The Irrelevant OPEC++ Production Cut

I’m in favor of the global output cut orchestrated by President Trump but let’s recognize it for what it is: largely irrelevant.

Mohammed bin Salman and Vladimir Putin were glad to burn down the world a month ago when they walked away from production cuts. They had dueling temper tantrums in the junior high locker room while the world descended into economic Armageddon. To Trump’s credit, he may have found a way for them to reverse their terrible blunder, save face and emerge looking like much better guys than they really are.

An agreement means conceding to the lack of demand for their oil. Price takers can’t be choosers. It will be lipstick on an ugly pig made larger than life by the closure of the world economy. If an agreement happens, we will see how much of it is sleight-of-hand arithmetic based on imaginary starting levels of output much mentioned but never seen.

Energy is the economy and oil is the largest and most productive part of world energy. The global economy has been dying of accumulated debt for 50 years. Coronavirus has sent it to the intensive care unit.

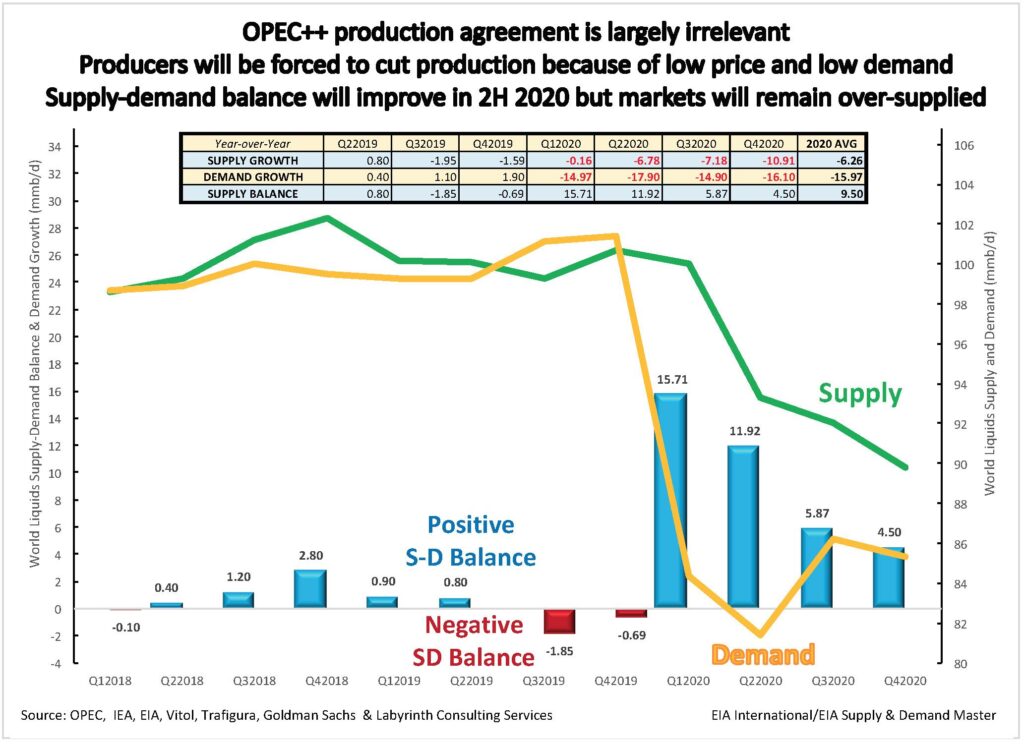

The closing of the world economy has caused the greatest demand decrease at least since the 1980s and probably ever. Many credible sources have estimated demand levels for 2020 but there is little data so far.

Figure 1 is a thought experiment. I have integrated many estimates into a possible scenario. It is based on expectations of how long the economy may be closed and how this will affect oil supply, demand and price. It anticipates an 18 million barrel per day maximum annual demand decrease in the second quarter of 2020. Unlike other models, it does not include a rapid economic recovery in the third quarter.

Source: OPEC, IEA, EIA, Vitol, Trafigura, Goldman Sachs, Rystad Energy and Labyrinth Consulting Services, Inc.

That’s because I don’t believe that the world will go back to work in May. I doubt that the world will go back to work in June.

That means that people–not just corporations–will have to be supported by thin-air money created by central banks or the economy will collapse. The $2 trillion allocated by the U.S. will be grossly insufficient. Use whatever imaginary multiple you like to estimate what the world must spend. This may become the greatest global currency devaluation in history.

If the economic patient survives the ICU, it will need a long period of recovery and therapy before returning to its previous life.

Which brings me back to oil. Demand is so weak and price is so low that all producers in the world will be forced to shut in production. The only reason Russia and Saudi Arabia may agree to a cut is because they now see that they have no choice but to decrease output. They might as well look good doing what is inevitable anyway.

An output agreement will result in higher oil prices–for awhile anyway. At $30 WTI and $35 Brent, prices are at least $20 under-valued so there’s room for higher prices. The problem is that supply cannot possibly fall as fast as demand in the present situation. Once markets realize or even suspect that this is the case, prices will collapse maybe to even lower levels than in late March.

Figure 1 also shows a second demand decrease in the fourth quarter. That is because it is possible that the second wave of Coronavirus will close the economy again, at least partially. I hope that I’m wrong.

I have not seen any analysis about why the United States is engaged for the first time ever in discussions with the two leading oil exporting countries in the world. It’s because the U.S. has become a major exporter since the crude oil export ban was lifted in late 2015. Exports averaged 3.5 million barrels per day in the first quarter of 2020. This trade depends on a $4.00 per barrel Brent spot premium to WTI to cover transport costs from Cushing, Oklahoma to overseas markets. Since the failure of OPEC+ talks in early March, that arbitrage has turned negative.

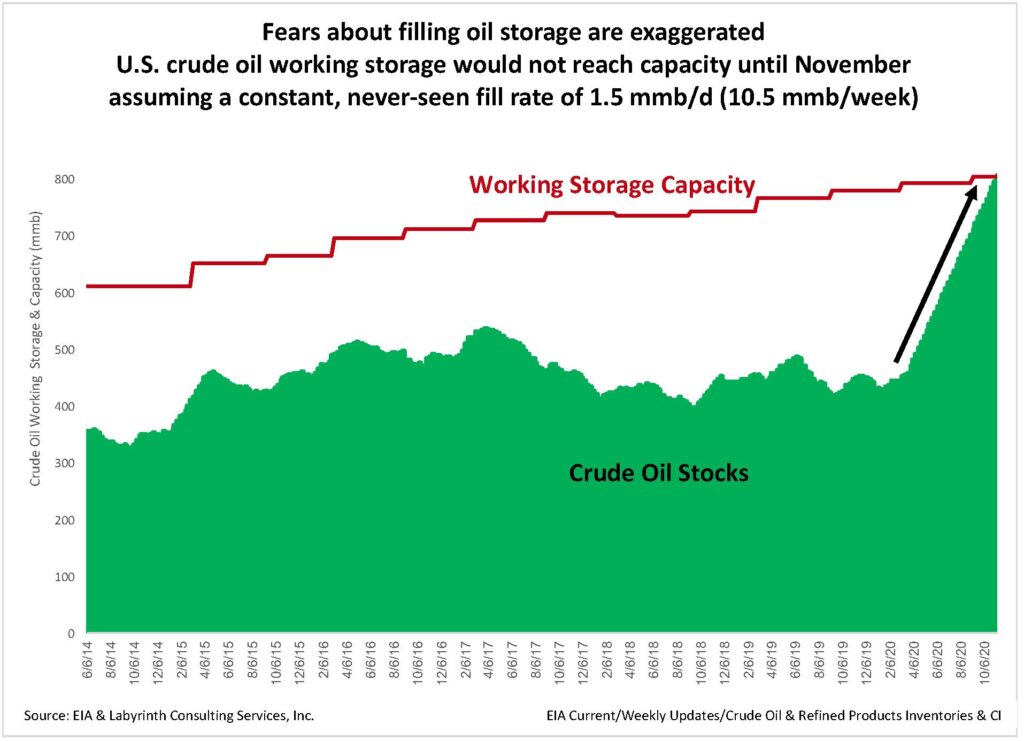

Most analysts believe that world oil storage will soon be filled to capacity because of falling demand. Even those who agree that a coordinated output cut would make little difference on the demand side believe that it would take help the impending storage crisis.

Fears of filling oil storage are exaggerated. It was widely believed that storage would be overwhelmed in 2016. The gap between crude oil stocks and working capacity never fell below 192 million barrels. If U.S. storage began filling at a constant and never-before seen rate of 1.5 million barrels per day, working capacity would not be filled until November (Figure 2). That doesn’t include the 77 million barrels available in the Strategic Petroleum Reserve. Markets are ruthlessly efficient and production will almost certainly slow before there is a storage crisis.

Source: EIA and Labyrinth Consulting Services, Inc.

It is curious that in this age of customer focus, oil exporters seem blind to the buy-side of the oil market. China is mentioned in almost every analysis of global economics yet has hardly appeared in any reporting on the potential coordinated production cut.

Almost everyone says that we will get through this. I wonder what things will be like when we do. It seems likely that oil markets and, therefore, the world economy will be quite different. Shale plays will continue to supply more than half of U.S. oil but total output may be lower. Many companies will disappear. I doubt that oil production or prices will return to 2018 levels for many years.

It seems unlikely that what is happening today will cause society to experience some transformative epiphany that will end the age of oil. If anything, we will need inexpensive liquid fuel more than ever in a poorer world. Rather than seeing 2020 as a year of unspeakable loss, it is my sincere wish that we somehow find ways to live better with somewhat less.

Thanks to Erik Townsend and Nate Hagens for useful discussions on this subject.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

[…] Berman predicts shale plays won’t vanish, but their output will be lower. “Many companies will disappear. […]

[…] Berman predicts shale plays won’t vanish, but their output will be lower. “Many companies will disappear. I […]

Yes, looks like we will be in this thing for a year or more. The Chinese, after a very draconian lock down for two months, are still finding asymptomatic positives walking around, infecting people after the lock down. For us to achieve what they did will take many months of time and a coordinated response from the top. Given the bickering between the two parties and lack of leadership from the top, I just don’t see it happening. Most likely, this thing will go right through the summer and into next year. Herd immunity is elusive. The Chinese just did anti-body testing in Wuhan. The hardest hit city in China, the preliminary results show 2-3% of the people in that city had positive anti-bodies, a long way away from herd immunity. Vaccine is our last hope, but that won’t come til next year.

John,

I don’t see a solution to CoV. It is now part of the human ecosystem like flu and the common cold. I don’t want to minimize the deaths but it’s more about managing the healthcare system load.

Best,

Art

Tom,

Nate and I are good friends. I am his oil and gas go-to guy and he inspires me with the larger biophysical systems perspective.

Natural gas is a mixed story. The decline in tight oil production will decrease gas supply but exports will evaporate adding 5 bcc/d back into domestic supply. Electric power and space heating demand is less elastic than other forms of energy consumption but with so many businesses closed and closing, the electric power future is unclear to me for now.

All the best,

Art

Thank you Art. A very good observation on Nat Gas exports (unless there are some fixed contracts?). If 5 bcfd remains in US, oversupply will persist longer than 2020 I’d think.

Another great piece and I’m glad to see you in touch with Nate Hagens on it. You are both ‘heroes’ in my book for your enlightened ways of analyzing and presenting energy data and extrapolating that to the broader economic/societal impact. Personally, I’m getting very interested in natural gas supply/demand. With natural gas supply still predominantly confined to US/Canada (LNG largely irrelevant at <$3/MMBtu IMO), I believe that natural gas supply will run short long before oil. But I may be underestimating the decline in demand if industrial use will remain depressed by social distancing? Will appreciate any data/thoughts you have on this. Thank you!

Thank you very much for your answer Art.

All the best,

Olivier

Thanks for the article. About all the the shale oil “revolution” has given the world is some oversized executive bonuses for incompetent executives and fees for wall street to sell overpriced junk bonds to gullible investors. This is in return for massive capital and environmental destruction.

It would be worthwhile to do an analysis of what the impact of coming bond defaults by shale oil companies will be on the broader financial system. One would think that this impact would be large enough to trigger a financial crisis in itself, notwithstanding the broader impact of the virus.

David,

Total shale debt maturing in 2020-2026 is approximately $133 billion. Assuming all of it defaults (I doubt more than 30% will), that would be equivalent to about 1.5 AIG bailouts in 2008-2009. I doubt that would be enough to trigger an economic collapse.

All the best,

Art

Hi Art,

Thank you very much for all the content and insights you’re providing. I agree with you views.

I would like to have your opinion, if demand rebounds after the coronavirus crisis, on possible oil supply crunch(es) before 2025 in Europe (as mentioned in the 2018 iea’s report). Matthieu Auzanneau (author of oil power and war, a dark history) says that 50% of Europe’s oil suppliers are threatened by structural decline (see the chart at the end of his article).

You will find his (and iea’s) views in this article (I hope you can translate it).

https://www.lemonde.fr/blog/petrole/2019/02/04/pic-petrolier-probable-dici-a-2025-selon-lagence-internationale-de-lenergie/

Thank you in advance for your answer.

Best regards,

Olivier

Olivier,

Thank you for your comments and question.

My French is decent. I do not agree with Auzanneau’s analysis. His opinion is dated in early 2019 and he, like most analysts, failed to understand the profound implications of the late 2018 oil-price collapse. This was a signal to producers to reduce output. Lower production rates only lasted a few months and then increased again. The present price collapse would not have been as profound without the CoV-19 crisis but was inevitable nonetheless. I anticipate low prices and ample supply for several years.

All the best,

Art