Stop Expecting Oil and the Economy to Recover

Global oil markets are on the cusp of something.

Nafeez Ahmed says that the oil age is coming to an end.

“The oil industry is on the cusp of a process of almost total decimation that will begin over the next 30 years, and continue through to the next century.”

Nafeez Ahmed, Director Institute for Policy Research & Development

Goehring and Rozencwajg say there’s not nearly enough oil to meet demand and that a global energy crisis is imminent.

“We are on the cusp of a global energy crisis…Global energy markets in general and oil markets in particular are slipping into a structural deficit as we speak. We believe that energy will be the most important investment theme of the next several years and the biggest unintended consequence of the coronavirus.”

Goehring and Rozencwajg

They are both partly right but miss the larger point namely, that it is unlikely that either oil supply or demand will ever return to 2018 levels on a sustained basis.

World Oil Growth is Dependent on U.S. Tight Oil

U.S. oil production fell -2.72 mmb/d (-21%) from 12.7 to 10 mmb/d from March to May as oil prices collapsed (Figure 1). It recovered to 11.36 mmb/d in June as shut-in wells were re-activated. EIA expects output to average 11.2 mmb/d in the second half of 2020 and 11.1 mmb/d in 2021.

That is impossible.

It recovered to 11.36 mmb/d in June as shut-in wells were re-activated.

Output expected to average 11.2 mmb/d in 2H 2020 and 11.1 mmb/d in 2021.

Source: EIA 914 and Labyrinth Consulting Services, Inc.

During the last oil-price collapse in 2015 and 2016, U.S. output decreased 1.12 mmb/d over a period of eighteen months. This time, a much larger decline has taken place over a period of just a few months.

Goehring and Rozencwajg are correct that tight oil is crucial to world supply growth and that the best parts of those plays are fully or nearly full developed.

U.S. tight oil accounted for 83% of growth in world production over the decade 2009 to 2019 (Figure 2). Deep water and oil sands were the other growth area at 23% while conventional production declined 9% over the same period.

World crude and condensate production fell an astonishing 10.8 mmb/d from 82.5 to 71.7 mmb/d from April to June of this year. About 30% of that decline was from U.S. output and a little more than half of the U.S. decline was from tight oil.

It recovered to 11 mmb/d in June as shut-in wells were re-activated.

Output expected to be flat through 2021 from 10.5 to 11 mmb/d.

Source: EIA 914 and Labyrinth Consulting Services, Inc.

Tight Oil Rig Count and Oil Production

Rig count is a good way to predict future oil production as long as the proper leads and lags are incorporated.

It takes a month or two between increased oil price and a signed rig contract. It takes another 5 or 6 months to drill and complete all the wells on a drilling pad. It then takes another 5 or 6 months from first production before new wells offset declining output from older wells. Add it all together and it takes at least a year between an upward price signal and enough new production to maintain or increase output.

Twelve-month lagged tight oil horizontal production reached 7.28 mmb/d when the rig count was 613 (Figure 3). That corresponded to 12.9 mmb/d of U.S. oil production (tight oil is about 53% of total U.S. output). The EIA forecasts about 11 mmb/d of output through 2021. Approximately 450 rigs are needed to maintain that level but the July tight oil rig count was 147, about one-third of the number needed to maintain 11 mmb/d.

Tight oil rig count is 147, 32% of 450 rigs needed to maintain

5.5 mmb/d tight oil/11 mmb/d total U.S. output.

Source: EIA, Baker Hughes and Labyrinth Consulting Services, Inc.

It is, therefore, inevitable that production will fall. The considerable lags and leads mean that production decline cannot be expected to reverse until well into 2021 assuming that large numbers of rigs are added immediately. That won’t happen because of constrained budgets and low oil prices. Based on rig count analysis, U.S. oil production will probably be about 6 mmb/d by mid-2021 or less than half of peak November 2019 levels.

This is why EIA’s production forecast is impossible. It does not acknowledge that production cannot be maintained without drilling new wells to offset legacy well declines.

What about DUCs (drilled, uncompleted wells)? The DUCs drilled before 2015 will never be completed because they were questionably commercial at $100/barrel oil prices. Many remaining DUCs are part of the 12-month delay from well spud-to-production. Nor is completing DUCs free. Completion accounts for roughly half of total well cost.

Supply and Demand: Two Parts of a Single Whole

Goehring and Rozencwajg believe that we are on the cusp of a global energy crisis because of the depletion of U.S. tight oil plays. They are right but are not paying enough attention to demand. Ahmed believes the oil industry is dying a slow death because of decreasing demand. He is right about lower demand but is not paying enough attention to supply.

Supply and demand are two parts of a single whole.

World liquids supply has fallen 9.5 mmb/d in the first half of 2020. Demand has fallen almost 19 mmb/d for a supply-demand surplus of almost 9.5 mmb/d (Figure 4). That is precisely why oil prices remain range-bound in the $40 range. A big drop in supply only results in an energy crisis if demand recovers to 2019 levels.

but a supply-demand surplus for the last 3 quarters of 2021.

-9.1 mmb/d demand growth and -6.1 mmb/d supply growth in 2020.

Source: OPEC, EIA and Labyrinth Consulting Services, Inc.

The integrated OPEC-EIA data shown in Figure 4 indicates a V-shaped demand recovery in the third quarter of 2020 with a lagging recovery in supply. I don’t believe that either forecast is likely but let’s put that aside for now so we can understand the best-case outcome.

A huge supply surplus in the first half of the year is expected to give way to a smaller yet significant supply deficit in the second half. A 2.25 to 2.50 mmb/d supply deficit in the second half of the year is not an energy crisis but it does suggest higher oil prices are ahead.

The OPEC-EIA model suggests approximate market balance in early 2021 followed by a substantial surplus during the rest of the year. That is hardly a death knell for the oil industry but it does suggest lower oil prices are ahead.

Where is the crisis for either supply or demand?

To be fair, I’m sure that Goehring and Rozencwajg, and Ahmed would say that they are thinking farther into the future. Their models assume some version of business-as-usual but I don’t think there is anything usual about the either the present or the future. The world has changed but paradigms change slowly.

Stop Expecting Oil to Recover

Many believe that oil markets are recovering and will return to normal sooner than later. I’m not sure that normal applies to oil markets but let’s look at the facts.

August average WTI price of $42.88 is less than the 2003 average inflation-adjusted price of $43.54 and, of course, every one of the sixteen succeeding years (Figure 5). That is hardly an impressive recovery.

but is lower than average price of each of 16 successive years.

Source: U.S. Bureau of Labor Statistics, EIA and Labyrinth Consulting Services, Inc.

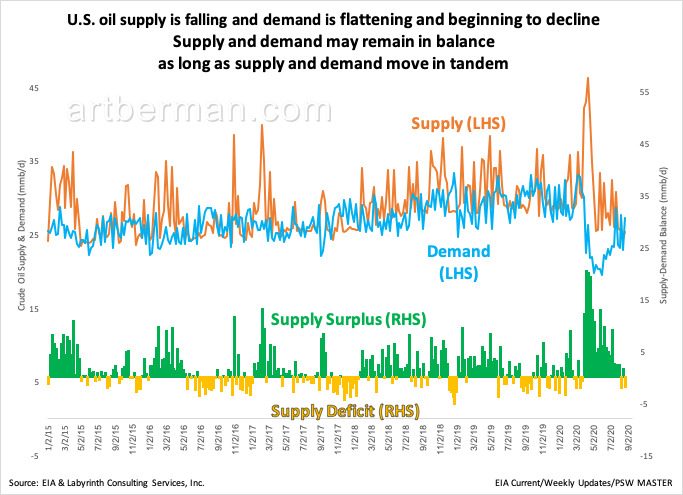

Figure 6 shows U.S. supply, demand and supply-demand balance. Supply has been trending lower since late 2018 except for the early 2020 spike that resulted from shutting in production with collapsing consumption and limited storage.

Although demand has recovered from early May low levels it appears to be turning downward now and is, in any case, far below levels for the last 12 months. Again, not a great recovery.

Supply and demand may remain in balance

as long as supply and demand move in tandem.

Source: OPEC, EIA and Labyrinth Consulting Services, Inc.

U.S. refined product consumption has recovered only to 62% of its 5-year average (Figure 7). Gasoline has recovered to 81% of 5-year average and diesel to 84% of 5-year average. Kerosene Jet has only recovered to 34% of 5-year average.

Gasoline has recovered to 81% of 5-year average and diesel to 84% of 5-year average.

Kerosene Jet has only recovered to 34% of 5-year average.

Source: OPEC, EIA and Labyrinth Consulting Services, Inc.

The recovery is not going all that well but history tells us that is what we should expect. It took 4 1/2 years after the 2008 Financial Collapse for U.S. refined product use to recover (Figure 8). The magnitude of the 2020 consumption collapse is far greater than in 2008 so why should this recovery be any faster?

It took 4.5 years after 2008 Financial Collapse for U.S. refined product use to recover.

The magnitude of the 2020 consumption collapse is far greater than in 2008.

Source: OPEC, EIA and Labyrinth Consulting Services, Inc.

In fact, the only thing that justifies calling what is happening today a recovery is the presumption that things can’t get any worse than they were in April. That presumption is probably wrong.

The Great Simplification

Energy is the economy. Money is a call on energy. Debt is a lien on future energy.

What is happening to oil markets and to the global economy is not because of a virus. The virus greatly accelerated what was already happening. Things won’t go back to normal when the virus ends.

The expansion of energy and debt have been leading toward some sort of reckoning for at least the last fifty years. That day of reckoning has been brought forward by coronavirus economic closures.

Oil prices had averaged $25 per barrel from the end of World War II until 1974 when average prices doubled (Figure 9). From 1979 through 1986, oil price soared to an average of $86 per barrel. These massive economic dislocations resulted in use of debt to maintain economic growth.

Source: EIA, Bureau of Labor Statistics and Labyrinth Consulting Services, Inc.

Excessive debt was the leading cause for the Financial Collapse of 2008. The crisis was resolved with more debt and monetary policies that ushered in the present era of central bank primacy in the world financial system.

Quantitative easing, near-zero interest rates and high oil prices led to the first wave of the tight oil boom. Over-investment resulted in over-supply and price collapse in 2014. By February 2016, WTI price reached $33 and investors rushed in to support the second wave of the tight oil boom.

WTI reached $72 by mid-2018 but by then, investors had begun to abandon tight oil as well as oil companies in general. The coronavirus economic closure brought monthly average prices to $17 in April, 2020—the lowest month on record. Unlike early 2016, investors weren’t writing any checks this time.

U.S. production may be 50% lower by mid-2021 than at year-end 2019. The implications for U.S. geopolitical power and balance of payments are staggering. It seems likely that the economy will weaken as government support for the unemployed decreases

I doubt that we are on the cusp of either a global energy crisis or the end of the oil age. It is more likely that both supply and demand will fall in tandem as the global economy contracts.

These observations are at odds with the mainstream view that both supply and demand are recovering. Some might concede that I am correct for the present but that things will improve and return to normal although it may some time.

Figure 10 shows credit growth and credit impulse for the United States from 1960 through the first quarter of 2020. Credit impulse is the change in flow of credit (debt) relative to economic activity (GDP).

Spikes in credit impulse correlate well with the oil-price shocks of the 1970s and 1980s. The extraordinary U.S. comparative inventory drawdown of early 2017 through the second quarter of 2018 also corresponds to credit impulse anomalies.

First quarter credit growth was greatest since 1984.

Source: EIA, Bureau of Labor Statistics and Labyrinth Consulting Services, Inc.

The chief feature of Figure 10, however, is that the magnitude of the first quarter 2020 credit impulse was more than twice as large as any previous increase. Moreover, GDP growth was either neutral or positive during previous spikes but was negative (-10%) for the first quarter of 2020. Also, oil prices were increasing during earlier periods but prices were decreasing in early 2020.

Ilya Prigogine was a chemist who won the 1977 Nobel Prize for his work on dissipative structures and self-organization. Dissipative structures are physical systems that release considerable heat as they consume ever-greater energy to support their growth and increasing complexity. A crisis occurs when growth can no longer be supported by available energy resources. The system either collapses or spontaneously re-organizes itself into a simpler form that uses less energy.

Empires, organizations and economies are dissipative structures. So is the human brain.

My friend Nate Hagens has applied some of Prigogine’s ideas to his own research about world energy, economics and ecology. He believes that we are on the cusp of something quite different from the scenarios suggested by Ahmed, and Goehring and Rozencwajg.

Hagens predicted a global economic decline in the 2020s and publicly expressed that opinion before the Covid pandemic. The main reason for decline, he stated, was too much debt undertaken to continue consuming and growing the economy. The virus has accelerated its timing and may result in contraction greater than the 30% drop during the Great Depression.

The Great Simplification will occur when the credit-supported part of the economy is removed. Economic activity will contract and less energy will be needed because it will be increasingly unaffordable to many parts of the population. People will be forced to adjust living standards downward and self-organize around energy with greater emphasis on local supply chains and regional economies.

I expect that the mix of energy sources will be similar initially. That will probably change as declines to meet the decreased carrying capacity of a society deprived of fossil energy productivity. Then, I imagine the world will move increasingly toward lower productivity energy sources like wind and solar. A viable economy may very well be created based heavily on wind and solar. It will, however, support a much poorer world than we have known for many decades in the world’s advanced economies.

Most ideas and analyses about future trends in energy and the economy fail to recognize that they are the two aspects of the same thing. That is why they are so far off the mark. This basic misalignment is painfully obvious because the energy sector represents only 2.5% of the S&P 500 valuation but underlies probably 95% of U.S. GDP.

That is what Hagens calls energy blindness.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

[…] L’influenza cinese sui mercati petroliferi si intensificherà nei prossimi decenni, in particolar modo se l’industria del fracking americana non riuscisse a ripartire, dopo il duro colpo inferto dal COVID. […]

[…] So, that’s a lot less oil-per-capita, to view it from another angle. Independent oil analyst Art Berman is predicting a more severe production crash by midyear 2021 to roughly half what it was at […]

[…] So, that’s a lot less oil-per-capita, to view it from another angle. Independent oil analyst Art Berman is predicting a more severe production crash by midyear 2021 to roughly half what it was at […]

I don’t respond to Anonymous commenters.

I agree. The current cheapness of solar panels and wind turbines is due to their being made using coal-fired power in China at $0.04/kWh. Under ideal conditions in the desert, solar panels produce power costing $0.15/kWh so you can’t use the power from solar panels to make more solar panels so they are neither renewable or sustainable. It is nuclear energy or the abyss. Nuclear energy though relies upon fossil fuels to do all the digging and shifting and processing, at the moment. There are a lot of things that can’t be electrified – plowing and harvesting for example. When the oil volume starts running down, coal to liquids comes in at around $120/bbl. Either that coal will be used to power electric cars (via power stations) or converted to liquid. Either way, coal consumption will double and the remaining reserve life will be halved. When all the coal runs out, carbon in the economy will have to come from wheat stubble and the like – to make plastics, lubricants and tens of thousands of other things. So the nuclear power at the time will have to be cheap enough to pay for all, pay for its replacement as plants run out and have enough left over to run civilisation. When the oil runs out, what happens to all those island nations that currently run on diesel? Places that are too small to justify a nuclear reactor at economic scale? All the fishing boats with diesel engines? 60 years ago Hubbert talked about civilisation’s margin of safety before the oil ran out. Well 60 years have passed and nothing has been done. Governments around the world are happy to squander money on everything except the one thing that matters – a self-sustaining nuclear technology that will provide the necessary surplus energy. The tight oil boom gave us another ten years but that time was wasted having a party.

David,

It is very good to hear from you!

Everything that you say is true but I don’t see nuclear power as a solution. We can discuss its pluses and minuses but it lost public opinion 35 years ago. Public opinion is often wrong but it’s hard to reverse at least until some catastrophe moves it in a different direction.

The present sentiment against fossil energy presents another magical mystery tour that will be judged harshly once it is understood that economic growth is impossible without it. Implications for the planet are another subject.

Human behavior only changes with trauma. That implies that energy solutions will remain improbable.

My work is for those who want to understand the present state of energy. I believe that is the role of science. Science is neither optimistic nor pessimistic. That seems to be in accord with the nature of the universe.

All the best,

Art

Thank you Art Berman for sharing your knowledge and insights.

Nancy,

Thank you.

Best,

Art

[…] naftowy Art Berman opublikował 3 września 2020 r. najbardziej wszechstronną analizę historyczną ropy naftowej i jej związku z gospodarką pt. Nie […]

[…] naftowy Art Berman opublikował 3 września 2020 r. bodaj najbardziej wszechstronną analizę historyczną ropy naftowej i jej związku z gospodarką […]

[…] will it end? Petroleum geologist and consultant Art Berman believes that U.S. oil production will be 5 million barrels below government estimates by July 2021 as U.S. shale production declines rapidly without renewed investment. He has logic on his side. […]

Art – Well written and thoughtful narrative. Thanks for sharing.

Thanks, Donald.

Best,

Art

I see it like this: The still growing world population till about mid-century will need lots more energy. However, the 2nd Great Depression we’re in – pick a fight with Jim Rickards if you don’t believe me – will probably last most of the first half of this century, driving down energy demand and prices as you say AB.

There is a lot going on with alternatives to oil, but much of it isn’t ready for prime time. Therefore the probability that there will be an energy shortage in the second half of this century when affordable oil runs out is high IMO. That will of course drive prices sky high.

AB, I’ve heard you on Macrovoices many times, and I know of nobody who understands energy better than you. Too few people understand the importance of energy. Those of us who do should do all we can to share our knowledge. Now please do shoot holes in my thesis for energy in this century.

I have met Jim Rickards and heard him speak several times. He is a bit of an opportunist but his thesis is fundamentally correct.

30 yearsis a long time from now. Your logic is sound assuming that we have any idea about what business-as-usual may be by then. My guess is that population will be much smaller and that the world will have self-organized around energy in more local or regional ways that are hard to imagine much less predict. That suggests that oil prices may not become very high but I honestly have no idea.

Best,

Art

[…] not foresee a normal recovery for either fossil fuels or the economy. In a recent presentation he notes that the pandemic has merely highlighted and accelerated the industry’s critical weakness: […]

[…] [iii] https://www.artberman.com/2020/09/03/stop-expecting-oil-and-the-economy-to-recover/ […]

Random rationalizations. I understand that Saudi Arabia is not the enemy of our oil industry based on the agreement from the mid-1950s. I hear rumors they are actually seriously thinking about cutting production, even though they are hemorrhaging economically since they are so heavily dependent on oil income, and mega cities built for tourism.

I also understand that Warren Buffett said that the time to buy is when blood is running in the street. Well, I haven’t heard a good word spoken about the oil industry in more than a year. Not sure how much worse I can get. Exxon’s stock is back to where it was when oil was $10/barrel, if I’m not mistaken.

If the share price goes up from here, great. If the dividend stays near 10%, great. I can take one of the other. But I can’t stomach the share price dropping substantially and the dividend being cut. That would really mess up my world. I’d be dictating my last history and physical as they are lowering my casket into the ground.

I realize your expertise is not financial advice. But, I value your insight even though I will eventually be making my own independent decisions.

Many thanks.

Art, i have been reading your work for some time and think it is great so thanks. i understand and agree with all that you are saying except the part about debt. money unlike energy is an artificial construct. yes conventional debt must be paid with interest but what happens when the federal reserve is buying treasuries. interest is paid to the fed by the treasury dept quarterly and at the end of the year that money is given back to the treasury dept. i am not at all sure how this changes anything you say but the confusing of money and wealth has always bothered me. oil is something that cannot be created by government fiat – a 20 dollar bill can be (or a computer generated one trillion dollar key stroke). i am not sure how or if this changes anything you say. here are two Alans on the subject –

ALAN GREENSPAN: “Well, I wouldn’t say that the pay-as-you-go benefits are insecure, in the sense that there’s nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The question is, how do you set up a system which assures that the real assets are created which those benefits are employed to purchase.”

Alan Watts – – on the fundamental confusion between money and wealth:

Remember the Great Depression of the Thirties? One day there was a flourishing consumer economy, with everyone on the up-and-up; and the next, unemployment, poverty, and bread lines. What happened? The physical resources of the country — the brain, brawn, and raw materials — were in no way depleted, but there was a sudden absence of money, a so-called financial slump. Complex reasons for this kind of disaster can be elaborated at length by experts on banking and high finance who cannot see the forest for the trees. But it was just as if someone had come to work on building a house and, on the morning of the Depression, the boss had said, “Sorry, baby, but we can’t build today. No inches.” “Whaddya mean, no inches? We got wood. We got metal. We even got tape measures.” “Yeah, but you don’t understand business. We been using too many inches and there’s just no more to go around.”

A few years later, people were saying that Germany couldn’t possibly equip a vast army and wage a war, because it didn’t have enough gold. What wasn’t understood then, and still isn’t really understood today, is that the reality of money is of the same type as the reality of centimeters, grams, hours, or lines of longitude. Money is a way of measuring wealth but is not wealth in itself. A chest of gold coins or a fat wallet of bills is of no use whatsoever to a wrecked sailor alone on a raft. He needs real wealth, in the form of a fishing rod, a compass, an outboard moter with gas, and a female companion.

Phillip,

I suppose you have not read or fully understood what I write about money as a call on energy and debt as a lien on future energy resources. The people you quote are experts on finance but not on economics, hence their foolish statements.

Best,

Art

Thanks for all your great articles and posts, Art! Perhaps a bit tangential to the conversation at hand, however I respect your knowledge and opinion and would be interested to know where you would invest your hard earned capital in the current environment. What are your thoughts?

Al,

Right now, I’m in wealth protection mode. I see a 50% chance of a major economic collapse in 2020 or 2021.

Best,

Art

Math error, or at least a strange calculation on your refined product consumption recovery graph. Current Gasoline rate is at 3.7/3.8 or 97% of historical value. Diesel is at 8.8/9.5 of historical, or about 93%. Kerosene is at 1.1/1.7 or 65% of historical. Much better than you presented, but the airlines are still hosed.

Mike,

Calculate the percent recovery from the 2020 minimum and the 5-year average and you will see that there is no error.

Best,

Art

It depends how far into the future you are looking. I don’t see a direct downward descent like going down a ladder. Rather it will be a rather bumpy decline, like going down a mountainside, with some periods of stability followed by further descent.

Not exact predictions but a rough model, say in 100 years, we are in the early 20th century. After 200 years, we will be likely at a 16th century level. And after 500 years, we will be at a 10th century level. By this time the descent will be over, and our political, economic and social realities will be in an essentially steady-state condition forever after.

All bets are off, of course, if drastic climate change or an asteroid strike happen.

Antoinetta III

Well, sure, the data is public. Your prediction is what I don’t think makes sense. EIA does a calculation of the decline of each tight oil play with no drilling at all and then adds drilling to get a prediction. Now some of their numbers are suspect, but declines are about 2% per field per month. That’s all production (all vintages). Do you really think the Permian etc will decline 50% in 1 year? Last year’s vintage might, but if you add up all the vintages (most of which decline at 10% or so), it’s far less than that.

Not sure how fast conventional is declining. You have it declining from 5.6mm to under 2.8 mm bpd from Jan to July of 2021. You’re curve fitting rigs to production (with a delay) but it doesn’t make sense, sorry at the extremes.

I guess we’ll see.

Oh, you’re reading the wrong numbers, lol. With an R0 of 3 and NO cross immunity, the number of humans on the planet that would need to get ANY virus would be 70%, or about 5 BILLION. I can tell you first hand that the 900K number from the CDC is a fabrication. Almost 4 MILLION US occupants die EVERY YEAR, and almost ALL of those deaths are DOWN this year, while CV is inflated. Pesky math. But we knew this, back in February.

Meanwhile, as you point out, the eCONomy is completely screwed. I’ve got my popcorn ready and no debt (in worthless dollars that is).

Randy,

It must be great to know more than everyone.

All the best,

Art

[…] Interesante análisis sobre la evolución del precio del petróleo y consumo de gasolina. Lo ponemos por su escepticismo con la tendencia reciente de recuperación y porque aun no siendo positivo sí justifica la inversión en petroleras a estos precios. link […]

How much of a downgrade in technology is going to occur? As we descend the ladder. Are we going to end up in the 19th to 20th Century level?

Evil,

I don’t know how to guess at that but I imagine internet will be an early casualty–gaming and the social BS that adds no productivity.

Best,

Art

“we will adjust to a large annual infection rate and death toll”

9200 US Covid deaths is considered large?! What data model are you using for your claim? What R0, what doubling time, etc? What are your primary vectors for spread? Curious.

27.7 mm cases and 900,000 deaths are big numbers.

Some of the numbers don’t make sense. You say refined product is 62% but the two largest pieces are 80%+. Also 18.5/21 is almost 90% (from your graph). Tight oil with no drilling probably declines 20% per year across all vintages. So how does it go from 7m to 3.5m in two years? And conventional declines 5m to 3m as well?

Brian,

The data is public. Work it out yourself: https://www.eia.gov/petroleum/supply/weekly/

Best,

Art

Hello Art,

Thank you for further insights.

As per your suggestion I’ve tried to crack down some numbers in order to understand how severe the issue is, and if, in fact, there is not enough discovered energy to repay outstanding debts.

With $255.3 trillion of global debt as of the end of 2019 we would need to use certain amount of energy in the future to repay the debt as per your point (“debt is a lien or a claim on future energy”).

If we can produce $1000 of global GDP with 0.125 TOE of primary energy, then we’d need almost 32 billion TOE of primary energy in order to produce extra $255.3 trillion of GDP. Would we continue to see some efficiency improvements as in the past we could reduce energy intensity of the global economy (say 1-3% annually) and assume this is an energy equivalent of the coupon for the $255.3 trillion debt principal.

Considering 2019 levels of total proven reserves of fossil fuels (Oil incl. other liquids, Nat. Gas, Coal) of 1.13 trillion TOE at the end of 2019 we would need 2.83% of them to repay all the 2019 outstanding debt (using only fossil fuels, ignoring other sources for simplicity). Additionally, 2019 R/P index for the fossil fuels at 86 years (ca. 83 years excluding the primary energy allocated to the debt repayment) should provide some comfort in terms of urgency of the matter.

The amount of energy available as per the proven reserves reporting allows also to believe that all future projected cash flows underpinning the 2019 value of global net wealth of $360 trillion are executable from an energy requirement perspective. There is still a lot of energy left for a further growth.

I understand that marginal cost of energy might be higher every TOE is produced, and total energy consumption will require more production of primary energy to cover additional energy allocated to the extraction and processing activities for more challenging resources from less dense sources but the absolute amounts still leave a lot of room. However much of this leeway is coming from coal, consumption of which does not fit any de-carbonization scenarios and is less energy dense. On the other hand, R/P ratios for oil and gas have been relatively stable in recent years showing the industry’s ability to replenish consumed reserves (with a massive support from debt markets).

I understand that some assumptions and energy conversion factors could be fine-tuned or discussed in this analysis but I’m wondering if the framework presented here addresses some of the issues with debt you were referring to?

Overall, such a holistic approach based on 2019 data does not reveal energy as a limiting factor for a global growth. In fact, it is more in line with a proposal of Daniel Lacalle and Diego Parrila from their book “The Energy World is Flat.”

I’m wondering where one should look to shed some light on the issues you raise in order to clearly show in a fact-based regime that the global economy gradually could not afford more costly reserves. Maybe an analysis aiming at marginal costs of energy production and their impact on global productivity curve could show this relationship more evidently – how reaching out for more costly reserves e.g. impacts productivity of capital and labor?

I’m curious what your thoughts are.

All the best,

Bohdan

Bohdan,

Surplus energy beyond energy need is required to fund the debt including the cost of drilling, transportation, refining and distrubution.

Best,

Art

Enjoyed the post Art. The ever-increasing debt in all systems is fascinating (and worrisome). Interesting analogy about ‘dissipative structures’ and always enjoy references to what Nate Hagen’s is thinking about. Regarding oil price/supply: If prices persist in the $40’s, 2021 will be another year of extremely constrained spending and US oil production may indeed drop to 50% of 2019. But we’ve proved US and world supply very responsive to price and if we can keep pushing on ‘this string of an economy’, O&G supply is not my main worry for the next decade.

Tom,

What is your main worry for the next decade?

Best,

Art

Good Morning!

Your response above: Energy is the economy and oil is the largest and most productive component of energy. ………. the next big thing in the U.S. economy. It will always be energy. ……….. Humans are only different in our ability to use technology to increase the flow of existing energy.

I fully understand and agree with your conclusions and have read your sources/references (e.g. Vaclav Smil)

HOWEVER, I must ask if you have an opinion/position on:

“Supposedly”, the efforts by Jeff Bezos’ “Blue Origin” space program is to overcome this reliance on “fossil fuels” and mine the moon for Helium 3 to power nuclear fusion for “unlimited cheap energy production”

https://tinyurl.com/yxtz2lkm

(This is why Blue Origin’s rocket engines are designed to operate on Hydrogen where as Musk’s SpaceX rockets are powered by kerosene. Bezos wants to produce hydrogen fuel IN space instead of lifting kerosene from earth.

Now ordinarily, I would have the opinion that “if it ain’t on the shelf, it’s Flash Gordon/Star Wars fantasies” and of no use to consider for the present or even the next 20 years.

Now, after researching and learning that China, India, Russia, EU and even Israel are making “moon-landing efforts” and China has landed on the dark side of the moon with a robot SEARCHING FOR AND FINDING Helium 3, (which would in a sense have an energy density far greater than oil)

Are we on the cusp of a new energy “transition”?

Various sources “claim” that they could be mining the moon by 2025.

And the ITER https://www.iter.org/ actually making progress on a fussion reactor (scheduled to start 2025)

When one considers the incredible investments (subsidies/debt) being pumped into these space programs and this International ITER project,

Is this the possible dawn of a new era? Or a massive government subsidized white elephant?

https://tinyurl.com/y5w5p4oh

Peter,

Thanks for your comments, links and thoughtful question.

I have little doubt that there is some potential for Helium as a future energy source. It’s existence on the moon and interest by China and others to be first movers has been known for many years. There is, however, a huge difference between pioneering R&D and anything remotely feasible commercially.

People have been searching for viable alternatives to oil for almost as long as it has been an important energy source. Those efforts have so far been unsuccessful for a good reason namely, that even at higher prices, nothing yields the same value per unit as oil (https://www.sciencedirect.com/science/article/pii/S0921800919310067).

That said, I am concerned about affordability of oil with the current economic disaster unfolding in the world. As you know from my latest post, I believe that the world will be much poorer going forward at least for a decade if not much longer.

I’m glad that visionaries are exploring the possibilities for Helium from the moon. I’m a lot more concerned with saving the global economy from collapse in 2021.

Please contact my business manager if you would like to continue this discussion: [email protected]

All the best,

Art

I

Hello Art,

Thank you for this article and your work, very inspiring. I’ve also followed Dr. Hagens’ and Gail Tverberg’ work recently.

I thinks I get what a reasoning might be here in regard to the role of energy and the value it brings to the economy and societies. I can see that costs of oil e&p have gone up as we’ve reached out for more difficult sources.

As per my understanding of those other reads, since the cost of energy goes up societies can allocate less capital and labour for other activities (Gail Tverberg) or more energy consuming activities become less profitable/ unprofitable (Dr. Hagens). In a result the economic growth is limited.

I’m trying to understand why relatively small changes in oil production costs make such a great difference for economic prosperity.

For simplicity taking 100 million bbl per day of daily oil consumption a $10 change in cost result in 0.4 trillion which is ca. 0.5% of global GDP ($80 trillion, 2019, nominal). On the other hand isn’t our productivity improvement offsetting this lost efficiency in energy production?

Or maybe measuring this in monetary terms doesn’t make sense and we should observe the cost level in more physical terms – are we employing more labor, are we using more of other production factors which reduces their availability to other activities. Well, we haven’t seen material shortages of labor (even qualified) in recent years of tight oil expansion.

I get that this additional cost may also kill some business cases for energy intensive industries, further reducing the growth but we don’t hear that some industries suffer seriously because of energy cost increases. Is the $10 or $20 increase in the oil production cost per bbl (all in, capex, opex, cost of capital) a game changer for the way societies live?

Would you please refer to this way of thinking?

All the best,

Bohdan

Bohdan,

I believe that the missing connection for you is debt. Debt is a lien or a claim on future energy. As society increases its debt, it’s ability to re-pay depends on the cost and availability of energy supply that isn’t fully known or even discovered.

While the cost of extracting and producing energy is increasing, the quality of the energy is decreasing. In the case of tight oil, its energy content is about 10% less than a standard barrel because it has a lower specific gravity (API) with more light hydrocarbons and fewer heavier hydrocarbon molecules. So, it costs more to get less.

Debt includes an interest expense. Debt is fine as long as debt productivity exceeds the debt service. Society’s debt is increasingly less productive.

I hope this helps you to understand things better.

All the best,

Art

[…] Art BermanStop Expecting Oil and the Economy to Recover – Art Berman […]

[…] Art BermanStop Expecting Oil and the Economy to Recover – Art Berman […]

Hi Mr Berman, EIA warned us of an energy shortage of 34 mbd of oil by 2025. Do you believe that we will achieve energy rationing and control of daily life as if it were a police state?. Thanks and congratulations for you great job

Juan,

As I stated in my post, I suspect that oil supply and demand will fall together. The initial rates may not be in phase and that may lead to temporary deficits and surpluses. EIA uses a business-as-usual assumption that is reasonable. Other assumptions are equally reasonable. EIA provides different cases in their annual energy outlook but these are still variations on business-as-usual. I don’t mean these comments critically.

Best,

Art

Art ,commenting for the first time ,but have been following your work for a very long time . As someone who learned about peak oil from Matt Simmons , Campbell and like you will know how back I go . Just to say thank you for cleaning the mirror when the whole world is stumbling with the smoke and mirror narratives . Once one understands “Energy is the economy” life becomes simpler . Thanks once again .

Ravi,

Colin and Matt were great mentors.

Best,

Art

Hi Art,

It is not evident to most but our global industrial civilization reached its peak in the early 70s. Unable to continue exponentially growing its energy consumption, our civilization turned to increasing levels of debt and globalization. Instead of flying cars and cities in space we got internet, which is a lot less energy consuming. In the 90s the incorporation of China to global commerce allowed to continue growing the World economy. Debt based growth is creating a global affordability crisis. It manifests as an increasing demand crisis that no amount of monetary expansion can fix. As a result industrial companies are increasingly becoming zombies. They get the money to continue pushing up their market value and dividends, but their sales are insufficient. Peak Car took place in 2017, more than two years before the COVID crisis. Peak Oil (C+C) took place a year later. Peak Coal in 2013. None of those look like is going to be surpassed any time soon.

We are already declining and will have to do with less. As people don’t like that, social unrest is increasing. We have rough times ahead.

Javier,

Thanks for those observations. Sadly, I agree.

Best,

Art

Great post Art! Thanks!

Thanks for the comment, Tarun!

[…] Stop Expecting Oil and the Economy to Recover September 3, 2020 […]

Hello Art,

I like your writing and position regarding unconventional exploration.

However, with the understanding that I am a “conceptual guy”, not a fact/detail guy, and not a financial type person.

This said, my understanding of oil and gas companies has evolved to:

Several large, extremely profitable discoveries/fields that generate tremendous cash flow. “In between” discoveries much money is spent/lost to dry holes, technology, CEO salaries, etc., until the next large profitable discovery. There may be significant periods of time between large discoveries, year or years.

The corporate view being stated, my view of the U.S. economy is similar.

Large discoveries with long periods of decline, money spending until the next large discovery.

For example, since 1950’s, U.S. automobile industry,oil and gas industry, computer/technology/electronics industry, as the three huge discoveries moving the U.S. economy forward(I’m sure I forgot something, but big three in my mind).

So question to you:

What do you think next big discovery will be to drive U.S. economy?

(note that I have already put oil and gas industry as a past driver of U.S. economy)

Regards,

Greg Hatch

Greg,

Energy is the economy and oil is the largest and most productive component of energy. I would, therefore, urge you to revise your framework for the next big thing in the U.S. economy. It will always be energy. It is energy for every living organism and species on the planet. Humans are only different in our ability to use technology to increase the flow of existing energy.

I suggest that you read Vaclav Smil’s “Creating the Twentieth Century.” He argues that all of the technological breakthroughs like computers, internal combustion engines, etc. were based on ideas and discoveries made before WWI.

All the best,

Art

Art, I followed your line of thinking until Figure 4. You said most of the 2009-2019 production growth came from shale and long cycle projects (deep water and oil sands), and conventional production declined 9%. I presume this decline will continue going forward.

How will 2Q21 supply rebound to the estimated levels in Figure 4 considering further declines in US production and what I assume is little to no CAPEX invested in long cycle projects?

Brian,

As I stated about Figure 4, “I don’t believe that either forecast is likely but let’s put that aside for now so we can understand the best-case outcome.” Forecasts are useful to summarize mainstream thinking about the present and near term future. The simple answer to your question about rebounding production is that it won’t.

The key message of the post is that “it is unlikely that either oil supply or demand will ever return to 2018 levels on a sustained basis.”

All the best,

Art

Art

From above: “U.S. production may be 50% lower by mid-2021 than at year-end 2019. The implications for U.S. geopolitical power and balance of payments are staggering. It seems likely that the economy will weaken as government support for the unemployed decreases.”

Staggering indeed.

Do you expect gasoline and diesel shortages to occur as a result of this possible 50% production decrease? You note above the impact to balance of payments, you are assuming we will be buying and importing some of the lost production from overseas? Can we (refineries?) purchase all the U.S. economy needs to satisfy (much lower) fuel demand?

Thank you.

Shawn,

The honest answer is, I don’t know. My guess as I stated in the post is that supply and demand will largely move in tandem. There may be short-term imbalances but I don’t see shortages or gluts.

Goehring and Rozencwajg seem to forget that refined product markets are international and other countries will gladly sell us their products if our supply falters.

Best,

Art

“Stop Expecting Oil and the Economy to Recover [, But Keep Eyeing When The Civilisation Releases You From Its Broken Social Contract]”

The social contract since the early coal of 1700s has been sealed between the Civilisation and its citizens with abundant fossil fuels supplies.

When supplies stop, the social contract stops being current, naturally and automatically, too.

Nafeez, a proponent of the-now outdated positive-EROEI line of thinking, assumes that in the 30 coming years the oil industry and the social contract will still be intact – as in the days of James Watt.

Nafeez ignores history where hand-picked coal didn’t need an Industry. Smuggled crude oil will not need an industry or governments, too. It needs smugglers and warlords (see stories coming from Syria, Yemen, Iraq, Libya on smuggled oil).

Ilya Prigogine in his Self-Organisation thesis assumes “The system either collapses or spontaneously re-organizes itself” but never dies!

Hagens assumes debt becomes real the moment the keyboard’s button is pressed issuing it, but never able to explain why something synthetically created out of a thin air must be taken so seriously and it should be considered so real – it even brings Civilisations to collapse?

Cannot the person who pushed the button creating the debt – push another button wiping it out – entirely?!

All three arguments above, or how they’ve been interpreted, in the case of Ilya Prigogine, overlook the impact of Energy on the continuity of the social contract itself when no excess energy will still be available enforcing it.

Citizens always outlast their Civilisations. They stick around when little surplus energy still possible to extract from them but turn against the social contracts with them the moment Civilisations become energy-negative.

(see BLM in the US, unrest in Belarus, Hungary, Hong Kong and elsewhere, and reports that are rushed over the media spectrum to assure that we are back-to-normal with fossil fuels demand – an assertion so essential to propagate for the sake of the continuity of the social contract, whether true or false).

For the Civilisation itself, the predicament cannot be won as – “in an Energy system, Control is what consumes Energy the most”, and that’s why Maxwell’s demon experiment in Physics always fails.

Nafeez, Hagens and Self-Orginisation proponents inspire that our Civilisation has decided to try what ever it takes to morph itself into the next.

It should be brave and responsible enough to consider dissolving itself and its fossil fuels-written social contract, peacefully and with dignity – instead.

Otherwise, for the citizens, the only option left is – Desertion!

https://youtu.be/xvsfHBuP_M4

Major,

I don’t see a question in your comment so I will only say that I disagree that self-dissolution is part of the genetic framework of life.

Best,

Art

Great post, Art!

Thanks, Eugene.

Very interesting read and perspective. Supply and Demand often moves in tandem, and of course could do here too. On balance I think you are only too certain for two reasons: COVID-19 could resolve quite quickly with a vaccine and then demand would be likely to return much faster (all other things being equal) than post the 2008 crisis while supply may still be tight (albeit probably for a shorter time than if demand remains depressed for longer) and I also think it is far from certain that the world goes wind and solar to the extent that you predict for the simple reason that people won’t accept lower living standards unless their lives depend on it, and growth and higher living standards is what 3 billion people in Asia and another 1,5 billion people in Africa will favour.

Olof,

As I stated in the post, this is not happening because of a virus. The virus was an accelerant. If there is a vaccine, it will certainly help but the economy is on life-support in the ICU and will remain in critical condition long after the virus is contained (it never will be fully contained; like flu, we will adjust to a large annual infection rate and death toll). Assuming the patient lives, he will spend a long time in physical therapy and may never return to his level of health before the emergency.

Among the many messages in Prigogine’s work is that non-unitary (time-variant) transformations are a feature of dissipative structures. These transformations are what classical physics called “irreversible processes.” In far-from equilibrium systems, irreversibility may not be applicable but time-variance indicates that the system will not return to its previous state.

Best,

Art

Hi Art, a great brief on the future. I will add that in his 1954 book “The Challenge of Man’s Future” Harrison Brown, a Caltech geochemist wrote: “we are quickly approaching the point where, if machine civilization should, because of so time catastrophe, stop functioning, it will probably never again come into existence”. He added: “It is not difficult to see why this should be so if we compare the resources and procedures of the past with those of the present. Our ancestors had available large resources of high-grade ores and fuls that could be processed by the most primitive technology” … “now we must dig huge caverns and follows seams ever further underground, drill oil wells thousands of feet deep”… “and find ways to extracting elements from the leanest of ores-procedures that are possible onlyu because of our highly complex modern techniques”.

When these are used up we can only scavenge from existing structures. best, Seppo

Seppo,

Complexification and the energy needed to support increasingly complex connections are a defining characteristic of dissipative structures. It’s the way life is–not just human life: the growth imperative is genetic. It is neither positive nor negative. All life self-organizes around energy. As organisms and species grow, they become more complex and need increasingly sophisticated means to ensure greater energy supply.

Best,

Art