Coronavirus Will Crush Oil Prices

Oil is being devalued. Prices have fallen 20% since early January on lower demand expectations because of Coronavirus. For those who think that devaluation or the effects of the virus will soon be memories, think again.

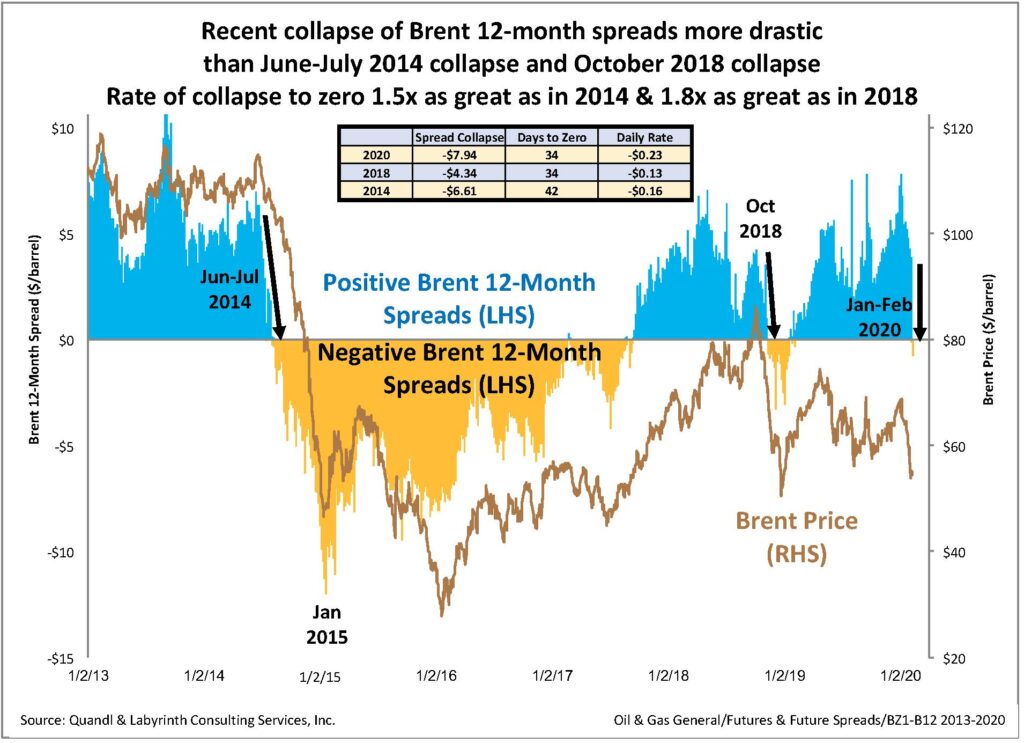

The severity of the market’s view is shown most clearly in Brent 12-month futures spreads. The collapse of spreads in January and February is more drastic than previous price collapses in 2014 and 2018 (Figure 1). In 2020, spreads fell from $7.94 to zero in 34 days for a decline rate of $0.23 per day. That rate is 1.5 times greater than it was in 2014 and 1.8 times greater than in 2018.

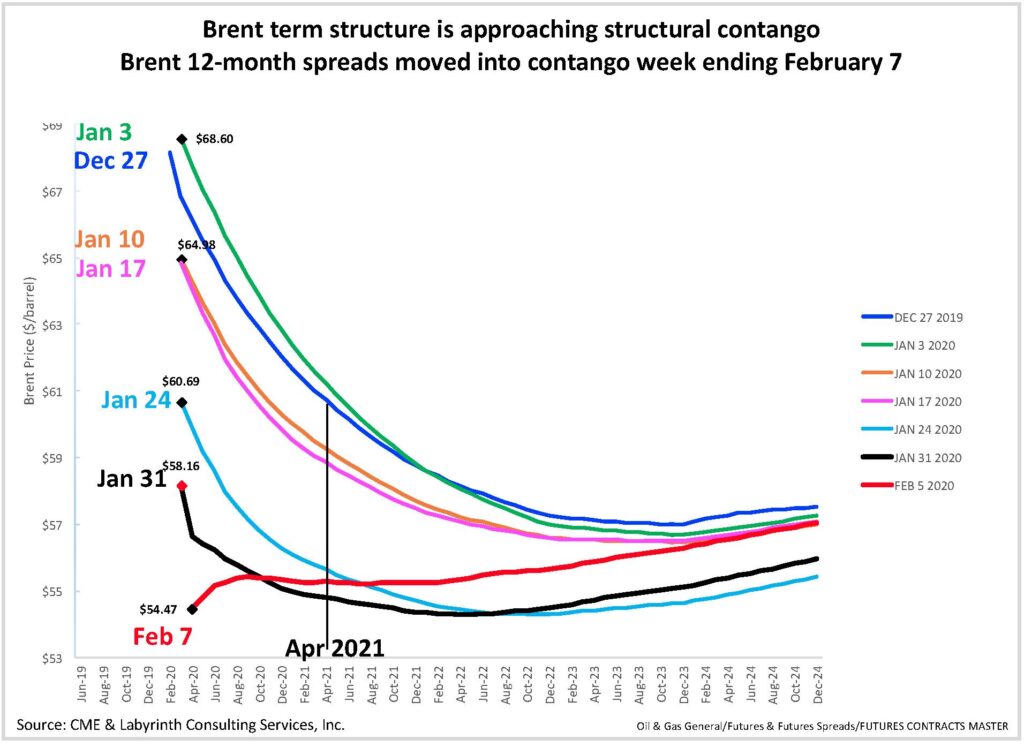

The term structure for the February 7 Brent forward curve is approaching structural contango (Figure 2). Forward curves have been in backwardation since early February 2019 but moved into contango last week. As recently as January 31, Brent was in steep prompt-month backwardation ($1.54) and in backwardation through May, 2022. The February 7 curve was in 5-month contango.

Source: CME and Labyrinth Consulting Services, Inc.

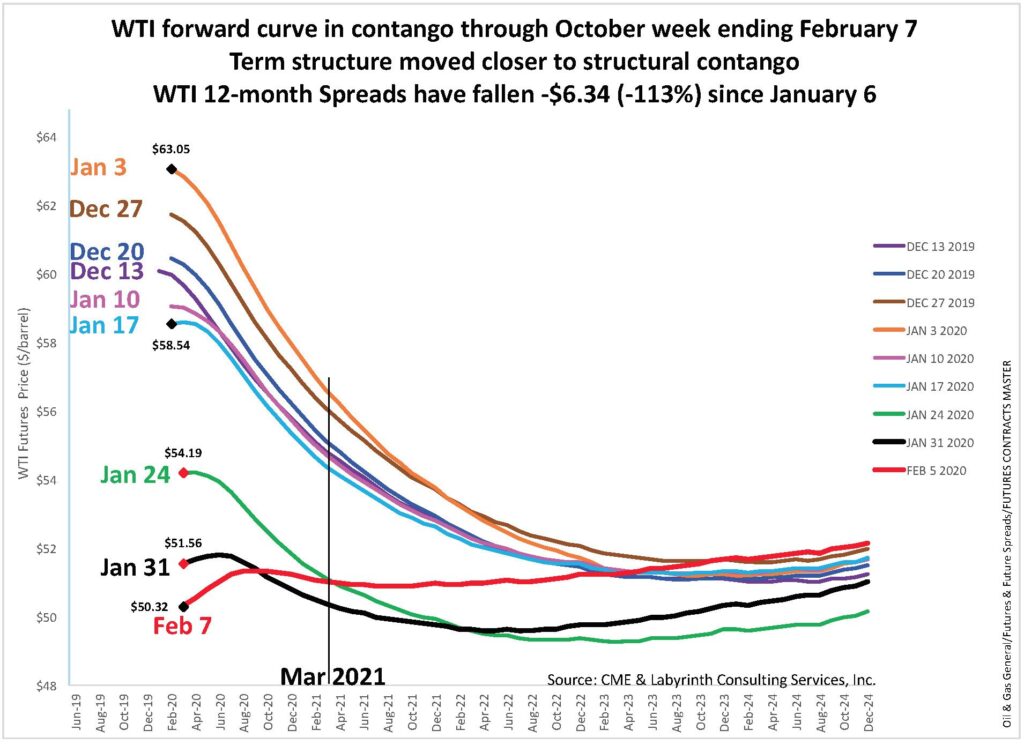

The WTI forward curve presents an even more pessimistic view. WTI is in contango through October 2020 (Figure 3). 12-month spreads have fallen $6.34 (-113%) since January 6,

Source: CME and Labyrinth Consulting Services, Inc.

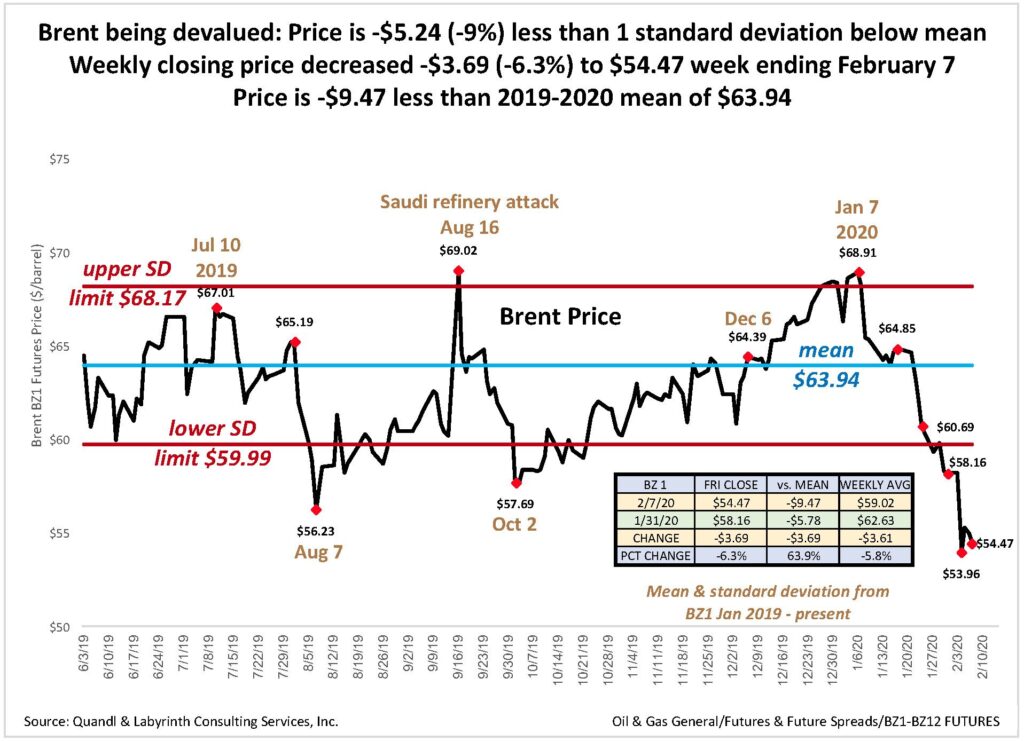

Brent devaluation may be occurring (Figure 4). Last Friday’s closing price of $54.47 was $5.24 less than one standard deviation below the 2019-2020 mean price. It was $9.47 less than the mean price of $63.94.

Source: Quandl and Labyrinth Consulting Services, Inc.

Same Trailer, Different Park

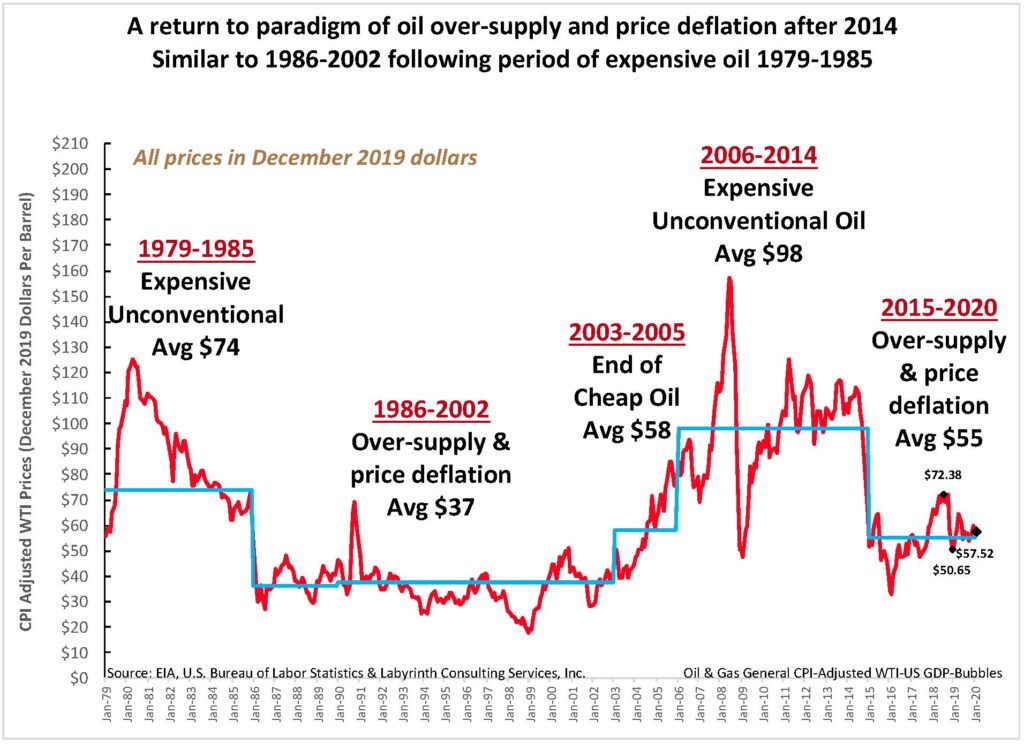

Supply deficits and expensive oil for most of the first decade and-a-half of this century have given way to surpluses and lower price over the last 5 years. Oil markets have struggled to adjust to the return of the old paradigm of over-supply and price deflation since mid-2014 (Figure 5).

This is the second showing of the same movie that opened after the oil shocks of 1979 to 1985. Higher prices provided incentive for producers to find new supply in places like the North Sea, Siberia and Mexico. The resulting supply surplus that followed caused low oil prices for the next 20 years.

Source: EIA, Bureau of Labor Statistics and Labyrinth Consulting Services, Inc.

As new fields depleted, higher prices again provided incentive to develop new supply, this time in the unconventional tight oil and oil sand plays of North America. Surpluses led to price deflation in 2014, just as they had 30 years earlier. Same trailer, different park.

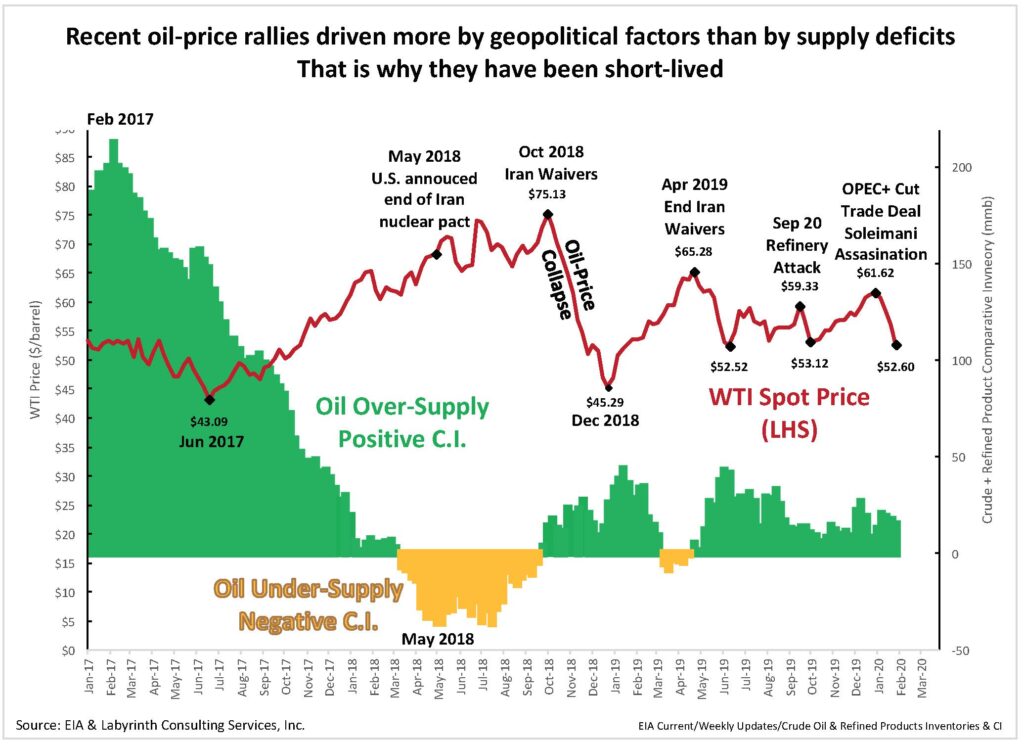

Markets are people and so they are slow to accept change. After the highest oil prices in history from 2006-2014, many assumed that this was the norm and that lower prices were a temporary adjustment. That did not happen but by May of 2018, supply deficits finally returned (Figure 6). At the same time, the United States announced it would withdraw from the Iran nuclear pact and put oil-export sanctions on Iran.

Source: EIA and Labyrinth Consulting Services, Inc.

Prices rose to the highest levels since 2014 and some analysts predicted $90 oil prices by the end of 2018. When the U.S. granted export waivers in October, prices collapsed. Since then, three successive price rallies have failed to approach October levels. That is because these rallies have been chiefly driven by geopolitical factors that were not supported by supply-demand fundamentals.

The most recent rally required three concurrent geopolitical events—a new OPEC+ production cut, a U.S.-China trade deal and the assassination of Iranian General Soleimani. Still, WTI did not reach $62.

Coronavirus Will Crush Oil Prices

In December, I predicted that higher prices would not last and in fact, the rally failed in the first week of 2020. Then, news of the Coronavirus in China began to dominate market sentiment. The result has been a 20% decline in oil prices. So far, broader markets seem largely unaffected. I do not take comfort in that because oil is commonly a bellwether. Energy is the economy.

Predictions and opinions about Coronavirus are largely useless because the reality is that no one knows enough to make predictions yet. Comparison to the SARS epidemic in 2003 is interesting but only marginally relevant. SARS was also a coronavirus but it was transmitted by person-to-person contact. The latest version is airborne and that changes everything.

SARS occurred when China was a $2 trillion economy. Now it is a $14 trillion economy. Chinese oil consumption is 7 times what it was in 2003. Global supply chains are much more complex and integrated today and China is central to all of them.

Oil prices rise and fall on daily news that is either more or less hopeful about containment and death rates. It is not contained and death rates are a total guess at the moment.

Markets seem to be assuming that Coronavirus is an Asian phenomenon. It is not and will unavoidably become a global problem. Markets will respond quite differently once this is understood. A major sell-off in broader markets seems almost certain.

Chinese efforts at containment are unparalleled and unimaginable in less autocratic countries. So far, it is unclear that containment progress has been made. Some argue that healthcare infrastructure is better in North America and Europe than it is in China. That may be but whatever facilities exist will likely be overwhelmed in short order.

I want to be optimistic but frankly cannot believe most of the information that passes government censorship. If a cure is found today, the effect of the disease on global markets will be severe. Since that is not the case, I have a hard time imagining an outcome that will not crush oil prices.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

[…] the Coronavirus outbreak became public. I wrote in early February that Coronavirus would crush oil prices. It did. The Saudi price cut in […]

[…] the Coronavirus outbreak became public. I wrote in early February that Coronavirus would crush oil prices. It did. The Saudi price cut in March […]

And I thought the numbers surrounding sports analytics could be a challenge. Hats off to you, sir. Found your site because I’m slowly working my way through CSPAN’s BookTV archives, as others might listen to radio. Listened to Greg Zuckerman’s 2014 presentation on his fracking book.

[…] February 11, I predicted that Coronavirus would crush oil costs. Prices collapsed on February 20. Today, costs have […]

[…] Mt (0.8em) – sm" type = "text" content = "On February 11th I & nbsp;predicted& nbsp; that corona virus would depress oil prices. Prices collapsed on February 20. Today […]

[…] 11. Februar habe ich vorhergesagt dass Coronavirus die Ölpreise drücken würde. Die Preise sind am 20. Februar zusammengebrochen. […]

[…] February 11, I predicted that Coronavirus would crush oil prices. Prices collapsed on February 20. Today, prices have […]

a real collapse in oil prices will put Saudi Arabia in a bad way as they cannot meet their budgetary needs at present prices. Also put the “tight oil” in the US out of business. We have a glut with Venezuela, Libya, Iran off and a demand drop will be a disaster. Oil could go to $10/bbl like in the late 80’s

Hi Art, Although “in writing”, I too am skeptical of Washington’s claims in light of the larger sale out of the reserve beginning in FY21, but it’s nonetheless one component in the demand equation we can’t overlook since we’re already pumping /exporting (and depleting) like mad. The rest of the energy producers must look at the US and laugh watching us deplete far smaller reserves than they have……..the party won’t last locally.

I also think the world’s largely over dramatized the effects of the current COVID-19 outbreak….relatively speaking (on the data) the US has managed to continue growing both liquids exports and GDP while experiencing far higher numbers of flu-related illnesses and deaths the past decade (below). Surprisingly, hospitalization rates have remained relatively constant across all strains over time and COVID-19 mortality rates are considerably below other corona viruses (e.g. SARS, MERS, etc)

https://www.cdc.gov/flu/about/burden/index.html

China has experienced much higher numbers of flu cases (historically) than the US (their reporting mechanisms are doctored, incomplete, frankly falsified like everything in country) but continues its insatiable demand for energy – exceeding 10m/bpd and on trend to go to 13m/bpd in spite of current COVID-19 related imports / usage reductions of around 3m/bpd which I believe will persist through the next 2-3 quarters. Much is unknown about COVID-19 but its transmission mechanisms (e.g. droplets, surfaces) appear similar to SARS so I’m not so sure it’s the “super bug” most claim. Some of the hysteria with COVID-19 is China’s newly instituted reporting / govt data intervention from their earlier egg on their face SARS episodes…..my guess is they’ll revisit these new reporting protocols, likely “tamp them down” in the future.

Ultimately, helicopter money and negative interest rates ($25T globally is earning neg interest), the race to debase currencies around the globe are forces that will counter longer term any near term COVID-19 demand effects. The USD is awfully stretched right now and all of us know its correlation to energy prices.

VR/ Francis

Francis,

I believe the converse namely, that the world has under-dramatized the potential effect of COVID-19.

Best,

Art

Totally with you, Ari. Heard of you from macro voices, and thought you sounded like you had integrity. This website and your interaction with posts proves me right. I think it’s pretty brave to publicly put out an opinion like this without hiding it in various other base cases; although, I honestly wish the consequences weren’t so dire.

Long Long Term I also agree with you too Francis. The money supply will be a huge factor when it’s actually released into the economy. But that’s a big when which the world CBs moving in unison. In the immediate future, the demand will fall when people simply aren’t getting on flights, or working at all (GDP is closely related to energy usage). No amount of stimulus can counter people literally staying at home.

This virus seems to be staggeringly infective even after the precaustions taken by the Chinese. When this goes to EM, they’ll have no way to close it down. Whats more, there are reports that being infected a second time by it is even worse for you. A vaccine that can be deployed is the variable that changes everything but we’re talking up to a year for all the research to be done. I’ve see that plasma (blood) from previously infected patients is helping. That could be difficult implement. I’ll agree in the grand-scheme, this isn’t so bad: the death rate isn’t that much. BUT, global governments will have to shut down to combat this anyway. Imagine trying to stay in power after you’ve just calmly accepted that 0.5-2% of your whole population (incredibly infective) is OK to die.

Shut down = no demand = bad for oil. That’s even not considering how cheap LNG is now and how it’s potential for substituting oil on various levels.

I don’t believe we can trust any so-called data on Covid-19 except in a notional way. Notionally, I expect it to reach some kind of maximum in China over the next month or so. The real issue is how the world reacts when it is no longer a China problem. I am concerned about lives and health, of course, but I suspect the larger effect will be from the fear and mistrust the virus engenders. The global credit system is fragile.

All the best,

Art

One area that will serve as a backstop on WTI pricing is the Phase 1 US China Agreement that calls for China to purchase $52B in US liquids, gas etc

Francis,

That target was shown to be improbable before the Coronavirus outbreak. Wasn’t a backstop before and clearly not since.

All the best,

Art

Thanks Art! I “feel” same things and you give me basement for them. Looks that actual mortality is about 50k in China now …

Will.

Thanks for your comment, Will.

Art

Art, excellent write up. You risk analysis is admirable. Many people, particularly those who underestimated the impact of this virus and now have positions stuck, are really repressing the virus’s pandemic potential. The broad market itself is as well. The market roars louder as if no virus was present at all.

We know quite certainly from multiple sources of the real severity of this virus and yet no one takes them seriously. The Chinese data is 99% false. Not a surprise from a totalitarian state. Chances are, infection rates are super high, death rates are way higher than reported. We will know exact numbers with international cases increasing by the day and legitimate data is released.

Many technical analysts predicting this is the bottom for oil and we will see a reversal, I disagree. A drop to $42 is imminent the moment global clusters begin to emerge. The previous lows are already breached and buying right now would be very risky and irresposnible.

Thanks for being one of the first experts I’ve read to actually give an unbiased and risk-oriented analysis on the current state of oil.

Cheers

Chris

Chris,

Many thanks for your comments. I wish that I could disagree but I see things the same way. Why would anyone believe the data coming from China? If it were happening in the U.S., I doubt the truth would be published.

People clearly are in denial to the point of delusion about how bad this could be.

I hope that we are both wrong.

Best,

Art

The mortality rate is only 2% but that has to be discounted by the fact the first wave of patients is getting first class care. Once the number of serious cases exceeds the available medical support infrastructure, obviously the mortality rate goes up.

But so far, containment seems to be working. However, if this virus were to get loose in India or Africa, then all bets would be off.

The rate of new cases is declining steadily so possibly there is reason for optimism.

John,

As I stated in my post, I have little faith in government reporting on this (any government) so containment seems speculative at best as does mortality. I see no possibility that it will not spread outside of East Asia so we are back to my premise: we really know nothing useful about this virus except that it is real and that China is taking it very seriously.

All the best,

Art

Thanks for this detailed in numbers and in time post, Mr. Berman!

I just came across some of your work. It’s opening my mind about the oil market. Since I am a beginner in this market, I would just like to check if I got all the points right. It seems that you foresee higher oil prices on a long term basis and lower oil prices on short term. Is that right? I came to that conclusion reading some posts and tweets of yours. Does that make any sense?

Sergio,

That is basically correct depending on how long and short long-term and short-term are defined. I suspect that Coronavirus could affect the short term for as much as a year or more. It really depends on mortality rates. I have seen credible models that suggest that 1 billion people might die. I hope that’s wrong but obviously, that outcome would affect oil prices for a long time.

Best,

Art

Art,

Thank you for the great work as always. Energy markets have at least begun to discount the impact unlike equities.

Initial narratives (seasonal flu) are a hard thing to shake. By the time the world economy realizes e impact, I wouldn’t be surprise the negative price discovery land WTI in the low 30’s.

It’s surprising that a post like this may indeed very contrarian right now. A contagious deflationary demand shock has crippled the world’s second largest economy and I’m afraid the worst is yet to come.

Alex,

I agree. Denial and delusion are important components of human psychology.

Best,

Art

Next week or two will tell, should be seeing gestation period ending on many worldwide cases that are under the radar. Freakout soon? Very convenient timing of a worldwide pandemic to coincide with the restructuring of the world economy, ala end of Breton Woods and the big looming financial crisis we’ve continuously put off.

I prefer to be optimistic but see little reason for it right now except hope.

Art

Thanks for this detailed in numbers and in time post, Mr. Berman!

The last MacroVoices podcast with you was also great!

Thanks!

Art

Two issues to consider about the new virus. First warm weather maybe a multimonth respite. Second the race to a vaccine is accelerating using new technologies like CRISPR.

I think we should consider two alternatives about the impact of the virus – the first that Art is suggesting that has a dire near term outlook which would indeed crush all markets. The second scenario would be a gentler outcome about containing the virus enough to give breathing room for the world to find vaccines and stop uncontrolled global spread.

Ganesh, I hope that you are right but it is difficult for me to be optimistic about things that might happen vs things that have already happened and are still happening.

Best,

Art