Art Berman Newsletter: September 2021 (2021-8)

Most analysts believe that higher oil prices are inevitable by the end of the year. Those same analysts were confident that prices would be higher by September but they have fallen by at least 10% three separate times in just over a month. After the latest rally, WTI is 8% less than it was in mid-July. These are not ordinarily signals for higher prices.

It is unlikely that WTI price will reach $80 in 2021 for reasons that include:

- Supply-demand forecasts agree that a global over-supply of oil is likely in late 2021 or early 2022.

- OPEC has almost 7 mmb/d of spare capacity.

- Comparative inventory suggests that markets have re-priced oil downward 10-15% since 2019.

- Supply urgency over U.S. output has decreased with rig-use efficiency gains.

- The demand recovery has stalled.

- Markets are shorting oil because of energy transition expectations.

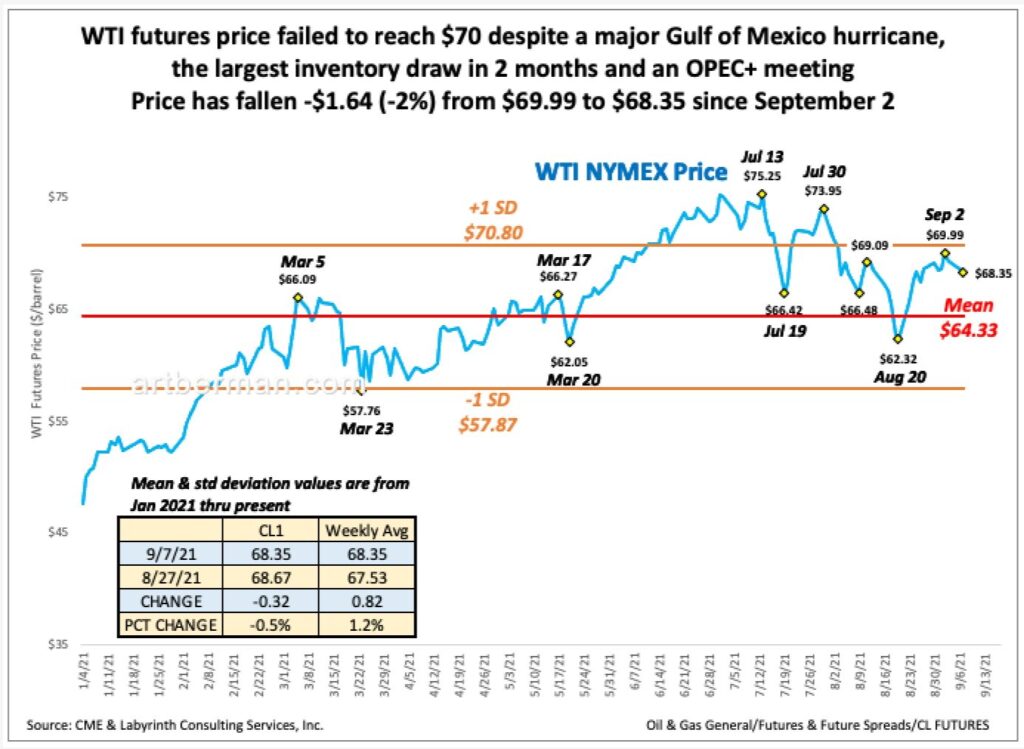

WTI futures price fell 12% from $75.25 to $66.42 between July 13 to July 19 (Figure 1). It rallied back to almost $74 before falling 10% to $66 ten days later. After a weak rally to $69, price fell 10% again to $62 by August 20. This pattern of lower highs and lower lows is rarely ends wells for those who benefit from higher oil prices.

WTI price improved to almost $70 by September 2 but has decreased to $68.35. This was the best the market could do despite a major Gulf of Mexico hurricane, the largest inventory draw in 2 months, an OPEC+ meeting and a failed drone strike on Saudi refineries near the Persian Gulf. Prices have recovered about $1 as I write on September 8 but remain below the September 2 level.

Saudi Arabia cut oil prices for Asian cargoes just days after OPEC+ moved forward with its second monthly 400 kb/d increase earlier this week. The Kingdom and OPEC+ are in a difficult spot. They must simultaneously express confidence that their stratagem of tapering back production is paying off while publishing data showing a looming supply surplus.

Supply-Demand Forecasts

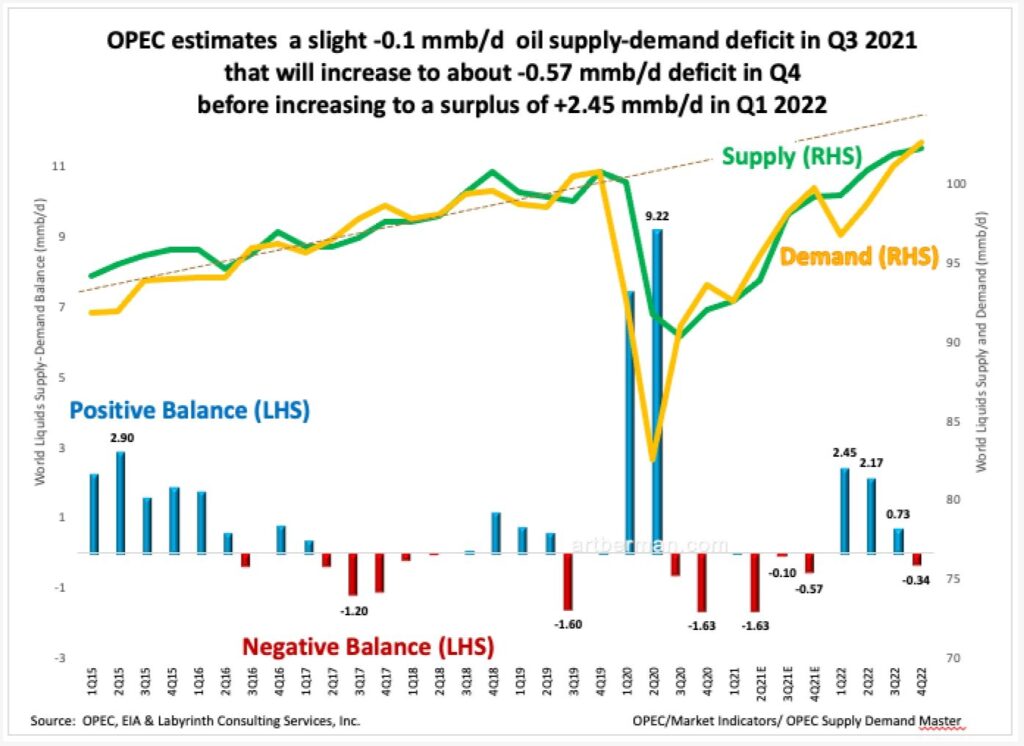

Figure 2 shows OPEC’s latest supply and demand forecast. It suggests a very slight -0.1 mmb/d oil supply-demand deficit in Q3 2021 that will increase to about -0.57 mmb/d deficit in Q4 before increasing to a surplus of +2.45 mmb/d in Q1 2022. Excluding the Covid collapse in the first half of 2020, that’s the biggest supply-demand surplus since the second quarter of 2015, following the largest price collapse before Covid in modern history.

OPEC does not expect world demand to return to 2019 levels of around 202.5 mmb/d until the end of 2022. Even that will fall about 2 mmb/d short of the demand growth projection shown by the dashed brown line in Figure 2.

These price fluctuations are widely attributed to demand concerns because of the resurgent Covid-19 delta variant. Most analysts believe that these are temporary setbacks and probably represent market over-reactions. I disagree and believe these closely spaced price adjustments reflect more fundamental concerns about the state of the global economy and its effect on oil-demand recovery.

IEA’s recent Oil Market Report downgraded demand for the second half of 2021 and added that non-OPEC supply will be higher than expected. As Julian Lee recently commented, “Unless oil demand turns out much stronger, or production outside the OPEC+ group much weaker than OPEC’s analysts predict, the time will soon come when the members will again have to contemplate cutting, rather than raising, output.”

Comparative Inventory

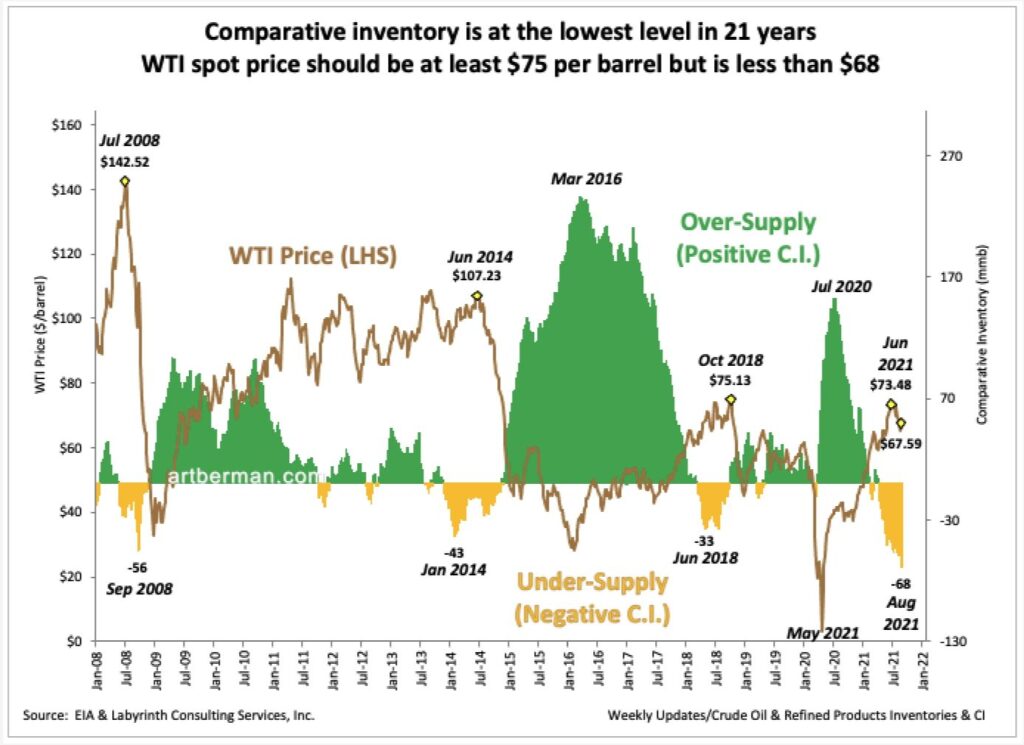

Figure 3 shows WTI comparative inventory (C.I.) versus WTI spot price from 2008 to the present. C.I. is at the lowest level in 21 years (March 2000, not shown in the figure). Yet price has fallen from the June 25 high price of $73.48 when C.I. was +20 mmb closer to the 5-year average than it is today.

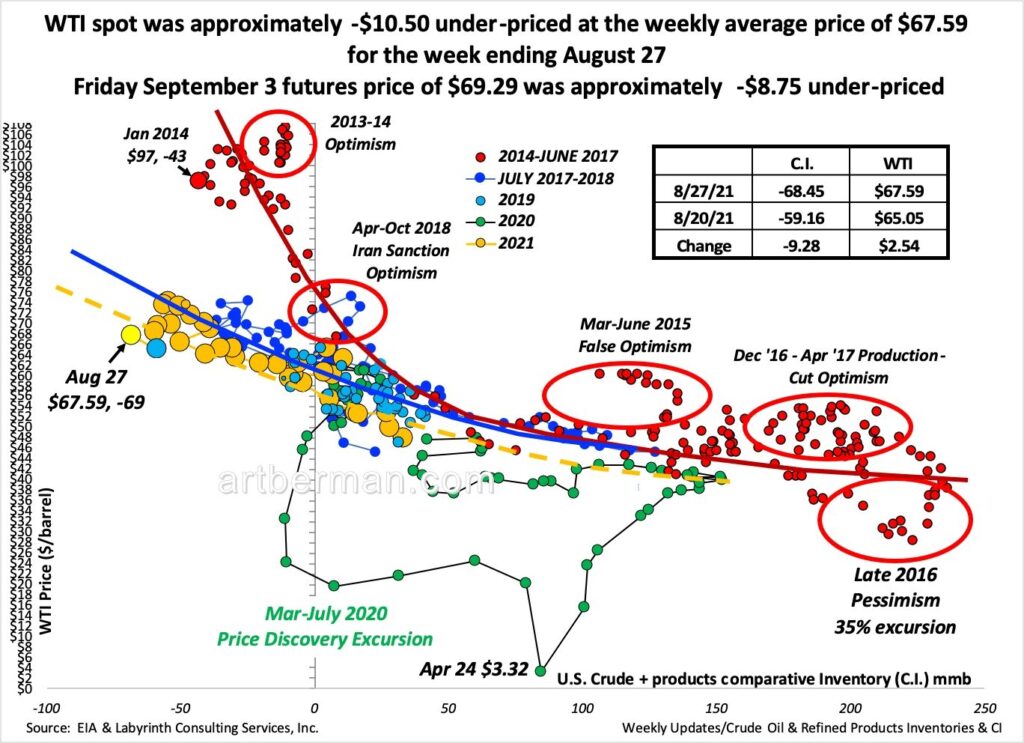

Figure 4 is the same comparative inventory vs WTI price data shown as a cross plot. The blue yield curve describes the volume-price relationship from 2017 through 2019. The green circles represent the market response in 2020 to the economic disruption and demand destruction of the Covid-19 pandemic. The gold circles represent 2021 with the latest data in yellow and last week’s data in light blue. Those data points fell on the gold, dashed line through May of 2021 and then moved back to the blue yield curve in June and early July.

The last six gold data point plotted well below the blue yield curve and indicates that WTI is approximately -$10.50 under-priced at the weekly average price of $67.59 for the week ending August 27. The closing futures price on September 3 of $69.29 was about -$8.75 under-priced.

This suggests that one of at least two things is happening: either WTI is discounted about 10% from the price that the blue yield curve indicates it should be or it is slightly under-priced based on the dashed, gold yield curve. Either way, prices are unlikely to move strongly higher unless markets change their mind about the price they are willing to pay for oil. Markets are just not feeling much supply urgency.

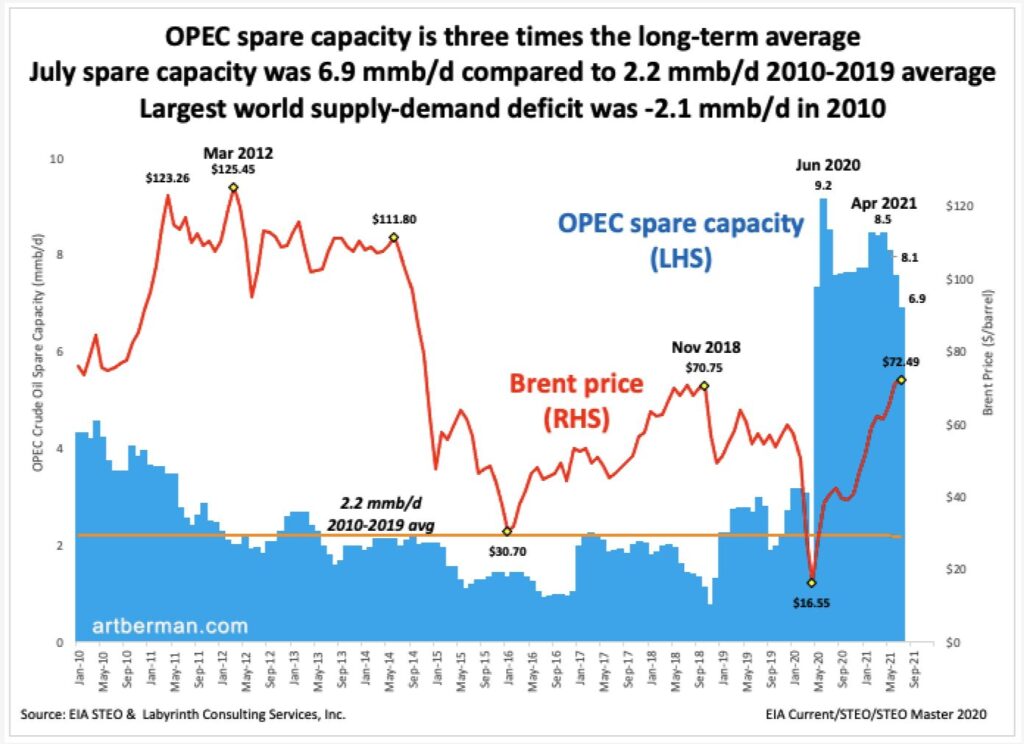

OPEC Spare Capacity

Part of the explanation for low supply urgency is that the world has been on OPEC+ life support since April 2020 when approximately 10 mmb/d were withheld from global markets. July spare capacity was 6.9 mmb/d (Figure 5). The 2010 through 2019 average was 2.2 mmb/d. The difference is twice the largest supply demand deficit of this century which was -2.1 mmb/d in the third and fourth quarters of 2010.

U.S. Output and Supply Urgency

More than 70% of the increase in world production from 2011 to the peak in 2018 was from the United States. The collapse of oil prices and drilling after April 2020 led to concerns that reduced U.S. output would lead to a global supply crisis.

U.S. production fell from almost 13 to less than 10 mmb/d initially but quickly recovered to 11 mmb/d. The U.S. produced 11.3 mmb/d in July 2021 and EIA expects levels to increase slowly to more than 12 mmb/d by December 2022.

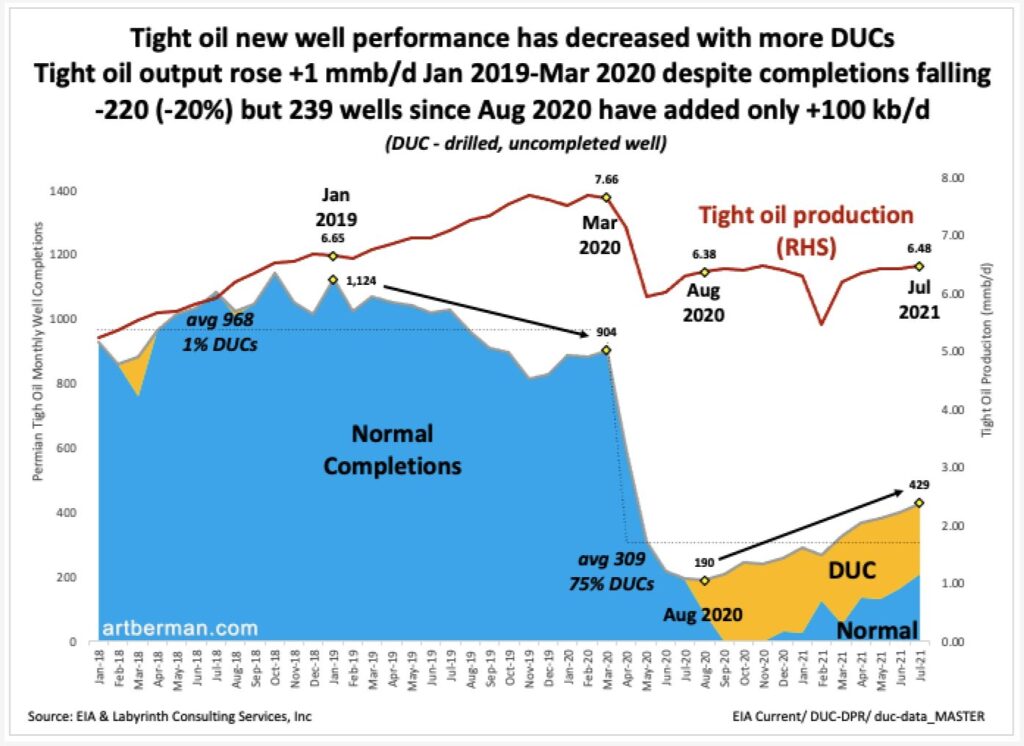

The explanation is that tight oil producers have greatly improved drilling and completion efficiency. Figure 6 shows U.S. tight oil production and the number of well completions. From January 2019 to March 2020, output increased +1 mmb/d (+15%) but well completions decreased from 1,124 to 904 (-20%). This had nothing to do with DUCs (drilled uncompleted wells) which made up less than 1% of completions at that time. It was because of much better well performance which may have resulted from longer laterals, more effective fracks or simply better well locations.

Whatever it was, it didn’t last because producers could no longer afford to drill as many wells—their source of outside capital had contracted. Operators were forced to rely increasingly on DUCs to maintain production–75% of all completions after August 2020 have been DUCs. These wells have not performed as well as those completed before March 2020. The number of tight oil completed wells increased from 190 to 429 (+126%) by July 2021 but production stayed flat.

Figure 6. Tight oil new well performance has decreased with more DUCs. Tight oil output rose +1 mmb/d Jan 2019-Mar 2020 despite completions falling -220 (-20%) but 239 wells since Aug 2020 have added only +100 kb/d. Source: EIA & Labyrinth Consulting Services, Inc.

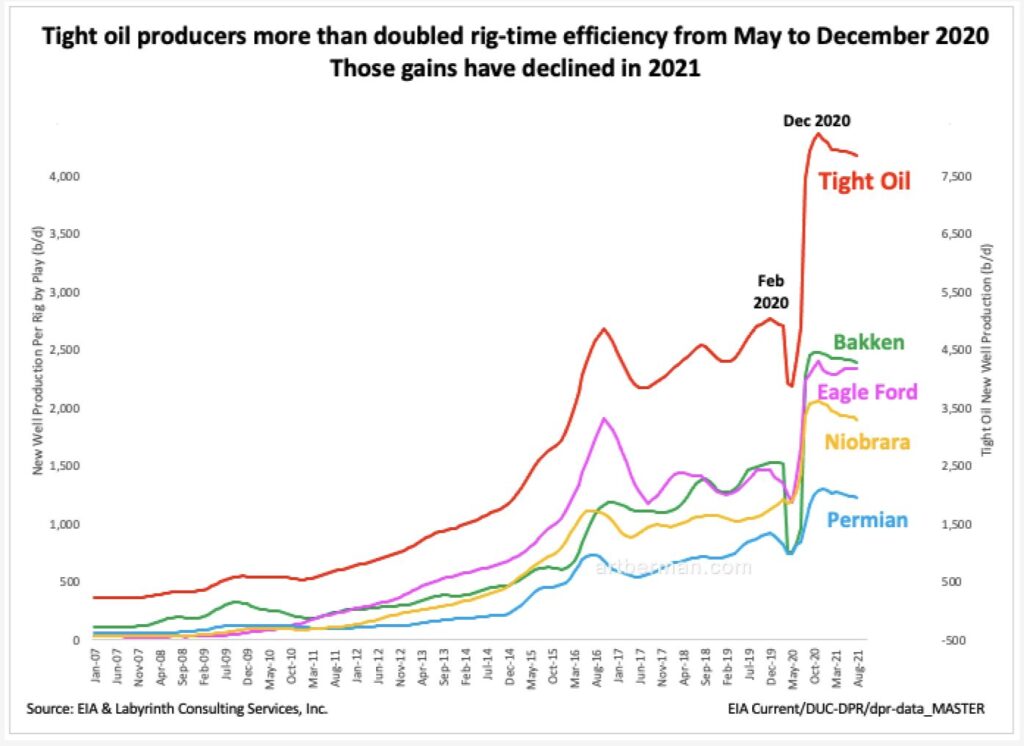

With less capital available to drill, companies have learned how to use rigs more efficiently. Tight oil producers more than doubled rig-time efficiency from May to December 2020 (Figure 7). Those gains have declined somewhat in 2021.

The Demand Recovery has Stalled

Data does not support widespread claims that oil demand has recovered and will soon exceed all previous levels.

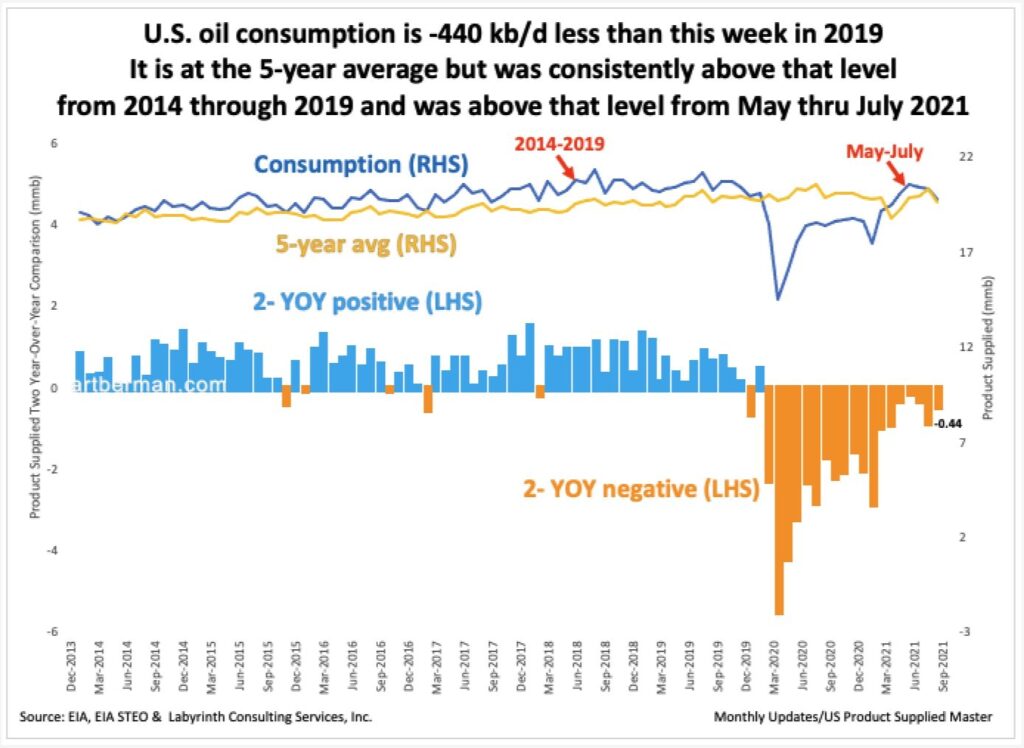

U.S. oil consumption is -440 kb/d less than this week in 2019 (Figure 8). It is at the 5-year average but was higher from May through July and has since moved lower. Even at May through July higher levels, it was lower than for the same periods in 2019. Moreover, consumption was consistently more than the 5-year average from most of 2014 through 2019. That is how growth is defined. Just reaching the 5-year average is not the same as reaching previous high levels.

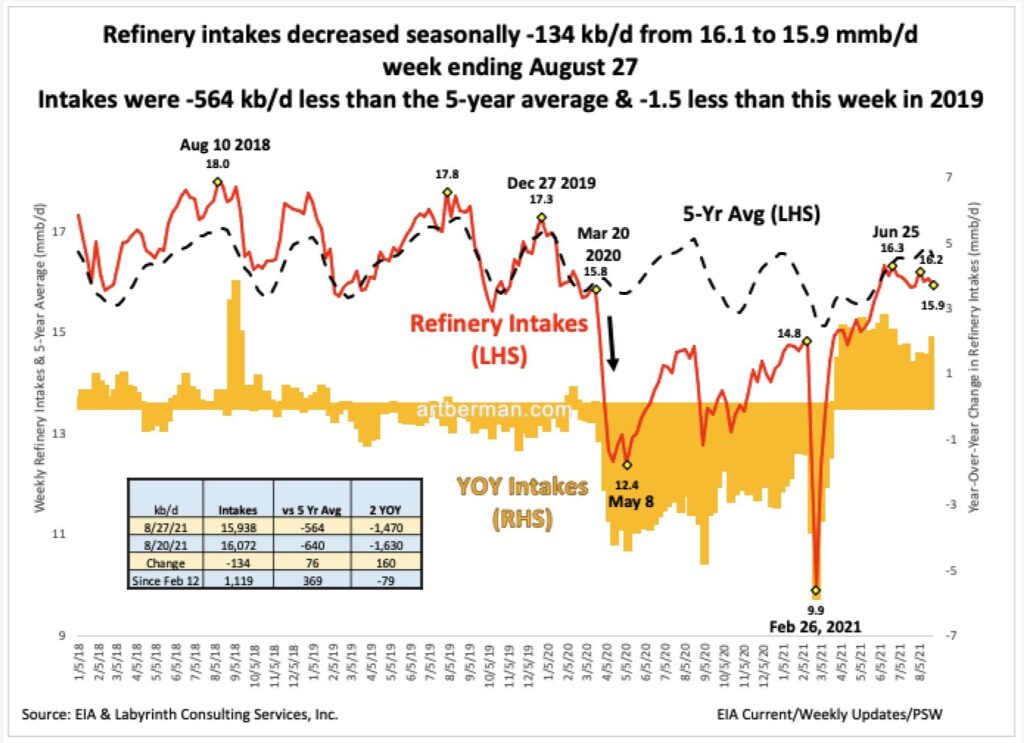

Consumption is difficult to measure and is inferred from refined products leaving refinery storage tanks. Refinery crude oil intakes is a more precise measure of oil demand. Refinery intakes were -564 kb/d less than the 5-year average & -1.5 less than this week in 2019 for the week ending August 27—the latest data from EIA (Figure 9). The data from both consumption and refinery intakes indicates that recovery still has some way to go.

Demand may well recover some time in 2022 as indicated by forecasts shown above in Figures 2 but for now, it is stalled.

Markets are Shorting Oil

Paradigms change but people keep expecting a return to something that used to be or never was. Those expecting a return to pre-Covid oil price levels have forgotten that those were a shadow of pre-2014 levels.

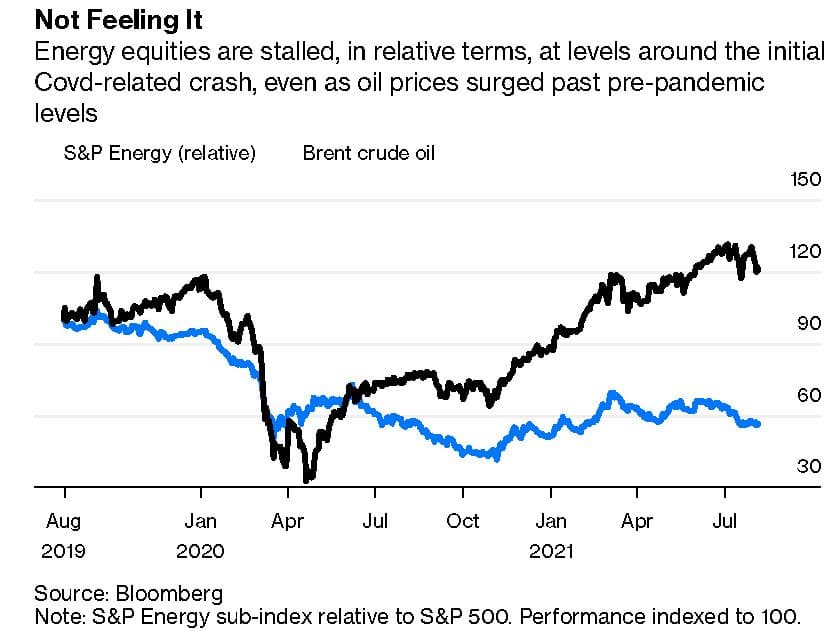

Even as oil companies rush to endorse balance sheet and drilling restraint, shareholder returns and a greener image, investors aren’t buying it. Figure 10 from a recent post by Liam Denning shows that energy share prices have not responded to higher oil prices as they have during past price rallies.

The debate about climate change continues but it seems that investors have voted with their feet. They’re not investing in oil companies.

More than $120 billion has been raised so far in 2021 for low-carbon alternatives to traditional oil and gas investments through Special Purpose Acquisition Companies (SPACs) . Only three E&P SPACs have been filed over the same period.

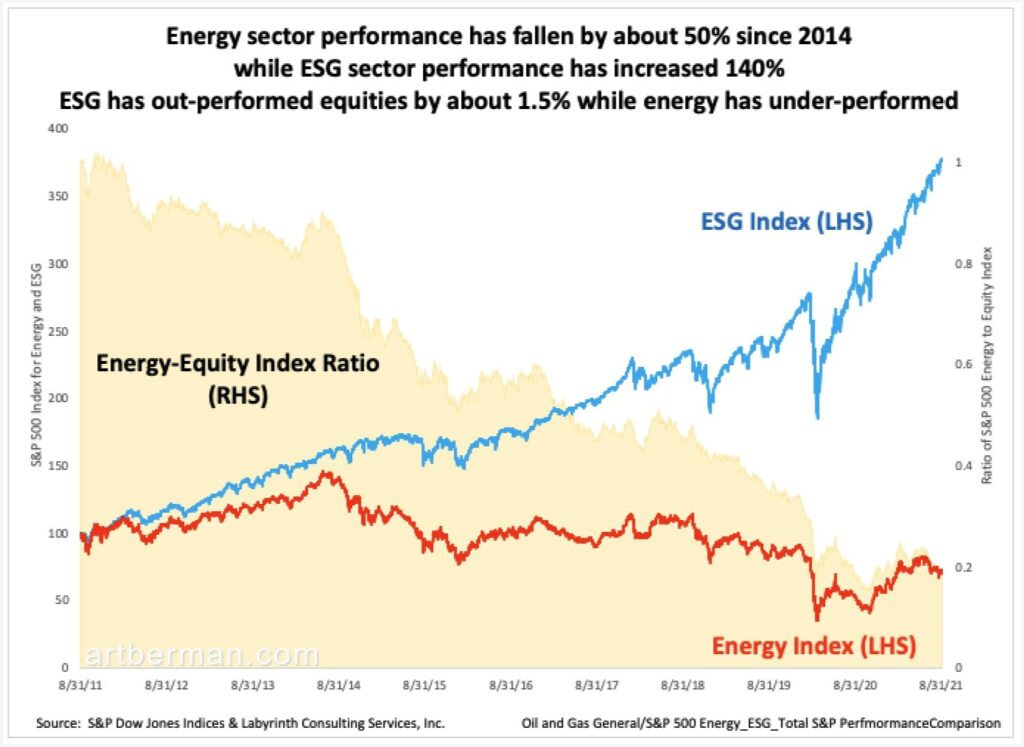

S&P 500 energy sector performance has fallen by about 50% since 2014 while ESG (environmental, social and governance) sector performance has increased 140% (Figure 11). ESG has out-performed S&P 500 equities by about 1.5% while energy has substantially under-performed.

Oil Prices Going Forward

It is difficult to understand the bull case for oil price in light of data presented in this newsletter.

The Dallas Fed’s survey of 150 oil and gas company executives indicated an average WTI price of $69.71 by year-end and EIA’s December forecast is $67 per barrel.

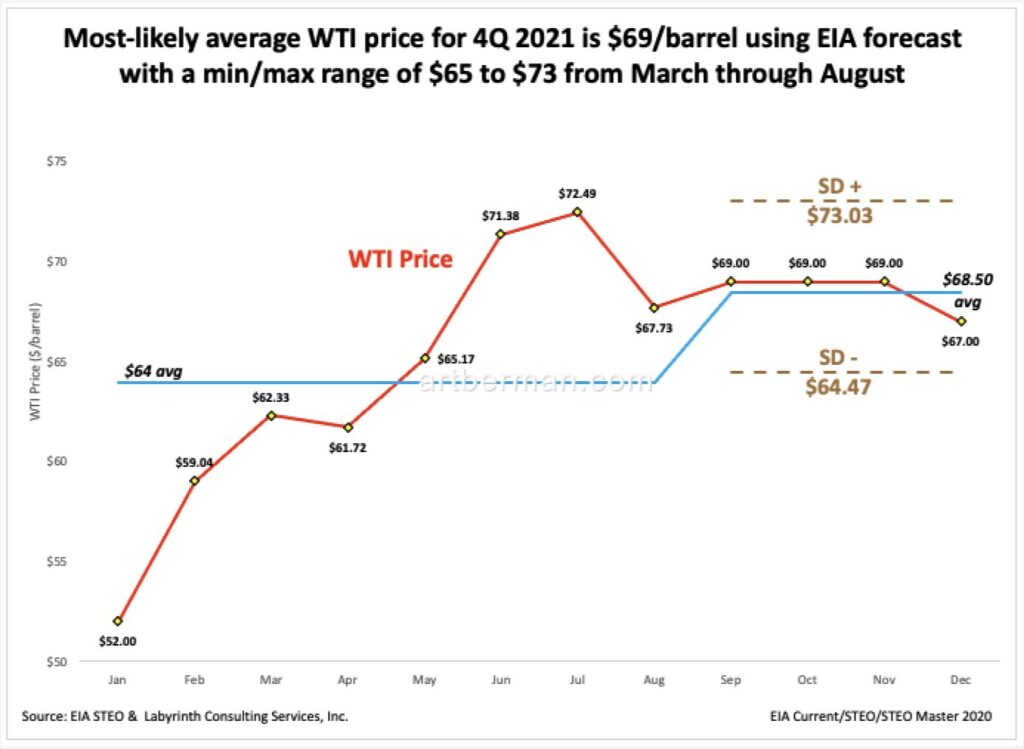

Using EIA’s forecast, I calculated a standard deviation of about $4.50 for actual monthly WTI prices from March through August. Using the $68.50 mean of forecast prices for September through December, the probable range for the fourth quarter is $65 to $73 per barrel (Figure 12). The most-likely fourth quarter average price should be about $69 per barrel, very close to the September through December mean.

The effects of the worst economic recession since the 1930s have not magically disappeared despite what some analysts say. The U.S. and advanced economies have been propped up by exceptional central bank liquidity. This cannot hide or heal the massive economic dislocations of the last 18 months. Economic activity has not recovered and oil demand has not recovered.

Among the unanticipated outcomes of the pandemic has been its affect on how people see the future of energy. Concerns about fossil energy and climate change began decades ago but seem to have come into a new focus in 2020 and 2022. Investors started losing trust in tight oil companies in mid-2018 but now they have moved on to different investments and asset classes.

There was great uncertainty about oil supply in 2020. That along with historically low oil prices contributed to a spectacular price rally. By July, much of that uncertainty had dissipated and it now seems that fears of an oil and gas supply crisis were exaggerated. The idea of a new commodity super-cycle seem more part of a past paradigm than of the emerging future.

Most investors know that oil is critical to the economy but they see it as a twilight industry. They understandably want to invest in the future. I suspect that they will return to traditional energy investments as some of the shine of the energy transition fades in the hard light of day.

Falling inventories are an artifact of OPEC+ export cuts and not a sign of under-supply. The present reality is that the world appears well supplied for 2022. Prices rarely increase when supply seems adequate. Markets are smarter than that.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts