Bakken Break-Even Prices Threaten Profits

The Bakken Shale play is following the same pattern of declining well performance that I have shown for the Permian and Eagle Ford in recent weeks. Bakken break-even prices have risen almost 70% as a result. If this pattern continues, it threatens the play’s future commercial viability.

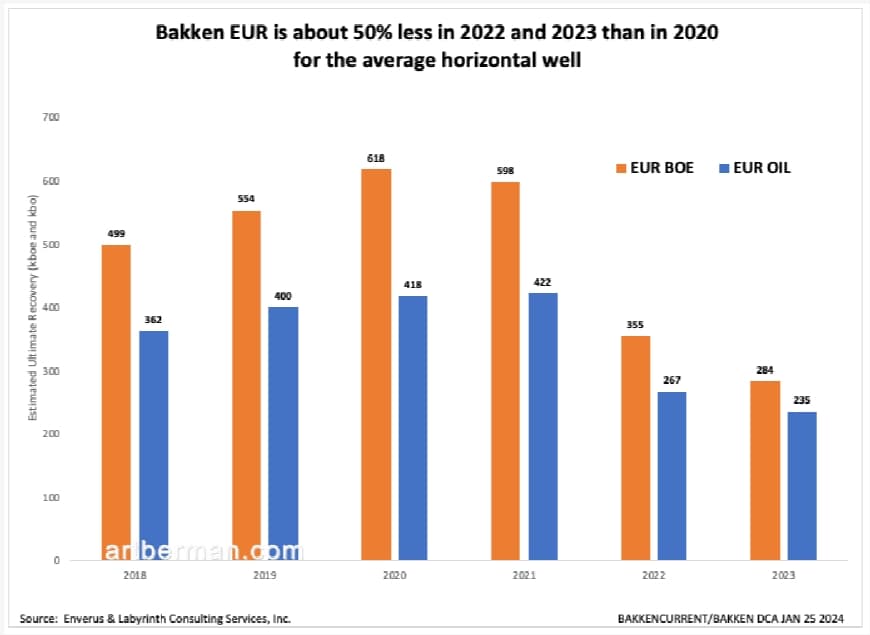

Bakken EUR (estimated ultimate recovery) has fallen almost 50% in barrels of oil equivalent from 2020 levels over the last two years (Figure 2).

Oil EUR decreased -151,000 barrels of oil per well (-37%) in 2022 compared to 2020, and -263,000 barrels of oil equivalent (-67%). Oil and gas EURs for 2023 were even lower but a less-complete production history adds some uncertainty to those values.

At the same time, Bakken production is increasing! How can that be?

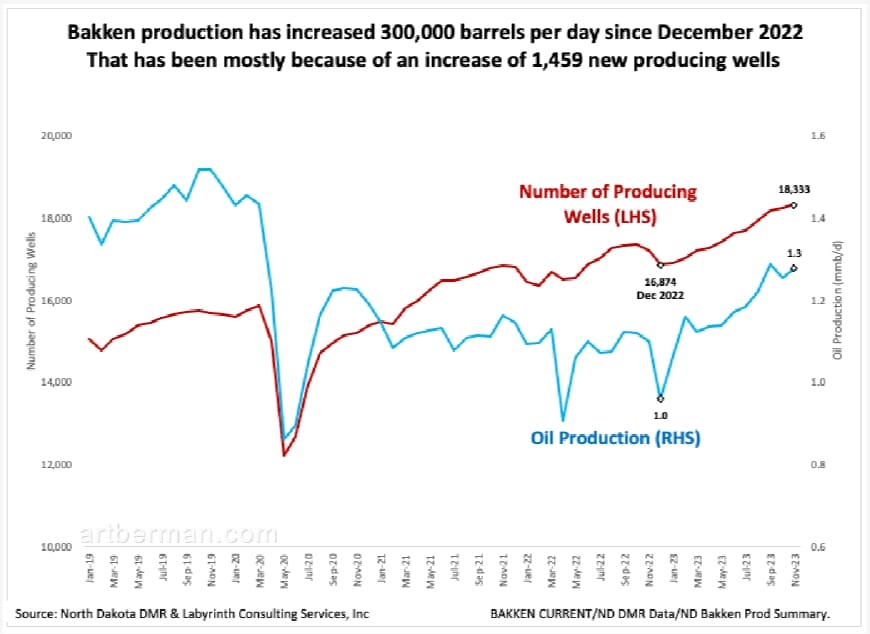

Bakken production has risen 300,000 barrels per day since December 2022 (Figure 3). That’s largely because 1,459 new producing wells were added. Production will increase even if new wells are not as good as those in earlier years if more wells are put on line.

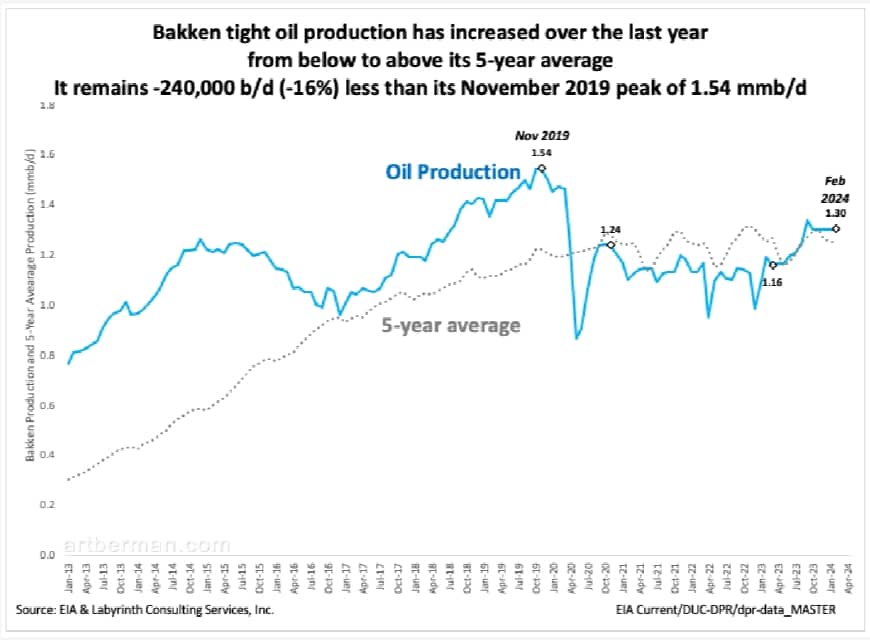

Also it took a long time for producers to fully restore wells that were shut in during the Pandemic recession. Bakken output only recovered to its 5-year average in May 2023 (Figure 4). Even so, It remains -240,000 barrels/day (-16%) less than its November 2019 peak of 1.54 million barrels/day.

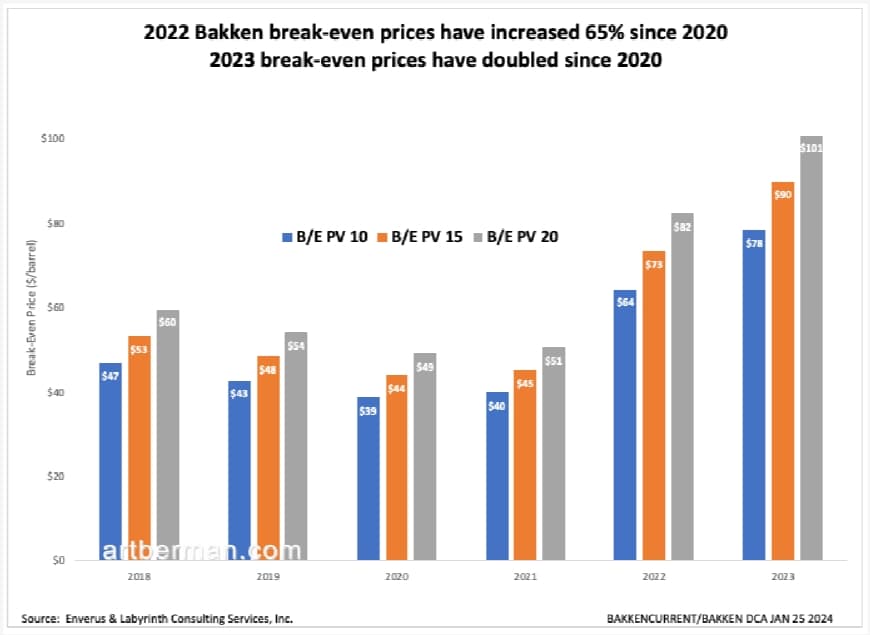

Lower well EURs have a profound effect on Bakken operator margins. That’s because wellhead prices in the Bakken are discounted about $5/barrel to WTI as a result of transport costs to refineries. Bakken break-even prices for 2022 wells have increased 65% since 2020, and have doubled for 2023 wells.

Figure 5 shows break-even prices for a range of discount rates. I have included 15% and 20% rates since investors now demand those returns because of higher perceived risk and price volatility. Present-value prices of $73 to $90 for the last two years are troubling especially compared to break-evens in the $40- to $50-range as recently as 2021.

In the Permian and Eagle Ford plays, I suggested that over-drilling might be a cause of declining EURs. That does not appear to be the case for the Bakken. Bakken bottom-hole locations are about 1000 feet apart on average compared to only a few hundred feet apart in the Permian and Eagle Ford plays (Figure 6). The average well density for the Bakken is about one well per 200 acres. For the Permian, it is about one well per 40 acres.

I did observe, however, a change in the pattern of average well decline beginning in about 2018. Figure 7 shows production histories for wells with first oil in 2014, and then for wells from 2018 through 2020. The chart in the upper left represents typical Bakken “hyperbolic decline“–a smooth progression from steep initial decline to flattening rates after the early flow period.

More recent vintages of Bakken wells show very different decline histories. The plot in the upper right, for 2018 wells, may be divided into two discrete, relatively straight-line “exponential decline” segments.

The two charts at the bottom of the figure, for 2019 and 2020 wells, represent hybrid versions of those in the top row but with stronger exponential than hyperbolic patterns of decline.

Neither well density nor lateral lengths changed appreciably among the years shown in the figure. Something in the reservoir, completion or production management of the wells changed.

Whatever the explanation, Bakken well performance has decreased and break-even prices have increased. In November, Continental Resources Chair Harold Hamm suggested that core areas of the Bakken play were reaching their peak, and that deeper “tough rock” objectives would be needed to sustain production. This study supports Hamm’s public comments.

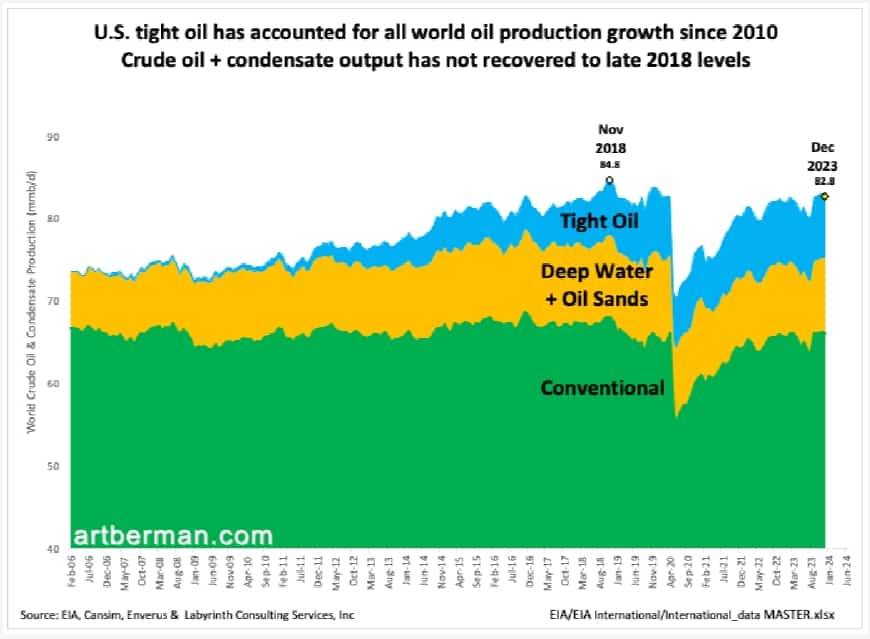

U.S. tight oil has accounted for all world production growth since 2010 (Figure 8). Despite that, crude oil and condensate output has not yet recovered to late 2018 levels. That suggests a period of relative supply scarcity going forward unless something changes

The implications of this Bakken study and recent evaluations of the Permian and Eagle Ford plays are clear—this is the beginning of the end for the tight oil plays. There are probably decades of remaining production but at lower rates. A long-term decline in shale play oil production suggests a future that may be quite different from the present.

The current over-supply of oil is almost certainly a short-term phenomenon. Since the world economy emerged from the Pandemic recession, supply urgency has always been the song playing in the background. I doubt it will remain in the background much longer based on trends in the Bakken and other U.S. shale plays.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Art, I have been a fan and follower of yours for more than a decade. With that said, the basic concept of breakeven reserves or prices, in any of these shale plays does not exist. The parameters of these plays simply has too much variation in costs structure and product pricing to make any generalizations. For instance, a well with a 10,000 ft lateral cannot be evaluated with a well with a 5,000′ lateral, operators with existing HBP acreage have significantly lower cost basis than later operators who spent massive amounts of money on their leases, operators who drilled single wells, early on, to hold acreage are at significant disadvantage to later operators who could do multiple pad wells. Production is old enough to quit using EUR as a component of analysis. Existing hard recovery numbers are available to show what recoveries have actually been on a per ft basis . Formations vary greatly within the fields themselves. No one wants to address the fact that public companies are mandated to use GAAP accounting which capitalizes total costs and depreciates over time. When the majority of the well’s production occurs in the first 24 months, companies can show a “PROFIT” on a well that might never recover the actual capital required to drill and complete the well.

Thanks, Don.

As with many things in life, assessments must be made despite uncertainties. As it turns out, lateral lengths among vintaged years of production do not vary that much. Capital costs are not a huge variable within reasonable ranges compared with opex, taxes, royalties, etc.

All the best,

Art

Just a peripheral observation, but isn’t there a strong incentive for energy companies to get as much as they can out of the ground as quickly as they can, given the increasing tilt towards windmills and other green initiatives? I see oil and gas price variation above and beyond a decreasing trend becoming a geopolitical play (it always was of course, but I think it will become even more so) and time value of money will drive getting it to market asap for most operators.

Just a thought. The Saudis seem to have grasped this anyway.

DRJ,

I recommend looking for answers on your own by searching through my posts. Get some basis and then we can have discussions.

All the best,

Art

Beginning in 2017/18, Electric Submersible Pumps (ESP’s) were utilized as the ‘initial’ lift by some of the operators. By 2020 ESP’s were commonly used by nearly all the operators (If not ESP’s, then gas lift or jet pumps to accelerate production vs the historic norm of rod pumps).

Would you conclude that increasing reserve declines are the main factor behind the recent flurry of acquisitions by the majors, plus it’s cheaper to drill on Wall St.?

Steve,

I have no information about the motives behind merger decisions other than analyst speculation that companies need a growth story.

All the best,

Art

Art you use a lot of sources in your work. Can you give the links to the sites?

Source: EIA, Cansim, Enverus & Labyrinth Consulting Services, Inc.

Kent,

I am available for consulting if you need further information about anything in my free posts.

https://www.artberman.com/services/energy-consulting/

All the best,

Art

Art:

You are influential! You came out with an article on shale gas peaking, and immediately the Biden admin blocks new LNG terminals. Congrats.

I figure all of the shale plays are either near or in decline. Not sure what that means in terms of price.

Richard,

I seriously doubt that the Biden Administration takes its cues from me but thanks.

Art

Nice work Art. You certainly have been a consistent voice of reason over the years of the shale play hype. These plays appear to destroy capital about 80% +- of their lifetime.

Thank you, Jerry.

I’m not sure that they destroy capital because the oil produced has real value to the U.S. economy but they certainly have lost money over most of their lifetimes.

All the best,

Art

Wiki leaks reported Saudi production decline starting around 2026-2027. Some are speculating that recent OPEC+ production cuts will be permanent, as Saudith are taking best care of their existing wells. Art what is your opinion on Saudi’s reported reserves? They never decline! Will they switch their production investments into Natural Gas liquids to offset their oil output? What does this mean for oil prices?

Andy,

Much of the skepticism of Saudi reserves is based on penis envy in my opinion.

I recommend reading DeGolyer and McNaughton’s reserve assessment from 2019: https://www.aramco.com/-/media/images/investors/saudi-aramco-prospectus-en-051219.pdf

All the best,

Art

Hello Art! I always enjoy your articles. Say, you mention “penis envy” regarding the Saudi’s oil production. Sigmund Freud came up with “penis envy,” not sure what you mean. I initially thought you just meant that people are jealous of Saudi production. What do you mean by that? Thanks!

Bill,

Penis envy is a psychological crisis when confronted with not possessing something that another does. I know that Freud meant it as a female phenomenon but I’m using it more generally.

All the best,

Art

So you seem pretty confident that the oil reserves shown in the Saudi-Aramco prospectus are pretty accurate?

Doone,

I trust a reserve audit more than unsupported opinions that reported reserves are wrong.

All the best,

Art

in the past 2 year or so, many new laterals are landing in the lower and upper Bakken which are true shale rock with very high TOC, which had been considered as impossible to frac before.

Results have been good.

Sheng Wu,

There is always a Shagri La story in the oil business about some new zone that was previously unrecognized or overlooked. These usually end in disappointment.

All the best,

Art

I know that the new wells being drilled by the main player around Williston are really cranking out some amazing production numbers.