Art Berman Newsletter: March 2020 (2020-2)

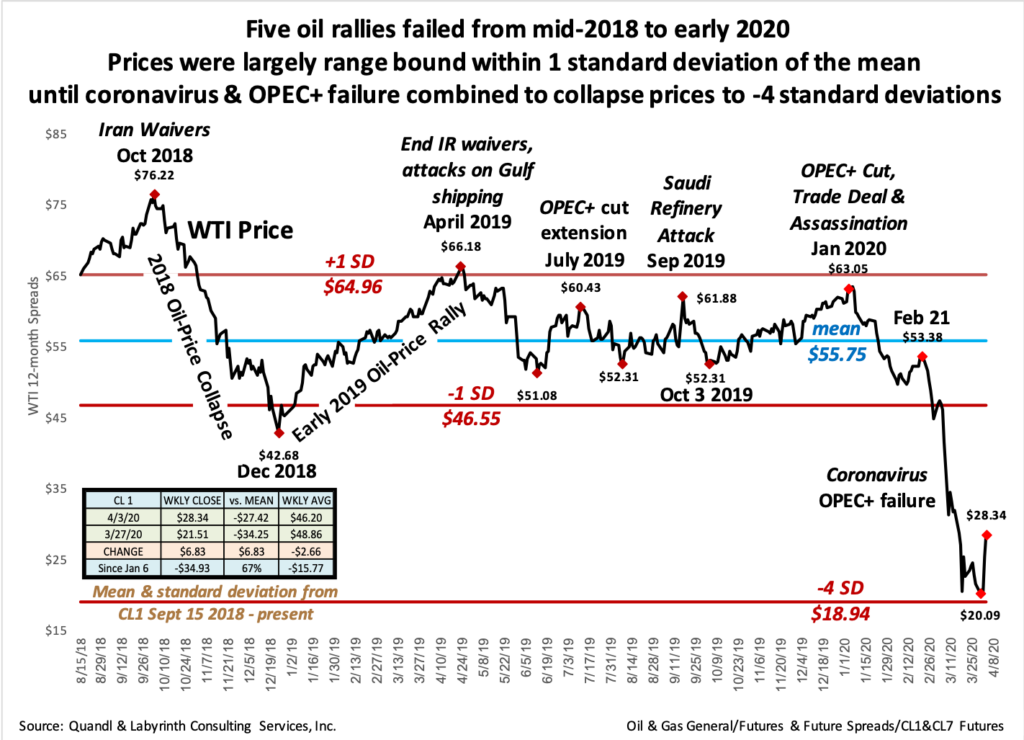

The March oil price collapse resulted from closing the U.S. economy and a terrible blunder by the world’s leading exporting nations. On Saturday March 7, discussions between Saudi Arabia and Russia ended with no agreement to cut production. On Sunday, Saudi Arabia announced price cuts and its intention to boost production. The largest single-day fall in oil prices occurred the next day.

Things were not looking good for oil prices before then. Prices had peaked in early January with the assassination of Iranian General Soleimani, the announcement of a U.S. – China trade agreement and an OPEC+ production cut. As I wrote in late December, the price rally was doomed because it was based on sentiment and not market fundamentals.

Then the Coronavirus outbreak became public. I wrote in early February that Coronavirus would crush oil prices. It did. The Saudi price cut in March compounded and accelerated the collapse of oil prices and of broader markets. Prices reached a bottom on March 30 at just above $20 for WTI (Figure 1).

Source Quandl and Labyrinth Consulting Services, Inc.

Why It Happened

Mohammed bin Salman (MBS), the Crown Prince of Saudi Arabia delivered an ultimatum to Vladimir Putin, the president of Russia, to cut oil production on his terms. Mr. Putin doesn’t accept ultimatums so he ignored it. MBS cut prices and announced a production increase.

The events of early March were an axiomatic response by Saudi Arabia taken from earlier playbooks. Between 1981 and 1985, the Saudis cut their production by 6.8 mmb/d hoping to stop the decline of oil prices in the face of new supply from the North Sea, Siberia and Mexico (Figure 2). King Fahd got tired of cutting without much help from OPEC allies and with no resulting price relief. He fired oil minister Ahmed Yamani, cut prices and increased production.

Source: EIA, BP and Labyrinth Consulting Services, Inc.

In 2014, world oil prices were again collapsing. Saudi oil minister Ali al Naimi asked Russia to join OPEC in cutting production. Russia refused. Saudi Arabia cut prices and increased production. See the pattern?

The guiding principle of Saudi oil strategy over the last three decades has been to never again make the mistake it made by cutting production alone in the early 1980s. Analysts and journalists who say that there is a price war or a war on shale should study history instead of inventing mindless memes.

Trump to the Rescue

Then, President Trump got involved and announced that a coordinated production by the U.S.-Saudi Arabia-Russia was being discussed. Prices increased to $28.34 by April 3. There was no output agreement , in fact, but market sentiment is a sucker for good theatre. Prices cratered on Monday as reality raised its head and prices are lower by more than $2.00 per barrel at this writing. Hope versus reality will be the manic pattern for 2020.

To Trump’s credit, he may have found a way for Mohammed bin Salman and Vladimir Putin to reverse their terrible blunder, save face and emerge looking like much better guys than they really are.

An agreement means conceding to the lack of demand for their oil. Price takers can’t be choosers. It will be lipstick on an ugly pig made larger than life by the closure of the world economy. If an agreement happens, we will see how much of it is sleight-of-hand arithmetic based on imaginary starting levels of output much mentioned but never seen.

Energy is the Economy

Energy is the economy and most of the world’s energy comes from oil. The present devaluation of oil will spread to other commodities and currency. Although oil-price devaluation was inevitable because of coronavirus, the recent Saudi price cut and production increase have accelerated and compounded its effect on the global economy. It may become a Lehman moment.

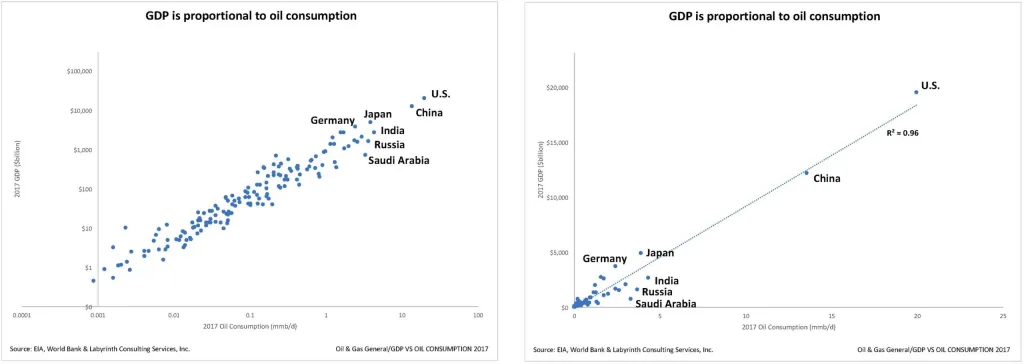

GDP will fall as less oil is consumed. That is empirical–GDP and oil consumption have an R2 correlation of 0.96 (Figure 3). What may not be well understood is how much the U.S. and China dominate this relationship.

Figure 3 shows two charts using the same data. The graph on the left has logarithmic scales and the graph on the right has cartesian scales.

The graph on the left has logarithmic scale and the graph on the right has cartesian scales.

Source: EIA, World Bank and Labyrinth Consulting Services, Inc.

The left-hand graph shows the correlation. The right hand graph shows the disproportionate weighting of China and the US on both GDP and oil use. Together, they account for 32% of world GDP and 34% of oil consumption.

China’s oil consumption is probably down 4 mmb/d for the first quarter of 2020. If it returns to normal by Q2 (unlikely), that implies ~1% drop in annual global GDP. Things won’t normalize in China and the U.S. contraction will compound lower consumption well beyond Q1 not to mention lower consumption in the rest of the world. There are lots of reasonable objections to using this correlation deterministically but it offers a high-level perspective about where the economy is probably going. That’s why it is difficult to imagine an outcome other than depression.

The global economy has been dying of accumulated debt for 50 years. Coronavirus has sent it to the intensive care unit.

Through a Glass Darkly

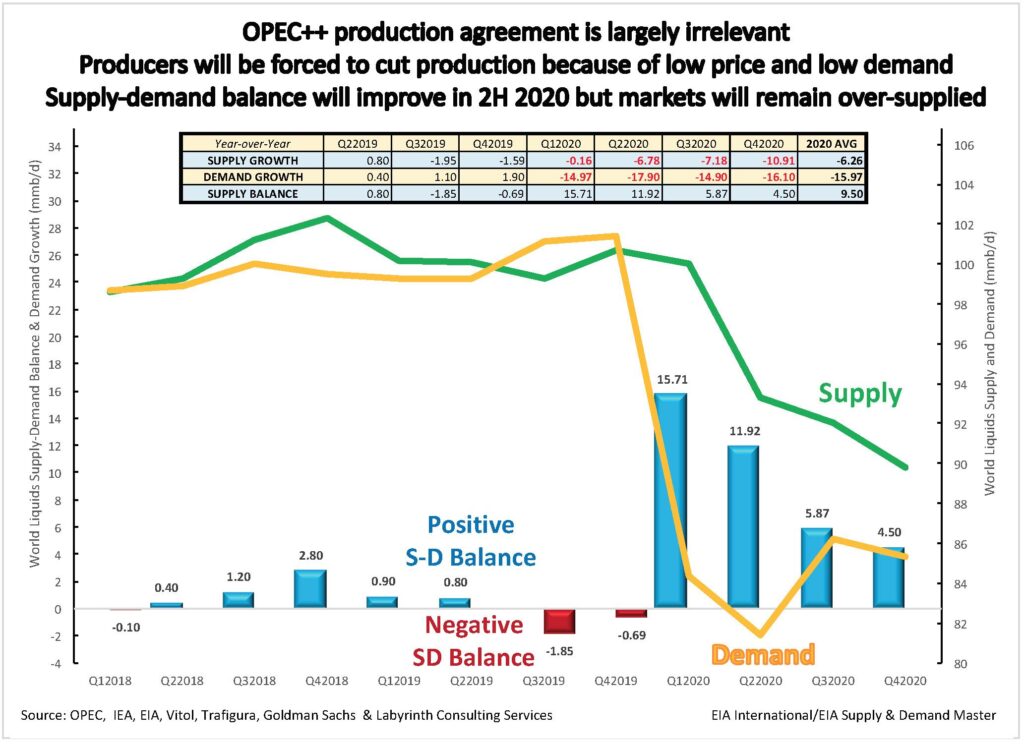

The closing of the world economy has caused the greatest demand decrease at least since the 1980s and probably ever. Many credible sources have estimated demand levels for 2020 but there is little data so far.

Figure 4 is a thought experiment. I have integrated many estimates into a possible scenario. It is based on expectations of how long the economy may be closed and how this will affect oil supply, demand and price. It anticipates an 18 million barrel per day maximum annual demand decrease in the second quarter of 2020. Unlike other models, it does not include a rapid economic recovery in the third quarter.

Source: OPEC, IEA, EIA, Vitol, Trafigura, Goldman Sachs, Rystad Energy and Labyrinth Consulting Services, Inc.

That’s because I don’t believe that the world will go back to work in May. I doubt that the world will go back to work in June.

That means that people–not just corporations–will have to be supported by thin-air money created by central banks or the economy will collapse. The $2 trillion allocated by the U.S. will be grossly insufficient. Use whatever imaginary multiple you like to estimate what the world must spend. This may become the greatest global currency devaluation in history.

Demand is so weak and price is so low that all producers in the world will be forced to shut in production. The only reason Russia and Saudi Arabia may agree to a cut is because they now see that they have no choice but to decrease output. They might as well look good doing what is inevitable anyway.

Figure 4 also shows a second demand decrease in the fourth quarter. That is because it is possible that the second wave of Coronavirus will close the economy again, at least partially. I hope that I’m wrong.

I have not seen any analysis about why the United States is engaged for the first time ever in discussions with the two leading oil exporting countries in the world. It’s because the U.S. has become a major exporter since the crude oil export ban was lifted in late 2015. Exports averaged 3.5 million barrels per day in the first quarter of 2020. This trade depends on a $4.00 per barrel Brent spot premium to WTI to cover transport costs from Cushing, Oklahoma to overseas markets. Since the failure of OPEC+ talks in early March, that arbitrage has turned negative.

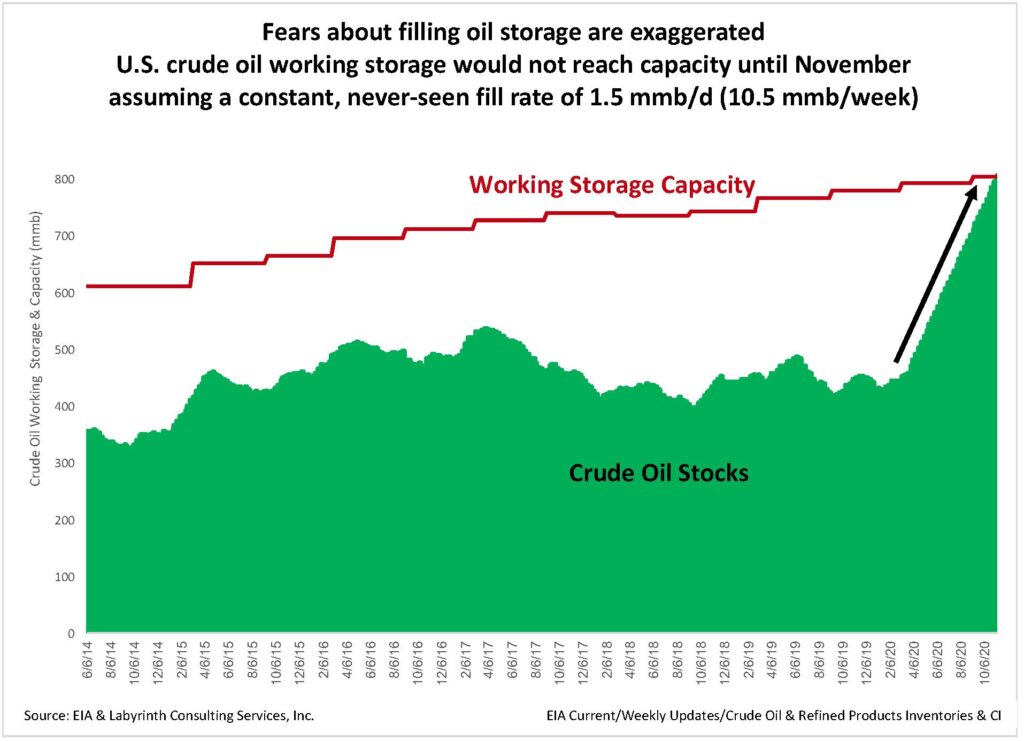

Most analysts believe that world oil storage will soon be filled to capacity because of falling demand. Even those who agree that a coordinated output cut would make little difference on the demand side believe that it would take help the impending storage crisis.

Fears of filling oil storage are exaggerated. It was widely believed that storage would be overwhelmed in 2016. The gap between crude oil stocks and working capacity never fell below 192 million barrels. If U.S. storage began filling at a constant and never-before seen rate of 1.5 million barrels per day, working capacity would not be filled until November (Figure 5). That doesn’t include the 77 million barrels available in the Strategic Petroleum Reserve. Markets are ruthlessly efficient and production will almost certainly slow before there is a storage crisis.

Source: EIA and Labyrinth Consulting Services, Inc.

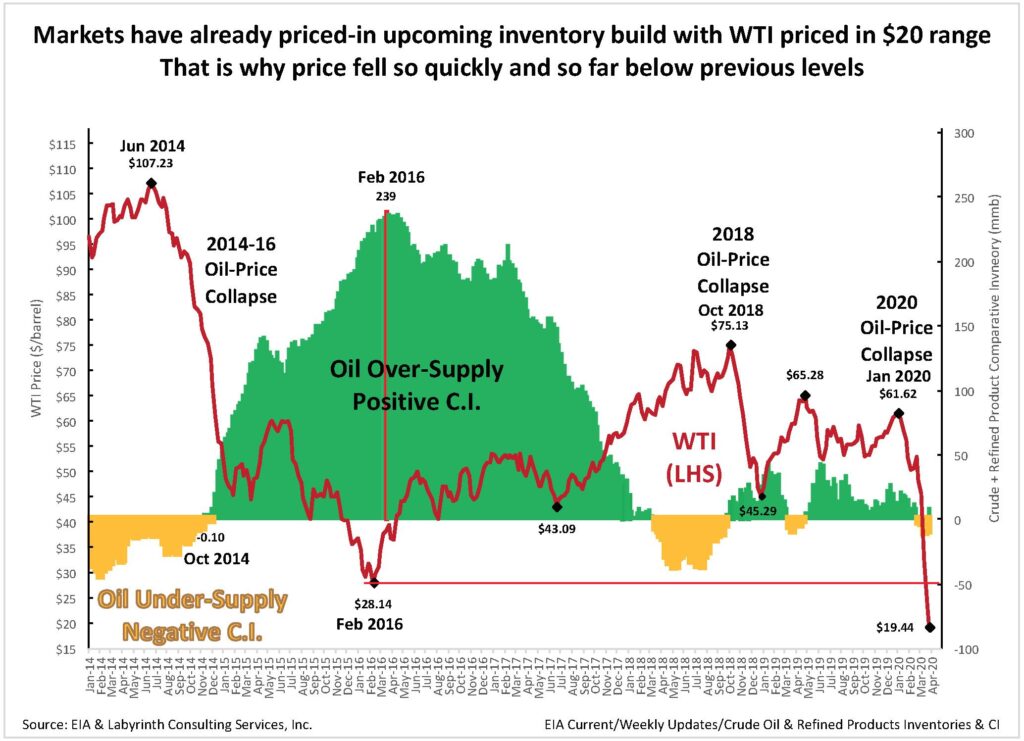

The reason that oil prices fell so rapidly and so low was because markets had already priced-in the upcoming inventory build. Ordinarily, the relationship between oil price and comparative inventory is a trial-and-error process that relies on weekly storage reports by the EIA. In the case of Coronavirus and the closing of the world economy, however, inventory build can be calculated based on estimates of how long the closure will last multiplied by a demand-loss scalar.

Figure 6 shows the comparative inventory build associated with the 2014 oil price collapse. I believe that markets expect a similar build for the Coronavirus crisis but assume that it will occur more quickly.

Source: EIA and Labyrinth Consulting Services, Inc.

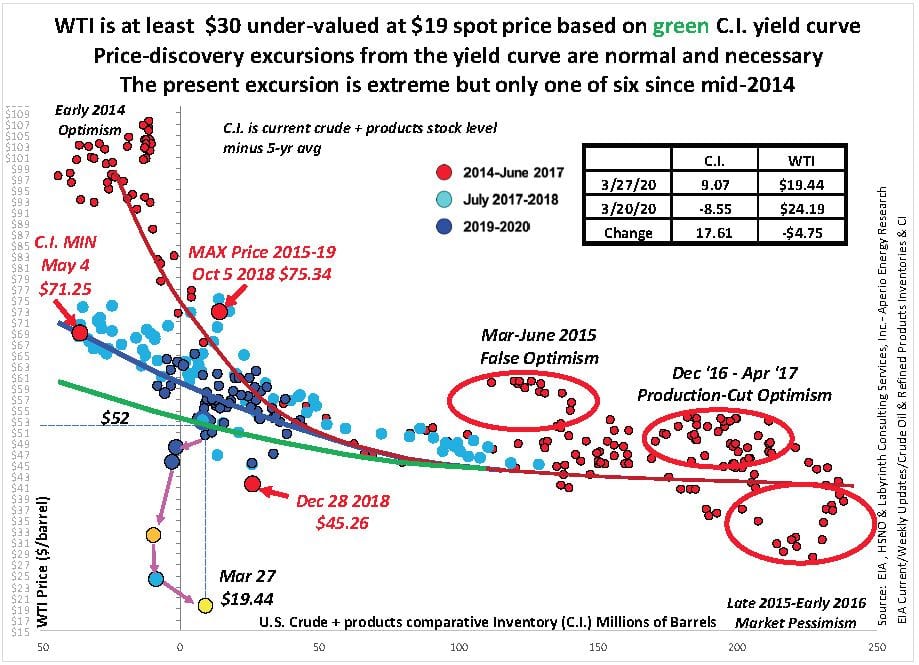

An output agreement will result in higher oil prices–for awhile anyway. Figure 7 shows U.S. crude + products comparative inventory versus WTI price for the week ending March 27, 2020. At $19, WTI was at least $30 under-valued based on the green C.I. yield curve. There’s room for higher prices.

Source: EIA and Labyrinth Consulting Services, inc.

The problem is that supply cannot possibly fall as fast as demand in the present situation. Once markets realize or even suspect that this is the case, prices will collapse maybe to even lower levels than in late March.

It is curious that in this age of customer focus, oil exporters seem blind to the buy-side of the oil market. China is mentioned in almost every analysis of global economics yet has hardly appeared in any reporting on the potential coordinated production cut.

Almost everyone says that we will get through this. I wonder what things will be like when we do. It seems likely that oil markets and, therefore, the world economy will be quite different. Shale plays will continue to supply more than half of U.S. oil but total output may be lower. Many companies will disappear. I doubt that oil production or prices will return to 2018 levels for many years.

It seems unlikely that what is happening today will cause society to experience some transformative epiphany that will end the age of oil. If anything, we will need inexpensive liquid fuel more than ever in a poorer world. Rather than seeing 2020 as a year of unspeakable loss, it is my sincere wish that we somehow find ways to live better with somewhat less.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts