Oil’s March to $100 or Just Another Little Rally?

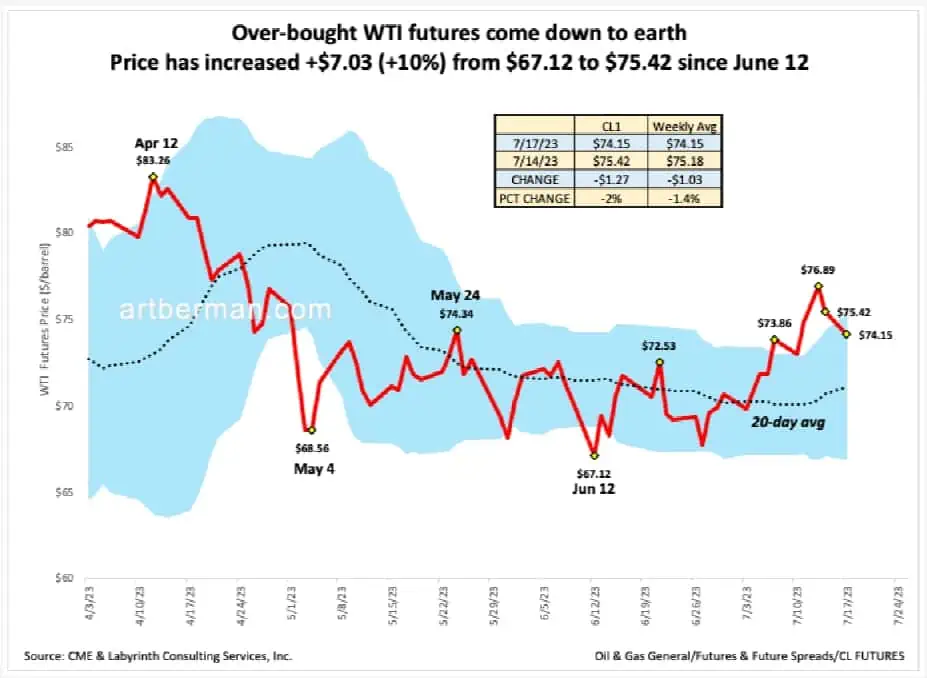

Mainstream analysts feel vindicated. After three months of reprising the incredibly tight market meme, WTI has finally increased into the mid-$70 range (Figure 1). Is this the beginning of the oil price’s march to $100 or just another little rally?

Today, Citigroup’s Ed Morse said about the potential trajectory for price,

“I’m comfortable thinking $90 as a real ceiling.”

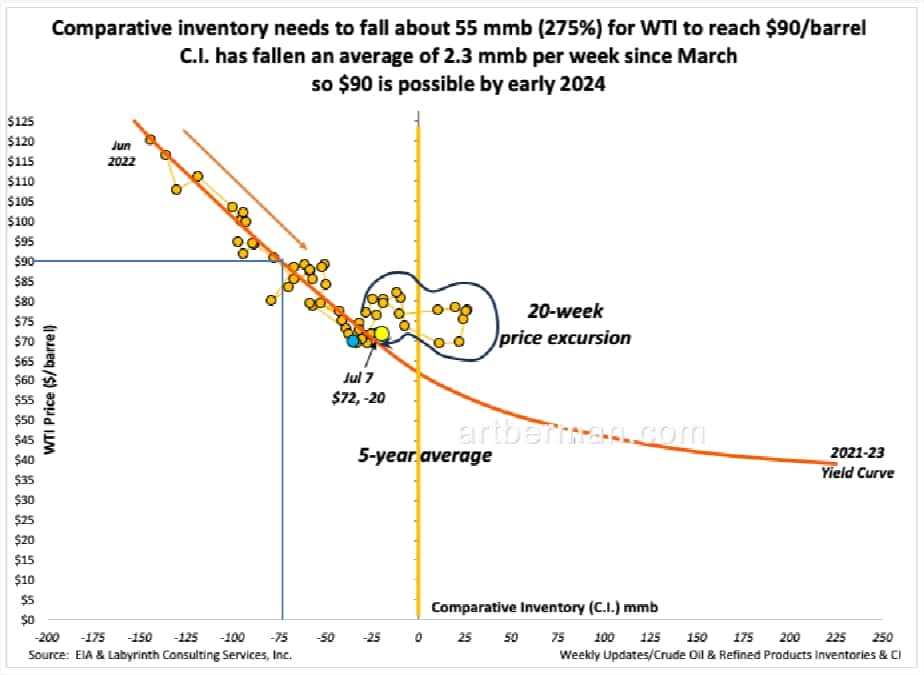

That seems reasonable to me but let’s put it into some context. U.S. comparative inventory (C.I.) was about 20 mmb less than the 5-year average as of last week’s oil storage report (Figure 2). It’s been falling about 2.3 mmb per week since March. At that rate, WTI could reach $90 per barrel in about 25 weeks so it’s possible by late 2023 or early 2024.

Does that reflect the incredibly tight supply that analysts have been hyperventilating about for months? Hardly. That’s about half-way back to levels in the aftermath of Russia’s invasion of Ukraine.

Figure 3 shows blended OPEC and EIA supply-demand data and it suggests a potential deficit of about 1.7 million barrels in the second half of 2023. That’s similar to deficits in the second half of 2021 and 2022 when WTI averaged $74 and $87, respectively.

In other words, over the next six months or so, oil prices are likely to return to pretty much where they have been in recent years at similar supply-demand balance and inventory levels.

There are a million things that could and are likely to happen in 2023 that could profoundly change this context. I just don’t see any extraordinary structural change about to happen that is outside of what is normal and expected for oil markets.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts