Complexity’s Revenge: Electric Power and AI

We need gas. We need nuclear. We need it all. We need it now.

That was Virginia Governor Glenn Youngkin’s message on surging U.S. power demand. It sounds decisive. It’s ignorant. It treats electricity like a menu where you can order more generation and it just shows up.

Energy will be a serious constraint before the end of the decade. But the nearer-term obstacles are simpler and harder: permitting, build times, turbine and transformer backlogs, skilled labor, capital costs, and the hard limits of grid physics.

Ignore those constraints and you don’t get more electricity. You get cost overruns, schedule creep, and a widening gap between demand and deliverable capacity.

Growth and Uncertainty

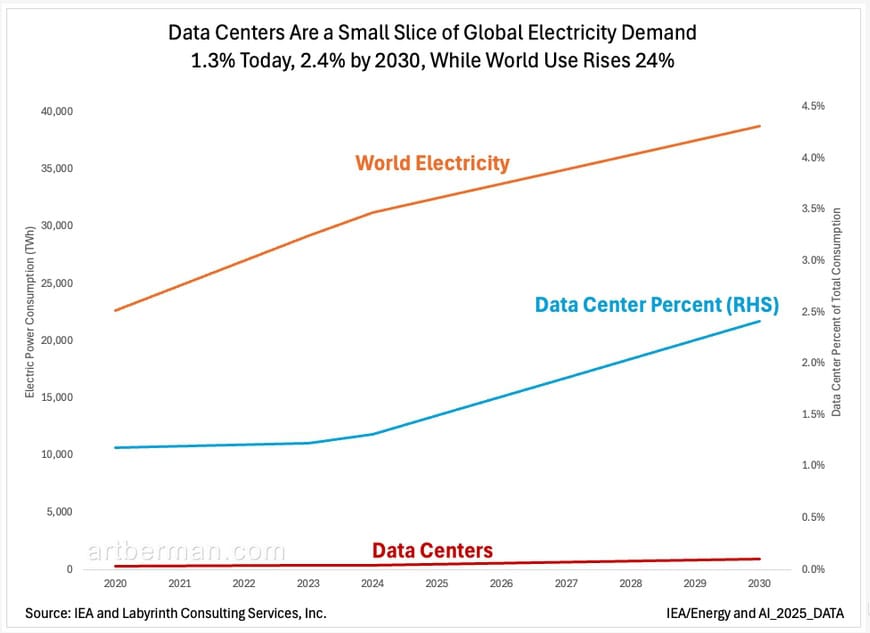

There’s almost as much hype about “soaring power demand” as there is about the AI supposedly driving it. Yes, data center electricity use could roughly double by 2030. But it’s doubling from a small base.

Data centers use about 1.3% of global electricity today, and the IEA sees that rising to only around 2.4% by 2030 (Figure 1). Over the same period, total world electricity demand is expected to rise on the order of 24%. So the idea that AI is the main driver of global power growth is badly overstated.

Source: IEA and Labyrinth Consulting Services, Inc.

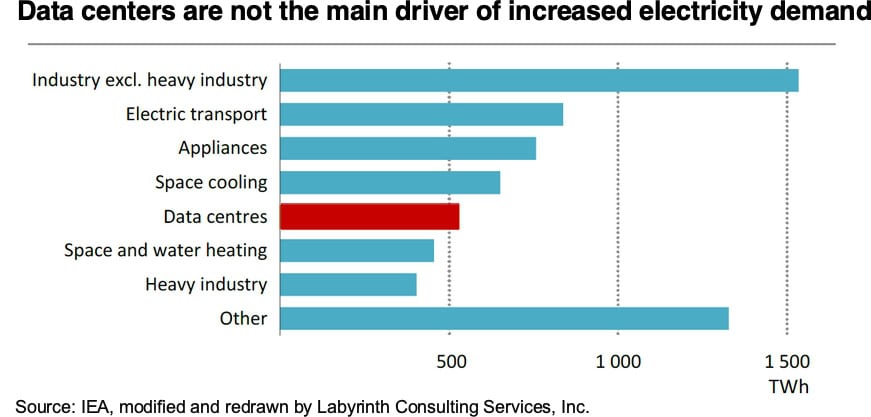

Most of the growth is boring, broad, and structural: industry and buildings (especially cooling), plus the steady electrification of transport and heating (Figure 2). Data centers matter operationally because their load is fast and geographically concentrated. But they’re still riding on top of a much bigger wave.

Source: IEA, modified and redrawn by Labyrinth Consulting Services, Inc.

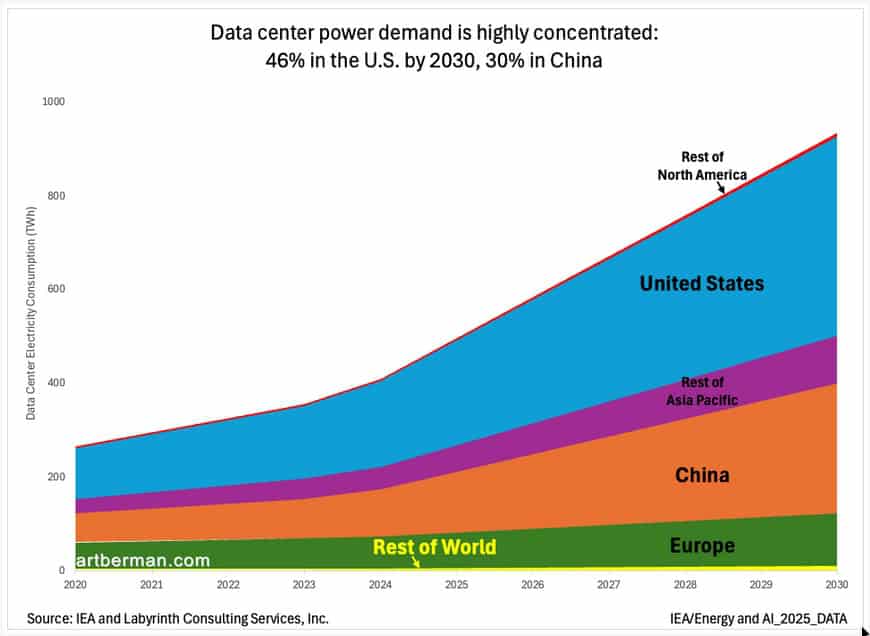

In the U.S. and other developed economies, data centers account for a larger share of incremental demand than they do globally. Even there, it’s still a fraction of total growth, not the whole story the headlines imply. What makes data centers uniquely disruptive is concentration: by 2030, nearly half of global data center electricity consumption is expected to be in the United States, and about 30% in China (Figure 3).

Source: IEA and Labyrinth Consulting Services, Inc.

So yes, data centers are a major source of power stress in parts of the Global North. But the real constraints aren’t “do we have enough gas, coal, nuclear, and renewables?” The constraints are time, siting, equipment, skilled labor, capital, and grid deliverability.

System Risks

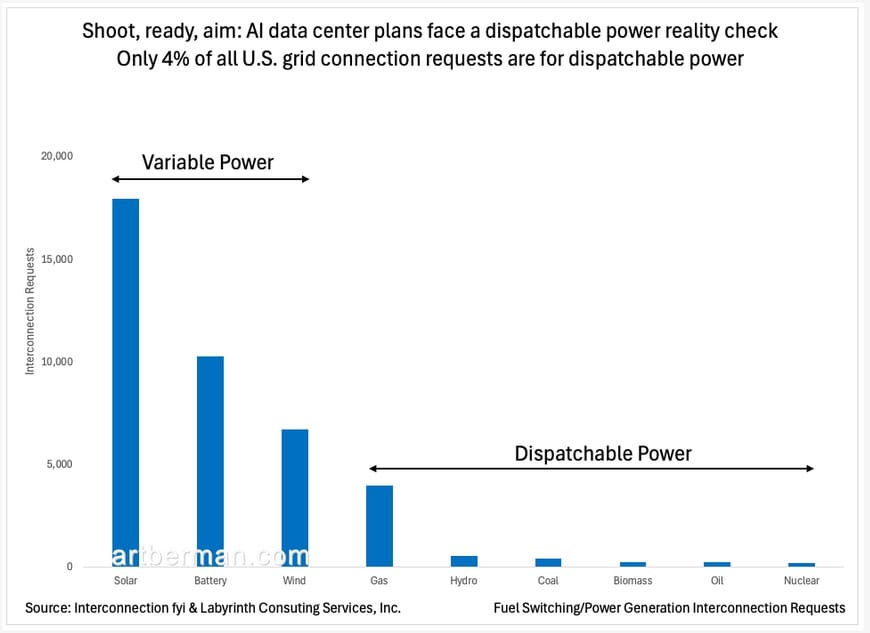

The first system risk is the shrinking dispatchable base. Nearly 79 GW of fossil-fired and nuclear retirements are expected through 2034. Add another 43 GW of fossil units that have announced retirements but haven’t entered formal deactivation yet, and you’re over 115 GW of potential dispatchable thermal capacity coming off the board in the next decade.

Demand is rising. Dispatchable retirements are growing. And the replacement pipeline is heavy on solar, batteries, and hybrids that aren’t arriving fast enough or carrying the same reliability attributes as the thermal fleet they’re replacing (Figure 4).

Source: Interconnection fyi & Labyrinth Consuting Services, Inc.

That’s why capacity-only planning is increasingly misleading. In a system with weather-dependent and energy-constrained resources, you don’t just need nameplate megawatt capacity. You need on-demand generation, transmission to move it, and the essential reliability services thermal plants used to provide by default: voltage support, frequency response, ramping, and reserves.

The second system risk is interconnection and delivery. Even if generation exists on paper, you may not be able to connect and move it. The interconnection queue is the grid’s choke point. Before a large generator plant can connect, the operator has to study whether the local and regional system can handle it. If not, you trigger upgrades: substations, transformers, lines, protection systems. Those take years to permit, procure, and build. Data centers can go up fast. Grid capacity can’t. The queue is where the mismatch becomes delay.

The third system risk is the supply chain.

Utilities are defaulting to gas plants to close the looming capacity gap, with plans implying roughly 19 GW per year of new gas capacity through the rest of the decade, about double the recent build rate. The problem is that the equipment and construction reality do not support the gas—or any other—solution.

Large gas turbine lead times are now measured in years, so what look like near-term fixes are increasingly late-decade bets. Costs are also rising. The old rule-of-thumb numbers no longer hold, and procurement quotes are coming in far above what utilities assumed in planning. Ratepayers end up paying the spread.

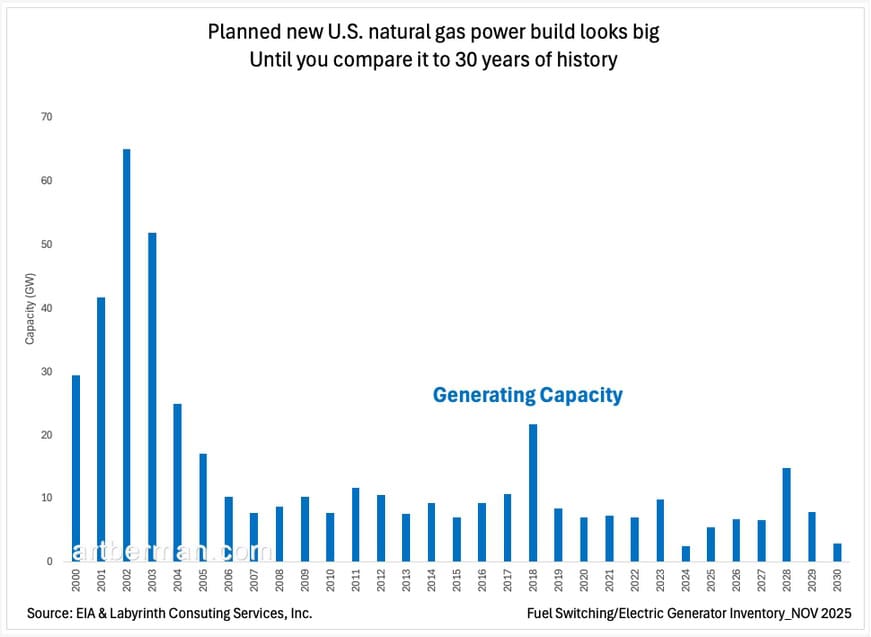

That creates a planning mismatch. Load growth is uncertain in timing and location, but gas plants are long-lead, high-capex commitments that require confidence you rarely have in this environment. And the risk is clear when you put planned capacity in historical context. New gas additions look big until you compare them to the early-2000s buildout (Figure 5).

Source: EIA & Labyrinth Consuting Services, Inc.

Energy Supply

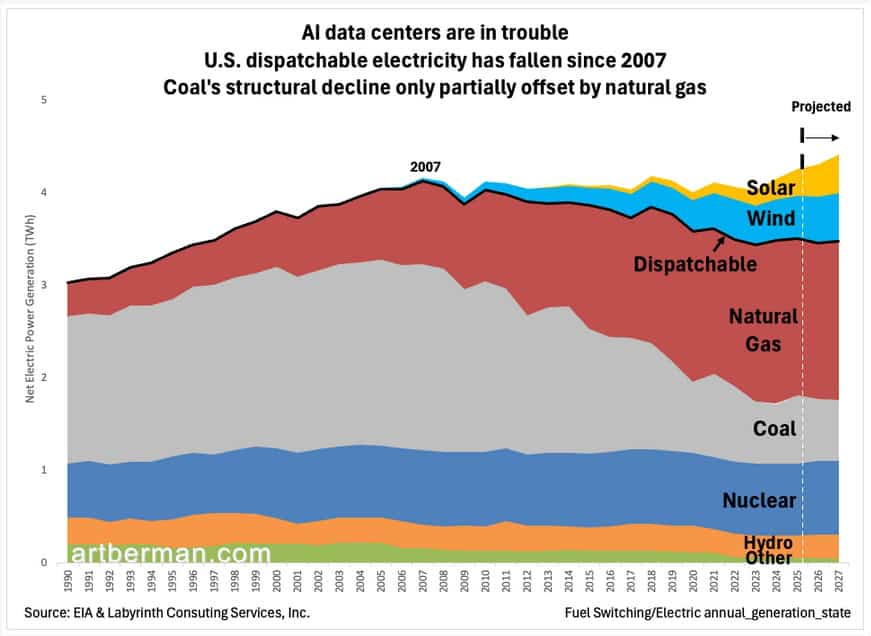

AI data centers in the U.S. are in trouble because the system has less dispatchable output than it did in the mid-2000s (Figure 6.) Natural gas and solar are the only sources of energy that have increased since 2022. Coal is in structural decline, nuclear and hydro are flat and wind has stalled at least for now.

Source: EIA & Labyrinth Consuting Services, Inc.

Natural gas is the default option for data centers because it’s dispatchable, scalable, and historically abundant. There’s no shortage of uninformed clamor for nuclear, renewables, even coal as the obvious answer. But nuclear is too expensive and too slow for this window of urgency, and variable renewables don’t solve resource adequacy for 24/7 loads without major add-ons: transmission, storage, firm backup, and real operational flexibility. Coal has no credible investment path and is in managed decline, not a comeback.

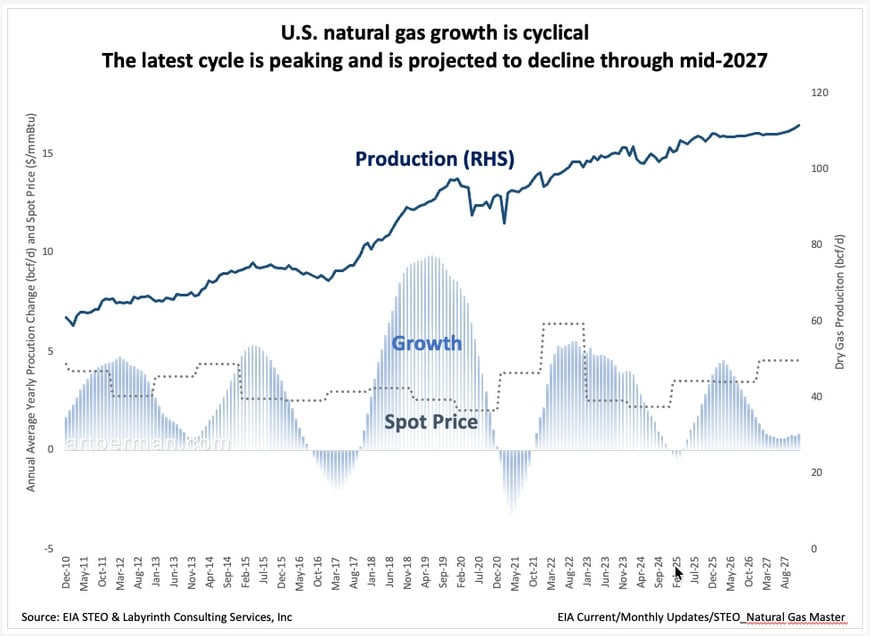

EIA projects U.S. natural gas production growth to slow through mid-2027 (Figure 7). Gas growth is cyclical and often weakly linked to gas price because a large share is associated gas tied to oil drilling, not gas economics. Forecasts are never perfect, but EIA tends to be most reliable in the near term. That implies a meaningful 2026 supply upturn is unlikely.

Source: EIA & Labyrinth Consuting Services, Inc.

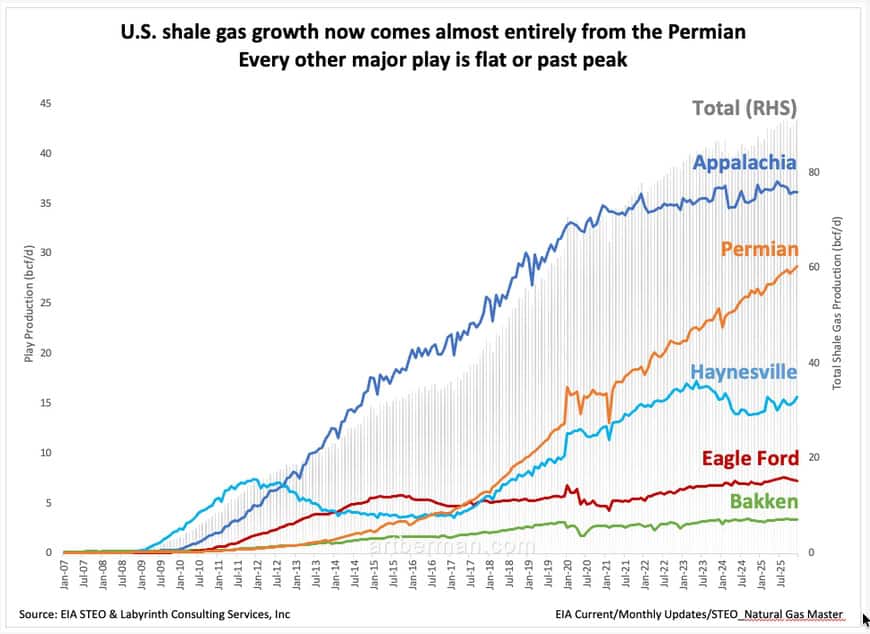

More importantly, shale gas now makes up over 90% of U.S. onshore supply, and the Permian is the only major play still growing (Figure 8). That concentration is a constraint. It narrows the factors that can lift supply, regardless of price.

Source: EIA & Labyrinth Consuting Services, Inc.

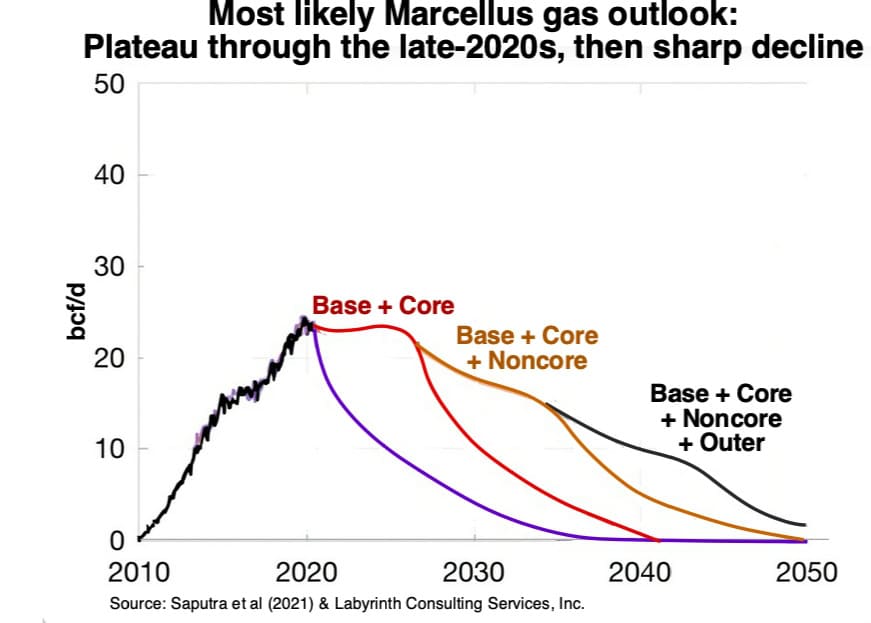

Many assume Appalachia’s gas supply is effectively limitless and that production is flat mainly because regulators won’t allow new pipelines. Takeaway constraints are real, but they’re not the whole story. A recent bottom-up assessment suggests the remaining growth potential is limited even if infrastructure improves. The most likely Marcellus path is a plateau through the end of this decade, followed by a sharp decline (Figure 9).

Source: Saputra et al (2021) & Labyrinth Consulting Services, Inc.

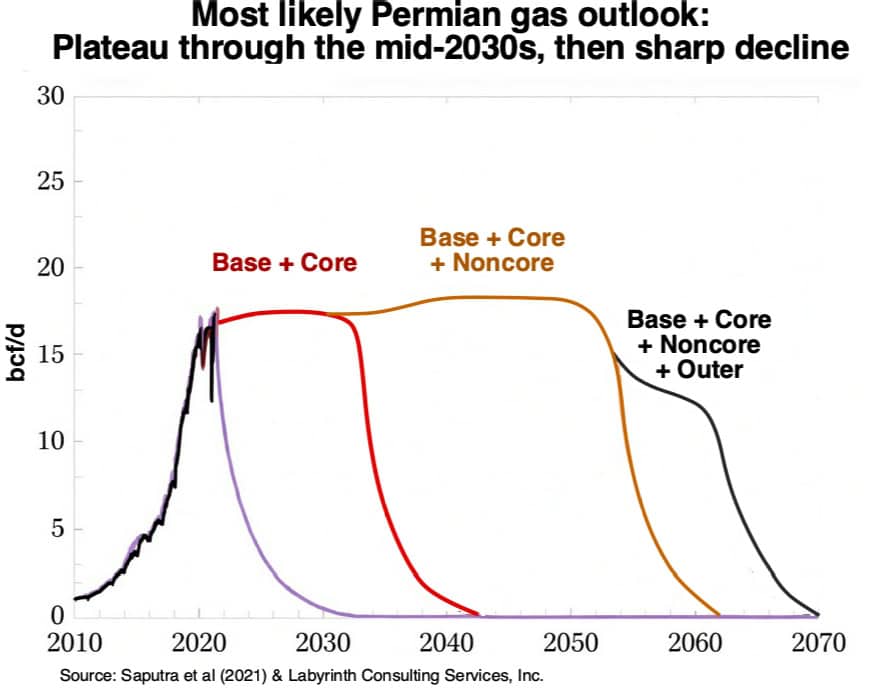

Even Permian gas has limits. Unconventional gas doesn’t get a pass on field physics: growth, peak, plateau, decline. The Permian is a mature play now, not an endless frontier. The most likely path is a plateau into the first half of the 2030s, then terminal decline (Figure 10).

Source: Saputra et al (2021) & Labyrinth Consulting Services, Inc.

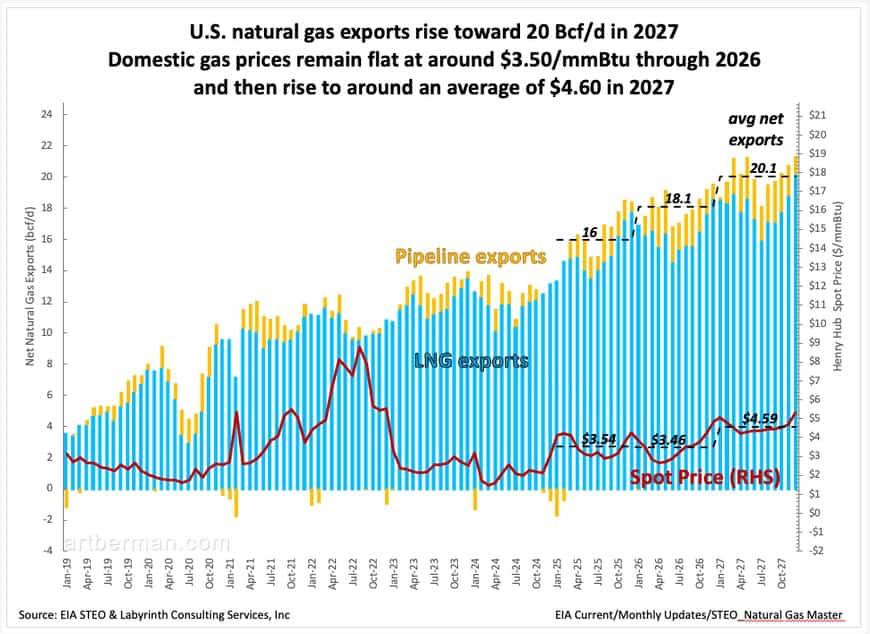

Exports are another hard constraint on U.S. gas availability. EIA projects combined LNG and pipeline exports exceeding 20 Bcf/d by 2027 (Figure 11), roughly one-fifth of total supply. In that scenario, marginal gas goes to the highest bidder, and domestic consumers pay the premium. EIA projects prices rising sharply in 2027.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

U.S. power isn’t a fuel shortage yet. It’s a deliverability problem. Demand is rising fast, but the system can’t add firm capacity, transmission, transformers, and interconnections on the timeline being implied by AI rhetoric. The mismatch is obvious to anyone looking at queues and lead times, but political leaders still talk as if you can order more supply and it just appears. The deeper issue is that rising complexity is intersecting with a physical system that can’t be expanded or maintained at the pace of demand growth.

Complexity’s Revenge

Meredith Angwin argues the U.S. grid has become a fragmented superstructure with diffuse responsibility and weak accountability. It’s optimized for narrow objectives and short horizons. Markets and regulators can deliver the next cheap kilowatt-hour. They don’t reliably deliver readiness. So we keep shaving margin, making assumptions about imports, gas deliverability, and whatever’s sitting in the interconnection queue, then act surprised when heat, cold, or equipment failures expose the gap. AI data centers make things worse by raising the demand floor and concentrating large, inflexible loads on a handful of nodes.

Over the last 20 years, new digital products behaved like free riders. More renewables, more compute, more networks, more always-on services, more electrification, more smart everything, all assuming the grid would somehow scale automatically at no cost. Complexity grew faster than the physical system that supports it. Now the cost of maintaining and expanding generation is rising while institutions remain optimized for cheap, just-in-time energy rather than redundancy, repair, and deliverability.

Joseph Tainter’s The Collapse of Complex Societies should be required reading for anyone who thinks more technology is the default solution to society’s problems. In his work across roughly 4,500 years of history, he argues that civilizations fail for a common reason: complexity becomes too expensive to maintain.

His core thesis is simple and brutal. Societies are problem-solving organizations. They build layers of administration, infrastructure, specialization, and control to manage challenges. At first, those layers pay off. But over time the marginal returns decline. Each new fix costs more energy, materials, and coordination than the last, while delivering less benefit. Eventually the system becomes fragile: a larger share of its resources goes to upkeep rather than real progress.

Specific triggers vary—resource depletion, invasion, climate shocks, financial breakdown—but those are excuses, not the underlying cause. The root problem is the rising maintenance cost of complexity itself. In that context, collapse isn’t mysterious or moral. It’s an economic adjustment: a forced simplification when the costs of complexity exceed what the society can afford. For Tainter, collapse is a loss of complexity, not the end of society.

Our civilization already meets Tainter’s criteria for collapse: an overextended financial superstructure, rising geopolitical conflict, weakened governance and a fraying world order, brittle supply chains, and ecological overshoot. AI doesn’t arrive as a neutral upgrade in that context. It arrives as an accelerant. It adds another layer of complexity that must be powered, cooled, financed, secured, and defended, at precisely the moment the underlying substrate is struggling to keep up.

In a purely rational world, you would scale the AI buildout to what the physical system can actually support. That won’t happen, because AI’s perceived purpose is not discretionary. It’s being treated as strategic infrastructure in a competitive, security-driven era.

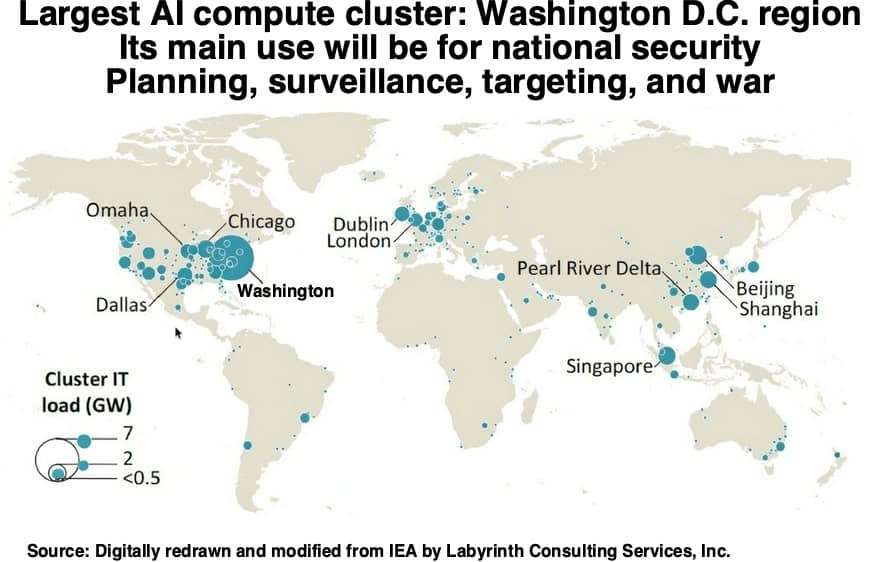

Craig Tindale puts it bluntly: AI is a weapon. The public story is productivity and medical miracles. But look at the map. The largest compute cluster sits in the Washington, D.C. region (Figure 12). That isn’t an accident. It signals the center of gravity: the military-industrial complex and the state’s demand for advantage. The real story is surveillance, targeting, influence, and faster decision cycles than rivals. Once you’re in that framework, restraint stops being an option. Governments and suppliers come first; consumers and environment come later.

Source: Digitally redrawn and modified from IEA by Labyrinth Consulting Services, Inc.

Conclusion

The era of material expansion is ending. We’ve entered a period of grid stress, financial fragility, and rising geopolitical conflict. Nations are competing for dwindling resources and to protect internal stability.

From that perspective, AI is not just innovation. It’s a tool of relative advantage, which is why the AI buildout is inseparable from power politics. Data centers require electricity, water, copper, transformers, turbines, land, and permits. That makes the future of AI automatically entangled with grid constraints, national security, and potential wartime allocation.

This isn’t a message of doom. It’s a call to see the world as it is unfolding. Awareness is the beginning. The next step is letting go of mental models that worked in a different era, models that treat this as a set of broken parts to be fixed. We’re at an inflection point. Decades of growth and abundance delivered plenty of stuff, but not the meaning and satisfaction that humans need for the true good life.

Simplifying is what adults do when circumstances change: clean house, reset priorities, stop living on failed assumptions. It’s not surrender. It’s an opening to build a life that fits the world we actually have.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

https://youtube.com/@samoandudet?si=tcnuXJGHwST8GXvX

Things have not stopped growing sir. For one person when is enough enough?

Emile,

I have no idea what point you’re trying to make and the link doesn’t help me.

All the best,

Art

Hi Art. I’m with you. I’m focused on seeking inner peace. We have a lot of noise and turmoil all around. It all causes a lot of stress and Doctors all will tell us stress is a major cause of illness. Focusing on friends, family and faith really helps! Spending time on enjoying life is the goal!

Discovering who you are is the key, Mark. If you aren’t what you do, what you think, or the result of who you are, then who are you?

All the best,

Art

So, you are saying that AI is here to stay, due to national security interests. Probably true. However, OpenAI seems to be running out of money. I keep hearing about a bubble. Is AI in a bubble?

Richard,

AI is unquestionably a bubble but like railroads and the internet, it isn’t disappearing–just not all the players will survive.

Here’s Jeremy Grantham talking about the AI bubble: https://www.youtube.com/watch?v=L-hLVS_53NU

All the best,

Art

Art, the image at top of this page is stunning. Was that generated by AI? Just curious because I can’t imagine anyone painting that! Thinking that maybe AI made a collage of images. There is a bit of information overload, people get tired of hearing AI but it certainly is capable of doing some amazing stuff.

Bill,

All of my “featured images” for posts for the last year of so are AI-generated. You’re right that there’s a lot of chatter about AI, most of it by people with limited experience using it. I’m hardly an expert but use it all the time in my research and as an aid in writing and images.

All the best,

Art

What is crazy, Bill, is every Ai image you see is generated from scratch – it is not a cut and past or a collage, every pixel is synthesised and never existed before someone prompted the creation of it!

Excellent analysis, Art—nobody does this better. We’re fortunate to have your clarity at a moment when so much public discussion remains untethered from physical reality.

A concrete example close to home: PJM recently announced that it failed to secure sufficient capacity in its latest auction. For the June 2027–May 2028 period, PJM sought commitments for over 152,000 MW and came up nearly 6,000 MW short—the first time it has missed its reliability target. As reported in my local paper on Christmas Eve, this isn’t a theoretical future problem; it’s already here.

Governors like Youngkin—and now Josh Shapiro—continue to speak as if firm power can simply be ordered on demand and are living in an energy fairy tale. As you show so clearly, time, deliverability, and system constraints say otherwise. We are indeed at an inflection point.

Frank,

Thanks for those comments. Each post is a discovery process for me. I think I know something fairly well and then, when I start creating graphs and writing, I learn that I didn’t fully understand what I thought I knew.

I criticize our leaders for their energy blindness but as my last statement suggests, it’s not easy to learn what’s needed.

All the best,

Art

I sure hope the “AI” they’re referring to for their “AI buildout” is not LLMs, because I can’t think of a bigger step backwards than a technology that continually makes up facts, misrepresents references it’s supposedly using, and randomly disobeys instructions.

Greg,

It sounds to me like you don’t have much experience using LLM. I use it all the time. It’s like any powerful tool–it takes time to learn how to use it well.

All the best,

Art

One empire at a time, Art? If it doesn’t work, it goes? It will leave a gaping hole. Classically, a lot of know-how is lost, including in the metropole, e.g. politics now?

I’m thinking about LLMs. Too useful but still tricky; its me that is insecure, dependent on an electronic know-how umbrella that does not translate enough to material resilience in this neighborhood (old age, house and family in GB) if America and electricity simplify. And there is war of course.

Phil,

You must be reading Ulysses and writing comments in stream-of-consciousness style–your comment was hard to decipher.

Your anxiety is understandable but remember that collapse is not a crash—it’s a loss of complexity. I believe that most people crave that in their lives, and only seek novelty because they aren’t happy with the way things are. It’s hard for me to imagine computers and AI disappearing as tools barring a true collapse but their use may be more limited or more costly.

My self-prescribed path is to focus on the inner life.

We sit in the center of the circle while Yes and No chase each other around the circumference.

—Chuang Tzu

All the best,

Art