OPEC’s Last Encore: Time to Leave the Stage

OPEC should abandon production cuts and quotas, letting members focus on their own interests. The oil market is too big to control, even for major producers.

It’s unlikely, but a rational move would be to admit the limits, stop chasing the impossible, and return to balancing market share and price individually.

Think of OPEC as a pop band with one big hit in 1973, a flop in 1986, and then a 30-year Vegas residency. Every decade brought a few new songs—mixed reviews, no top 10 hits. In 2014, oil prices collapsed, giving OPEC a chance at a comeback, but it fumbled the timing and the look. By late 2016, it was back on stage, but the old fans were only half-interested. The band was past its prime.

For the past year, the OPEC band has been booking shows only to cancel last minute, wearing out even its most loyal fans.

Javier Blas made a sharp observation this week in an article he called “The Wrong Oil Price Is Truthfully a Problem for OPEC+.” He argued that OPEC+ has kept oil prices high, creating a supply glut that subsidizes its rivals, especially U.S. shale. This strategy has backfired, limiting OPEC+’s ability to boost production and sparking internal discord. Angola has already exited, others may follow, and a senior Iranian official publicly admitted the cracks, forcing a postponed meeting. Saudi Arabia is now pushing to delay production hikes and enforce quotas on members like Iraq and Kazakhstan. Meanwhile, U.S. shale thrives on efficiency gains, leaving OPEC+ in a position where its own strategy could be its undoing.

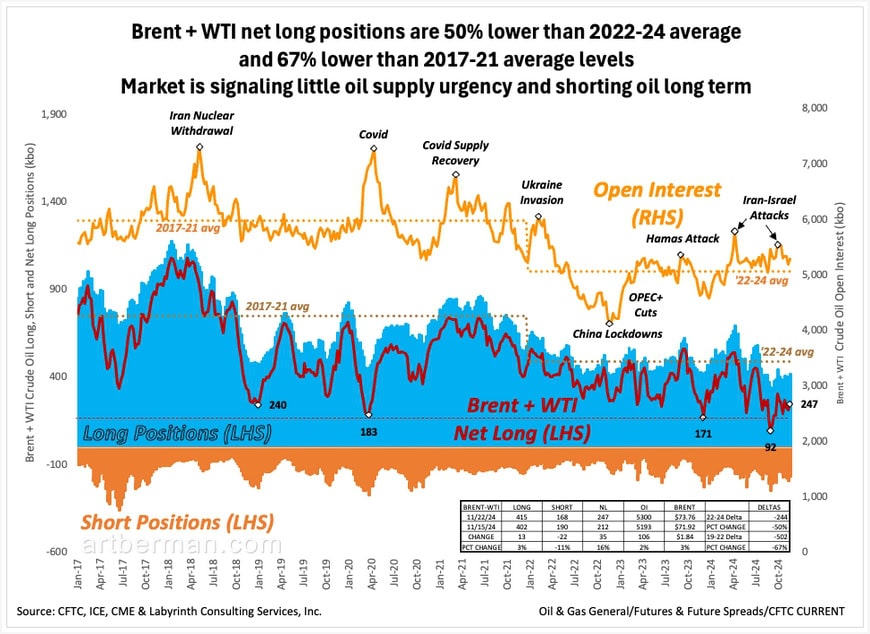

It seems that fund managers reached a similar conclusion several years ago. Figure 1 highlights a steady decline in net long oil futures positions (dark red line) since 2018. These positions—representing the gap between long (blue) and short (orange) holdings by hedgers and funds—are down 67% from their 2017-2021 average. The data show oil markets have largely ignored supply scarcity fears since early 2021, even during the Ukraine price shock.

In September, net longs dropped to 92 million barrels, a level even lower than during the COVID crash in 2020. Sentiment has improved slightly since, but last week’s 247 million barrels is still 50% below the 2022-2024 average.

Oil fund managers have been shorting the market since 2018, and they aren’t doing it blindly. Markets aggregate informed perspectives and data, cutting through the noise of daily commentary. They’re not perfect, but they’re often more objective than analysts with agendas.

The message? There’s no urgency about supply. Demand has been weakening for a decade. Prices have stayed afloat thanks to geopolitical shocks, creating a false sense of tightness. Strip away those crises, and the underlying weakness is plain to see.

Oil isn’t just another commodity—it is the economy. And the market’s signal couldn’t be clearer: the era of growth is over.

OPEC is not going to manage its way out of this. It’s a long-term problem that keeps getting worse despite all of the group’s production cuts and attempts to manage the market.

The band should call it quits.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

“Oil (and Fossil Gas) isn’t just another commodity—it IS the (Energy) economy. And the market’s signal couldn’t be clearer: The era of growth is over.”

And the biggest driver is RISK. Flood, Fire & Hail Insurance cancellations are like a punch in the face to homeowners & real estate business owners. Can’t get insurance?…… Can’t get a mortgage. New industries, like server farms & AI, that demand 24/7 firm power, are not going to invest in antiquated fossil fuel power. It’s the era of massive cheap surplus solar, wind, & 24/7 geothermal energy. Industry, Housing & Transportation, including aviation, will be running on renewable electricity or renewable synthetic fuel derivatives by 2040.

Sorry, Jerry, but you’re 100% wrong.

You brought up AI. With the biggest expansion in electric power demand in decades, where are the providers looking for power? Not renewables even though electric power is their supposed forte.

Nope, they’re looking to natural gas and nuclear.

Please read this post for the details: “Blows to the Body Electric: AI meets Renewables–Renewables Lose”

https://www.artberman.com/blog/blows-to-the-body-electric/

All the best,

Art

The band analogy is great Art.

Thanks, William. I thought it was a good analogy.

Best,

Art

“Demand has been weakening for a decade”. Guess its growing and growing.

https://www.iea.org/data-and-statistics/charts/global-oil-demand-growth-2011-2025

Rolf,

Your comment and link confuse me. Are you agreeing or disagreeing? Please be a bit clearer.

Art

Thanks Art,

To summarise, do you see the end of growth as being caused by the inability to expand oil production? And that the end of growth is leading to oil price decline?

It feels a bit circular, but maybe another way to think about it is that the broader economy can’t afford to pay the marginal oil price required to expand (or perhaps even maintain) production?

Cheers Gus

No, Gus, that’s not what I see. Please read this recent post: This Is How Oil Ends

https://www.artberman.com/blog/this-is-how-oil-ends/

Production has reached a plateau because of weak demand; this is, in turn, because of a weak global economy.

All the best,

Art

A question.. some questions!

Is one of the reasons because the extraction is becoming more expensive? Which means, there IS oil, but they are too deep or they are only shale (expensive to extract and refine). What about those ambitions of the global powers to go to the Arctic? Does it just shows the despair?

And what about correlation with other resources? Like minerals.

(Simon Michaux does a nice work.)

Gesvos,

The affordability of oil is an issue but the more immediate problem is OPEC’s attempt to manage an unmanageable market. OPEC had success with its oil embargo in 1979 but that was really an equilibration of oil price after Nixon’s exit from Bretton Woods and the subsequent global devaluation of currencies.

The advent of futures markets for oil in the 1980s seriously limited OPEC’s ability to control prices. You would think that the group had learned but go figure.

All the best,

Art