Art Berman Newsletter: November 2021 (2021-10)

Oil prices corrected strongly downward last week. WTI fell -7% and Brent dropped -6% between October 26 and November 4. Analysts didn’t offer much explanation but instead focused on how much higher prices are likely to go. A meaningless bump in the road. Bank of America now thinks that Brent will be $120 per barrel by June 2022.

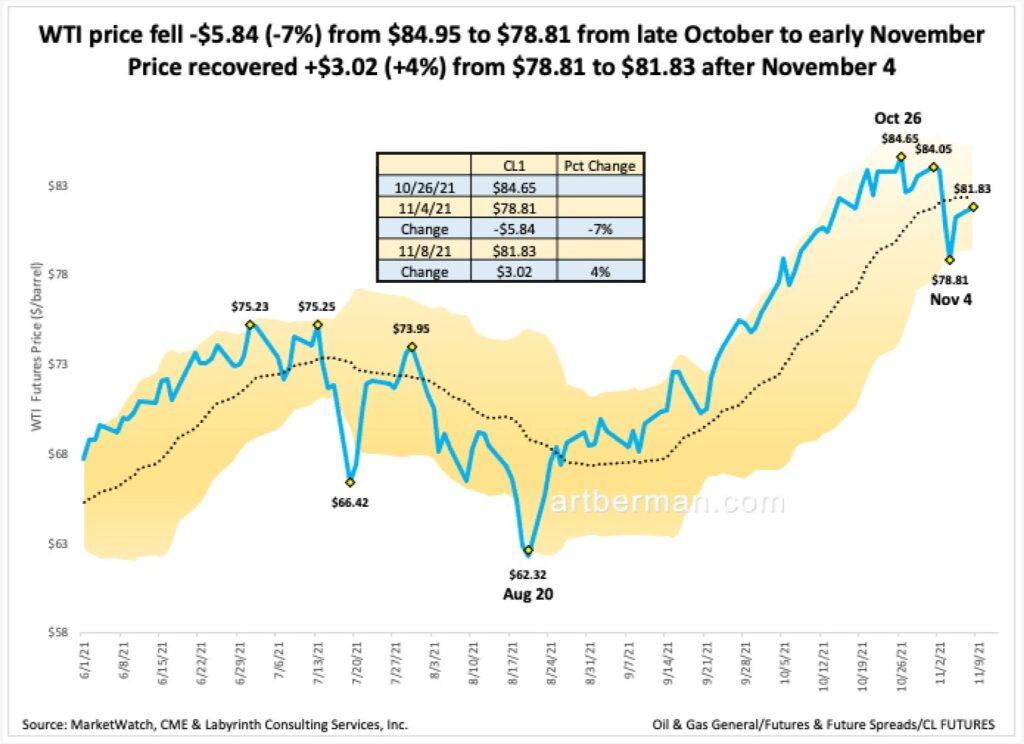

WTI price fell -$5.84 (-7%) from $84.95 to $78.81 from late October to early November (Figure 1). Price recovered +$3.02 (+4%) from $78.81 to $81.83 after November 4. I expect more downward price corrections as the end of this long price rally approaches. The principal reason is inflation.

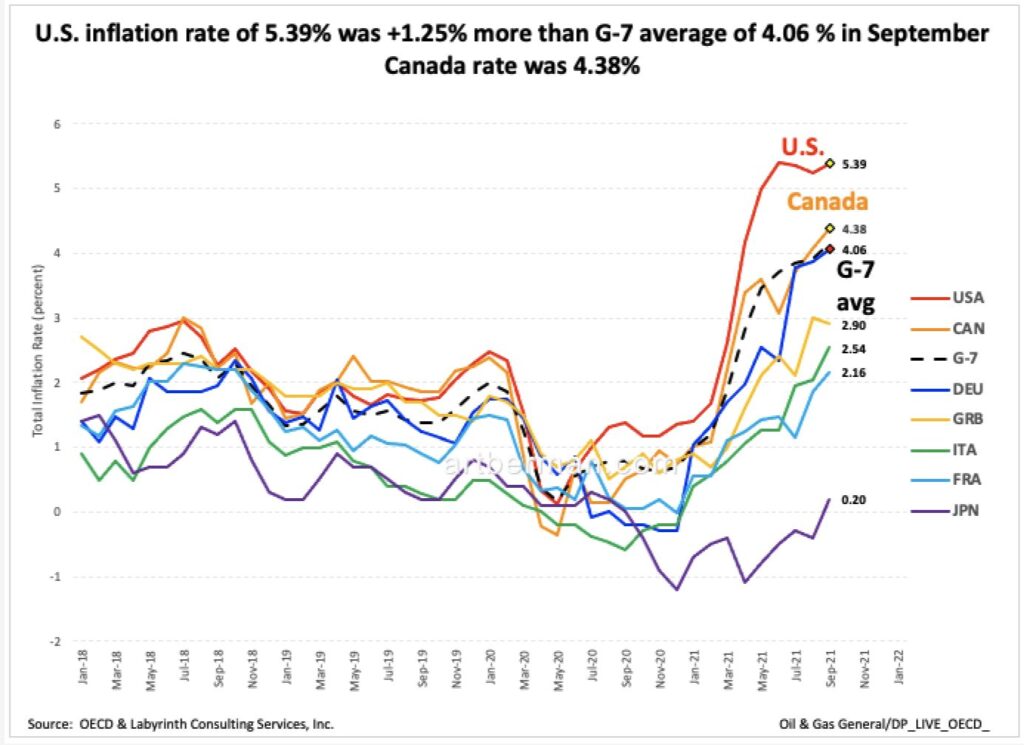

Calls for $90, $100 or $120 oil prices fail to adequately reflect the effect of inflation on the global economy and oil prices. Figure 2 shows the latest inflation data for the United States through August. The correlation between inflation rate and WTI spot price is compelling especially since 2015.

That should be no surprise to those who understand that energy is the economy and that oil price is the leading indicator of inflation. Inflation will probably slow global economic growth and limit oil demand at current oil prices. Pimco’s Erin Browne recently said the the current energy crisis is a real inflation “risk that is being underestimated by the market right now.”

The U.S. inflation rate is the highest among the G-7 countries. It was +1.25% more than the G-7 average of 4.06% (Figure 3). . The U.S. average inflation rate since 2000 is 2.2% and the G-7 average is 1.75% so present rates are nearly 2.5 times the twenty-year average.

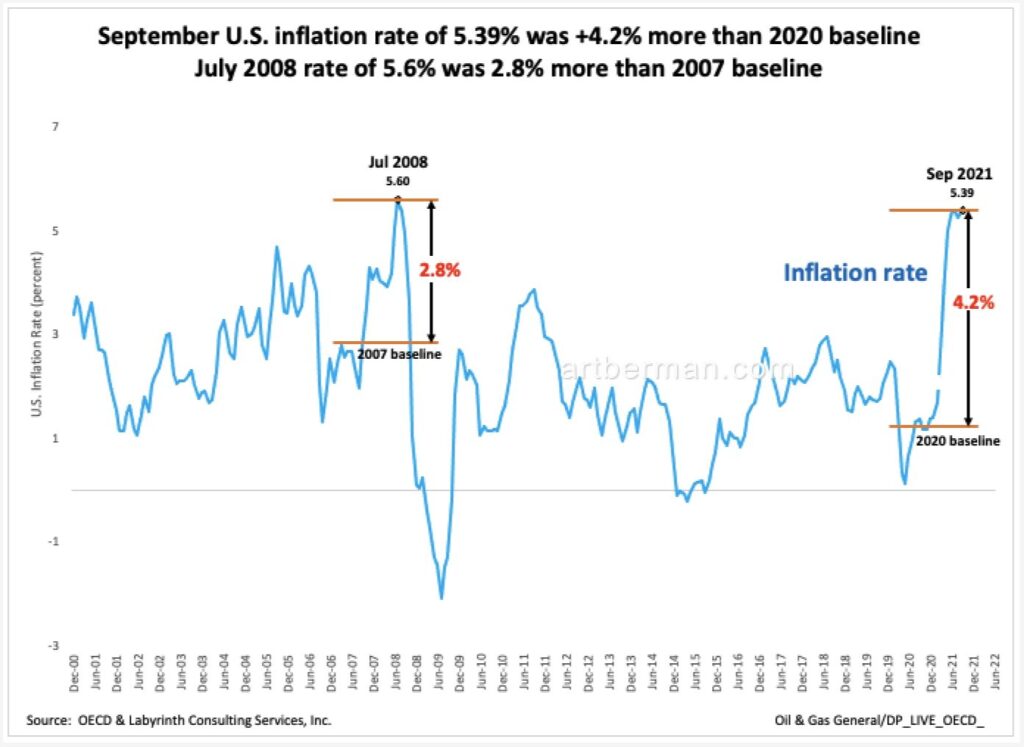

U.S.inflation for September was the highest monthly level since July 2008 just before the Financial Collapse (Figure 4). It was more than 4% more than the 2020 baseline of 1.24%. By comparison, the July 2008 level of 5.6% was only 2.8% higher than the 2007 baseline of 2.85%.

The significance of the information in the last three charts cannot be understated.

Figure 5 shows the relationship between oil demand growth, inflation and U.S. treasury yield for the last 50 years.

2021 oil demand growth is the greatest in data history. The best analogue was in 1986 after WTI prices fell from $117 in 1980 to $36 in 1986 in 2021 dollars per barrel. Demand growth and inflation soared. Oil demand crashed.

The 2021 annual inflation rate is estimated to be the highest since 1990. At the same time, the 4% gap between inflation and treasury yield is the highest in 50 years. It was 3.1% during the first oil shock in 1974, and approximately zero during the second oil shock and the 2008 Financial Collapse.

Inflation is noted by oil analysts but always seems secondary to their confidence that oil prices will continue to increase for the near term. They don’t appear to acknowledge the significance of Figure 5.

Economists have been debating the causes and implications of inflation for months now but somehow the price of energy is almost never mentioned by those experts.

John Mauldin is a notable exception. He recently wrote that, “Energy prices affect everything. They are a necessary input to all other production. Some things are more energy-intensive than others, but without it we are all back in the stone age. The price matters for the same reason tax rates matter. Both are unavoidable costs, so we can produce more of everything if they’re low or at least stable.”

A recent Bloomberg headline proclaimed a new era of oil prices as “higher for longer.” Some of the biggest commodity desks on Wall Street, it stated, now believe that the era of cheap oil is over for good.

I don’t see how that view is consistent with current inflation, treasury yields and oil demand data.

There is a case for under-investment. Supply is tight because outside capital has contracted for oil companies. Investors feel that they were played by shale plays and by poor E&P poor returns for a decade. The energy transition away from fossil energy has gained momentum.

Talk of a commodity super-cycle has returned as shortages of almost everything including natural gas, coal, aluminum and copper have emerged in recent weeks. RBC Capital Markets and Goldman Sachs have proclaimed a structural bull market for oil.

The problem with under-investment and super-cycle arguments is that the market has to be wrong for them to be right.

At the same time, Citigroup believes that oil prices above $60 are unsustainable. ““Mid-term, cost indicators keep pointing to a fair-value range between $40-$55 a barrel.”

Last week, Citi’s Ed Morse said, “Next year is going to be a very big surprise…The growth in U.S.production…is going to be bigger than anything…from an individual OPEC country…If we look forward to a year from now…is [OPEC] going to be restraining production again to fight what might otherwise be a $20 lower price?”

The cliché is that the cure for high oil prices is high oil prices. I suggest that inflation is the cure.

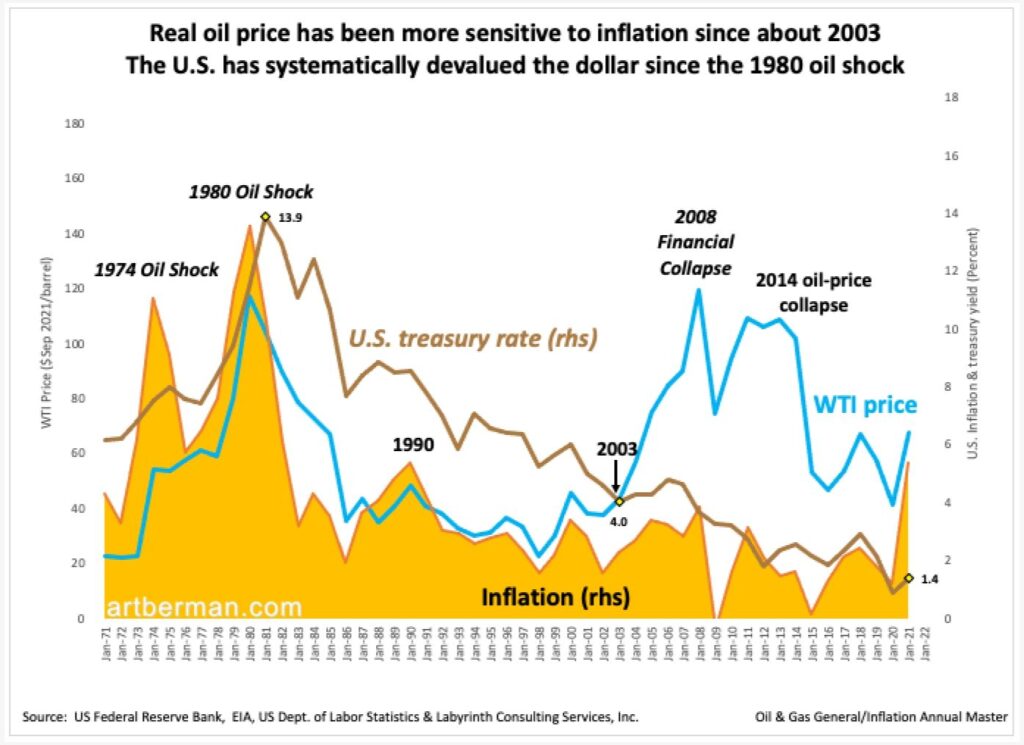

Figure 6 shows inflation, U.S. treasury rate and real WTI price in September 2021 dollars per barrel. It suggests that oil price has been more sensitive to inflation since about 2003 which coincides with U.S. interest rates falling below about 4%. The U.S. began systematically devaluing the dollar after the inflation that followed the 1980 oil-price shock. The financialization of oil markets began in earnest during the period of peak oil concerns in the early 2000s.

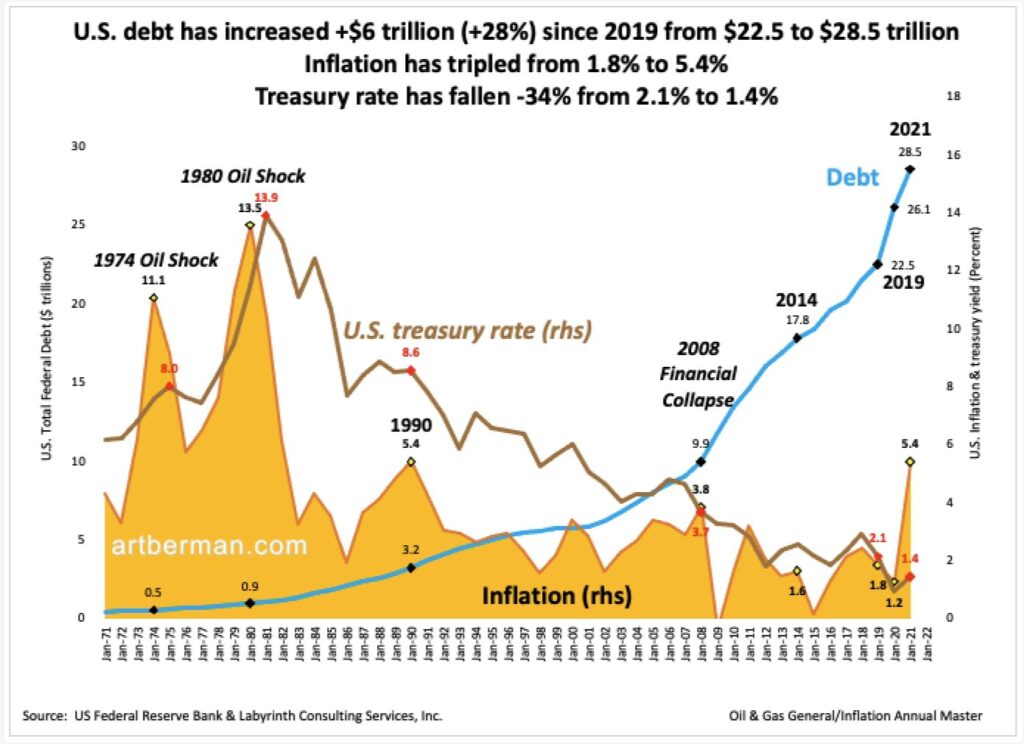

U.S. debt has increased +$6 trillion (+28%) since 2019 from $22.5 to $28.5 trillion (Figure 7). That seems to be the main focus for economists and it is important. At the same time, money is a call on energy and debt is a lien on future energy so debt is really a reflection of how energy affects society.

I believe that data supports what Ed Morse has said namely, that current oil price levels are unsustainable.

I’m not predicting an imminent collapse in oil prices. The above figures show that there is considerable uncertainty about the lags between inflation and oil-price. The time scale is, after all, annual. I am saying that higher for longer seems like an improbable outcome based on what we know today.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Art,

First of all it seems to me that the two Alans (Greensapn and Watts) and you and I all agree that real wealth is not money but the real world assets that we need to survive and run our modern economy. Your comment says it perfectly – “Most people think the economy runs on money, and that’s completely untrue, the economy runs on energy.” You are correct, of course – and it runs on lumber, copper, steel, rare earths and water. Alan Greenspan said exactly that same thing when he mentions “real assets” – here is the whole quote –

ALAN GREENSPAN: “Well, I wouldn’t say that the pay-as-you-go benefits are insecure, in the sense that there’s nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The question is, how do you set up a system which assures that the real assets are created which those benefits (money) are employed to purchase.”

So as Greenspan says federal government can and does create money, When it buys treasuries it directly funds the government. And do we need to pay the Federal Reserve back for the computer key stroke they used to buy that treasury bond? The fact is that the treasury does pay the Fed back and then the Fed turns around and gives the money back to the Treasury so where is the debt and who must pay it?

My question is why is today’s debt a problem when it could all be retired in the same way that Goldman Sachs etc were made whole and given trillions of dollars (nobody seems to know exactly how much?) after the 2009 financial crisis. Or in the same way that the Fed used its computer money to keep people and companies afloat during the pandemic.

Wouldn’t it be wise for our country to “create all the money we need” and pay it to Saudi etc for their oil and keep ours in the ground for our grandchildren and beyond? Give the Saudis all the $100 bills the fed can create and keep the oil, nat gas, timber, copper etc that this resource rich country has for future generations. Let the Saudis put dollar bills in their gas tanks and furnaces?

for anyone interested in more info on fiat currency and monetary policy I would start with Stephanie Kelton –

” The government’s IOU—the United States dollar—sits at the top of the pyramid. It is a fiat currency. The United States government is the monopoly issuer of the U.S. dollar—the only entity on the planet that can legally create the currency. The U.S. government taxes in dollars. It spends in dollars. And it controls its own currency. Why is this important? What are the benefits of issuing your own currency? They are extraordinary.

“The government, when it issues its own currency, and goes into debt in that currency can always pay its debt, can never go broke, can never run out of money. It can afford anything that is for sale in that currency. It doesn’t need to borrow its own currency.

philip

Philip,

Draining America first is a terrible idea.

Best,

Art

great article as always – thanks. i am curious about your thinking regarding debt. how much of that $6 trillion in new debt is held by the Fed and can’t it be retired with the stroke of a computer key? and isn’t it possible for the Fed to retire student debt or any debt in the same way? remember how Alan Greenspan responded to Paul Ryan – “There is nothing to prevent the government from creating as much money as it wants.”

and the Indian proverb about the teacher appearing is great – maybe you know Alan Watts – here is his take on money –

Alan Watts – – on the fundamental confusion between money and wealth:

“Remember the Great Depression of the Thirties? One day there was a flourishing consumer economy, with everyone on the up-and-up; and the next, unemployment, poverty, and bread lines. What happened? The physical resources of the country — the brain, brawn, and raw materials — were in no way depleted, but there was a sudden absence of money, a so-called financial slump. Complex reasons for this kind of disaster can be elaborated at length by experts on banking and high finance who cannot see the forest for the trees. But it was just as if someone had come to work on building a house and, on the morning of the Depression, the boss had said, “Sorry, baby, but we can’t build today. No inches.” “Whaddya mean, no inches? We got wood. We got metal. We even got tape measures.” “Yeah, but you don’t understand business. We been using too many inches and there’s just no more to go around.”

A few years later, people were saying that Germany couldn’t possibly equip a vast army and wage a war, because it didn’t have enough gold. What wasn’t understood then, and still isn’t really understood today, is that the reality of money is of the same type as the reality of centimeters, grams, hours, or lines of longitude. Money is a way of measuring wealth but is not wealth in itself. A chest of gold coins or a fat wallet of bills is of no use whatsoever to a wrecked sailor alone on a raft. He needs real wealth, in the form of a fishing rod, a compass, an outboard moter with gas, and a female companion.

Philip

Philip,

The government doesn’t actually create money. It creates credit. New money is not created until banks loan that new credit reserve. Credit is imaginary and can only exist as long as people believe it is real. It disappears if trust is lost in its artificial existence. That is how depressions begin.

Money has no independent reality except as a claim on energy. Debt is a lien against future energy claims.

Wealth has no tangible existence except as the potential for access to more energy. It is a form of credit. Wealth is the emperor’s clothing.

Few people understand how finance really works and it leads to fundamental misconceptions about past, present and future. The Great Depression was mostly about the demise of American manufacturing and the displacement of manual farm labor by machines that ran on petroleum. There’s a lot more to it but that’s the simple version.

Great states rise and fall based on their access to credit.

Alan Watts was a great cosmologist but was not qualified to discuss money and wealth.

Best,

Art