There’s Nothing Confusing About Natural Gas Prices

If you are confused by low natural gas prices then comparative inventory is your friend.

Companies have over-produced gas, storage is exploding, and prices have fallen. Comparative inventory (C.I.) makes this crystal clear.

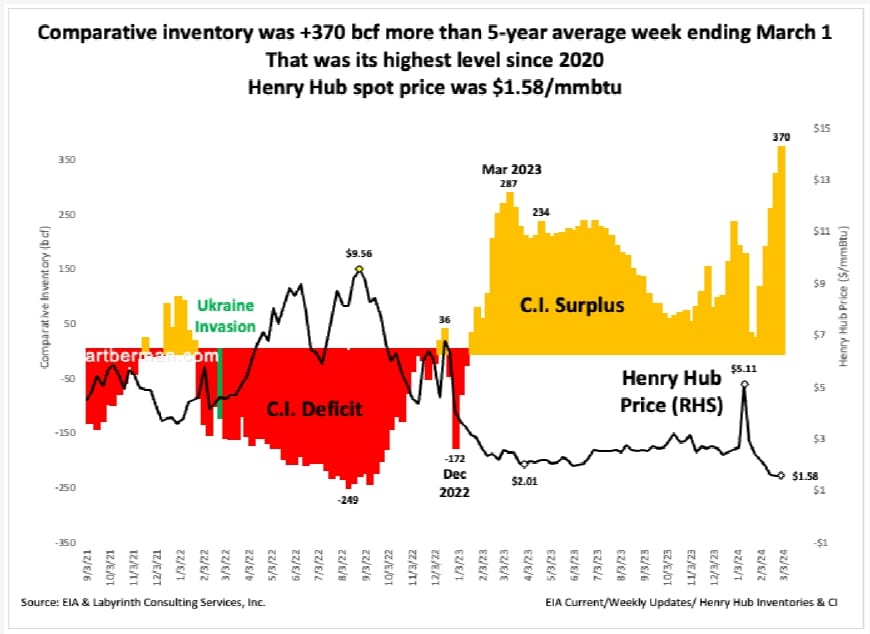

U.S. natural gas C.I. was 370 bcf (billion cubic feet of gas) more than 5-year average for the week ending March 1 (Figure 1). That was the highest level since 2020. The Henry Hub gas spot price was $1.58/mmbtu (million British thermal units). That was the lowest price level since 2020.

C.I. and price correlate inversely. When C.I. is high, gas price is low and vice versa. Without C.I., it’s confusing. With C.I. it makes perfect sense.

There has been more than enough gas in storage for winter heating since early January. Markets have discounted the price accordingly. The prompt gas futures contract rolled into March during the last week in January so winter has been over for gas traders for five weeks. The contract rolled to April ten days ago so now gas is trading in the “shoulder” period of seasonally weak demand between winter and summer. Still confused about low gas prices?

Figure 2 shows the same C.I. and price data shown in Figure 1 as a cross plot. The spot gas price of $1.58 for last week was exactly what it should have been at current inventory levels. It plotted right on the yield curve (red dashed line) that relates price and comparative storage volume. There’s nothing confusing about that at all.

based on the 2023-2024 comparative inventory yield curve. Source: EIA & Labyrinth Consulting Services, Inc.

Storage is full because there’s been mild winter in the United States so heating demand was low. Warm winters in 2022-2023 and 2023-2024 led to less natural gas consumption than normal and lower natural gas prices in 2023 and 2024.

Figure 3 shows degree days compared to their five-year average for the United States since January 2007. A degree day is a measure of how much hotter or colder temperature is compared to a standard level.

Degree days are a proxy for natural gas demand for heating and cooling. The blue bars represent periods in which energy use was greater than the five-year average and the orange bars, periods where use was less than the five-year average.

January 2023 to the present is dominated by orange bars. Mild winters have resulted in low natural gas use so produced gas has gone into storage. The red line in Figure 3 is spot gas price which correlates inversely with degree days just like it does for C.I.

and lower natural gas prices in 2023 and 2024. Source: EIA STEO & Labyrinth Consulting Services, Inc.

Oil and gas companies have historically overshot demand about every four years causing gas prices to plummet.

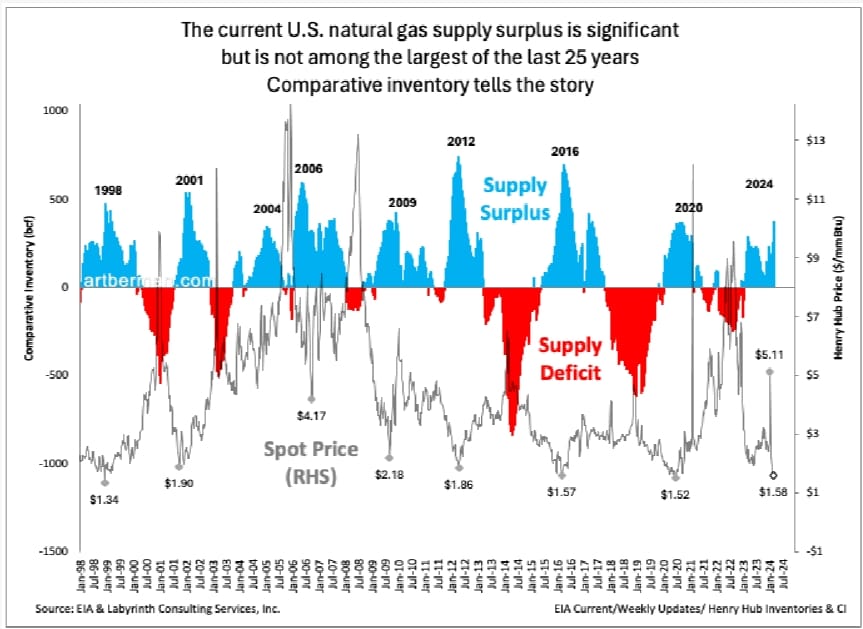

The current supply surplus is significant but it is not among the largest of the last 25 years. Supply surplus was comparable in 2004 and in 2020 but was greater in 1998, 2001, 2006, 2009, 2012 and 2016 (Figure 4).

Shale gas is the main reason for oversupply of natural gas over the last fifteen years. The Barnett, Fayetteville, Haynesville and Marcellus pure shale gas plays began in the first decade of the 2020s. Associated gas from the Eagle Ford, Permian and other tight oil plays followed in the second decade of this century.

Except for the Ukraine anomaly in 2022, price has declined consistently since about 2010 (Figure 5). Dry gas production increased from an average of about 51 bcf/d (billion cubic feet per day) from 2000 through 2007 to an average of more than 73 bcf/d in 2015 and 2016. By the end of 2018, output was more than 89 bcf/d. By the end of 2019, it was more than 97 bcf/d. Average supply for that year exceeded consumption by more than 5 bcf/d.

In 2023, gas supply was 16.5 bcf/d more than consumption. That should make the reason for low gas prices fairly clear.

Gas price has declined as a result except for the Ukraine anomaly in 2022. Source: EIA STEO & Labyrinth Consulting Services, Inc.

This irrational level of gas over-production puts the industry’s obsession with LNG export into perspective. Unable to control themselves, they need to send some of the excess to foreign markets so prices don’t drop toward zero. This also puts Biden’s recent announcement to pause gas exports into the same perspective. Why should bad producer behavior that drains America first be acceptable?

Investors sent a strong message to oil companies that production growth must end. They wanted to see returns instead of growth. It seems like a good time to send those companies the same message about natural gas.

Enough is enough. Learn to manage your business like adults.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

I have a technical question, which is maybe not related to this post and i already apologize if it is kind of dumb, but what happens when the gas is mostly gone? Are they going to install pumps on these tight reservoir wells or how do i have to imagine that?

Kali,

Gas expansion is the reservoir drive. It won’t go to zero but pumps will be necessary.

All the best,

Art

Oil companies should learn to manage their business like adults? From under what rock did you crawl out?

The first time oil companies coordinate to reduce production in order to increase the price of natural gas there would be immediate howls of “price gouging,” vehement accusations of greed, and an explosion of congressional hearings. How can you present yourself as an energy consultant and not acknowledge the nearly impossible position in which oil companies find themselves? Damned if they do and damned if they don’t.

Rick,

I can present myself as I am–a petroleum geologist who has spend 45 years working mostly in oil and gas. Running a business according to basic principles of supply and demand should not put anyone in an impossible situation.

All the best,

Art

Enjoyed your insights on the Behind the Markets podcast

Thanks, Dan.

All the best,

Art

I enjoy your analyses of oil and gas production, prices and demand. Do you ever look at the liquids like propane, butane and other products stripped from the gas stream? I am curious about them too and how they fit into the overall scenario. Thanks!

Mark,

I look at lots of thing but I’m only one guy with no staff.

All the best,

Art

The unique circumstance of Freeport LNG causing nearly 400 bcf to backup into the system in 2022-2023 and making 2 bcfpd find a home was certainly a significant contributor to the current storage excesses. And now they are off again on Train 3 for what’s now projected to be 2 months …

David,

Freeport LNG is counter-factual logic. It only accounted for 0.5 bcd/d anyway. Over-production is and always was the problem.

All the best,

Art

Per Figure 5, and since 2020, it appears that the bulk of the growth has come from the Permian, which is perhaps the byproduct of oil production. The other gas-basin operators appear to be gaining in discipline, and perhaps are producing at volumes aligned w/current operating efficiencies. It could be that further shale-gas industry consolidation will be required in order to further drive production discipline and cost efficiencies.

Christian,

Permian and Haynesville are the only plays that haven’t peaked. It has nothing to do with producer behavior.

All the best,

Art

Thank you for your nat gas assessment!

What is your latest FMV for WTI?

JSG says $83 on 3/6/2023:

https://twitter.com/UndervaluedOnG/status/1765413278631498174/photo/1

Was a plant being built in Louisiana to turn natural gas to liquid and export it that way. I haven’t heard if that’s still a possibility?

Jim,

Gas-to-liquids in Louisiana was someone’s wet dream but it hasn’t happened (and probably won’t happen unless oil prices go to $150). The economics and EROI of GTL are atrocious.

All the best,

Art