What The Market Knows About Oil’s Future

Warren Buffet is bullish on oil and gas. He recently committed more than $3 billion to an LNG export terminal in Maryland after increasing his stake in Occidental Petroleum. That’s because Buffet is a value investor and energy stocks are relatively cheap. Energy also generates more cash than any other sector.

Why doesn’t the market agree with Buffet?

Robert Bryce wrote a thoughtful article this week in which he explored this question. He argued that gasoline demand is booming and is likely to remain strong, and that world oil demand is expected to reach record levels in the next few years.

Javier Blas echoed some of those observations in a post this morning.

“Even with the boom in electric cars, the absolute number of gasoline-powered cars is still increasing; consumers are holding onto their vehicles longer, delaying the improvement that comes with newer and more fuel efficient models; and in Europe, consumers have swapped their diesel cars for gasoline ones, giving the latter an unlikely boost.”

Bryce further explained that America has a long-lived fleet of 284 million conventional cars that will last for years despite the strength of electric vehicle sales. He concluded that seven oil and gas companies are under-valued based on standard price-to-earnings and enterprise value-to-EBITDA ratios.

“The supermajors are all selling at big discounts to the S&P 500. So are the independents, including Devon and Diamondback.”

I agree with most of what Bryce says but am hesitant to say that the market’s view of oil and gas companies is wrong.

On the most basic level of net returns, energy stocks have consistently under-performed the S&P 500 for most of the last decade (Figure 1). The 10-year net total return for the energy sector is 3.2% compared with 11.9% for the broader market. Moreover, energy stocks have returned -0.6% so far in 2023 while S&P performance has averaged 19.7%.

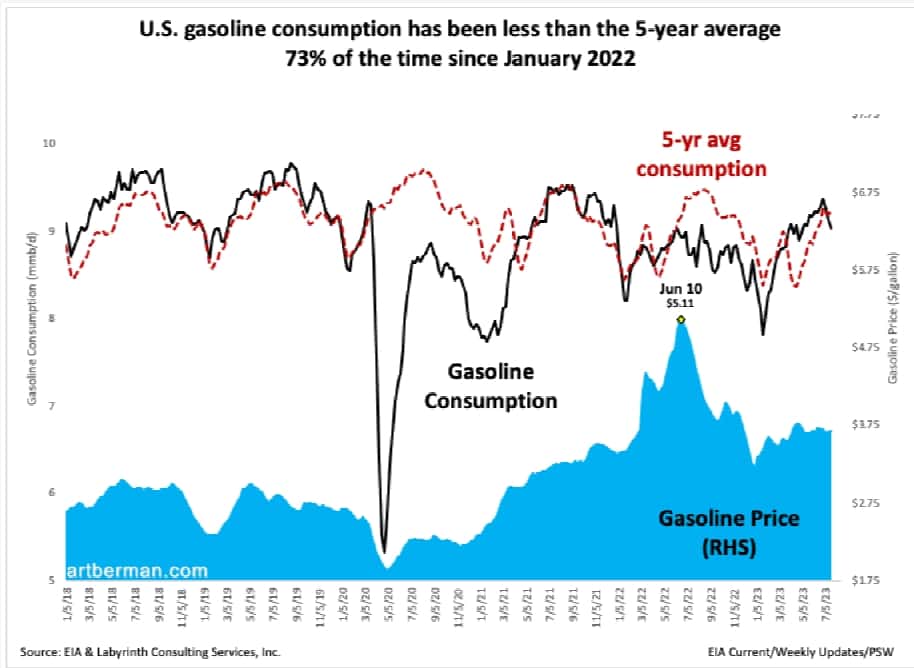

Furthermore, U.S. transport fuel consumption does not seem quite as straight-forward to me as it does to Bryce. Gasoline consumption has been less than the 5-year average 73% of the time since January 2022 (Figure 2).

Similarly, diesel consumption has been less than its 5-year average 68% of the time since January 2022 (Figure 3).

Despite reports about the strength of the U.S. economy and the recent oil-price rally, energy is the economy. Neither gasoline nor diesel data provide strong support for the popular idea that the U.S. economy and oil markets are booming. Lower-than-average diesel consumption is especially disturbing because it is the hemoglobin for the movement of goods and materials. Its use is fairly inelastic in normal economic conditions. When diesel consumption falls, it is ordinarily because orders are weak.

The U.S. and world economies are still recovering from the effects of the Covid economic closure and associated supply chain problems. The supply and price shocks that followed Russia’s 2022 invasion of Ukraine will probably have a lasting effect on global markets. This coincides with a reversal in the globalization of trade that led to commodity deflation throughout much of the last 30 years.

Liam Denning made these observations a few days ago.

“As much as the onset of the war in Ukraine offered a taste of those lucrative periods where OPEC could capitalize on disruption, it was also another visceral indicator of wider disruptions. Oil embodied globalization before that was even a term, but the notion of relying on fragile or even hostile nations for life’s essentials is fast falling out of fashion. At the same time, climate change is forcing a reevaluation of energy’s physical foundations.”

Public debt rose to extraordinary levels because of both Covid and Ukraine. It is naive to believe that is all or even mostly behind us, and it is easy to see why why markets remain cautious.

Vaclav Smil’s four pillars of modern civilization—steel, cement, plastic and ammonia—require fossil fuels now and in the foreseeable future.

“The scale of our dependence on fossil carbon make any rapid substitutions impossible…Modern economies will always be tied to massive material flows and…will remain fundamentally dependent on fossil fuels used in the production of these indispensable materials.”

Vaclav Smil, How The World Really Works

The idea that electric vehicles may displace gasoline reflects a fundamental ignorance about the oil refining process. The idea that a green energy transition is reshaping society ignores the way the world really works.

Warren Buffet’s investments in oil and LNG make good sense because energy will always be important and well-managed companies will be successful.

At the same time, it is impossible to ignore that oil production and consumption are declining—forecasts to the contrary notwithstanding. That is because of massive public and private debt loads, inflation, economic contraction, declining oil affordability, consumer behavior change, and limited credit for new drilling and development. The imagined transition to renewable energy is a secondary factor at best.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Makaleniz çok güzel olmuş…

Thank you!

Humans cannot fight fossil fuels – powered by fossil fuels;

“In any system of energy, Control is what consumes energy the most.

Time taken in stocking energy to build an energy system, adding to it the time taken in building the system will always be longer than the entire useful lifetime of the system.

No energy store holds enough energy to extract an amount of energy equal to the total energy it stores.

No system of energy can deliver sum useful energy in excess of the total energy put into constructing it.

This universal truth applies to all systems.

Energy, like time, flows from past to future” (2017).

My basic takeaway is despite an optimistic future (energy is the economy and fossil fuels will still play a key role (Smil)), we should not dismiss the caution that the market is showing regarding the oil and gas industry. Recent global turmoil (and the resulting high debt overhang – both public and private) could make fossil fuels unaffordable to large portions of the world’s population. High and profitable oil prices could lead to an equally high level of demand destruction.