Comparative Inventory and Natural Gas Storage Report June 8, 2020 (2020-1)

Highlights of this week’s report:

- Natural gas surplus greatest in 2.5 years.

- Storage levels are higher than any previous year except for 2016.

- Henry Hub correctly priced at $1.76/mmBtu.

- Production is lower but so is consumption.

- Cool weather has not helped prices but that is changing.

Comparative Inventory and Storage

Many analysts and investors believe that lower associated gas production should lead to higher natural gas prices. The data does not support that view so far.

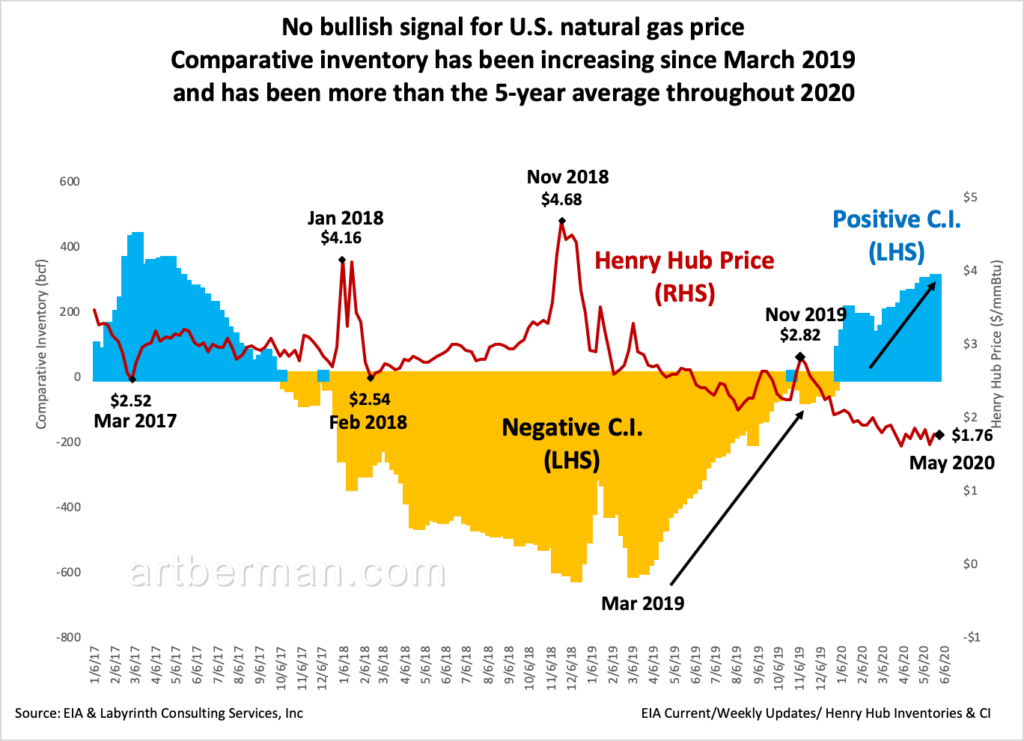

Natural gas comparative inventory (C.I.) has been increasing since March 2019 and has been higher than the 5-year average throughout 2020 (Figure 1). The negative correlation between C.I. and gas price is strong so it is not surprising that gas prices have fallen since the maximum negative C.I. more than a year ago. For more on comparative inventory, please see this and other posts on my website.

This means that gas markets are more over-supplied than they have been in 2.5 years and that the over-supply is increasing for now. That is hardly a bullish signal for gas prices.

Comparative inventory has been increasing since March 2019

and has been more than the 5-year average throughout 2020.

Source: EIA and Labyrinth Consulting Services, Inc.

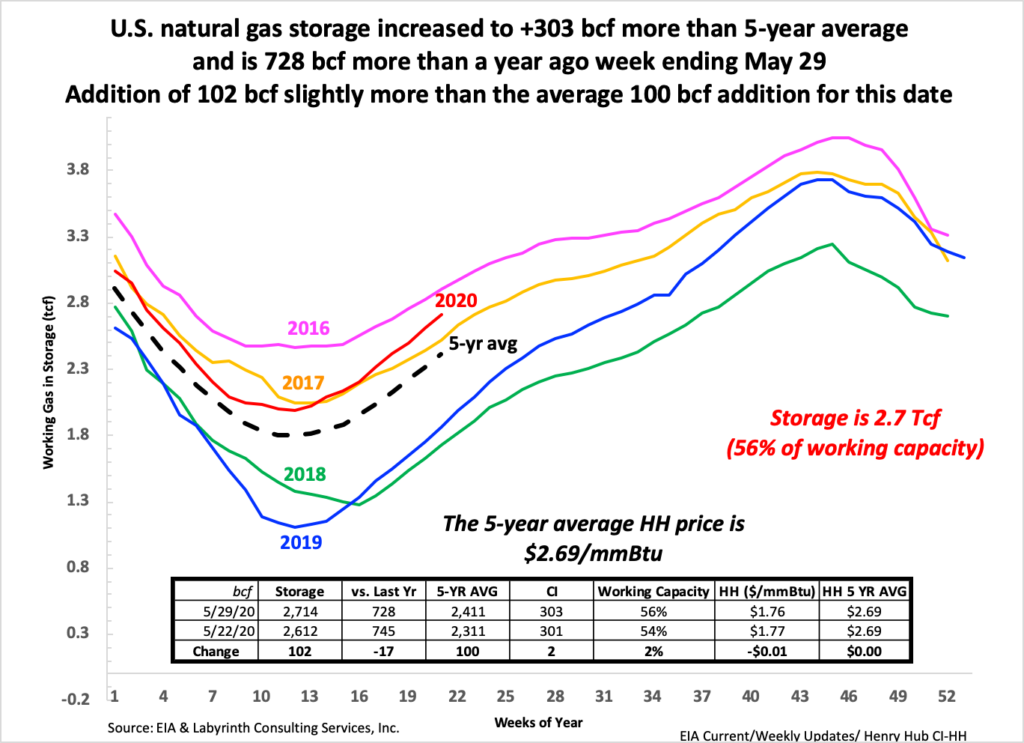

In fact, working gas in storage is at a higher level for this date than it has been since 2016 (Figure 2). Stocks increased to 303 bcf more than the 5-year average the week ending May 29 on a slightly larger-than-normal addition of 102 bcf. That is a stunning 728 bcf more than during this week a year ago. Total storage is 2.7 tcf which represents 56% of working capacity.

and is 728 bcf more than a year ago week ending May 29.

Addition of 102 bcf slightly more than the average 100 bcf addition for this date.

Source: EIA and Labyrinth Consulting Services, Inc.

Cross-plotting C.I. and Henry Hub spot price results in the red yield curve in Figure 3. The C.I. – price point for the week ending May 29 (shown in yellow) plots essentially on the yield curve meaning that gas is priced correctly at $1.77.

The yield curve suggests that gas price at the 5-year average should be about $2.20/mmBtu. Yield curves change as markets perceive different levels of supply urgency but for now, it seems unlikely that winter gas prices should be very different than during the previous winter. The future strip shows the January 2021 contract price at less than $3 which is consistent with winter C.I. levels less than the 5-year average.

Comparative inventory data has not moved from $2.20 mid-cycle price green yield curve.

Gas is correctly priced at $1.77 on larger-than-average +109 bcf addition.

Source: EIA and Labyrinth Consulting Services, Inc.

Supply and Demand

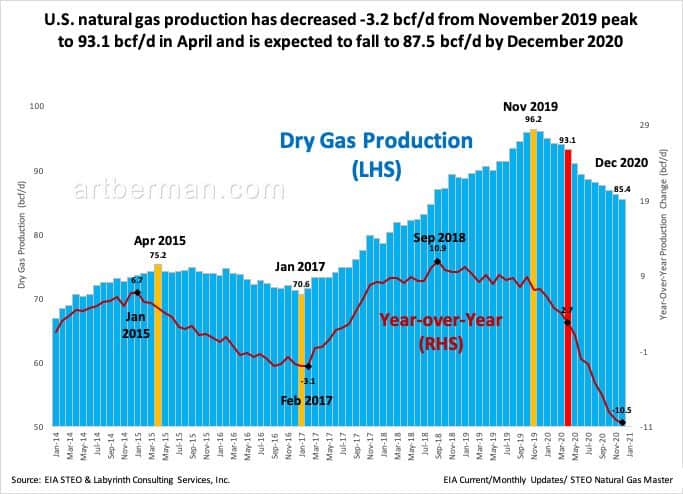

U.S. gas production has fallen more than 3 bcf/d from the November 2019 peak of 96 bcf/d to 93 bcf/d in April (Figure 4). It is expected to decrease another 7.7 bcc/d by December to 85 bcf/d so some see that as support for higher gas prices later in 2020

to 93.1 bcf/d in April and is expected to fall to 87.5 bcf/d by December 2020..

Source: EIA and Labyrinth Consulting Services, Inc.

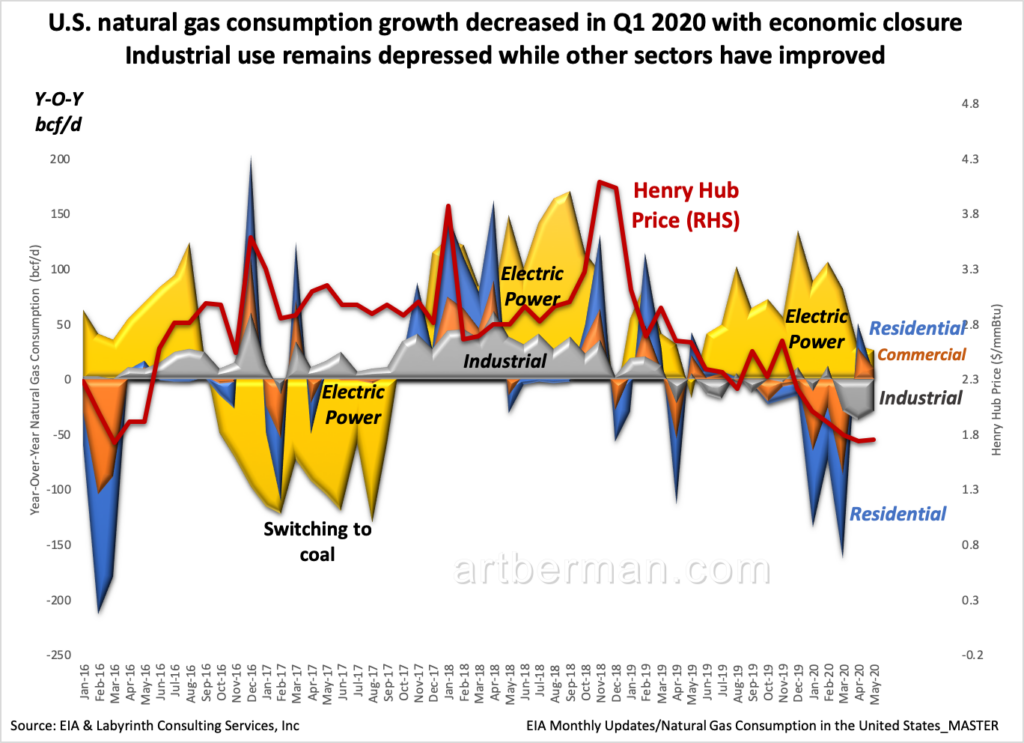

The problem with that thinking is that it ignores consumption. Gas consumption decreased in the first quarter of 2020 because of the coronavirus economic closure (Figure 5). Industrial use remains depressed while other sectors have improved but have not recovered to pre-closure levels.

Industrial use remains depressed while other sectors have improved.

Source: EIA and Labyrinth Consulting Services, Inc.

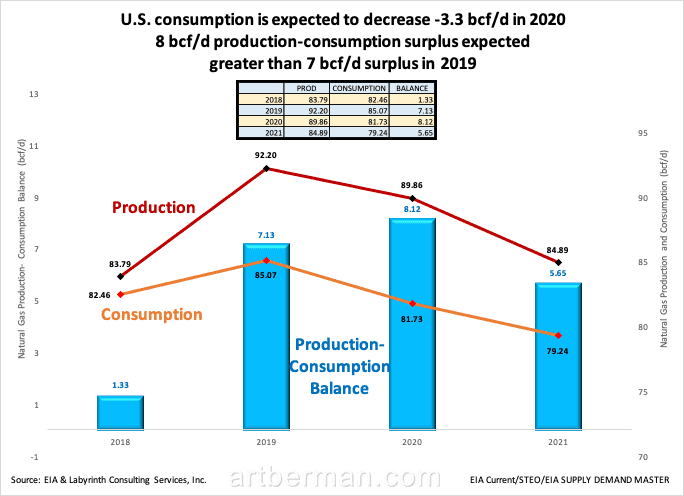

Consumption is expected to decrease by about 3.3 bcf/d in 2020 compared to 2019 based on EIA forecasts (Figure 6). Forecasts are always wrong but are worth our attention because they summarize current thinking based on credible modeling assumptions.

8 bcf/d production-consumption surplus expected

greater than 7 bcf/d surplus in 2019.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

Weather

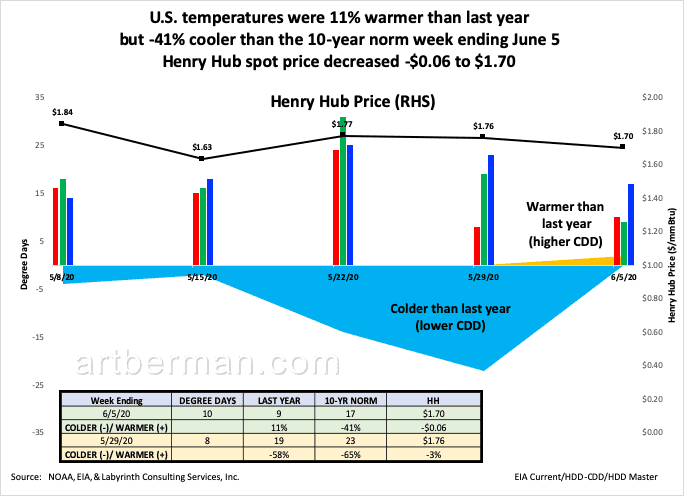

May temperatures were cooler than last year but were slightly warmer than last year for the week ending June 5 (Figure 6). If that trend continues, it will be less negative for gas prices which fell $0.06 despite demand for more space cooling. Temperatures were substantially cooler than the 10-year norm.

June through August weather forecasts indicate warmer-than-normal summer weather for the U.S. so weather may provide some upward pressure on prices in coming weeks.

but -41% cooler than the 10-year norm week ending June 5.

Henry Hub spot price decreased -$0.06 to $1.70.

Source: EIA STEO & Labyrinth Consulting Services, Inc.

Discussion

Natural gas pricing for the next 6 months should be similar to the last 6 months. The economic slow-down from Coronavirus has affected gas as well as oil consumption.

Despite lower production levels, storage is well above the 5-year average and continues to increase. Over-supply is at the highest levels in more than two years.

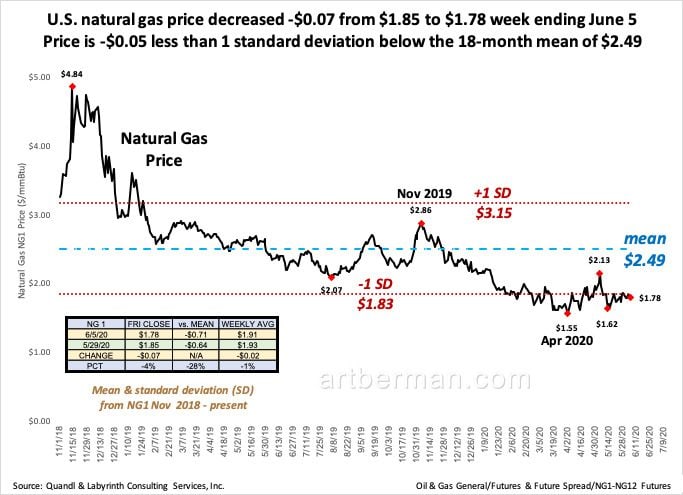

Futures prices rallied to $2.13 in early May but then collapsed to $1.62 by mid-month (Figure 8). This was a classic example of price discovery based on sentiment that lower associated gas might result in tighter gas supply. The answer was discovered and prices have been in the $1.70-range since then as I expect they will remain for awhile.

Price is -$0.05 less than 1 standard deviation below the 18-month mean of $2.49.

Source: Quandl & Labyrinth Consulting Services, Inc.

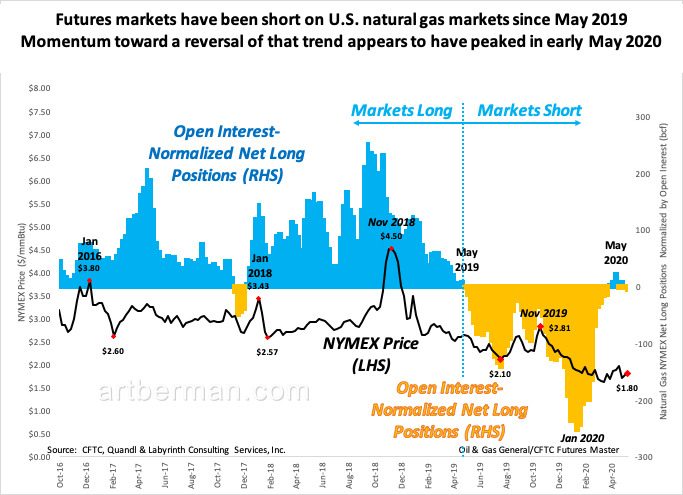

Managed money has been short on U.S. gas since May 2019. That is clear from falling net long positions which paralleled declining futures prices from late 2018 through January 2020 (Figure 9). During the first quarter of the year, that trend reversed but peaked in May and is now moving in the opposite direction. Traders continued to unwind their long bets through the latest commitment of traders report last week.

Momentum toward a reversal of that trend appears to have peaked in early May 2020.

Source: CFTC, Quandl & Labyrinth Consulting Services, Inc.

I am not saying that there is no possibility of a gas-price play in late 2020 and 2021. There is always considerable uncertainty about weather and the pace of economic recovery from coronavirus shutdowns. These could surprise either to the positive or to the negative for gas supply and demand. The point is that lower production of associated gas does not logically result in a supply deficit. Markets are more complex than that.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Thank you ART, the DATA at times is overwhelming , so much to understand and comprehend . Thank you Art for being our guide , best, jerry , Mundiregina Resources

Excellent Analysis Art, Excellent report. Art , I will be signing up for the natural Gas weekly report .Art In many of your other Reports on your site we are able to download your Reports ( which I use to double check my thinking from time to time ) Art will we be able to download the weekly Natural Gas reports 9 be happy to wait 1-2 weeks to download so I can check and double the Stats ) It is good to have a Reference set of data .Thank you Art

Jerry,

You can save any post by using you browser.

File > Print > PDF

All the best,

Art

Happy to help share why this analysis may be incorrect. First, it has been well documented that the associated gas decline was not as large as expected. In fact, it is fair to say that most is now back online. Second, the analysis does not consider company required price points to begin increasing production. As you correctly pointed out, production is declining and in fact will continue to decline for years until the price goes above $3 which is the required price for producers to drill. Third, a revision to the mean will have a colder winter this year and see consumption increase in the largest use of NG. Heading Degree Days are far more likely to increase winter 20/21 simply because a warmer winter than last year is statistically unlikely (not impossible however). Finally, bankruptcies – 50% of companies producing gas will go bankrupt and as the saying goes, the cure for low prices is low prices. This is the longest period of sub $2 prices since the 1990s and it is about to end imho.

Dana,

I agree with most of your comments but fail to understand why you say my analysis is incorrect.

Please understand that this is a weekly report on comparative inventory and the EIA gas storage report. It is not a white paper on natural gas.

All the best,

Art