Art Berman Newsletter: May 2020 (2020-4)

The Little Price Rally That Could

Last month I said that the current oil-price rally would end in tears. It hasn’t yet so let’s talk about why it hasn’t and why it still probably will.

U.S. producers shut in more production than most analysts believed possible and thus avoided full storage. That was a good thing that showed that the market may accomplish what people, companies and governments cannot.

The economy re-opened and increased economic activity rescued demand from the cellar. That was also a good thing again showing that markets cannot be constrained for long.

The OPEC+ production cuts that began on May 1 were deeper and more effective than most thought likely. That’s also a good thing because something drastic was needed in the face of the greatest demand destruction in history.

This rally began at the lowest real oil prices ever and has not yet reached the $40 threshold that comparative inventory indicates is the correct WTI price for present storage levels.

Oil Consumption Remains Low

The fact that the price rally has continued was the good news. The bad news is that there is little about the fundamentals of oil markets or the world economy that supports a continuation of rising oil prices.

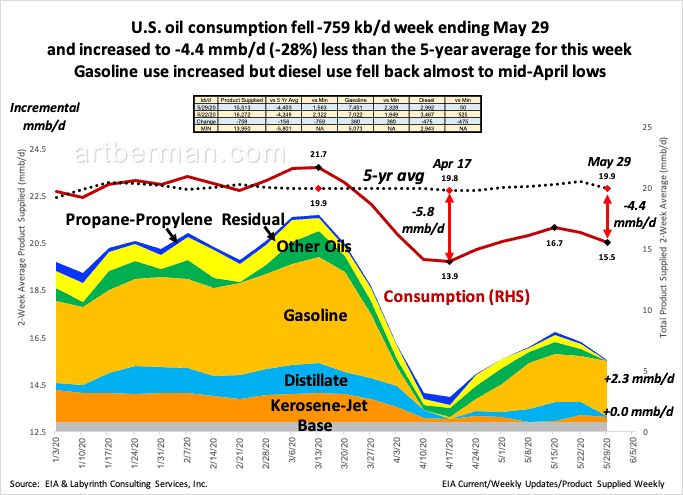

Oil consumption decreased for the second week in-a-row. It fell -759 kb/d and is now 4.4 mmb/d less than the 5-year average for this week (Figure 1).

It has recovered 1.6 mmb/d from the low point in mid-April. Gasoline use increased +380 kb/d last week but diesel use fell -475 kb/d almost back to its April minimum.

That is quite important because diesel use reflects the movement of manufactured goods by ships, trains and trucks. As such, it is a better gauge of economic recovery than gasoline consumption which merely reflects mobility; gasoline consumption does not necessarily mean that the economy is more productive.

and increased to -4.4 mmb/d (-28%) less than the 5-year average for this week

Gasoline use increased but diesel use fell back almost to mid-April lows.

Source: EIA and Labyrinth Consulting Services, Inc.

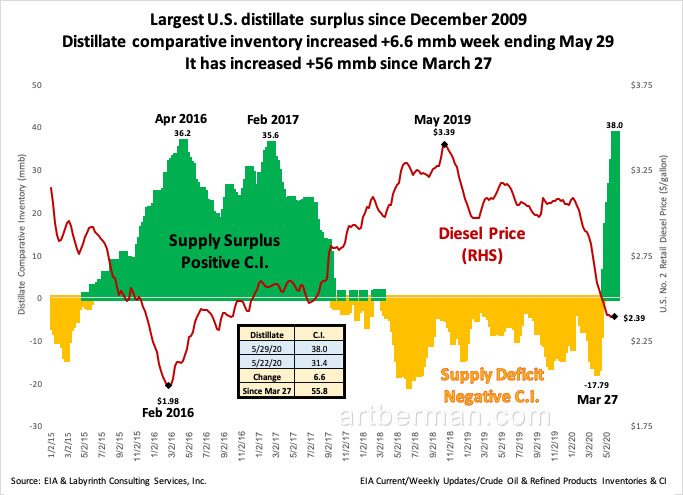

Diesel comparative inventory shows the biggest biggest surplus since 2009 and it is growing (Figure 2). Even with the increase in gasoline consumption, it’s comparative inventory is near record levels also.

Distillate comparative inventory increased +6.6 mmb week ending May 29.

It has increased +56 mmb since March 27.

Source: EIA and Labyrinth Consulting Services, Inc.

The economy will improve and consumption will increase along with it but it’s not an on-off switch. I expect that the recovery will be slow and uneven. More than 40 million people filing for unemployment benefits and a renewed trade war with China will complicate things.

An End to Shale Shut-Ins and Negative Brent-WTI Premium

Today, Pioneer Natural Resources CEO Scott Sheffield said that shale companies plan to re-activate most of the wells that they shut in during May. That means that there will be only one month of production constraint.

If he’s right, U.S. output may not fall below 11 mmb/d. At the same time, production probably will not increase much because few companies are likely to add rigs at $35 or even at $40 prices.

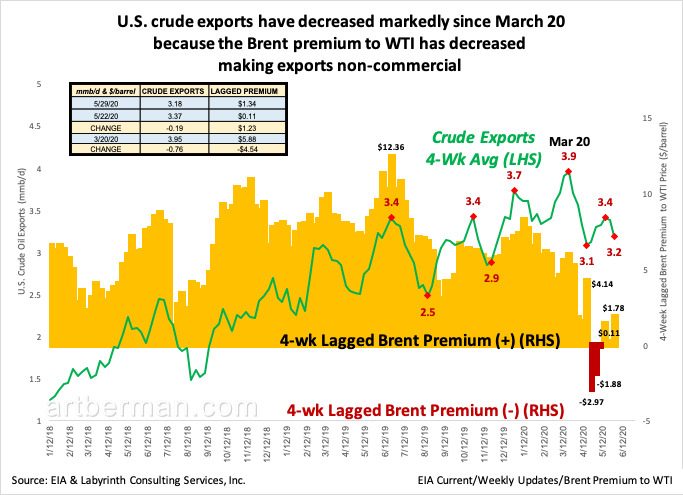

Another important development is that Brent price has moved lower than WTI.

Last week, the Brent-WTI premium -$0.49. That is bad for U.S. crude exports because the higher price for Brent is what covered transport costs for U.S. exports. Even with lower costs from Cushing to Houston and much lower super tanker rates, exporters need a Brent premium of about $1.40 to break even.

Export shipments typically lag price change by about four weeks and Figure 3 is adjusted to show that lag. As the Brent premium has fallen in 2020, U.S. crude exports have decreased by about 20%. That trend should continue and that means that U.S. domestic supply will increase by several hundred thousand barrels per day or more. Most of that excess will probably go into storage and that, in turn, will put downward pressure on oil prices.

because the Brent premium to WTI has decreased

making exports non-commercial.

Source: EIA and Labyrinth Consulting Services, Inc.

What To Expect Going Forward

The last three months have been an extraordinary period in the history of oil markets. Oil prices fell below zero and oil-price volatility remains higher than at any time in history. That suggests that any forecast about what may happen in oil markets going forward will probably be wrong.

Here it goes.

The current oil-price rally has room to continue to $40 or a little higher but I suspect it will weaken before then. Anticipation about the OPEC+ meeting this week was sufficient to maintain the last gasps of the rally. The predicted outcome left prices unchanged. That means the uplift was already priced in.

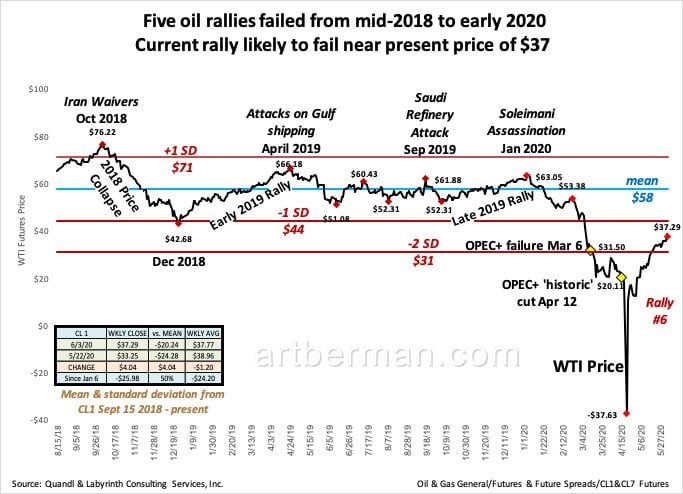

Five oil-price rallies failed from mid-2018 to early 2020 (Figure 4). They were all triggered and supported by geopolitical events. They all failed because once the crisis passed, the world was back to an over-supplied oil market on the life support of continued OPEC+ production cuts.

The late 2019 rally had failed massively before the failed OPEC+ meeting on March 6 and before the economic shut-downs because of Covid-19. Those factors compounded the failure culminating in negative WTI prices on April 20.

Current rally likely to fail near present price of $37.

Source: EIA and Labyrinth Consulting Services, Inc.

This rally has always been about correcting from that gross under-valuation back to prices at about the time of the OPEC+ failure in early March. We are there.

It was only the hand of OPEC+ that rescued markets from the April Armageddon, this time by withholding 5 times the amount of oil of any previous cut.

Managed markets have a limited life expectancy. Oil markets have now been managed for almost 3.5 years and they are showing the signs of wear.

Relieved players are now half-heartedly celebrating the rally back to the mid-$30s. Once that is over, I expect the cold reality of an end to shut in shale production, a less robust-than-expected oil demand recovery, renewed China-U.S. trade tensions, and reduced U.S. crude exports will cool whatever enthusiasm remains.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts