The Iran Card Played Again: Is It Enough to Move Oil Prices Higher?

The oil price rally got a big boost last week with the assassination of the Iranian General Qassem Soleimani. Will that be enough for prices to continue increasing or will they flatten and decline in coming weeks?

Markets are presently engaged in “fear premium” price discovery. So far, the fear premium is modest. At this writing, WTI is $63.56, $0.51 higher than its close of $63.71 on Friday; Brent is $0.71 higher at $69.31.

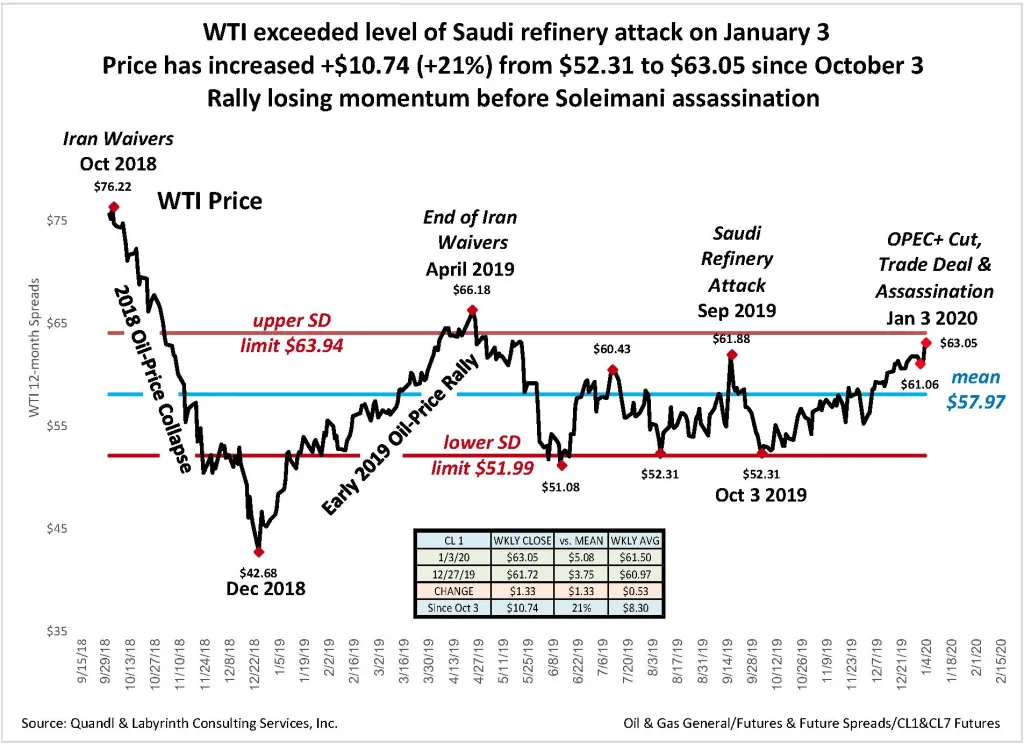

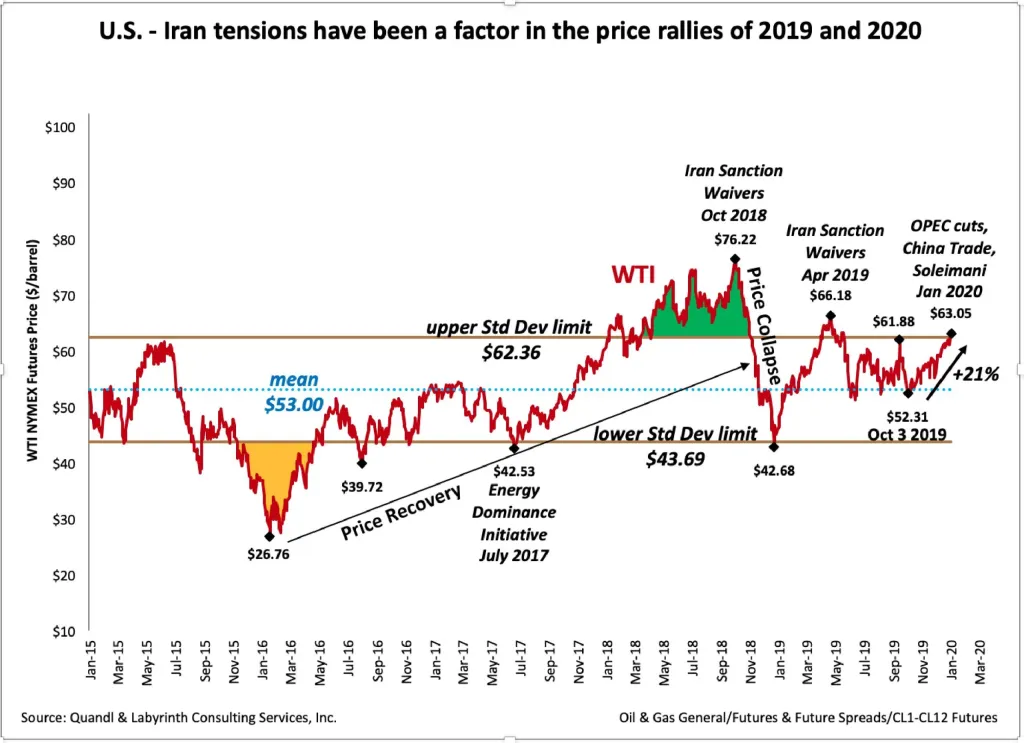

WTI prices have increased 21% since early October (Figure 1) exceeding the $62 level of the September Saudi refinery attacks.

Previous 2019 rallies reached similar levels before failing. That is because they were based mostly on expectations of supply constraints and not on actual market tightness. When the reason for that expectation disappeared, prices fell. The latest rally probably represents more of the same.

It has required more substance to continue than previous surges. Markets are wary and needed something more tangible than possibility. In late November, a new OPEC+ production cut and a U.S. China trade pact provided the jab and the cross within days of each other.

Just as the rally was losing momentum again, it got another boost when a U.S. drone killed Qassem Soleimani on January 3. The specter of war pushed WTI prices to a 9-month high.

There are two reasons why Soleimani’s death will probably not be enough to sustain the price rally for long unless open conflict with Iran occurs.

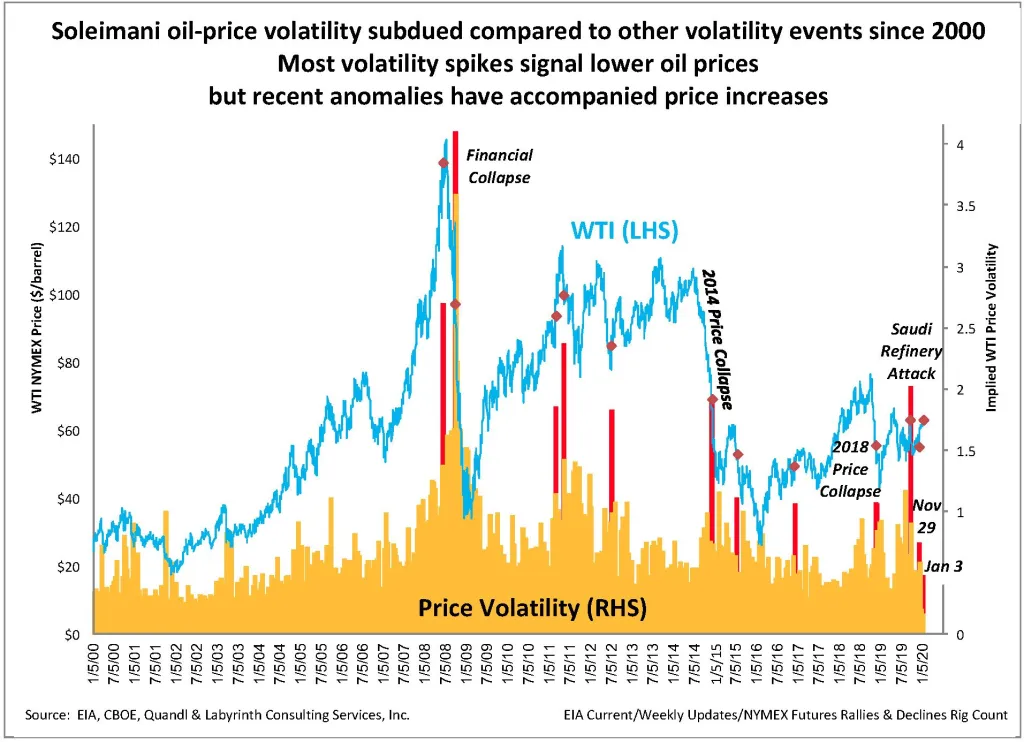

The first reason is implied volatility. Volatility is the degree of daily price variation, not the level of prices themselves. Implied volatility and oil price ordinarily correlate negatively: high volatility signals lower oil prices and conversely, low volatility characterizes periods of price increase. There are exceptions to this empirical observation.

Figure 2 shows implied oil-price volatility since 2000. The greatest volatility responses were from the 2008-2009 Financial Collapse, the Arab Spring uprisings in 2011, the oil-price collapse of 2014-2015 and the attack on Saudi oil refineries in September of last year.

Last week’s volatility was much less significant than those. It was also less significant than most smaller spikes over the last decade.

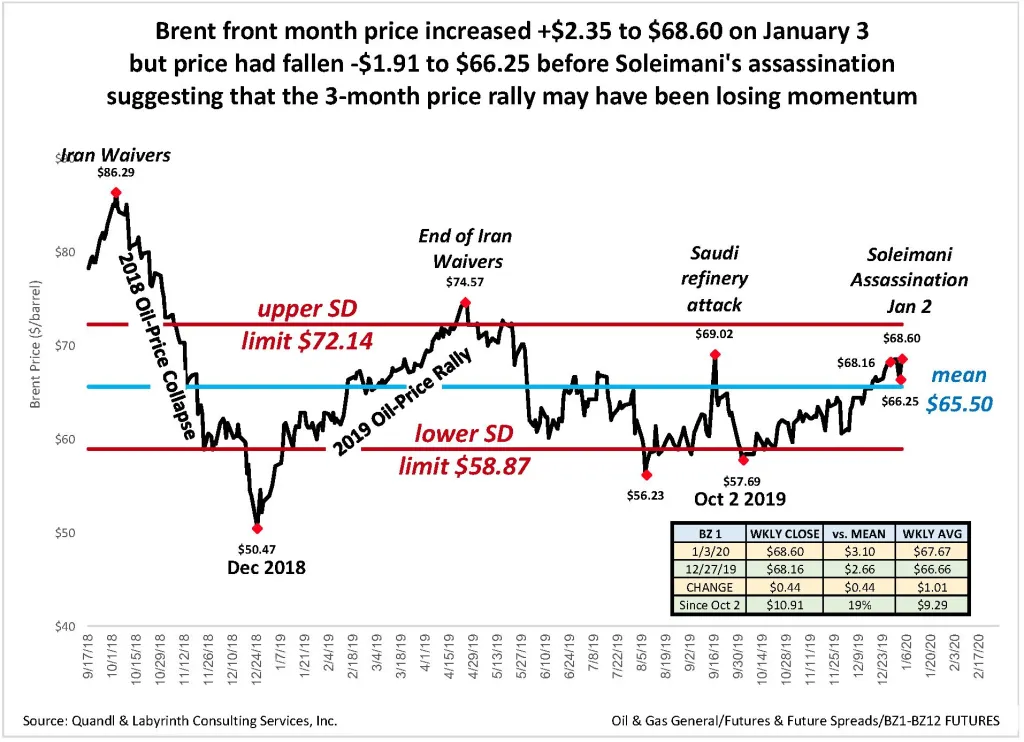

Brent front-month price increased +$2.35 to $68.60 on January 3 when the assassination was announced but it had fallen -$1.91 to $66.25 the week before (Figure 3). The 3-month price rally may have been losing momentum. Soleimani’s death merely adjusted the rally back to its earlier trajectory.

The second reason why this event may not have lasting effect on oil prices is that the resulting “fear premium” has been relatively small so far.

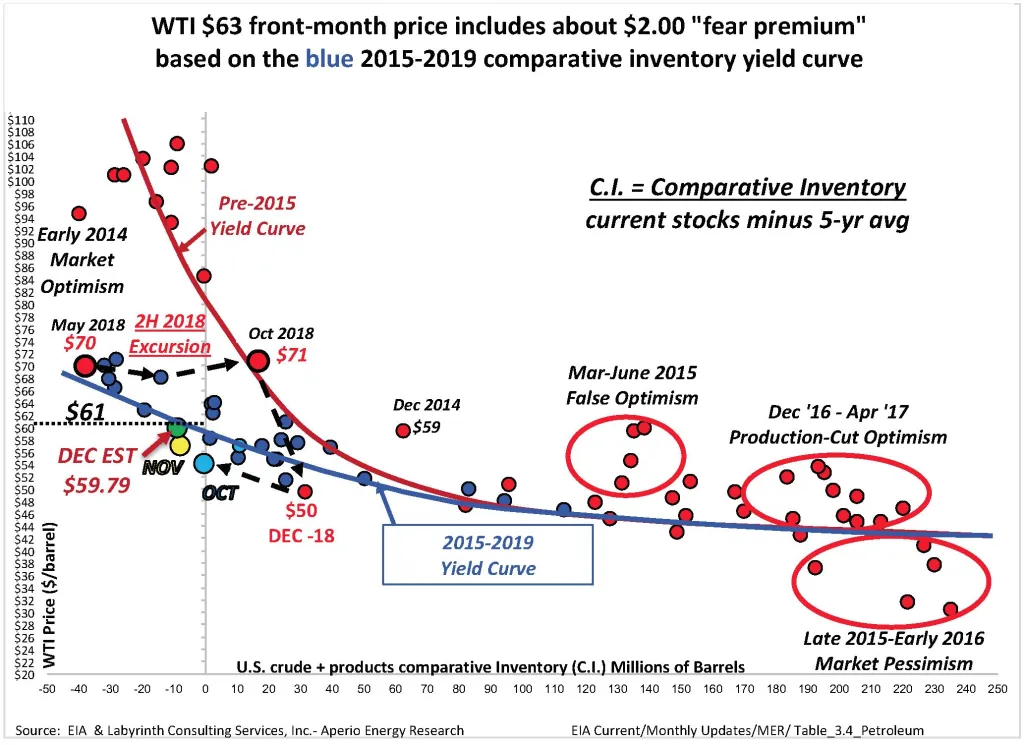

The latest price increase indicates only about a $2.50 WTI and $3.50 Brent “fear premium” based on comparative inventory data. Comparative inventory (C.I.) vs WTI spot price for December plots on the blue yield curve for 2015 through 2019 (Figure 4). This indicates that WTI should be approximately $61/barrel at that inventory level. The January 3 futures closing price of $63.04 was, therefore, only about $2.00-$2.50 over-valued.

The relatively flat slope to the yield curve reflects a low sense of supply urgency by oil markets. This is consistent with the limited price response a few months ago to attacks on Saudi oil refineries. That had an immediate effect on physical oil supply. There is no reason to expect that the more abstract potential for future supply loss from this event should have more effect on oil prices.

Low fear premium and price volatility suggest that markets probably do not consider Soleimani’s assassination a substantive cause for more than a temporary spike in oil prices.

And then there’s the Trump factor. The American president’s quarrel with Iran has been a key component in the three major oil-price rallies of 2019 and 2020.

His threat to block Iranian oil exports was the main reason for the April to October 2018 price increase (Figure 5). When he reneged and granted waivers, oil prices collapsed. The catastrophic investor losses because of this head-fake cannot be understated. Trump’s mood swings add uncertainty to an already risky market and are one of the main reasons that investment money has been on the side lines for oil.

Last week’s assassination of Soleimani marks the third time in less than two years that the Trump administration’s policy toward Iran has been a key factor in oil price rallies and failures. Markets have learned painfully that the American president’s bluster has faded in the fact of conflict.

Conflict might break out and, if it does, prices will surge. It is more likely that markets will revert to the proverb: Fool me once, shame on thee; fool me twice, shame on me.

We’re beyond twice.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts