Iran: Another Shock to a Fragile System

The Strait of Hormuz is not formally closed, but traffic has effectively stalled.

Only four tankers transited on March 1 as crude carriers paused to reassess security conditions. Kpler is tracking roughly 40 tankers idling nearby. Fearnley Securities notes that shipowners are shifting to a “wait-and-see” posture, which means inefficiencies and delays are likely to increase even if the waterway remains technically open.

You don’t need a declared closure to disrupt flows. Insurance repricing, crew safety concerns, and internal risk committees can slow movement almost as effectively as mines.

Oil has responded, but not explosively—yet. WTI is roughly 6% above Friday levels near $71, and Brent is up about $5, or 7%, near $78. Some are surprised prices haven’t spiked more. But this is a dynamic situation. Physical flows, insurance terms, and military posture are still evolving. Early pricing reflects uncertainty more than worst-case assumptions. As the situation becomes clearer on throughput, premiums, and escalation risk, the risk component can widen quickly.

Natural gas has reacted more sharply. Roughly 20% of global LNG trade transits Hormuz. With Qatari operations reportedly paused, Dutch TTF futures have jumped more than 40% since Friday. Gas markets are less flexible than oil, effects are seen sooner.

A wider lens suggests that conflict with Iran is a major macro shock regardless of duration.

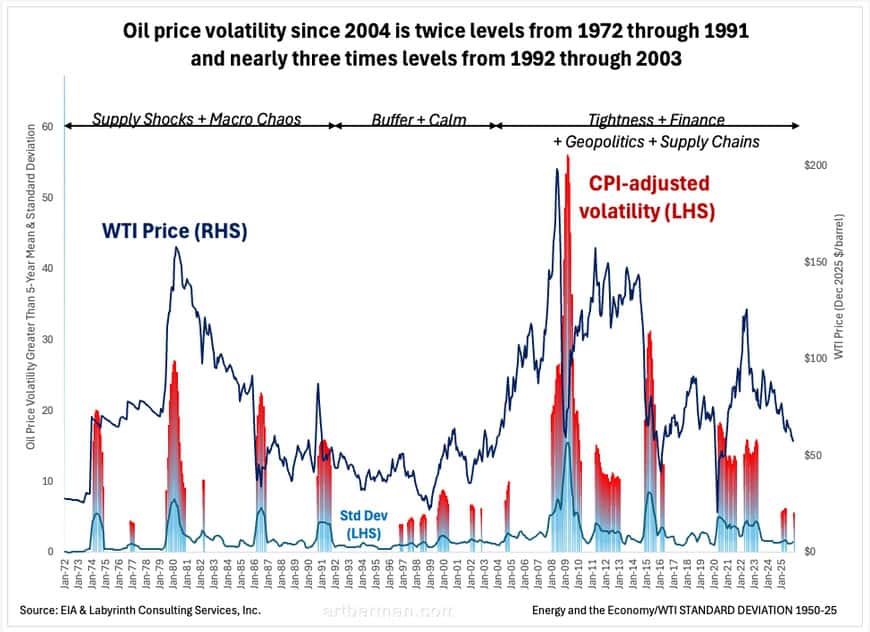

Over the past two decades, markets have absorbed repeated body blows—financial crises, wars, supply disruptions, pandemics. Since 2004, oil market volatility has roughly doubled versus 1972–1991 and is nearly triple 1992–2003 levels (Figure 1). Not every shock is geopolitical, but energy is almost always central.

Source: EIA & Labyrinth Consulting Services, Inc.

The system today is more tightly coupled and more financialized. Shocks propagate faster and their residual effects are greater even after they seem to be over. Supply risk overlaps with demand risk, currency moves interact with credit stress, and tail risks are repriced more frequently and more aggressively.

The result is a higher-frequency, higher-amplitude market regime. The margin is always moving. In that environment, commodities function both as industrial inputs and as monetary hedges—stores of value against instability.

Energy is both a physical input and a key driver of geopolitics. When confidence weakens, both roles assert themselves at once.

What is unfolding with Iran is not just a regional flare-up. It is a stress test of the broader global order. Russia has condemned the strikes rhetorically while avoiding direct military intervention, underscoring the limits of its partnership with Tehran and the constraints of a fragmented world. China, heavily dependent on Middle Eastern energy but cushioned by diversified supply and strategic reserves, is critical in tone yet cautious in action. Both powers are balancing economic exposure against strategic positioning.

This is the reality of a more fractured system. Russia’s strategic alignment with Iran reflects an effort to counter U.S. dominance, yet it has stopped short of material military support. China’s relationship with Iran and Russia sits alongside deep trade ties with the United States and Europe. The multipolar narrative runs into hard economic interdependence.

That is why Hormuz matters beyond tanker counts.

This moment sits at the intersection of energy security, great-power rivalry, and global fragmentation. Higher oil and gas prices are the immediate signal. Insurance repricing and idled cargoes are the operational expression. But the deeper story is structural: a world in which supply chains are politicized, alliances are conditional, and shocks ripple across multiple theaters—from the Gulf to the Indo-Pacific.

In short, the Iran crisis is not just about chokepoints or missiles. It is a microcosm of a more brittle global system where energy, industrial capacity, and geopolitical competition are inseparable. Markets are pricing disruption.

Many thoughtful observers frame the question as whether this proves to be another episodic shock or a structural turning point toward sustained fragmentation. I think that framing is too narrow. The more important point is cumulative. Whatever the tactical outcome of this war, it adds to the aggregate stock of insecurity, mistrust, and strategic decoupling already embedded in the system.

Shocks are layered on top of previous, unresolved shocks.

Covid fractured supply chains and normalized emergency state intervention. The Ukraine war weaponized energy, finance, and trade flows in ways that are still reverberating. The Iran conflict now pressures energy chokepoints, insurance markets, alliance structures, and great-power balances all at once.

Even if this crisis stabilizes quickly, it reinforces a world defined by higher risk premia, more defensive policy, and greater geopolitical friction. If it escalates, the fragmentation accelerates.

This is not just another headline event. It is, in my view, the third major systemic shock in five years. And the long-term consequences of the first two have not yet been fully absorbed.

The direction is clear: greater volatility, thinner margins, and a global order less confident in its own continuity.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Hi Mr. Berman, your recent Requiem for an Oil Glut post confuses me. Are you back on the peak oil train? I thought your “Peak Oil: Requiem for a Failed Paradigm” post put it to rest?

See my answer to your previous question, Jeffrey.

Thanks art, I thought you didn’t reply to older posts. Anyway, what do you think will happen to the balance of power in the future? Will it be tilted to the east, stay in the west, or corrode entirely?

As a separate question, Whats your vision for living within limits (willingly or not)? In the far far future, woukd we be Hunter gatherers again? Agrarian? Woukd regional empires return?

Thank you for your analysis! (Although the second question may be pushing the envelope a bit)

Jeffery,

I don’t know what will happen in the future–read my recent post “The End of Certainty” and you may understand the context.

I doubt humans will revert to hunting and gathering.

All the best,

Art

Excellent commentary Art, I really like the nuance you bring with this analysis! And I agree, receding trust horizons are a major concern. Who will ever trust the USA in negotiations again..?

Thanks for your comments, Nathan.

All the best,

Art