Permian Production Will Not Peak Because of Depletion

Production from the Permian basin is increasing and has years if not decades before depletion. Whether production rises or falls will have less to do with geology than with market forces.

This is based on data and runs counter to the narrative championed by Goehring and Rozencwajg. Since 2018, G&R have called for a Permian production peak by about 2025. In its recently published The Permian Basin Is Depleting Faster Than We Thought, the analysts stated,

“For the first time, productivity per lateral foot registered a 6% year-on-year decline in the Permian. According to our models, this proves the industry has drilled its best wells; basin-wide production decline is likely not far behind.”

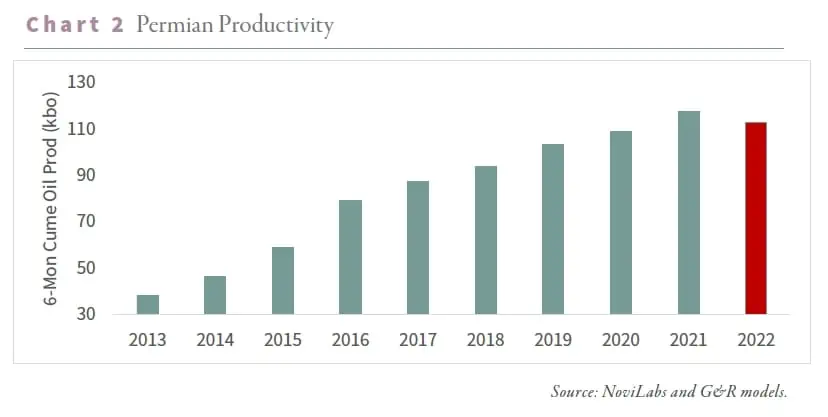

G&R provided this graph in partial support of their claim.

The graph does not support G&R’s conclusion that the Permian basin is depleting faster than we thought. It shows that the average production rate for wells completed in 2022 was less than for wells completed in 2021. Those are very different things and G&R doesn’t seem to understand the difference. It is hardly surprising that investors misinterpret G&R’s message to mean that Permian production’s days are numbered.

In fact, G&R conflate three separate factors: production rate, decline rate, and depletion rate.

Production rate is a measure of how many barrels per day a well or a field produces at some moment or over some interval of time. Goehring & Rozencwajg’s graph (my Figure 1) shows the first 6-month cumulative production for a series of years divided by the number of days in 6 months to show a rate.

We do not know if that is necessarily a maximum rate or if producers were limiting output because of economic factors. We do not know how many wells were used in each year to determine the average. We do not know how drilled uncompleted wells (DUCs) affected the lower 2022 value. DUCs were completed to save money not because they were the best wells—why were they left uncompleted in the first place? Nor do we now how limited frack crew availability may have affected well performance.

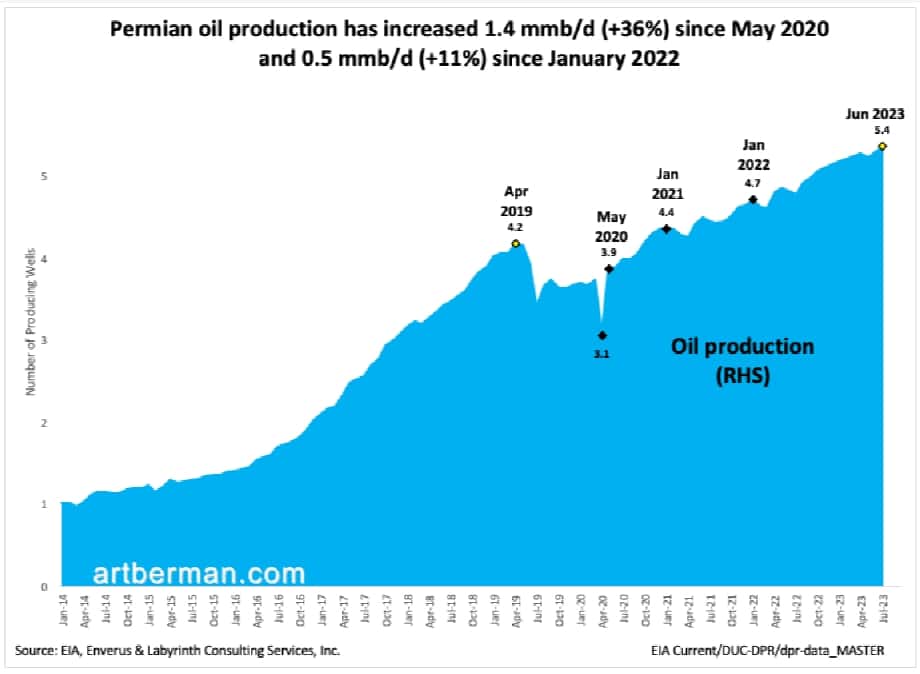

Decline rate is a measure of how production from a well or a field decreases over time. Permian production has not declined nor does its rate of increase suggest that decline is imminent. It has increased 1.4 mmb/d (+36%) since May 2020 and 0.5 mmb/d (+11%) since January 2022 (Figure 2).

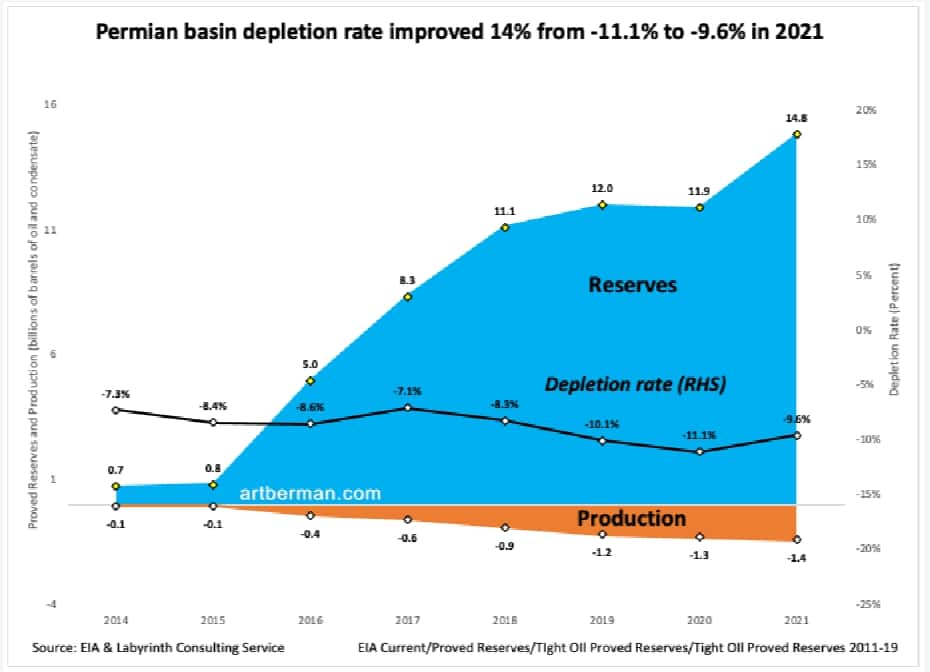

Depletion rate is a measure of how proved reserves decrease over time because of production. The Permian basin depletion rate actually improved 14% from -11.1% to -9.6% in 2021 (Figure 3). More importantly, proved reserves have increased every year since the EIA has reported tight oil reserve data. Depletion is, therefore, a moving target and hardly a concern for now.

Another way to think about the same data is to divide reserves by production to estimate remaining years of supply. Permian basin years of supply increased +16% from 9 to 10.4 years in 2021, and proved reserves increased +24% from 11.9 to 14.8 billion barrels (Figure 4). That means that if no new reserves are found and production continues at the current rate, full depletion will not occur before 2031. If depletion begins, it will be because new reserves are not found and, in that case, the rate of production will decrease thereby extending the field life well past 2031 in the most pessimistic case.

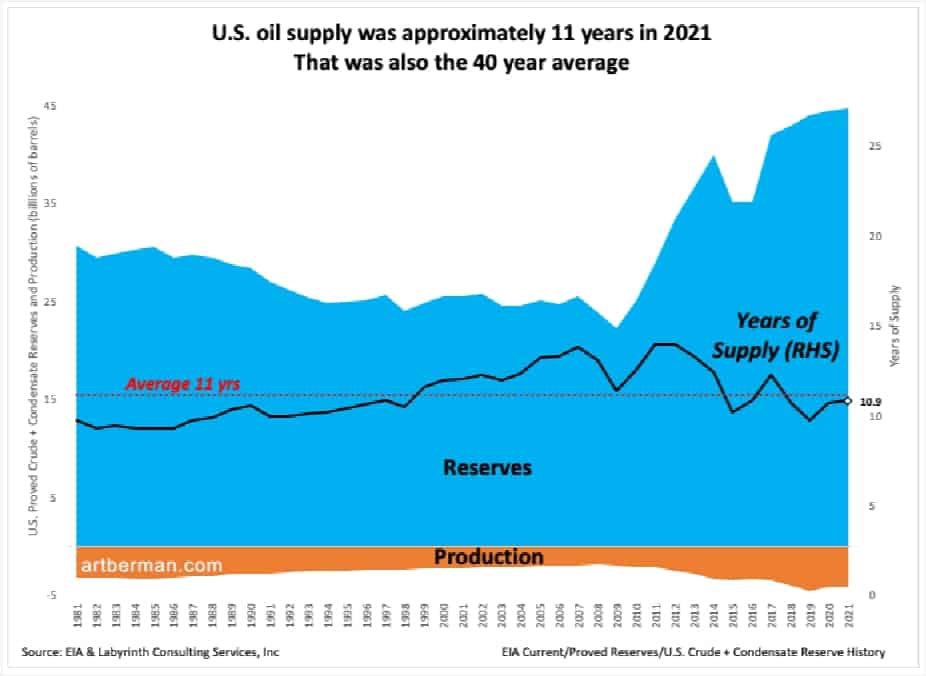

That’s still a sobering thought but the bigger picture is that there were about 11 years of U.S. oil supply in 2021 (Figure 5). The U.S. has had about 11 years of oil supply in every year since 1981! That’s because more reserves are added in almost every year. That will not always be the case but it does reflect the history for the U.S.

The Real Deal

Goehring & Rozencwajg do not specify the basis for their belief that a Permian production decline is imminent beyond the chart shown above, and their usual mumbo-jumbo about their neural network methodology.

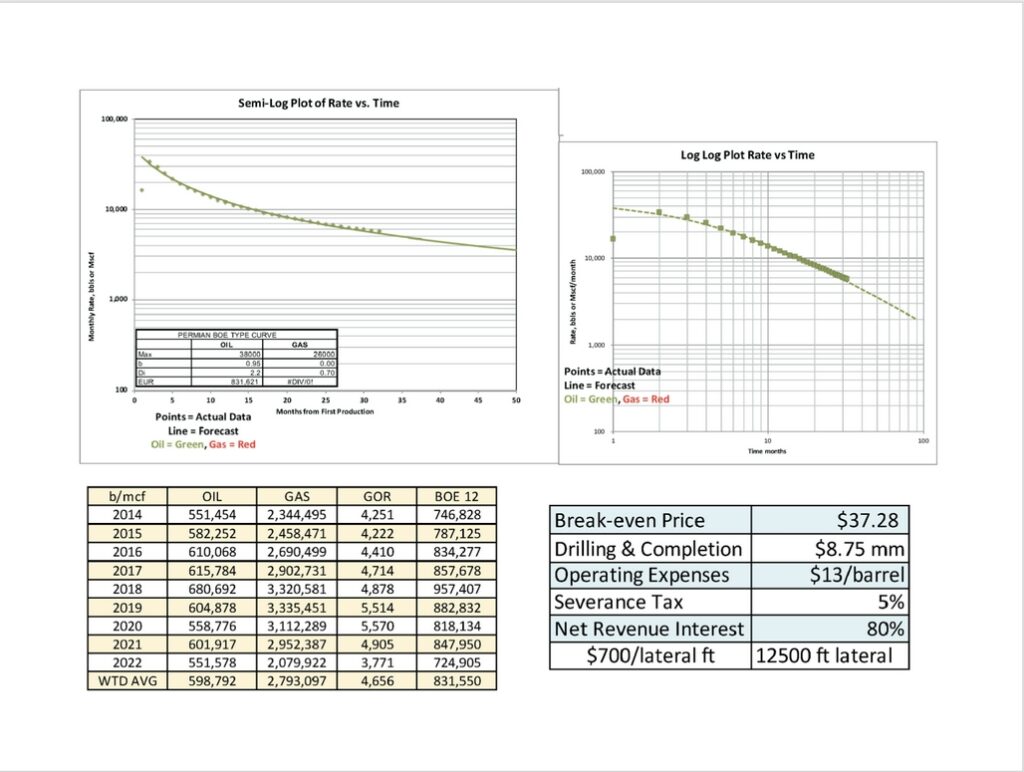

My approach, on the other hand, is straight-forward and based on bottom-up well performance and map evaluation. I determined average well EUR (estimated ultimate recovery) using standard rate vs time decline-curve analysis for each of the three main tight oil plays in the Permian basin. I consolidated these into an integrated type-curve based on weighted averaging. This indicates that the average Bone Spring-Trend/Spraberry, and Wolfcamp EUR is almost 832,000 barrels of oil equivalent, and its break-even price is about $37 per barrel using an 8% discount rate (Figure 6).

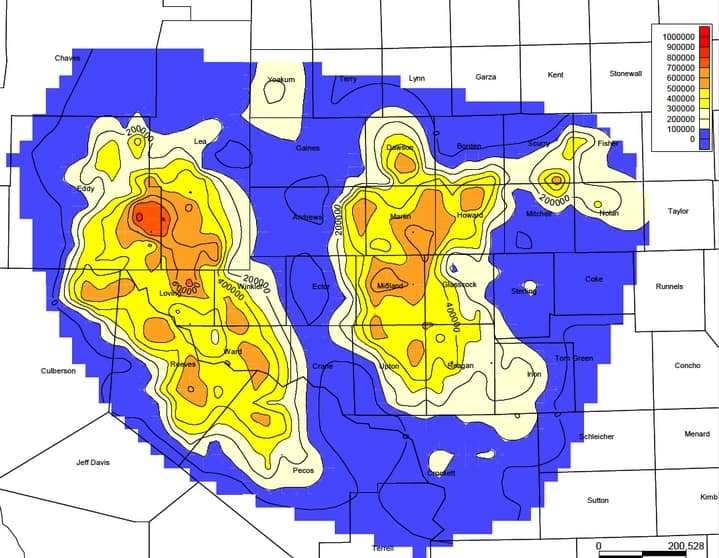

Next, I made a map of EUR values by well in barrels of oil equivalent (BOE) (Figure 7). The blue color represents EUR from zero to 100,000 BOE and the yellow, orange and red colors show progressively higher EUR values up to 1 million barrels per well.

I then determined the average well spacing by counting wells inside the 275,000 barrel-per-well contour (approximate break-even price at about $100/barrel as a long-term average over the next decade or so) and divided by the area. That calculation resulted in an average well spacing of 1 well per 175 acres or 4 wells per square mile.

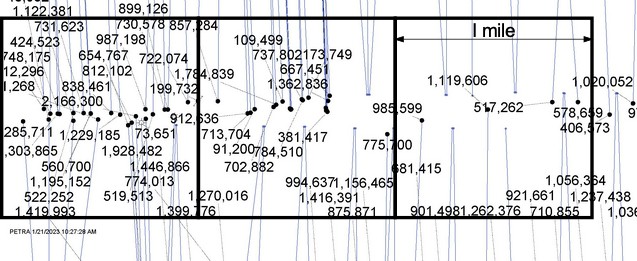

Finally, I compared that well spacing to areas with the closest well spacing in which average well EURs were commercial at present prices (Figure 8. EUR values are shown). That well spacing averaged about 1 well per 40 acres although in some areas spacing was even closer (as in the left-hand square mile in Figure 8).

That suggests that as few as 25% of potentially commercial well locations have been drilled on 40-acre spacing so far in the basin. Adjusting for areas that are already drilled on closer well spacing, perhaps only 50% of potentially commercial locations have been drilled so far.

What I have described here is a very-high level evaluation that is intended only to provide a rough approximation of remaining oil potential in the Permian basin. Nevertheless, this study suggests that many years and perhaps decades of drilling remain in the plays based on the geology. Discount my estimates all you want and it is still difficult to agree with Goehring and Rozencwajg’s claim that the Permian basin is depleting rapidly.

Arjun Murti summarized the state of the Permian clearly in late June.

“Are we seeing signs of basin maturity in the Permian basin?…We’re not seeing that yet…We’ve added supply.”

Goehring and Rozencwajg may be right that Permian production will peak in a few years but if so, it will be for lack of available capital and credit, and not because of the medium-term limitations of geology. In any case, G&A’s claim that this will happen because of depletion is patently false.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts