June 2023 Energy Newsletter

The market has given up on the long-awaited China demand rebound.

Oil has been a bear market for a year yet analysts continue saying that prices will rally. Goldman Sachs, if fact, has called for an unparalleled increase after consistently over-estimating price calls since mid-2022.

A week ago, Goldman wrote,

““Bulls, like ourselves, find comfort in the fact that end-use demand across the commodity complex has not shown recessionary signs and investment in supply remains elusive…We are currently seeing what is likely the largest commodity destocking the complex has ever witnessed.”

I’d like more explanation of what exactly de-stocking means because, frankly, I have no idea what Goldman is talking about for oil.

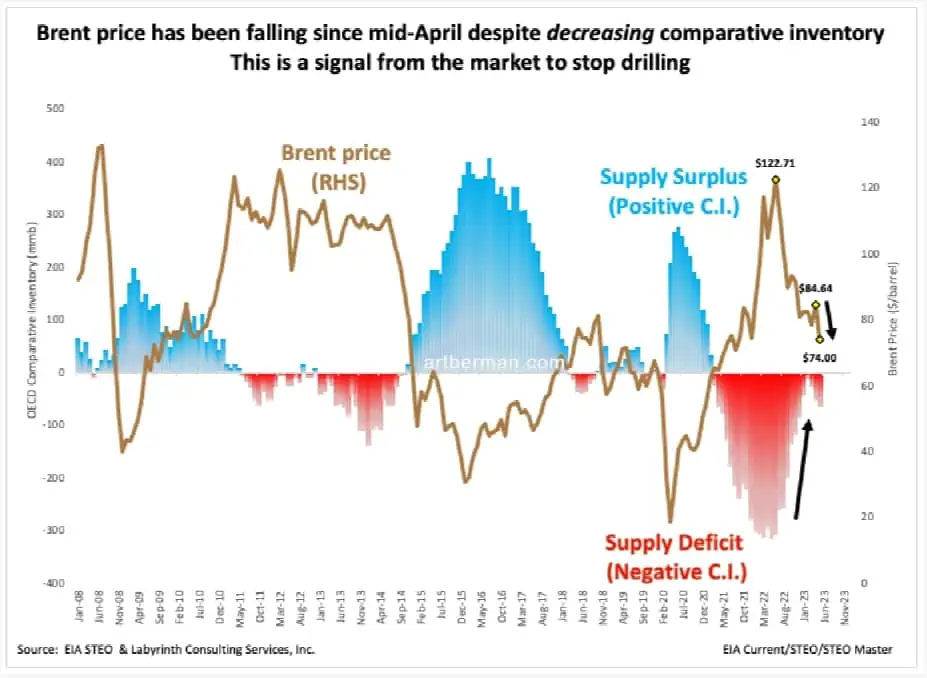

Brent comparative inventory (C.I.) underwent one of the largest commodity re-stocking events the complex has ever witnessed from mid-2022 through the end of last year (Figure 1 red fill). It has gone back into a slight deficit but oil price has fallen. That is a signal from the market to stop drilling because supply is more than adequate.

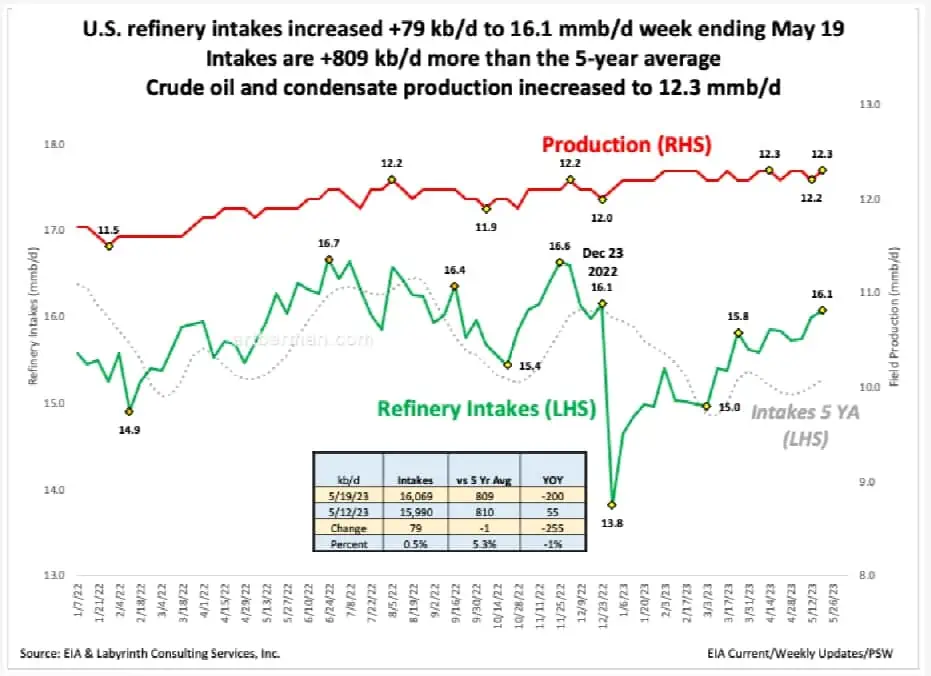

There are for sure some positive indicators—the most important being that U.S. transport fuel consumption has increased to more than the 5-year average since April after languishing below average for most of the period since 2019 (Figure 2).

It is also notable that U.S. refinery intakes are running well above their 5-year average probably reflecting refiners’ sense that demand is healthy and will remain that way for the near term (Figure 3).

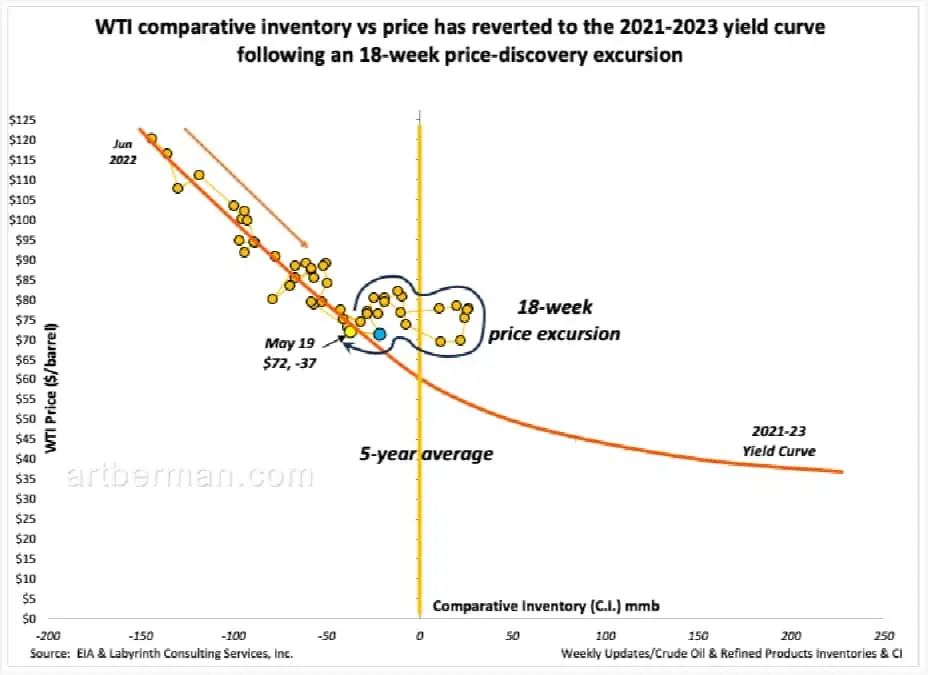

On the other hand, markets seem to be pricing in a fairly substantial economic slowdown as evidenced by the WTI comparative inventory trend shown in Figure 4.

An 18-week WTI price-discovery excursion appears to be over. For more than 4 months, prices have been elevated relative to what the comparative inventory yield curve indicates for the market-clearing price.

Prices began this excursion from the norm at the beginning of 2023 as expectations grew that a strong economic recovery in China would create a massive surge in oil demand. Prices reached $20 more than yield curve indicators as markets sent a supply-urgency message to producers. For the week ending May 19, WTI price returned to the yield curve for its corresponding inventory level.

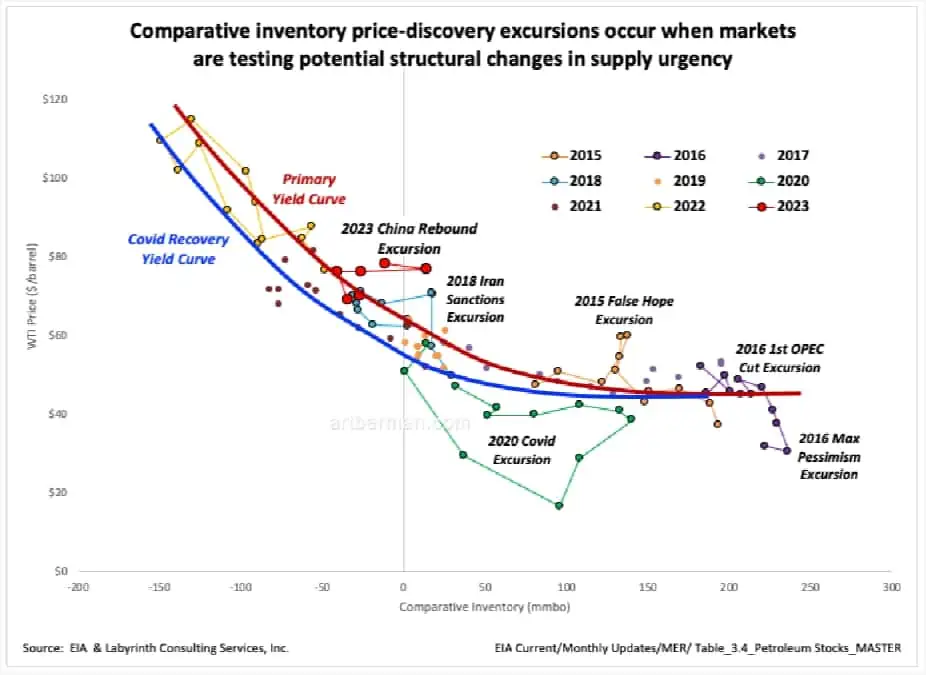

Price discovery excursions generally occur when markets are testing potential structural changes in supply urgency (Figure 5). Notable examples include the “2015 False Hope Excursion,” the early 2016 “Max Pessimism Excursion,” the late 2016 “First OPEC Cut Excursion,” the “2018 Iran Sanctions Excursion,” the “2020 Covid Excursion,” and the “2023 China Rebound Excursion.”

These excursions commonly last 4-6 months as traders test how far counter-parties are willing to go to bet that a structural change has occurred. It is not uncommon for prices to reach 30% more than yield curve estimates. With few exceptions, these prove to be false alarms and price-volume data reverts to the yield curve over time.

The recent 2023 China Rebound Excursion is geometrically similar to the 2018 Iran Sanctions Excursion that happened when the United States abandoned the Iran nuclear agreement and announced full oil-export sanctions against Iran. The market braced for the loss of millions of barrels per day of crude oil by raising prices. In the end, oil supply was adequate and prices collapsed in late 2018.

Meanwhile, WTI price fell to the bottom of the Bollinger bands on May 31 (Figure 6). This suggests that it is oversold. Comparative inventory indicates a market clearing price of at least $70-72 at this inventory level so it is not surprising that futures are trading higher at almost $71 this morning, June 1.

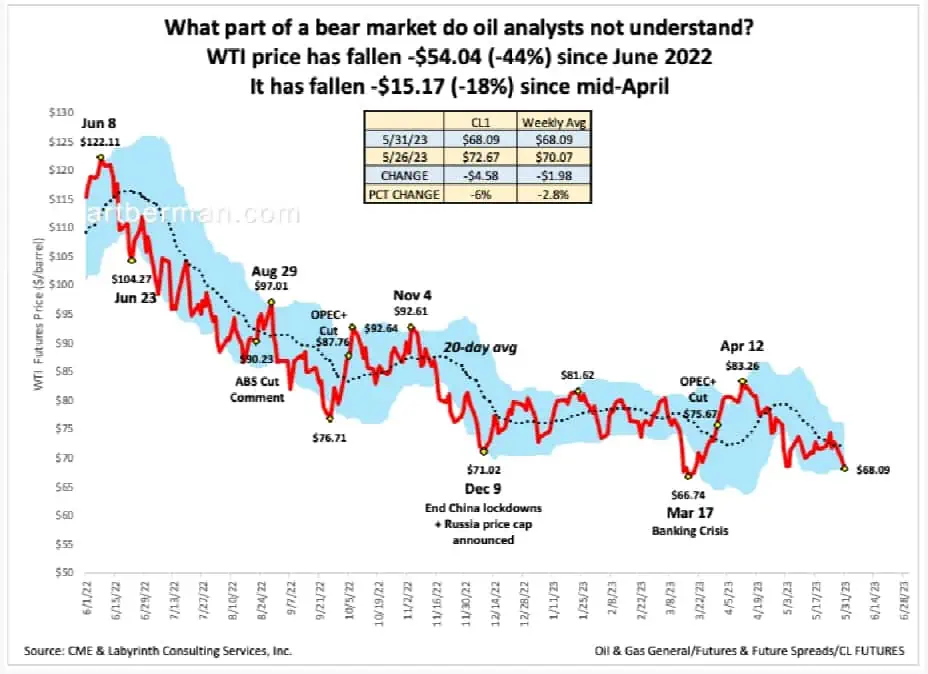

It is difficult to understand why smart analysts continue to expect higher oil prices just around the corner. What part of a bear market do they not understand? WTI price has fallen -$54.04 (-44%) since June 2022. It has fallen -$15.17 (-18%) since mid-April.

China is recovering but how could it be otherwise after months of Covid lockdowns? The much-anticipated surge in oil demand has not and is unlikely to happen based on the economic data coming out of China.

Oil is priced about where it should be all things considered. I expect the market to go largely nowhere until something new happens to affect supply urgency. It will pass through high frequency cycles as it always does but reading anything more into the upward parts of those cycles risks falling into the trap of bear-market math.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts