Art Berman Newsletter: August 2021 (2021-7)

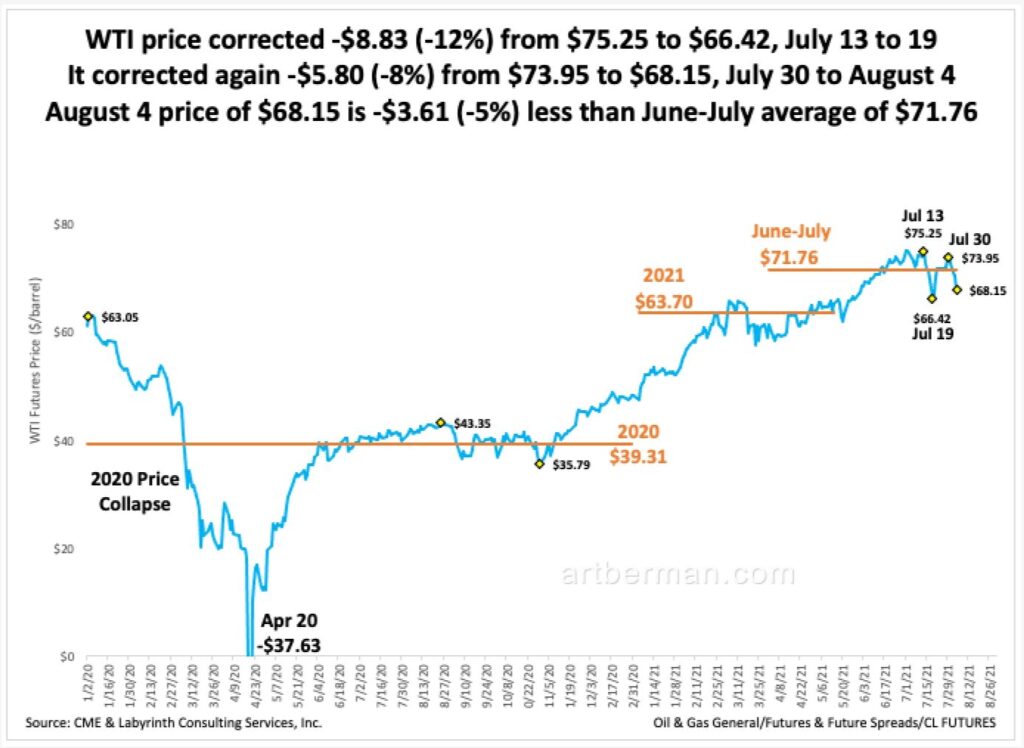

Oil price has corrected downward twice in the last three weeks.

Brent fell -$7.87 (-10%) and WTI dropped -$8.83 (-12%) between July 13 and July 19 (Figure 1). WTI moved back into the $70 range two days later but fell again, this time by -$5.80 (-8%) from from $73.95 to $68.15 between July 30 to August 4. Price was higher yesterday, August 5, but is again trading lower than on August 4.

Recent price fluctuations are generally attributed to demand concerns because of the resurgent Covid-19 delta variant. Most analysts believe that these are temporary set backs and probably represent market over-reactions.

I disagree and believe these closely-spaced price adjustments reflect more fundamental concerns about the state of the global economy and its effect on oil-demand recovery.

The popular narrative is that oil supply is tight and that oil demand is surging and will soon surpass 2018 and 2019. I find little technical support for those opinions.

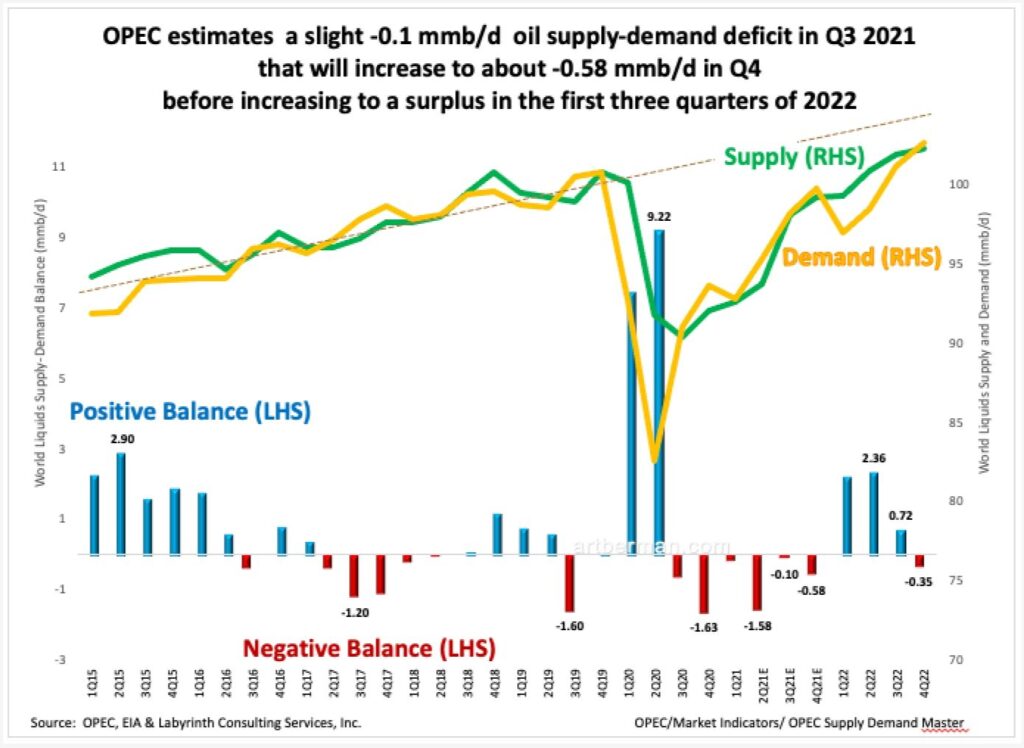

Figure 2 shows OPEC ‘s forecast for supply in green and demand in gold. The corresponding supply-demand balance values are shown by the blue and red bars.

OPEC estimates a slight -0.1 mmb/d oil supply-demand deficit in Q3 2021 that is expected to increase to about -0.58 mmb/d in Q4 before moving to a surplus in the first three quarters of 2022 (Figure 2). That sounds like approximate balance and not a bad place to be but certainly not the incredibly tight supply than Amrita Sen describes.

OPEC believes that demand will surpass the Q4 2019 level in Q3 of 2022. That somewhat supports the popular narrative about demand although Q3 2022 is not exactly right around the corner.

The important thing, however, is that markets don’t care about demand—they care about demand growth. The dashed brown line in Figure 2 shows the trend of demand growth from 2015 through 2019. Even though demand in late 2022 may exceed 2019 levels, demand growth will about -2.5 mmb/d less than the pre-Covid trend. In other words, demand growth will not yet have recovered by the end of 2022.

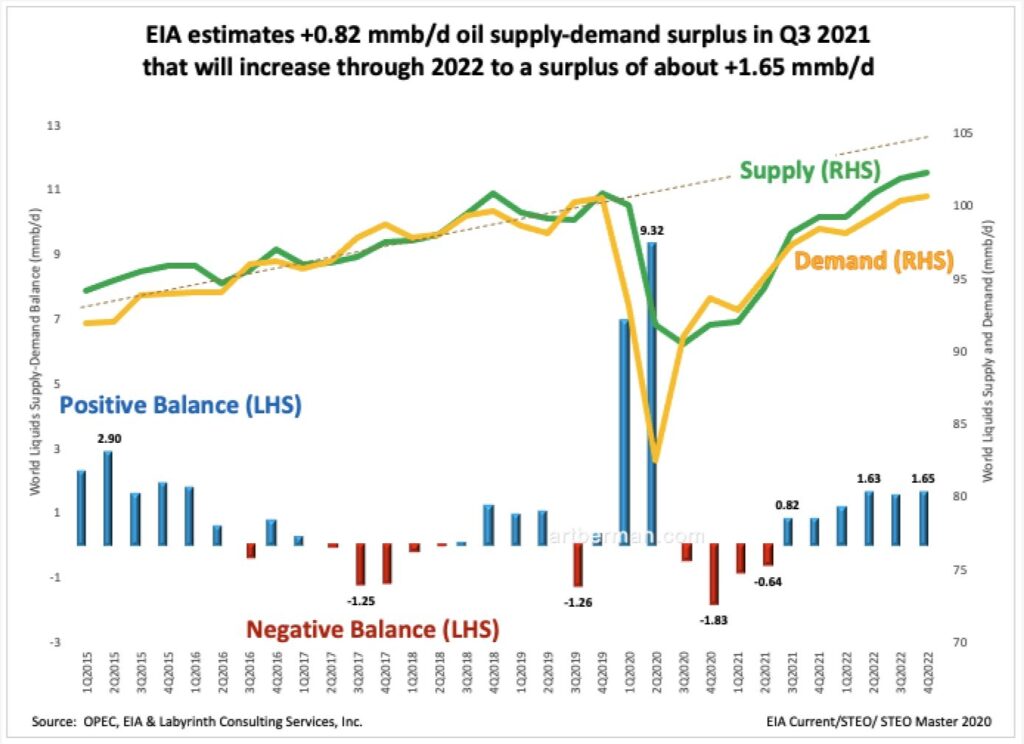

Figure 3 shows EIA’s forecast for supply and demand using the same symbol conventions as in Figure 2. Although its form is similar to OPEC’s, it indicates that world supply and demand are already in a surplus of +0.82 mmb/d in Q3 2021. It projects a surplus that will increase through 2022 to about +1.65 mmb/d. EIA’s forecast for demand in Q4 2022 is 100.6 mmb/d which is about equal to the level in Q4 2019. Supply is expected to be about +1.65 mmb/d more than demand.

The striking feature in both forecasts is that supply is expected to exceed demand for much of the forecast period. World supply is estimated to increase about +8 mmb/d from 94 mmb/d in Q2 2021 to 102 mmb/d by the end of 2022. Where will that supply come from?

Much of it will come from OPEC+ as it gradually releases withheld volumes back into the world market but some will have to come from non-OPEC+ countries.

U.S. output has accounted for nearly all supply growth over the last 10 years. Production is down from almost 13 mmb/d in early 2020 to about 11.2 mmb/d today. EIA forecasts a gradual increase to 11.5 mmb/d by the end of 2021 and additional increase to 12.3 mmb/d by the end of 2022. That will add about another +1 mmb/d to world supply.

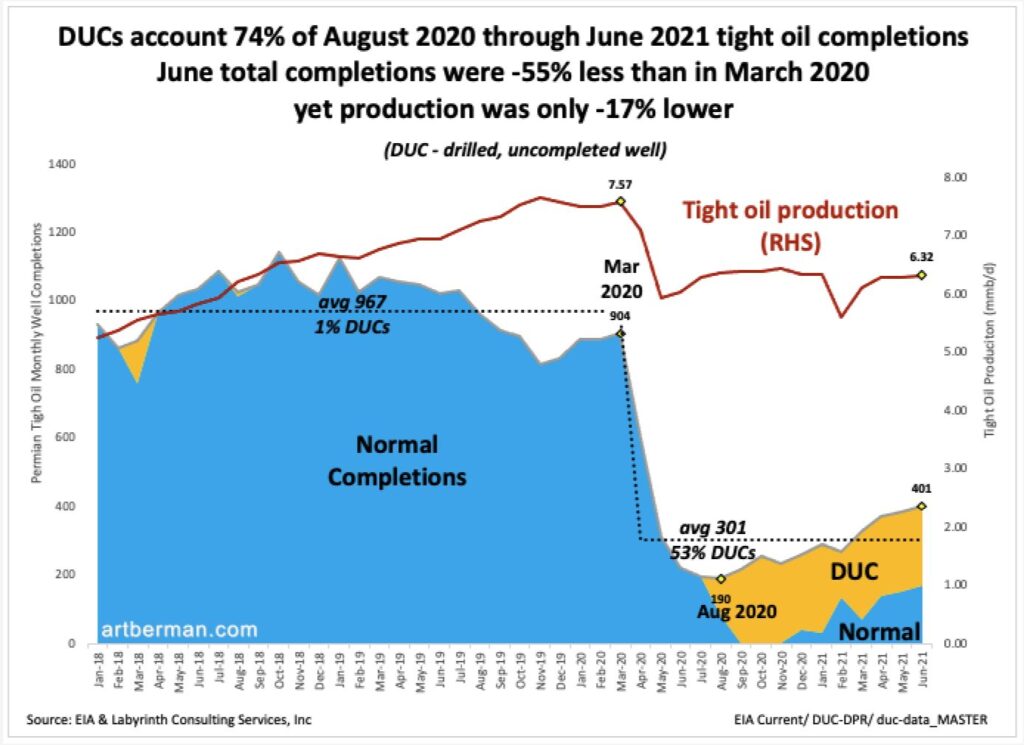

I have been skeptical of EIA’s forecasts because rig counts are only about half of what they were in 2018 when U.S. output was 11 to 11.5 mmb/d. On the other hand, drilled uncompleted wells (DUCs) are often mentioned as a way around the problem of too few drilling wells. I looked at well completions in order to address the role of DUCs in U.S. supply. This data is only publicly available for tight oil and shale gas wells.

In Figure 4, normal completions are shown in blue and DUC completions in gold. DUCs account for 74% of tight oil completions since August 2020 but were inconsequential before March 2020. DUCs are, therefore, an important component of today’s supply.

Total completions including DUCs are less than half the levels now as in March 2020 before the Covid-19 collapse in production and drilling. That seems to support the observation about rig count being too low to support 11.5 mmb/d. The problem is that oil production was only -11% lower in June compared to March 2020 despite -56% fewer well completions.

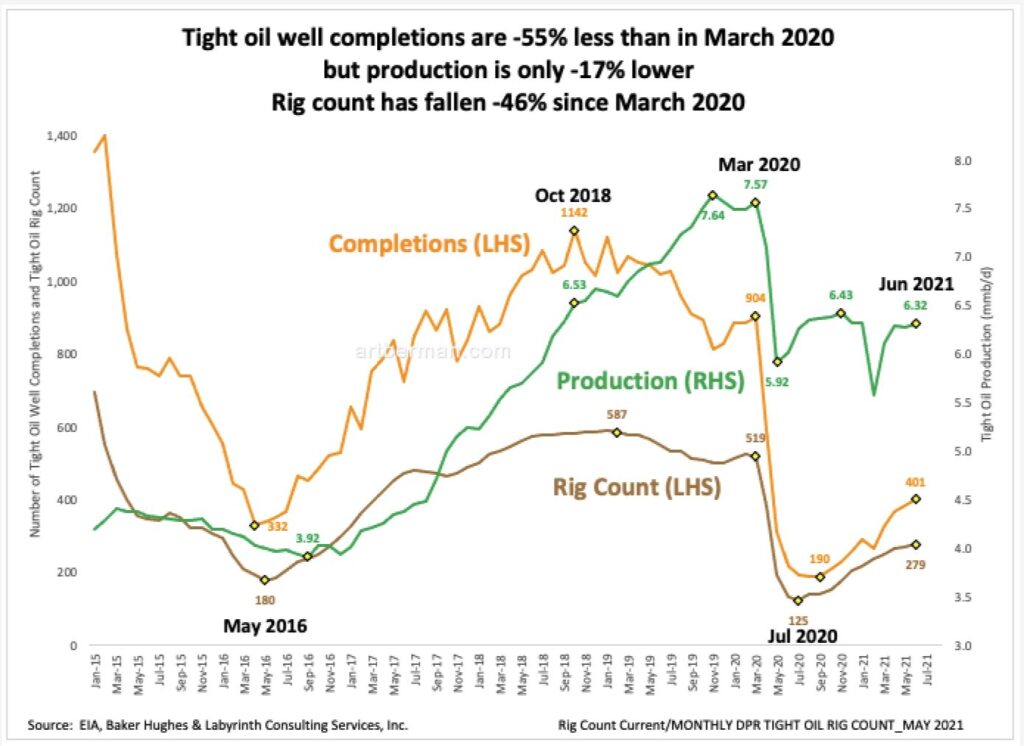

The explanation seems to be that well performance has improved dramatically. In Figure 5, tight oil completions are shown in gold, the tight oil rig count in brown, and tight oil production in green.

Completions after the 2014-2016 price collapse reached a monthly maximum of 1,142 in October 2018. By March 2020, the number of monthly completions had dropped -20% to 904 but tight oil production increased +16% from 6.53 to 7.57 mmb/d. The only way to explain that is for the performance of newly completed wells to be far better than previously completed wells.

The good news is that well performance increased before the Covid collapse in March 2020. The bad news is that as rig count and completions recovered, production has stayed flat or decreased somewhat. That may mean that the large number of DUCs completed during that time period have not performed especially well or that companies are unable to afford the technology that worked so well from 2018 to 2020. Alternatively, it may mean that the performance gains were because of location high-grading that was not sustainable.

Oil has corrected downward twice in three weeks. That is a signal that analyst pronouncements about tight supply and surging demand may not be quite right. Pioneer CEO Scott Sheffield recently said that the oil market is “is probably better than any time that I’ve seen it in the last 10 years.” That’s a good indication that they are not.

The effects of the worst economic recession since the 1930s have not magically disappeared. Most analysts and investors apparently believe that they have. Markets are smarter and know that is nor true. For at least the second time in the last 20 years, a debt problem has been resolved with more debt.

The five charts in this newsletter say the same thing in different ways. Oil markets have made an impressive recovery since last March and April but considerable weakness and uncertainty remains.

Oil markets have been on OPEC+ life support for 15 months. Now, analysts assure us that the patient can go home, is stronger than ever and will need no medication or therapy. I would get a second opinion.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

I’m not seeing how this current strategy by most US producers can maintain current production levels through 2022.

So does this mean there is a massive decrease in duc inventory and at some point in the next year all this “restraint” in capex by producers will disappear?