What the Oil and Commodity Bulls Are Missing

The oil bulls have come out of hibernation.

Last week, the IEA (International Energy Agency) raised its oil demand forecast. This week, the EIA (U.S. Energy Information Administration) increased its oil price forecast following another extension of the OPEC+ production cuts.

Former Goldman Sachs commodities chief Jeff Currie commented in a recent interview that,

“Being short oil and commodities in a late-cycle expansion is like being short natural gas in a blizzard…The upside here is significant.”

Jeff Currie, Carlyle’s chief strategy officer of energy pathways

Being short on oil is a terrible idea right now but I’m not as confident as Currie that the upside is significant.

His logic is that the cycle of economic weakness produced by central banks’ efforts to slow inflation is ending. As economic activity recovers, demand for commodities including oil will increase substantially.

Perhaps but I believe that this is old-paradigm thinking.

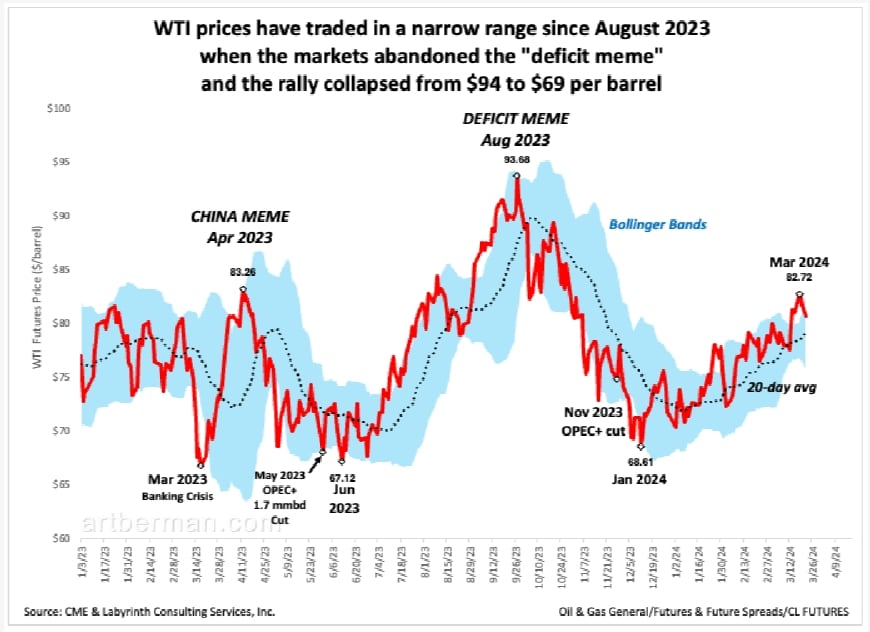

Oil prices have traded in a narrow range since markets abandoned the “deficit meme” that produced a false price rally from June through August 2023 (Figure 1). At the same time, prices have gradually increased since mid-January 2024 with generally higher, high prices and higher, low prices within short-term cycles.

when the markets abandoned the “deficit meme” and the rally collapsed from $94 to $69 per barrel.

Source: CME & Labyrinth Consulting Services, Inc.

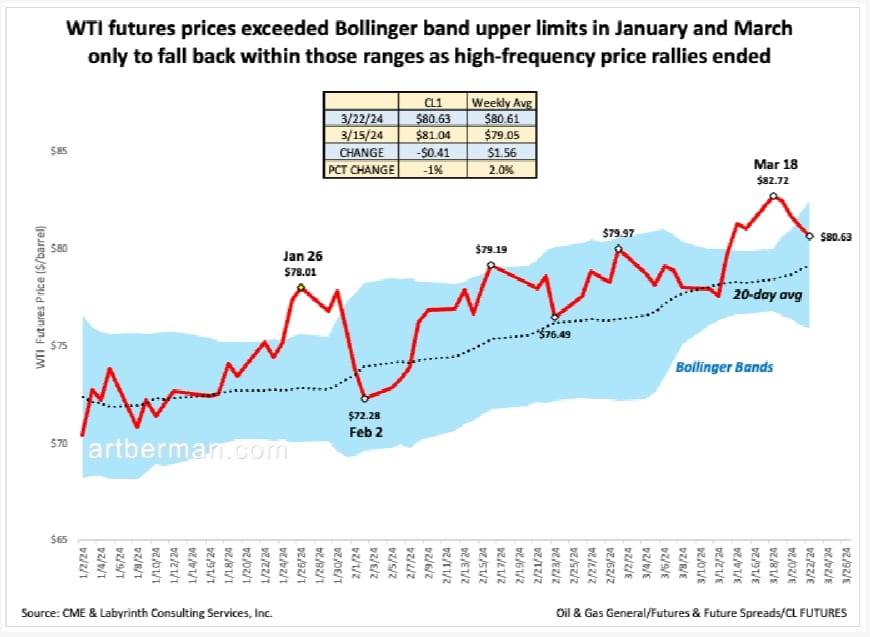

During that period of gradual price rise, WTI futures prices only exceeded Bollinger band upper limits in January and March before falling back within normal ranges (Figure 2).

There are some fairly hard limits on how quickly markets allow prices to rise or fall under ordinary circumstances. In other words, prices will probably increase slowly and in uneven cycles as they have all year rather than more intentionally as oil bulls anticipate.

only to fall back within those ranges as high-frequency price rallies ended.

Source: CME & Labyrinth Consulting Services, Inc.

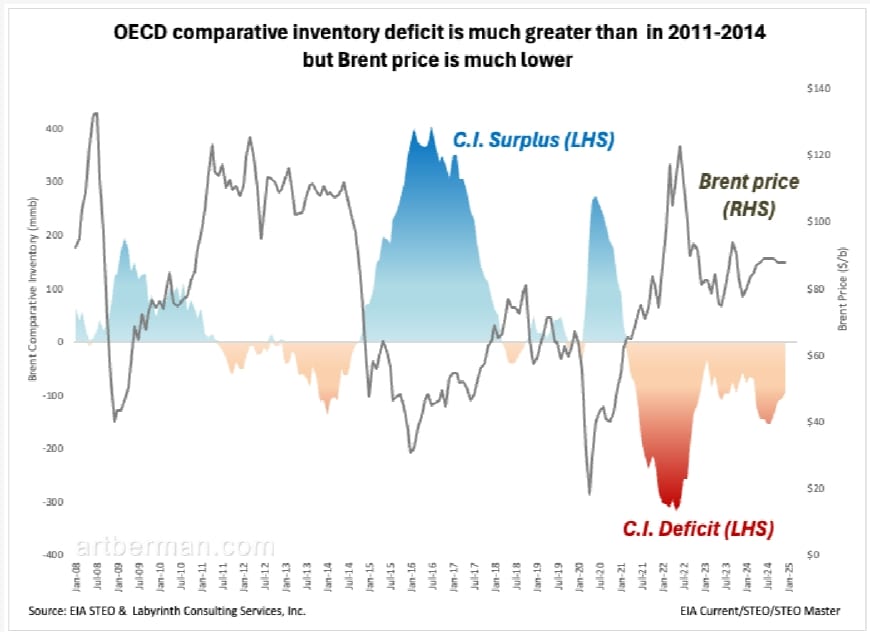

Figure 3. shows that the current OECD comparative inventory (C.I.) deficit is much greater than in 2011-2014

but Brent price is much lower. That’s how much things have changed for oil.

A decade ago, a persistent C.I. deficit that averaged -47 mmb resulted in the longest period of sustained high oil prices in history—Brent price averaged $109 per barrel from mid-2011 through the end of 2014.

By contrast, the C.I. deficit since October 2022 is twice as great—after the main effects of the Ukraine invasion subsided—but Brent has averaged only $85. The market’s sense of supply urgency is much lower than it was from 2011 through 2014.

but Brent price is much lower. Source: EIA STEO & Labyrinth Consulting Services, Inc.

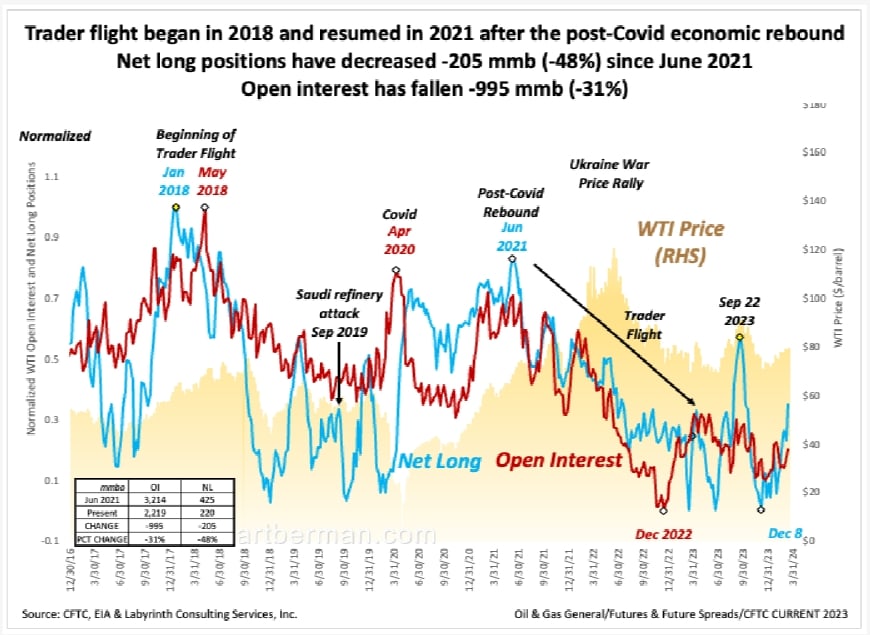

The change in supply urgency is underscored by the flight of portfolio and money managers from trading in oil futures.

Trader flight began in 2018. Investors lost patience after a decade of poor financial returns from shale gas and tight oil companies and began exiting their stocks. Traders followed.

In April 2018, U.S. president Trump announced that the United States would withdraw from the Iran nuclear deal (JCPOA) agreed to by his predecessor Obama in 2015. The U.S. would fully sanction Iranian oil exports which amounted to about 2.1 million barrels per day at the time. Oil prices reached their highest level since 2018.

When Trump changed his position and granted waivers to certain countries that imported Iranian oil, traders lost billions of dollars. The oil industry has never recovered from 2018 and may never recover. This is what oil bulls fail to understand or accept.

When Saudi Arabia’s main refinery complex was attacked by Iran-backed Houthis in September of 2019, oil markets barely reacted. If anything like this had happened in the previous fifty years, oil prices would have almost certainly gone to record high levels.

This should have been a flashing yellow light for bullish analysts and investors that the oil paradigm had changed.

The trader flight that began in 2018 resumed in 2021 after the post-Covid economic rebound. Since then, WTI net long positions have decreased -205 mmb (-48%) and open interest has fallen -995 mmb (-31%) (Figure 4).

Net long positions have decreased -205 mmb (-48%) since June 2021.

Open interest has fallen -995 mmb (-31%). Source: CFTC, EIA & Labyrinth Consulting Services, Inc.

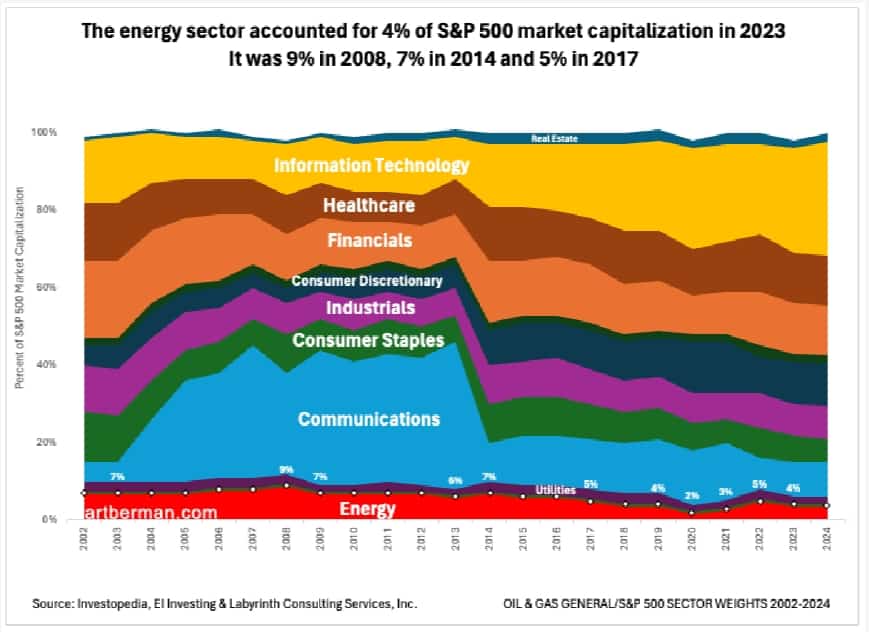

The entire energy sector—including renewables—made up just 4% of S&P 500 market capitalization in 2023 (Figure 5). It was 9% in 2008, 7% in 2014 and 5% in 2017.

It was 9% in 2008, 7% in 2014 and 5% in 2017. Source: Investopedia, EI Investing & Labyrinth Consulting Services, Inc.

The problem is no longer performance as it was in the decade before 2018. Higher oil prices and less emphasis on production growth have transformed oil and gas companies into cash machines in the last few years.

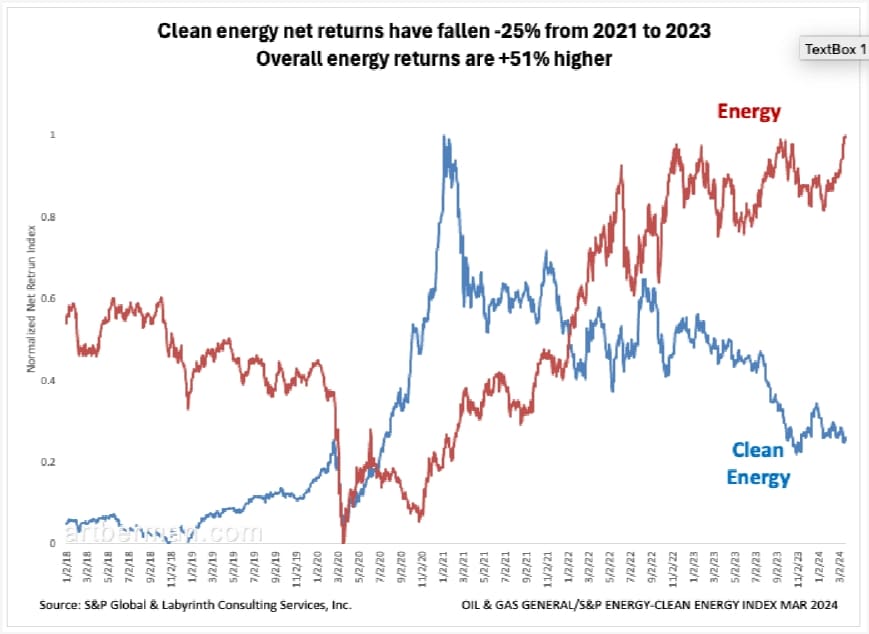

Overall energy returns were 51% higher in 2023 than they were in 2021 (Figure 6). That has not increased the energy’s sector weighting. Interestingly, clean energy returns fell 25% during that period.

Overall energy returns are +51% higher. Source: S&P Global & Labyrinth Consulting Services, Inc.

The market is neither energy-blind nor wrong.

What is the market? It’s our collective knowledge and experience about the marginal returns on trades and investments. Markets do not always do what is best for society but they are incredibly good at picking winners and losers.

Markets are telling us that oil and gas—and indeed energy—is a losing bet at the margin. That means that the cost of expanding new capacity beyond its current rate of growth does not warrant its cost. That message probably applies to commodities as well.

This seems counter-intuitive because society’s need for energy and commodities is growing faster than its supply. And that is where the market is sending a message that most are not ready to hear.

The market is shorting growth. That’s a paradigm change.

In 2022, Goehring and Rozencwajg boldly announced that the commodity bull market has only just begun. They have since acknowledged that the bull is moving more slowly than they believed in 2022 but have not changed their story. They have lately stated that oil has moved “From Uninvestible to Must Own.”

There’s nothing wrong with Goehring and Rozencwajg’s—or Jeff Currie’s—analysis except that the paradigm that made it valid has expired. It assumes that demand for oil and other commodities will continue to increase because the human enterprise must continue to grow.

The market is saying that it’s not so sure about that.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Art, we’re talking growth in terms of “The Limits to Growth,” per the Club of Rome? If so, 1) looks like it’s right on schedule and 2) I would think the overly financialzed layers of our economy are especially susceptible in such a situation, as they are epiphenomena of the overall energy scenario and predicated on the notion of continual growth. Any refuge from a storm of that nature?

Thanks for your analysis and insights.

Pete,

The Limits to Growth projections have been recently fact checked and they are tracking amazingly well from assumptions made 50 years ago.

https://onlinelibrary.wiley.com/doi/full/10.1111/jiec.13442

All the best,

Art

Thanks, Art.

Tangent, but perhaps in that same vein, Geoffrey West of Santa Fe Institute recently did a talk at John Hopkins where he presented data pertaining to a speculative upcoming “singularity”…not exactly in the Kurzweil sense, necessarily, but holding forth the possibility of stagnation preceding collapse: https://youtu.be/pjJFzZpBN2c?si=ZJxg6ba4RgYW8b76

Looking around, stagnation and then collapse seem like they might well be on the menu for our complex civilization…

Pete,

I’m familiar with West’s ideas about singularity or phase shift. This is what Nate Hagens calls The Great Simplification.

All the best,

Art

What about the so-called dumb money? Won’t average people invest in energy and commodities if their prices go up due to shortages? Though it won’t help, which the smart money knows since there’s little oil to be discovered that’s profitable. Sounds like a depression is coming, and worse

Alice,

Oil and commodity prices will increase–no doubt. The smart money will profit by trading futures contracts or playing stock price fluctuations but I don’t see much appetite for true investment.

All the best,

Art

Thanks again for sharing your expertise in this complicated arena!

David,

Thanks for that!

All the best,

Art

I think the paradigm shift is Saudi will not maintain industry spare capacity any more. With only 3% surplus capacity left globally, this means increased volatility in prices as the surplus erodes over the next 2 or 3 years. Surplus will erode very quickly once US shale peaks. Eventually, consuming countries must fill strategic storage because Saudi will be wide open (and on decline). Volatility will be required to balance markets (not Saudi).

Also, the pace of Energy Transition will disappoint. These are big projects which take 4 to 7 years to get to production. Most of the projects are low return and will struggle to get financing. Meanwhile, electricity demand will march higher because of AI and emerging countries electrifying.

Upstream development capital is being reduced by 15 to 20% because of the capex to reduce co2 emissions and ch4 emisssions. This means we are actually reducing upstream capex by alot more than most realize.

Rudy,

I agree with your comments. The energy transition is largely imaginary.

All the best,

Art

All people strive to improve their living conditions which requires an increase in personal energy consumption. Whether the “strivers” work to improve the general status of a lower level country as a whole or, as been seen recently, cross an open border into a country with a much higher per capita carbon footprint, energy consumption will rise as a result of either action.

Markets may be like weather but I allow that both can change quickly. The past decade has spoiled us in the US with energy abundance. When that paradigm changes , I expect prices to increase but this will have unknown impacts. I would love to see an Apollo type small nuclear program but I would also like to see the national debt decrease. For some reason, it takes a bigger and bigger crisis for us to move.

Ron,

I am deeply skeptical that nuclear energy can make much of a difference—there’s just no possibility that capacity can be increased under any frictionless scenario to supply more than a few hours per day of renewable backup. Here is a thought experiment from a recent post: https://www.artberman.com/blog/the-energy-transition-is-being-led-by-a-clown-car/

I think it’s time to stop chasing nuclear windmills and get honest about what can be done.

All the best,

Art

Debt-driven global demand, w/China as the poster child, has been artificially pulled forth for many goods and services. Now perhaps we’re hitting the “demand wall” though G&R contend that demand will not be an issue.

Interesting take on oil markets and by extension commodity markets. If you’re reading the tea leaves properly, we are going to be in for a rough ride. You’re really suggesting that despite upcoming shortages, there won’t be the demand, and as a result prices will not rise on the shortage of supply. I think you’re suggesting a depression, am I right?

Ted,

Society may have reached a level of complexity in which additional investment in energy does not justify its marginal cost, that the growth of the human enterprise including economic growth is being discounted by the market. That doesn’t mean a depression necessarily although collapse of the financial system is a valid concern. It could also mean massive disruption of civil society through war, immigration and other geopolitical crises.

I recommend reading Joseph Tainter’s The Collapse of Complex Societies https://theworthyhouse.com/wp-content/uploads/2020/03/Collapse-of-Complex-Societies-Tainter-PDF.pdf

All the best,

Art

Art – Great analysis! I also believe the Kabul actively intervenes in the oil market. This leads to negative sentiment driven by a desire to suppress market forces that previously created the bullish euphoria.

The sentiment may still change as demand continues to whittle down limited supply.

Time will tell.

Carl,

Thanks for your comments.

I don’t believe that oil market manipulation is a big factor. It takes far more money than anyone—-including countries—-has to affect the largest commodity market in the world for very long.

All the best,

Art

Interesting. Given the structural crude oil deficit that you anticipate later this decade, Art, isn’t the market wrong? Even if the economy doesn’t grow new sources of supply to replace depletion will be costlier?

Archith,

Markets cannot be wrong any more than the weather can be wrong. They simply are.

Markets are apparently indicating that the cost of increasing supply rate cannot be justified. Read Joseph Tainter’s Collapse of Complex Societies.

All the best,

Art

Thanks Art!