crude is being deeply discounted but sellers can find few buyers. The market capitalization of the four Russian oil and gas majors has fallen 95% since the Ukraine attack began. Ukraine and Russia provide approximately 25% of the world’s wheat supply, and Russia and Belarus are the world’s second and third largest suppliers of potash and nitrogen for fertilizer.

With all of that in mind—not to mention the risk of nuclear war—the higher price of oil is hardly surprising. In last month’s newsletter, I made the case that higher prices were inevitable based solely on supply urgency. Goldman Sachs’ Jeff Currie’s comment in that newsletter bears repeating.

“This market is incredibly vulnerable to any supply or demand disruption…The question is, Can you come up with any supply or reduction in demand as you move into the Spring to be able to ease the situation.”

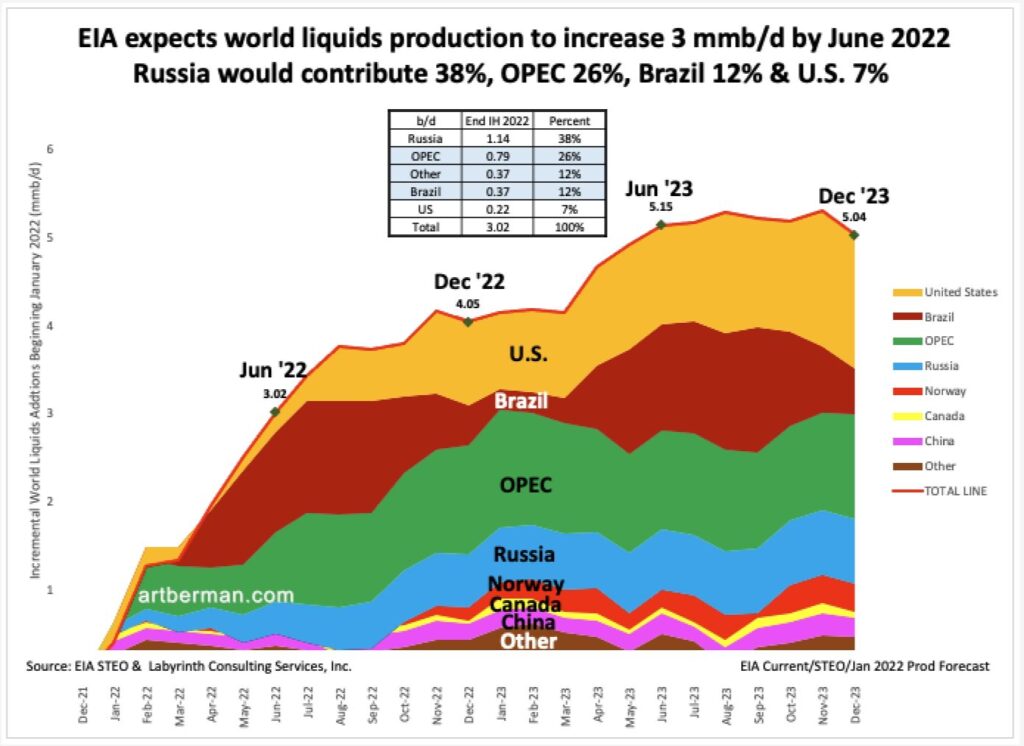

EIA expected about 38% of new oil supply to come from Russia in its latest Short-Term Energy Outlook (Figure 2). That now seems even more unlikely than it did a month ago. OPEC agreed to maintain its approximately 400 kb/d monthly increase so EIA’s projection of 26% may be reasonable. Much of Brazil’s contribution is corn ethanol so that invites the question of whether the U.S. shale patch can somehow come to the rescue of world oil supply.

Figure 2. EIA expects world liquids production to increase by 3 mmb/d by June 2022. Russia would contribute 38%, OPEC 26%, Brazil 12% & U.S. 7%. Source: EIA STEO & Labyrinth Consulting Services, Inc.

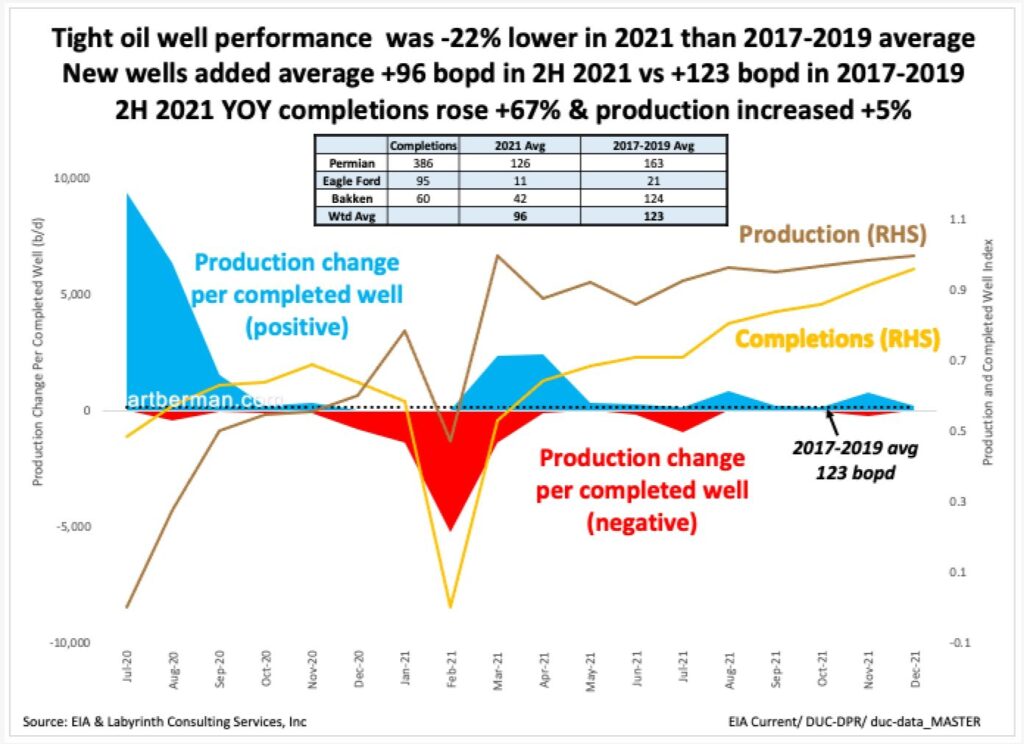

I use EIA’s monthly Drilling Productivity Report (DPR) as a high-level source for tight oil volumes, completions and drilled, uncompleted well percentages. Figure 3 shows the monthly increase and decrease in tight oil production divided by the number of newly completed wells with positive change in blue and negative change in red. The average for 2021 was 96 b/d per newly completed well. That was 22% less than the 2017-2019 average of 123 b/d.

Tight oil production (brown) and the number of completions (gold) are shown as indices on the right-hand scale. It appears that production is increasing despite poorer per-well production rates largely because of the large numbers of new well completions compared to 2020 through mid-2021 levels.

Some part of lower production rates may be because of the large percentage of drilled, uncompleted wells (DUCs) in 2020. That is because the DUCs may not be represent the better wells or they would have been completed previously. Producers resorted to completing these wells because it was cheaper to pay for their completion rather than to drill and complete a new, potentially better, well.

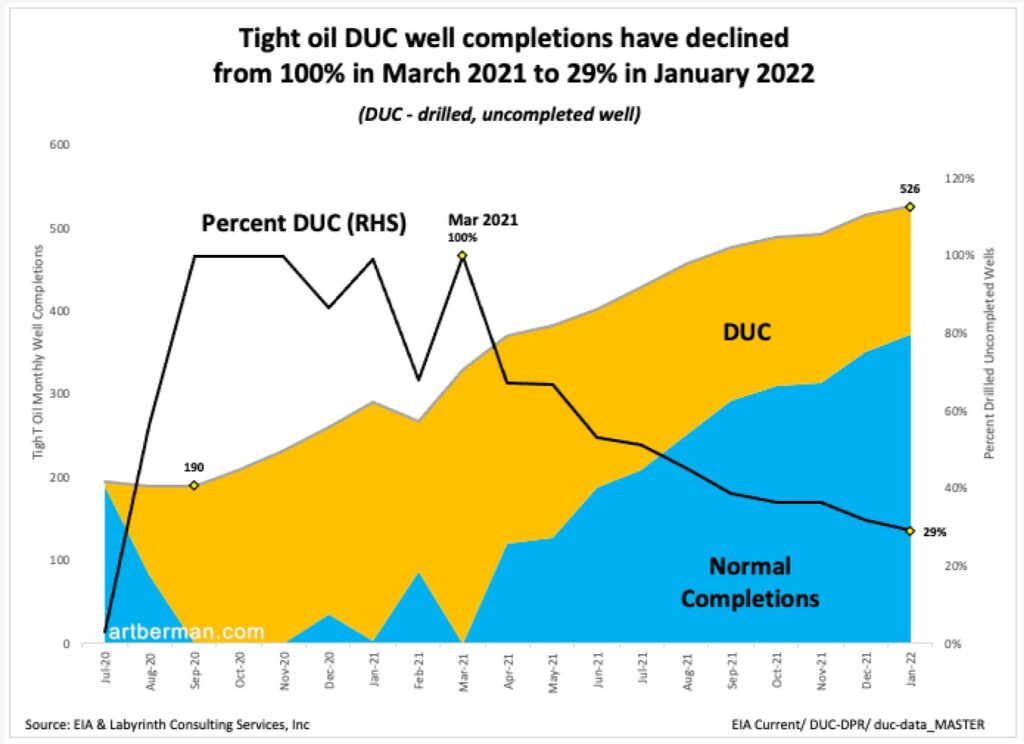

Reliance on DUCs has changed in 2021. Tight oil DUC well completions have declined from 100% in March 2021 to 29% in January 2022 (Figure 4).

In order to test the DPR data, I evaluated the performance of Permian basin tight oil wells from the Trend Area. This includes the Spraberry and Wolfcamp plays and accounts for almost half of Permian tight oil production. Leading operators include Pioneer Natural Resources, Chevron, EOG, ConocoPhillips and Diamondback.

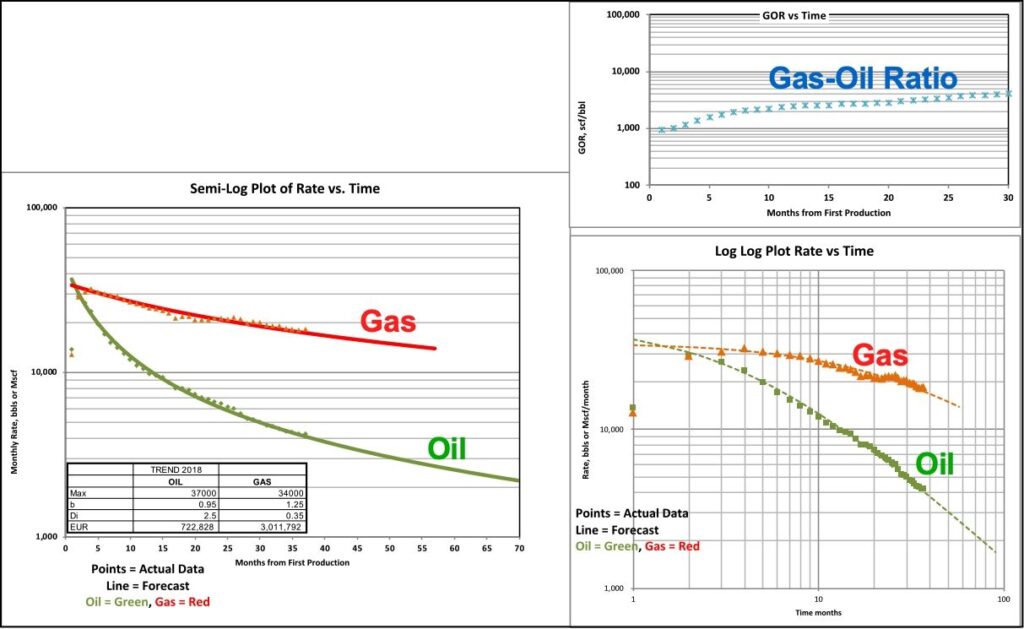

I did standard rate vs. time decline-curve analysis for approximately 4,000 horizontal wells with first production in 2018, 2019 and 2020. I then projected estimated ultimate recovery (EUR) for each vintaged group of wells. Figure 5 shows the history matching for 2018 wells on both semi-log (lower left) and log-log (lower right) plots, and the gas-oil ratio (upper right).

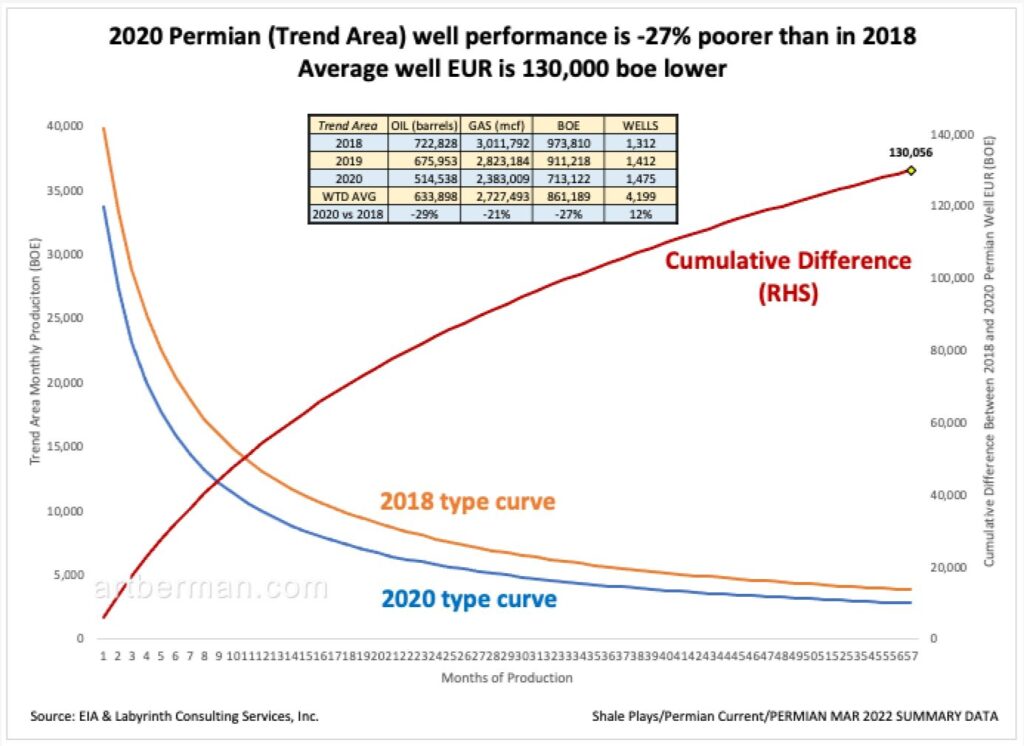

Figure 6 shows the results both as a table and as a graphic comparison of 2018 and 2020 wells. The 2020 type curve (blue) has a lower initial flow rate than the 2018 type curve (orange), a steeper decline rate and a lower EUR. Wells with first production in 2020 had 27% lower EUR than wells with first production in 2018. The cumulative difference between the two curves is shown in red and amounts to 130,000 barrels of oil equivalent.

Higher oil prices will help but this analysis suggests that a surge in U.S. tight oil production is unlikely.

Recent events in Ukraine introduce unthinkable uncertainty into energy markets and the world order that may emerge. Geopolitical consequences are likely to be the most serious in decades. Whatever the military outcome, the Russian economy will probably be ruined. It is difficult to imagine what may happen to the leadership of Russia. Even if Putin maintains power, the level of economic unrest, repression and violence may become extreme. The use of nuclear weapons seems greater than at any time since the 1960s.

Higher energy prices were likely before events in February. Even higher prices seem inevitable even in the most benign forward scenarios that I can imagine. The pandemic was an extraordinary disruption. The energy transition complicated its effect. I cannot comprehend how the devolution of Russia will amplify the already fragile state of world energy and economic systems.

“When you get something that’s disruptive, it creates fragmentation within countries and fragmentation among countries.”

Ed Morse, Citigroup

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts