Art Berman Newsletter: March 2023 (2023-3)

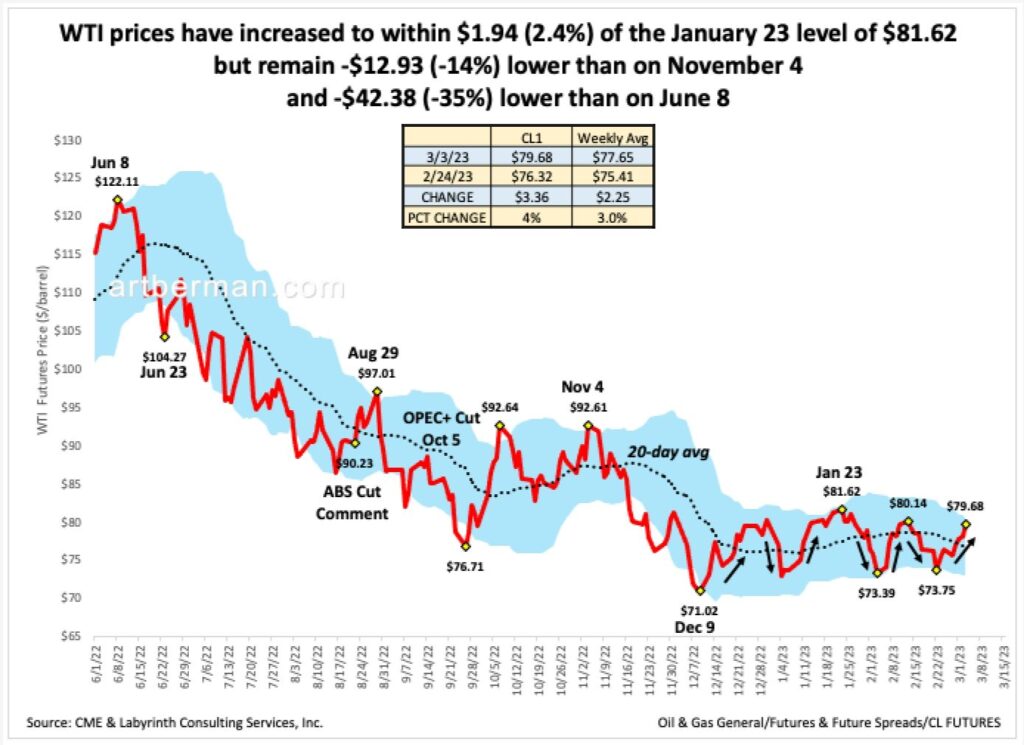

Analysts continue pitching the idea that oil prices are about to cross a threshold into a brave new world of supply-demand deficits. Indeed, WTI futures prices have increased almost $6.00 (+8%) from $73.75 to $79.68 since February 23 (Figure 1).

This time, however, is not very different from the three previous short-cycle rallies that began on December 9 2022. All ended in lower prices. In fact, it’s difficult to look at Figure 1 and see anything other than a bear market.

Prices have recovered to within $1.94 (2.4%) of the January 23 level of $81.62 but remain -$12.93 (-14%) lower than on November 4 and -$42.38 (-35%) lower than on June 8.

Figure 1. WTI prices have increased to within $1.94 (-2.4%) of the January 23 level of $81.62 but remain -$12.93 (-14%) lower than on November 4 and -$42.38 (-35%) lower than on June 8. Source: CME & Labyrinth Consulting Services, Inc.

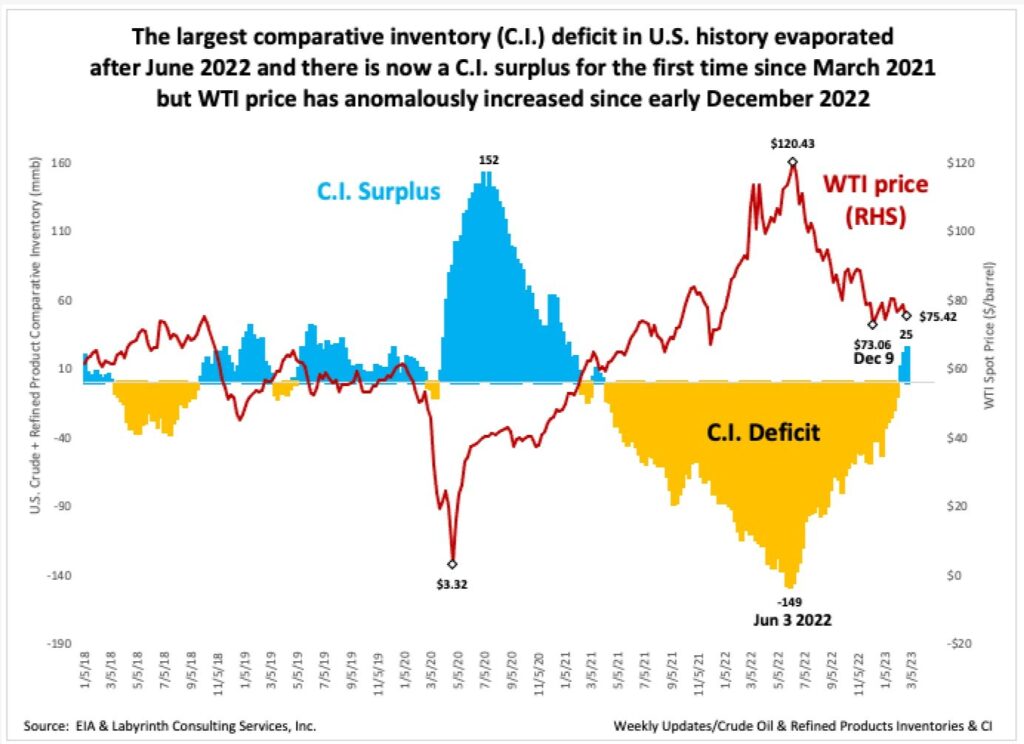

The larger problem is that the recent price rally is occurring against the backdrop of rising U.S. inventories. Since early June 2022, the largest comparative inventory (C.I.) deficit in U.S. history has evaporated (Figure 2).

Now, there is a C.I. surplus for the first time since March 2021 but WTI price has increased from $73 to almost $75.50 since early December 2022.

The simple explanation is that markets are concerned about supply because of the much-anticipated recovery in China demand now that Covid lockdowns are ending. Supply urgency usually results in higher prices as markets try to motivate companies to drill more wells.

This situation reminds me of the second half of 2018. In April 2018, the United States announced its intention to withdraw from the Iran nuclear agreement and impose full oil export sanctions on that country. At the time, Iran was producing about 4.8 mmb/d so markets were in a state of supply panic.

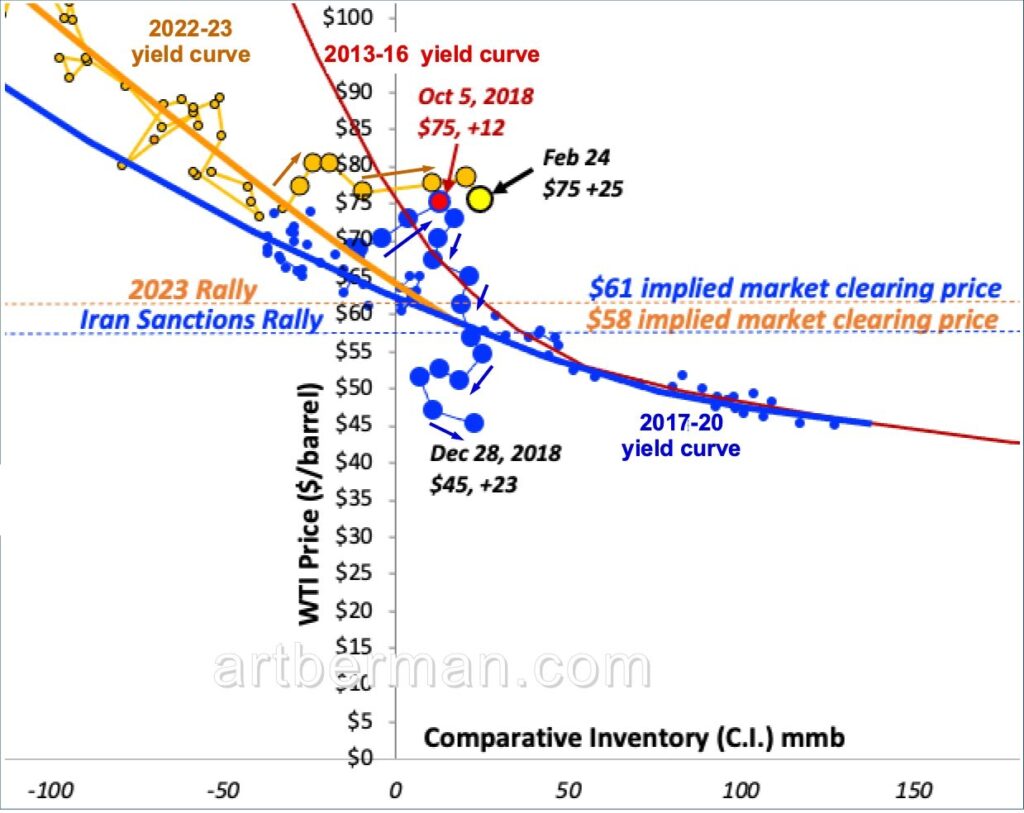

Figure 3 shows the same WTI price versus comparative inventory data in Figure 2 except that it is cross-plotted rather than displayed as a time series. The large blue circles and blue arrows show that as comparative inventory increased above the 5-year average (y-axis) in late 2018, price increased because of supply urgency.

Price increased to a maximum of $75 as C.I. rose to +12 mmb more than the 5-uyear average in early October 2018 (red circle). Dropping a perpendicular line from the red circle to the blue yield curve indicates that WTI was about $14 over-priced at that time.

Later, as markets determined that supply concerns were largely a false alarm, price collapsed. It reached a bottom of $45 on December 28.

The current price rally is shown by the large orange circles and organge arrows in Figure 3. Just like in 2018, comparative inventory increased to more than the 5-year average while price increased to last week’s value of $75 and C.I. was +25 mmb more than the 5-year average (yellow circle). All signals indicate that markets are adequately supplied.

The bearish market fundamentals that I described in last month’s newsletter have not materially changed. The bull thesis rests almost entirely on an explosive renaissance of oil demand by China. I understand the logic of the argument but believe that it ignores basic realities of China’s changed economic condition that began before COVID lockdowns.

This week, China set a modest 5% growth target for it economy at its annual National People’s Congress meeting. That’s an improvement from the 3% growth recorded in 2022 but it is a setback for the China growth story.

At the same time, February was the strongest month for oil imports since July 2020.

“The question is whether demand for crude oil will continue at the high levels of the first two months of 2023, or whether it will level off as the initial demand for travel after the end of restrictions is sated.”

Clyde Russell, Reuters

Economist Harald Malmgren noted earlier this week that China’s economic future is dependent on “horrendously challenging domestic policy reforms” and questioned whether the the 2023 growth target of 5% is even believable, given domestic challenges.

Separately he commented

The Chinese economy has been undergoing a structural contraction over the last 10 years. Lower productivity, lower asset returns and an aging population are among the explanations. The collapse of China’s real estate sector and the effects of the pandemic worsened those trends.

In early December, macro investor Felix Zulauf stated that Chinese demand for commodities including oil may not rebound for perhaps a decade.

“I think that the lockdowns [in China] are sort of a camouflage to not show the world how structurally weak China has become.

“Because the Chinese economy has hit the same point as Japan in the early 1990s. It was exhausted after one of the biggest investment and credit booms of mankind…So, my guess is at least 10 years to get over this restructuring of the economy. It took Japan 20 years, and the excess is real small.

“So, I think, China you can forget as a locomotive for the world economy. And it has been the locomotive for the world economy in the last 15 years.”

Felix Zulauf

I have little doubt that China’s oil demand will increase but what if it does not increase as much or as fast as some analysts expect?

The price collapse in late 2018 along with investors fatigue with poor shale company returns were key factors for investor flight from oil stocks. A repeat of those events in 2023 is improbable because many other circumstances are different now. It is, nonetheless, a cautionary tale about how wrong analysts–not the market–can be.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

On Fox business this am Gordon Chang proposed that China was preparing for war. When economies fail war is a ready option. What is your opinion of this Chinese agressive build up and possible effects on oil prices?

Pure Fox News nonsense, Doug.

Art