Art Berman Newsletter: February 2020 (2020-1)

Coronavirus is Crushing Oil Prices

On February 11, I predicted that Coronavirus would crush oil prices. Prices collapsed on February 20. Today, prices have reversed and are more than $2.00 higher on expectations of an OPEC+ production cut and central bank stimulus. These themes plus rising and falling sentiment about Coronavirus will be the framework for the rest of 2020.

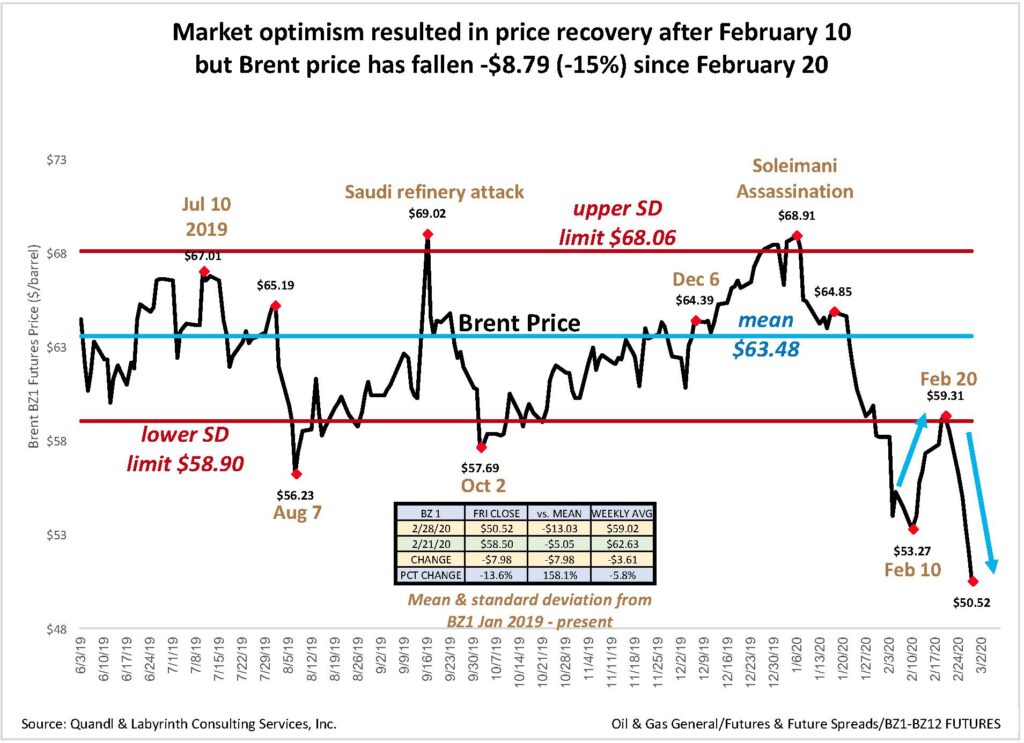

As of last Friday, WTI prices had fallen 27% and Brent had fallen 15% since late December. Oil price is being devalued despite today’s gains. Most of this is because of lower demand expectations and disruption of supply chains from Coronavirus (Covid-19). For those who think that devaluation or the effects of the virus will soon be memories, think again.

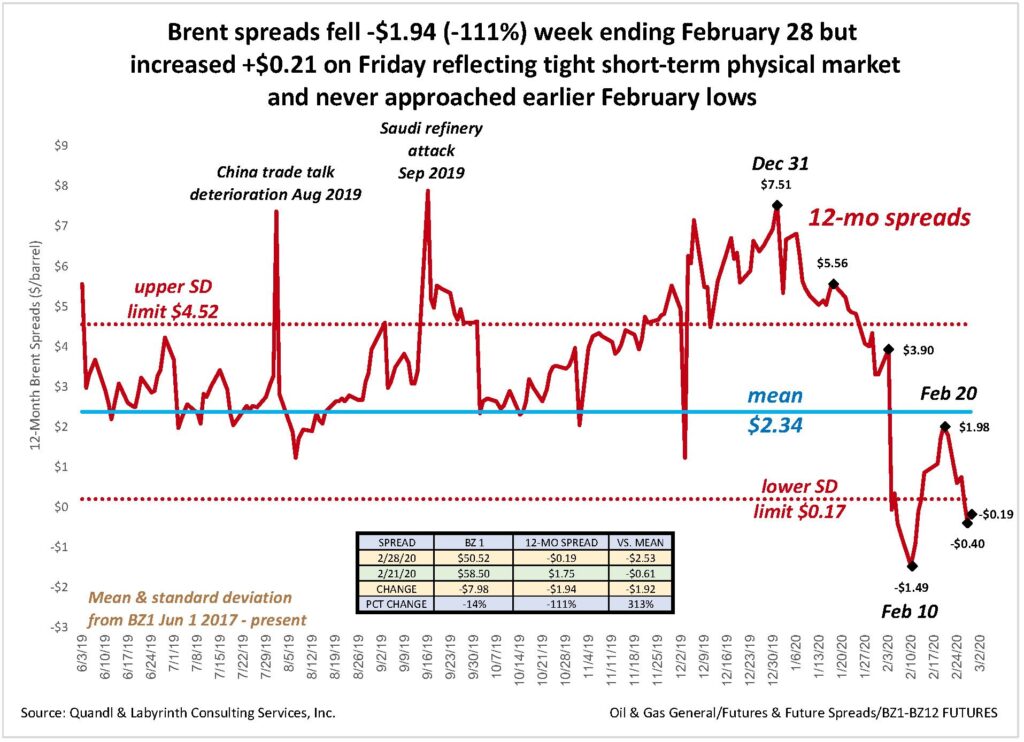

The severity of the market’s view is shown most clearly in Brent 12-month futures spreads. The collapse of spreads in January and February is more drastic than previous price collapses in 2014 and 2018 (Figure 1). In 2020, spreads fell from $7.94 to zero in 34 days for a decline rate of $0.23 per day. That rate is 1.5 times greater than it was in 2014 and 1.8 times greater than in 2018.

The optimistic rebound of price (Figure 2) during the week ending February 14 was short-lived and turned to capitulation the following week. WTI price dropped $8.62 and Brent fell $7.98.

Source: Quandl and Labyrinth Consulting Services, Inc.

At the same time, spreads often more accurately reflect the perspective of experienced traders. Brent 12-month spreads did not approach the low levels of February 6 to 11, and actually moved slightly higher on the last day of trading at this writing (Figure 3).

Markets seem to be reflecting two contrasting themes . Prices are collapsing but spreads are indicating that the worst effects of the Coronavirus on oil markets may be past, at least for now. I doubt that but if true, we are seeing the effect of normal price discovery.

As consensus builds toward Coronavirus apocalypse, short-term oil traders can easily find counter-parties to take the other side of a bet that prices will probably improve over the term of a contract. This pushes prompt contract prices down. Meanwhile, longer-term players may be able to see their way clear to an upturn in prices later in 2020 or in 2021, hence the slightly less pessimistic picture from futures spreads.

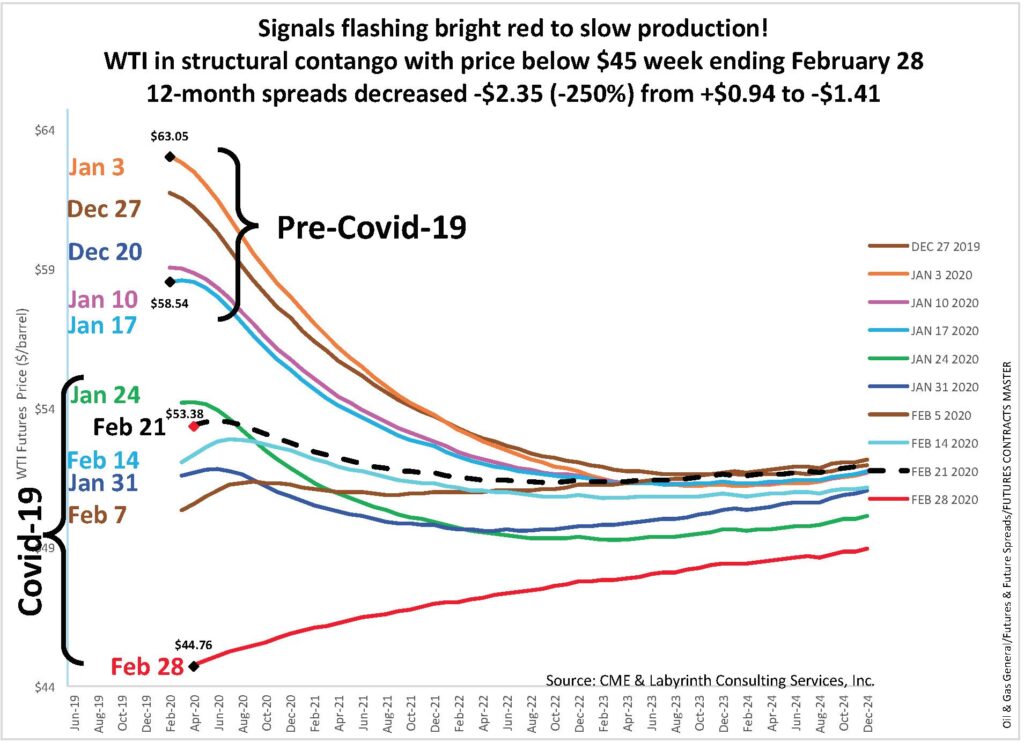

This duality is also expressed in the forward curves of WTI and Brent futures. The term structure of WTI forward curves has gone through the full spectrum from structural backwardation in December and early January to full structural contango by late February (Figure 4). This is a strong signal to U.S. companies to slow or stop production. Contango generally means that markets anticipate an over-supply. It accordingly provides incentive to store rather than to sell oil since it is worth more in the future than it is today.

Source: CME and Labyrinth Consulting Services, Inc.

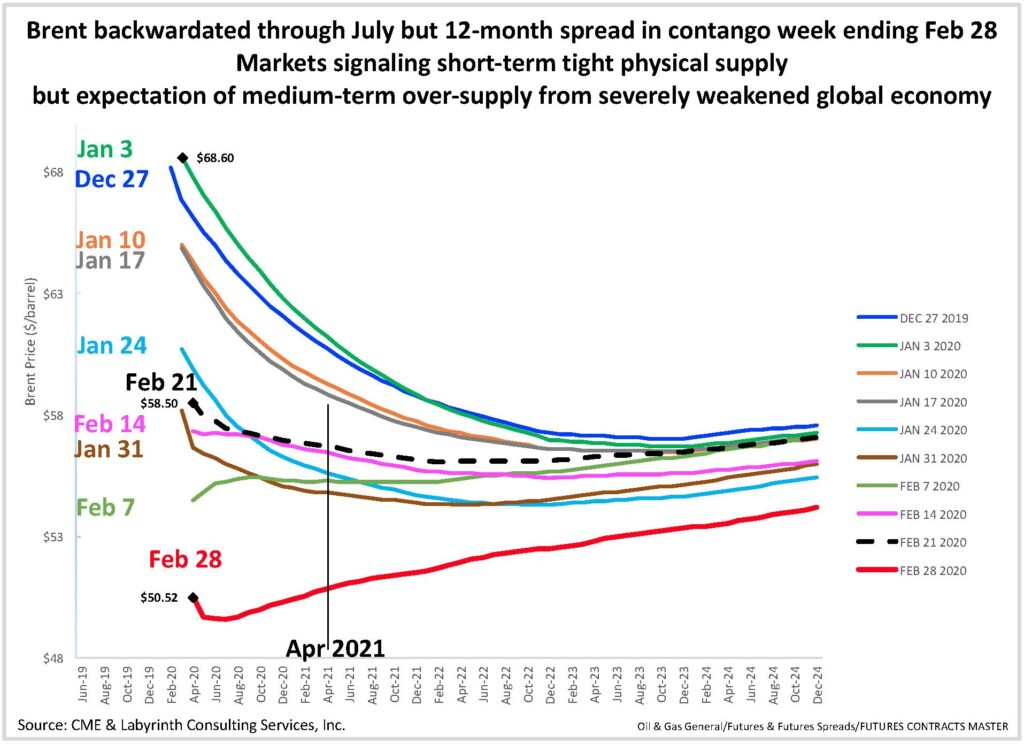

Brent forward curves present a somewhat different perspective. Brent is backwardated through July 2020 but the term structure beyond July was in contango (Figure 5). That suggests that markets see short-term tight supply followed by over-supply. It is worth noting that there is very little liquidity beyond a year and 12-month contango is weak (-$0.19). By contrast, WTI 12-month contango is -$1.41.

Source: CME and Labyrinth Consulting Services, Inc.

Same Trailer, Different Park

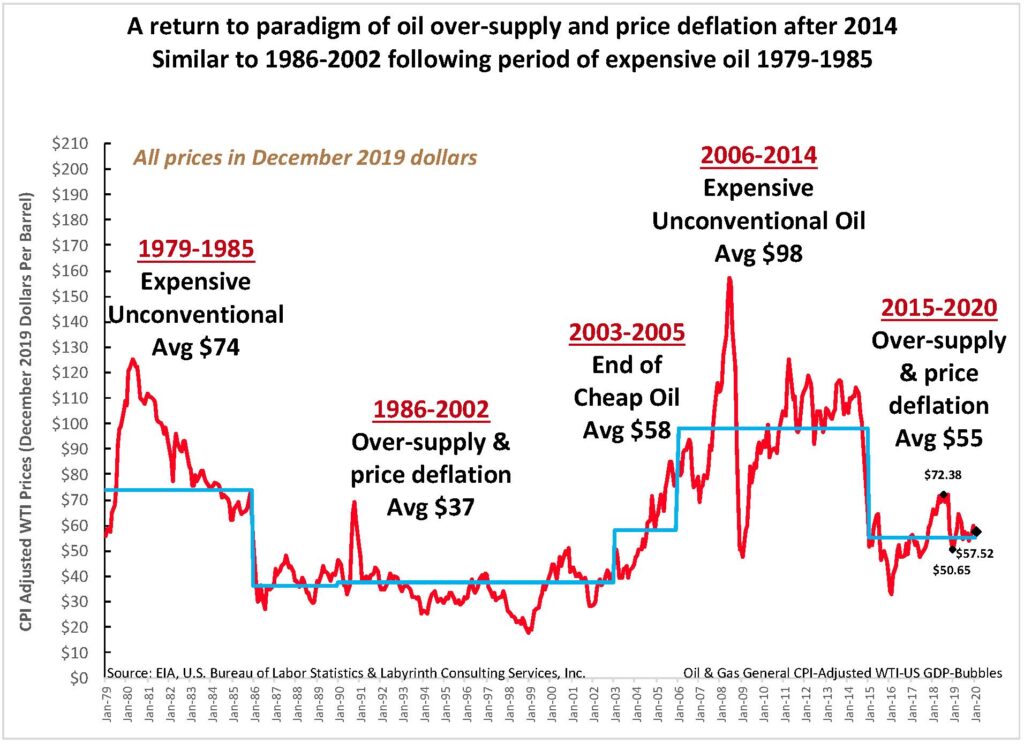

Supply deficits and expensive oil for most of the first decade and-a-half of this century have given way to surpluses and lower price over the last 5 years. Oil markets have struggled to adjust to the return of the old paradigm of over-supply and price deflation since mid-2014 (Figure 6).

This is the second showing of the same movie that opened after the oil shocks of 1979 to 1985. Higher prices provided incentive for producers to find new supply in places like the North Sea, Siberia and Mexico. The resulting supply surplus that followed caused low oil prices for the next 20 years.

Source: EIA, U.S. Bureau of Labor Statistics and Labyrinth Consulting Services, Inc.

As new fields depleted, higher prices again provided incentive to develop new supply, this time in the unconventional tight oil and oil sand plays of North America. Surpluses led to price deflation in 2014, just as they had 30 years earlier. Same trailer, different park.

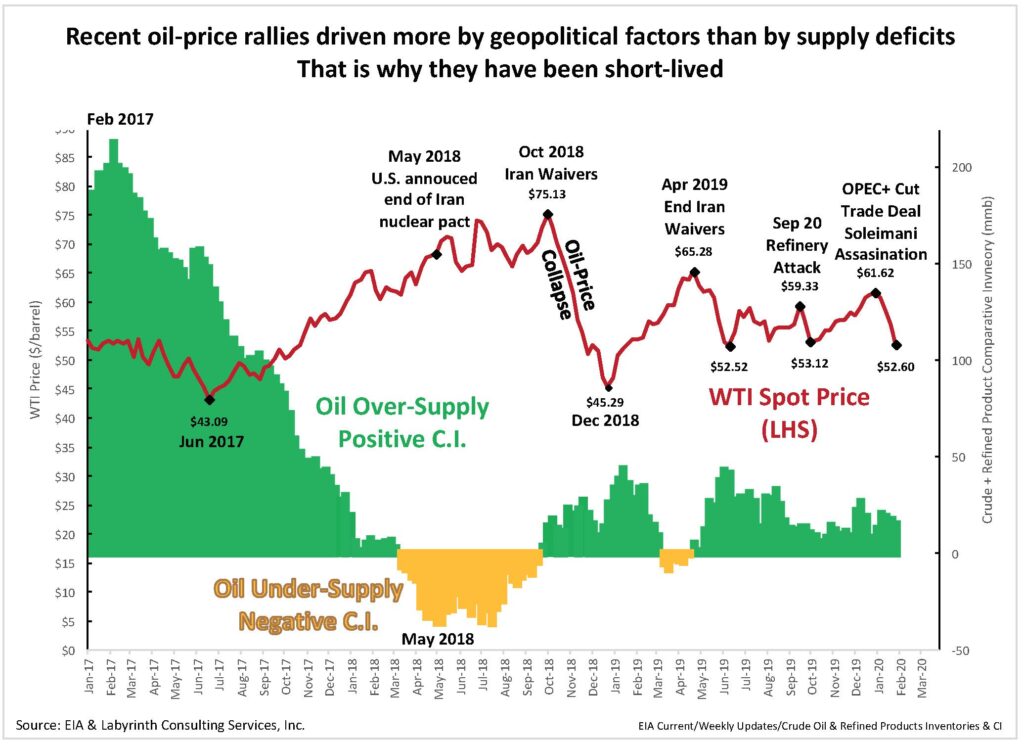

Markets are people and so they are slow to accept change. After the highest oil prices in history from 2006-2014, many assumed that this was the norm and that lower prices were a temporary adjustment. That did not happen but by May of 2018, supply deficits finally returned (Figure 7). At the same time, the United States announced it would withdraw from the Iran nuclear pact and put oil-export sanctions on Iran.

Source: EIA and Labyrinth Consulting Services, Inc.

Prices rose to the highest levels since 2014 and some analysts predicted $90 oil prices by the end of 2018. When the U.S. granted export waivers in October, prices collapsed. Since then, three successive price rallies have failed to approach October levels. That is because these rallies have been chiefly driven by geopolitical factors that were not supported by supply-demand fundamentals.

The most recent rally required three concurrent geopolitical events—a new OPEC+ production cut, a U.S.-China trade deal and the assassination of Iranian General Soleimani. Still, WTI did not reach $62.

How This May End

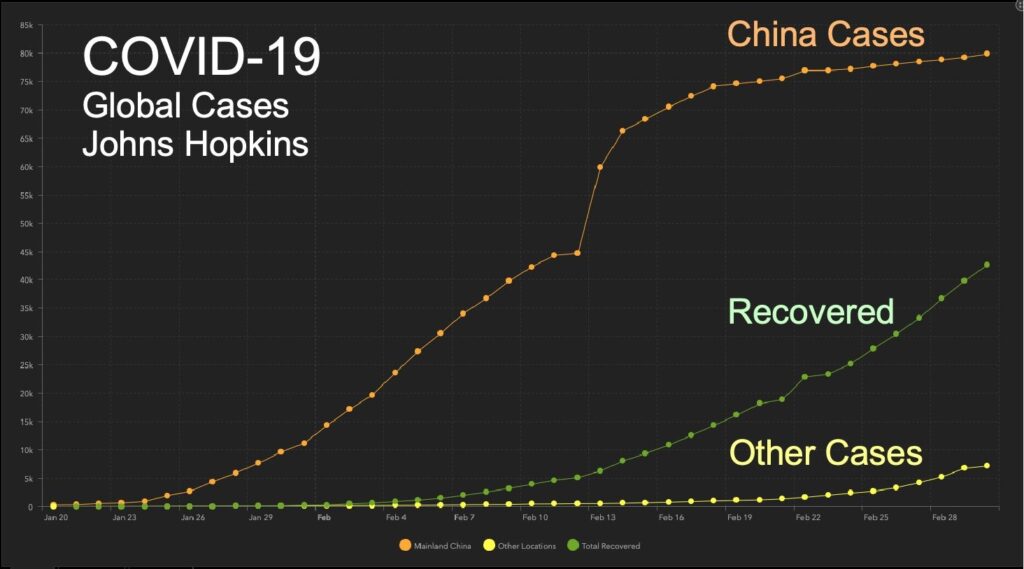

While the news about Coronavirus and its effect on oil markets is bad, there are some hopeful elements that may explain how markets are reacting now. Figure 8 shows that the number of cases in China appears to be leveling off and that people who have recovered is increasing. The scale of the chart under-states the expansion of cases outside of China. Still, the data suggests that fears of an apocalyptic pandemic may be exaggerated.

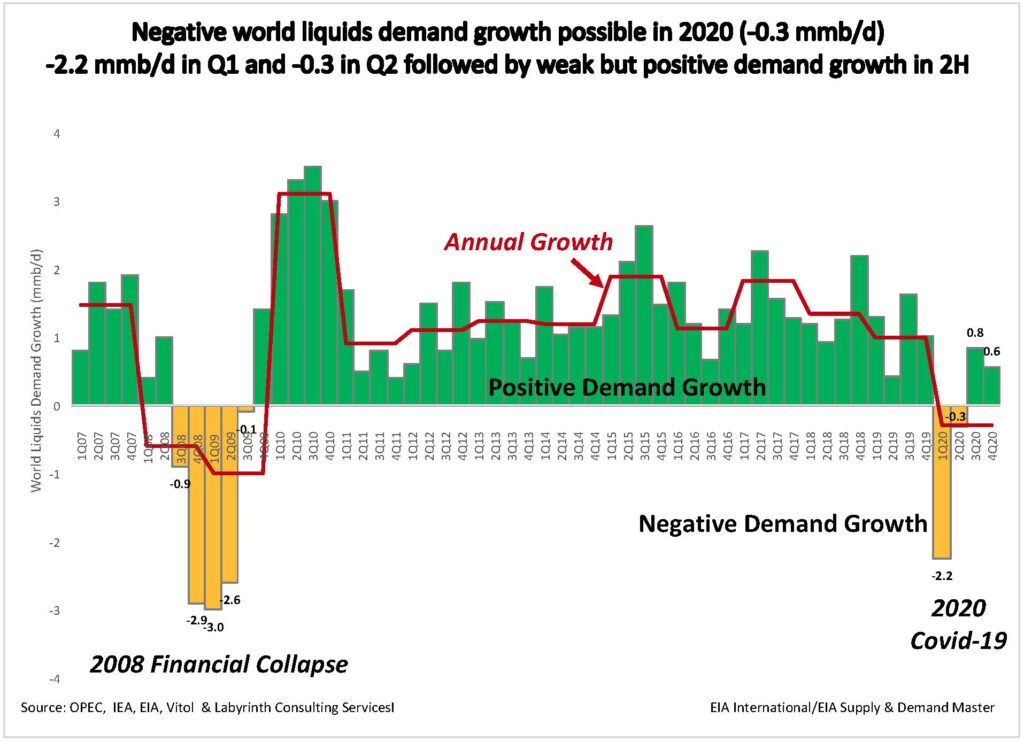

This does not mean that oil prices will recover soon or that Coronavirus will be a distant memory by mid-year. In fact, negative world demand growth is likely for 2020 (Figure 9). This optimistically assumes that only demand from China is affected and that a decrease of 200 million barrels for the first quarter is followed by recovery in the rest of 2020.

Source: OPEC, EIA, Vitol and Labyrinth Consulting Services, Inc.

That would result in the first quarter of negative demand growth since the 2008 Financial Collapse and the first year of negative demand growth since 2009. The “knock-on” effects of broken supply chains and demand destruction outside of China would result in an even more pessimistic, if more probable, forecast. In either case, it is unlikely that oil prices will recover substantially from current levels in 2020 or that Coronavirus will become a distant memory.

The near term is anyone’s guess at the moment but it is probable that the panic will be worse than the pandemic. I can imagine a scenario in which prices continue to fall from current levels but start to stabilze. This could begin as soon as early March.

Comparative inventory suggests than the current WTI front-month price of about $45 is under-valued by at least $8 per barrel. I don’t believe that sentiment alone is responsible for this. Markets are assuming a substantial inventory build once lower demand begins to affect shipments at least for U.S. stocks. The price is still under-valued because inventory build will probably be more gradual than price anticipates.

I can also imagine a scenario in which panic drags near-term prices into the $30 range. That would probably not be sustainable for more than a few months but a lot depends on reduced global demand for all products because of Coronavirus.

Whatever the short term brings, WTI prices should stabilize as the emerging effect of Coronavirus on oil markets and the economy becomes clearer. This may not happen, however, in 2020. Until then, prices will rise and fall on daily news that is either more or less hopeful about the impact of Coronavirus on demand and supply chains. The world economy and oil markets will probably be in a period of flux may last for 18 months or longer before prices begin a long journey back to 2019 levels.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts