Art Berman Newsletter: July 2020 (2020-6)

Highlights

- Oil prices are stalled in the low $40s for WTi and mid-$40s for Brent.

- Producer behavior indicates that prices are too high.

- The oil demand recovery is uneven and weak.

- Oil prices will probably fall in coming weeks or months until producer behavior changes..

- Oil markets will recover but not as soon as we would like.

Producer Behavior Suggests That Prices are Too High

A massive explosion rocked Beirut’s harbor and downtown area yesterday morning. There was a time when something like this would have caused oil prices to increase by $5/barrel or more. That changed after 2014 when over-supply began to dominate oil markets. A year ago, an attack on Saudi Arabia’s main oil refinery only moved prices higher for a few days.

Yesterday’s explosion did not move oil prices outside of ordinary recent trading ranges. The EIA oil storage report this morning did but that too will fade as the day and week passes. Despite a healthy crude oil withdrawal, comparative inventory only fell 2 mmb.

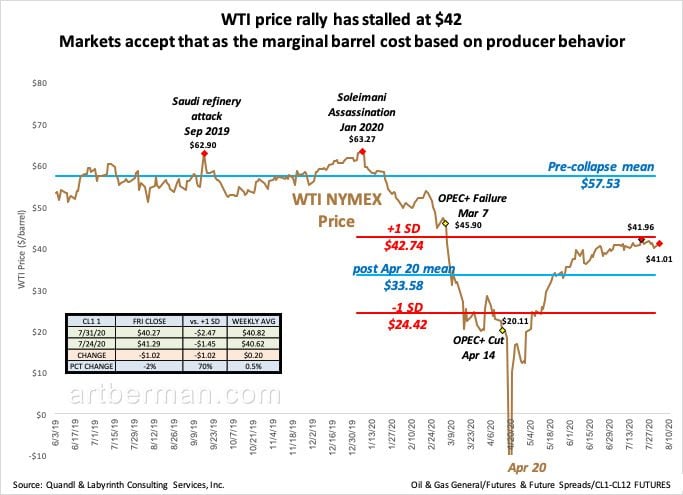

The price rally that began in late April has lost momentum in the low-$40s for WTI and the mid-$40s for Brent (Figure 1). There are many news cycle causes cited by analysts and journalists but it’s not really that complicated—the world is well supplied with oil and producer behavior signals that there is more supply coming.

Markets accept that as the marginal barrel cost based on producer behavior.

Source: Quandl and Labyrinth Consulting Services, Inc.

In mid-July, OPEC+ agreed to scale back production cuts by 2 mmb/d despite a prodigious supply-demand surplus. Russian Energy Minister Alexander Novak has stated his belief that there may be a 3 to 5 mmb/d supply this summer. Don’t believe it.

Analysts continue making silly proclamations about tight physical markets. They’ve been doing this since at least mid-2018 despite two major price collapses since those declarations began.

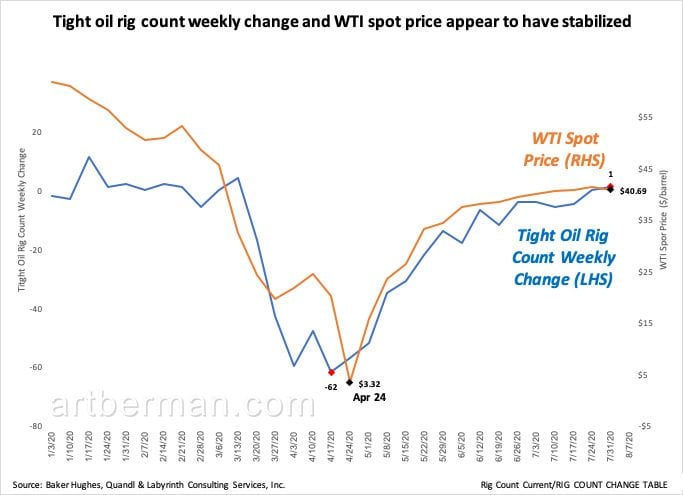

In addition, U.S. rig counts have probably reached a minimum. The tight oil rig count increased for the first time last week since mid-May (Figure 2). For some that’s a signal that the worst of the oil industry’s problems are over. The message it sends to markets is that price needs to go down to prevent more drilling.

Source: Quandl and Labyrinth Consulting Services, Inc.

Comparative Inventory

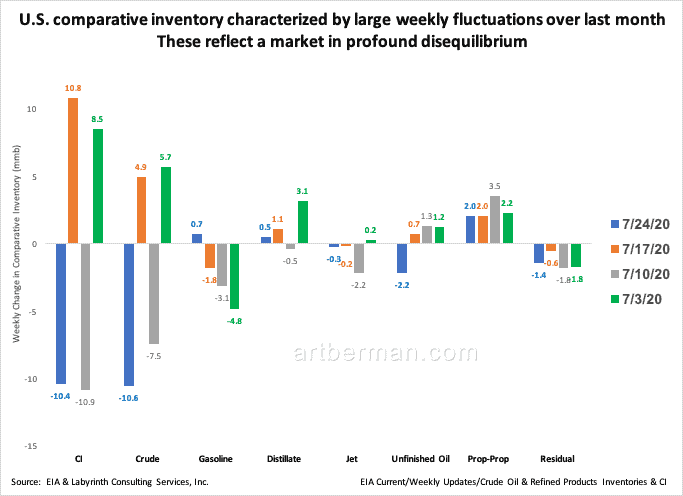

U.S. comparative inventory (C.I.) has finally begun to decrease in recent weeks but progress is slow and uneven. C.I. has been characterized by large weekly fluctuations over last month (Figure 3). These reflect a market in profound disequilibrium.

C.I. fell -10.4 mmb the week ending July 24, gained +10.8 mmb the week before, lost -10.9 the week ending July 10, and rose +8.5 mmb the week previous for a net loss 0f -2 mmb for the last month.

These reflect a market in profound disequilibrium.

Source: Quandl and Labyrinth Consulting Services, Inc.

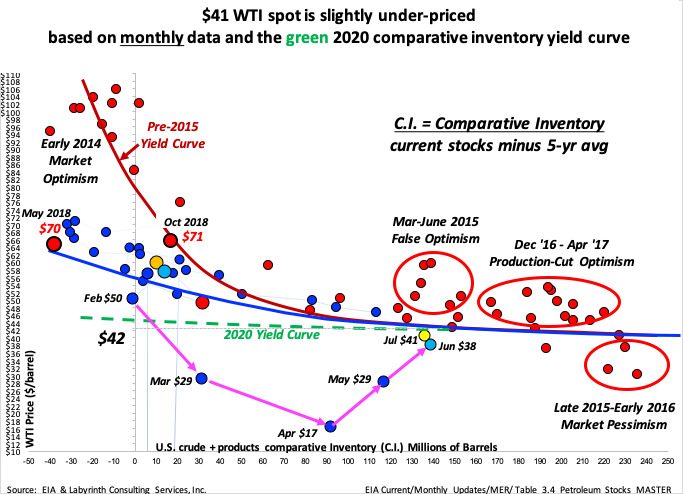

Comparative inventory vs WTI price data continues to behave exactly as I predicted in March. Data points are converging on the current green C.I. yield curve and ~$40 – 45/barrel prices (Figure 4). The WTI spot average of $41 for July is slightly under-priced based on the yield curve.

The trajectory of prices since February (shown by the pink arrows) reflects a 4-month price discovery process that is finally stabilizing in the low $40 range. The flat slope of all three yield curves shown in Figure 4 means that price is unlikely to increase much until C.I. is reduced by about 50% of its present level of almost 140 mmb more than the five-year average.

Attention is always focused on crude oil stocks but the truth is that no one consumes crude oil except refineries. Refined products are the market place so clearly, lower supply and greater demand are what will drive down inventories.

based on monthly data and the green 2020 comparative inventory yield curve.

Source: Quandl and Labyrinth Consulting Services, Inc.

Oil-Demand Recovery is Weak and Uneven

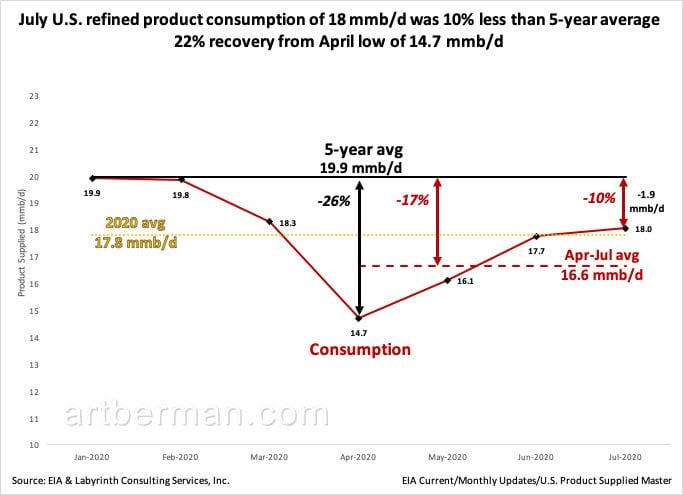

From a distance, the U.S. oil-demand recovery looks good. July U.S. refined product consumption of 18 mmb/d was only 10% less than the 5-year average (Figure 5). That suggests that real progress has been made and we’ll soon be back to normal levels of consumption.

22% recovery from April low of 14.7 mmb/d.

Source: Quandl and Labyrinth Consulting Services, Inc.

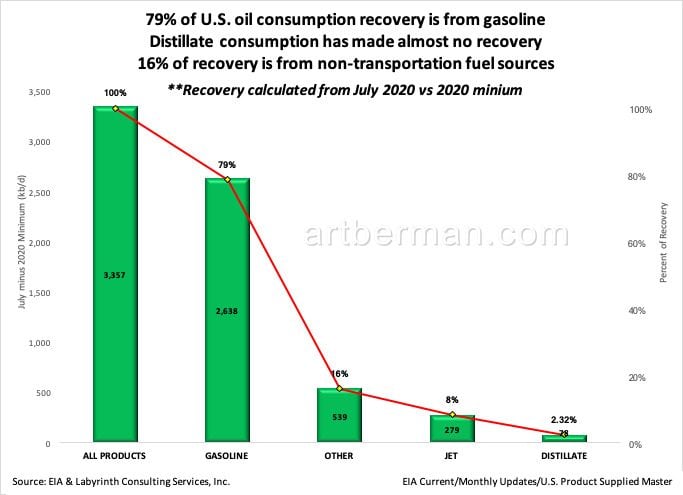

The details, however, reveal that most (79%) of the recovery is gasoline (Figure 6). That makes a certain amount of sense since gasoline is the principal product refined from each barrel of crude. Gasoline’s portion of the refined barrel, however, averaged 46% in 2019 and not 79%.

Distillate consumption has made almost no recovery.

16% of recovery is from non-transportation fuel sources.

Source: Quandl and Labyrinth Consulting Services, Inc.

Distillate or diesel is the second largest fraction of every barrel at about 20% but distillate consumption has made almost no recovery from its 2020 minimum.

The second largest component of the demand recovery is “other” which includes natural gas liquids, propane and propylene, unfinished oils and residual fuel oil. These products are not particularly meaningful measures of recovery. None are transportation fuels and some are not really even oil but rather, a by-product of the refining process.

Gasoline does not add much to economic activity other than driving to work. It’s a big piece of the background but not really in the foreground of what drives economic growth.

That is what diesel provides and it has gone nowhere. Diesel consumption is about 12% less than normal and that’s about what I expect economic contraction to be for 2020.

What to Expect

July was an important month for world oil markets. Inventories have finally started to decline. That is because OPEC+ has withheld almost 1 billion barrels from global supply, and demand has begun its long path to recovery.

There is nothing magic or surprising about that. But people have selective memories and believe that things are going to return to the way they were at the beginning of the year. That is just wrong.

The coronavirus epidemic continues to be a drag on the economy and oil demand. The president made some comments last week indicating that perhaps he was taking the problem seriously. He has since sponsored several meetings where no one wore a mask, endorsed a doctor who believes that aliens have sex with earthlings, and has criticized his top medical advisors. Without national leadership, this virus is going to permanently degrade the economic strength of the United States and drag much of the world along with it toward economic collapse.

That is the theme music playing behind the daily news cycle of events that analysts present to suggest that everything in oil markets is fine.

While people fret about demand, markets are focused on supply. Supply is the lever that causes producers to add or subtract drilling rigs. OPEC+ is increasing exports and the U.S. rig count has stopped falling. That means more supply and markets will respond with lower prices until producers get the message.

Oil markets will recover but not soon. Nothing in nature moves in a straight line. The recovery will be weak and uneven. That is how is recoveries are—bright spots that encourage us against a backdrop that reminds us of how far we have to go.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts