Why Analysts Are Wrong About Oil Prices: What The Market Knows

Analysts have been wrong about oil prices for most of 2022 and continue to be wrong. Why?

Goldman Sachs provides a good case history.

In early June, the bank predicted $140 average Brent price between July and September. It was $100. In late August, when prices fell below $100, Goldman’s Jeff Currie said that Brent would return to $120. The September through October average was $92. In late November, the bank forecasted an average Brent-price of $100 for the fourth quarter of 2023. It has averaged $89 through December 19. In mid-December, Goldman’s latest forecast is for $90 for the first quarter of 2023 and an $98 average price for 2023.

My point is not to criticize Goldman Sachs but to try to understand why analysts have been consistently wrong.

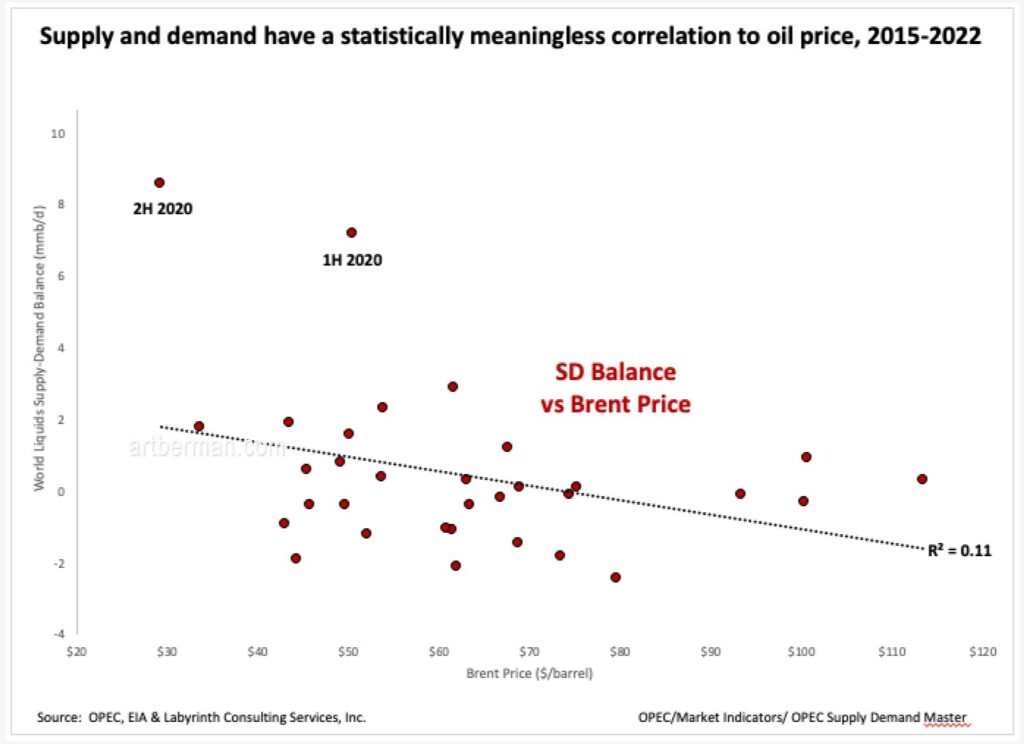

The first problem is that supply and demand are central to their forecasts but supply-demand balance is a poor predictor of price. In fact, it has a statistically meaningless correlation to oil price (Figure 1). The R² correlation coefficient from 2015 to the present is 0.11. Leaving out the 2020 anomalies, R² gets worse and falls to 0.02.

I’m not saying that supply and demand don’t matter. The difficulty is that supply and demand are at best gross estimates. It is impossible to integrate every nation’s production, consumption and exports into a single framework. The data simply doesn’t exist. More importantly, supply and demand are transactional factors that largely exclude storage.

That’s right. Storage is not part of supply. Supply equals production, and demand equals consumption plus net imports minus storage withdrawals. That’s like saying that someone’s net worth only includes investments and savings when withdrawals are made from them.

Price formation in oil markets is all about supply and inventories are a big part of supply. Demand is of course important but markets cannot control demand. They can, however, use price as a lever to encourage drilling when there are concerns about under-supply, and to discourage drilling when over-supply dominates.

Oil price is not an input factor for either supply or demand. It’s relationship is implied or deduced.

The way that most analysts use supply and demand is unrealistic. It assumes that markets are ordinarily in equilibrium with occasional periods of dis-equilibrium. The truth is that, like all complex systems, markets are rarely in equilibrium except in the human imagination. Here’s what Goldman’s Jeff Currie said on December 15:

“Commodity prices perform an economic function. They have to rebalance supply and demand, bring them back into line, when they get out of line like they did in the end of 2021 and the early part of this year.”

Jeff Currie, Goldman Sachs Head of Commodity Research

In other words, commodity markets are equilibrium systems that occasionally get out of whack.

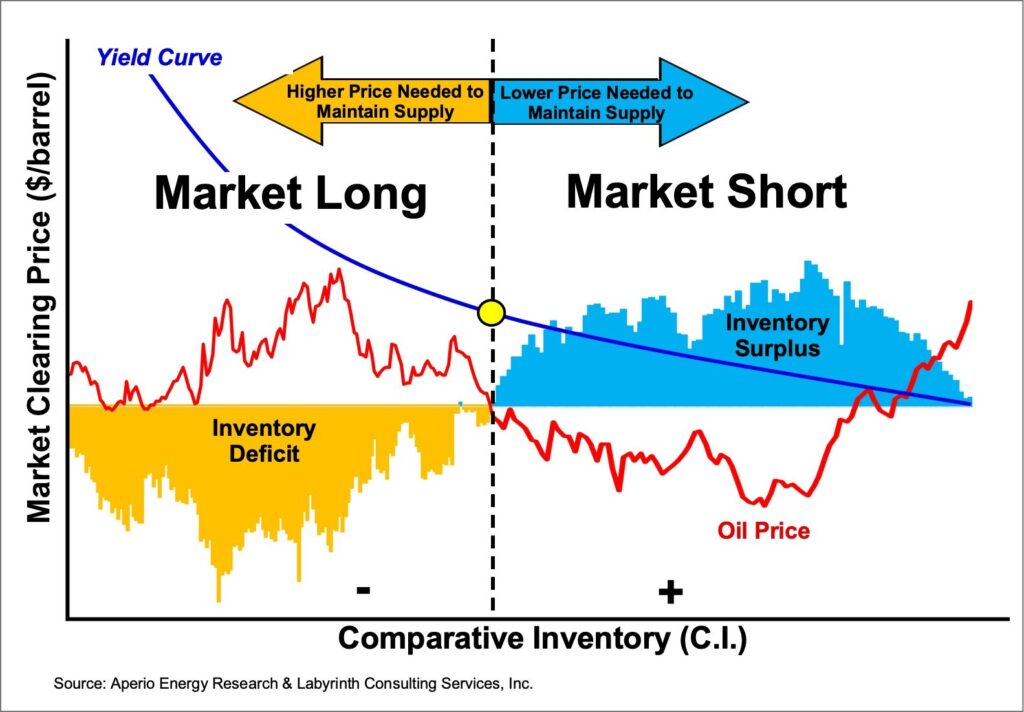

Comparative inventory (C.I.), on the other hand, assumes that oil is a mainly a disequilibrium system in which equilibrium is the exception rather than the rule. Crucially, oil price is a direct input factor. C.I. accounts for additions to and withdrawals from storage based on supply and demand, as well as for the reserve base that represents the storage equivalent of investments and savings.

Markets are always long or short (Figure 2). When C.I. is in deficit, markets are long and use higher price to encourage producers to drill more wells. When C.I. is in surplus, markets are short and use lower price to discourage drilling.

In a recent written communication, Mike Bodell who originated the comparative inventory method, stated,

“Simply, price formation requires a comprehensive, integrated view incorporating equilibrium and disequilibrium economic approaches.”

J.M. Bodell

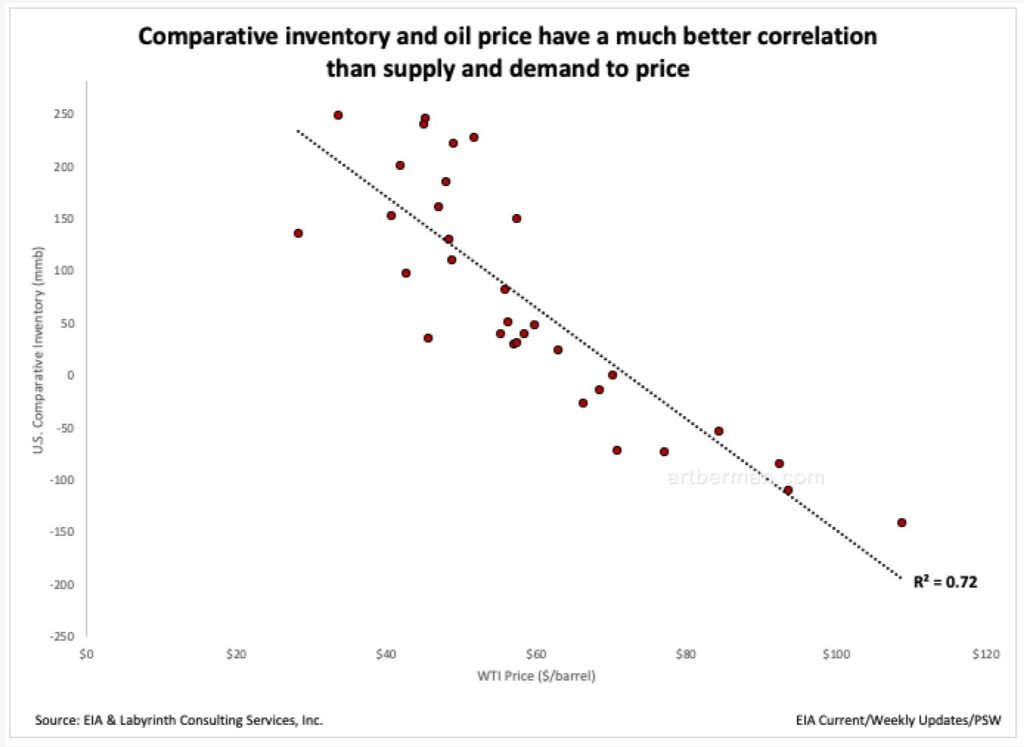

Not surprisingly, comparative inventory has a stronger correlation to oil price than supply-demand balance with an R² of 0.72 from 2015 through the present (Figure 3). It’s not perfect but its correlation coefficient is 6.5 times better than supply and demand.

Figure 3. Comparative inventory and oil price (quarterly data) have a much better correlation than supply and demand to price. Source: EIA & Labyrinth Consulting Services, Inc.

That brings me to the second reason that analysts have consistently gotten oil price forecasts wrong in 2022. Because they treat oil as an equilibrium system, they focus mainly on areas that are upsetting that equilibrium while treating most other factors as more-or-less static. Here is Jeff Currie again.

“Markets are re-balanced now today. Why? Because China is being locked down so demand came back down on top of supply and prices collapsed back down.

“We have not been investing in supply. Supply is stagnant.

“So I have to simply ask, What happens when China, the largest commodity consumer, the largest oil importer in the world, begins to rebound significantly in the first part of next year? It’s going to tighten all of these markets tremendously and put a lot of upward pressure on prices.”

I respect Jeff Currie and always pay attention to what he says but this is an incorrect view of market dynamics. In his model, the rest of the world is static and China is the only variable. According to his narrative, China’s zero-Covid policy put the market back into equilibrium by lowering demand; its rebound after lockdowns end will put the market into disequilibrium until higher prices “re-balance supply and demand.”

Felix Zulauf offers a very different perspective from Currie’s about what is happening in China. In a podcast with Wealthion’s Adam Taggart, he states that the risk is high for a Chinese “credit event” or financial collapse. There are at least $3 trillion in dollar-denominated loans to Chinese companies along with a major real-estate bust led by the downward spiral of developer Evergrande. This may put deflationary pressure on the global economy and may even result in a cascade of credit events outside of China.

In another podcast with Mauldin Economics’ Ed D’Agostino, Zulauf says that Chinese demand for commodities including oil may not rebound for perhaps a decade.

“I think that the lockdowns [in China] are sort of a camouflage to not show the world how structurally weak China has become.

“Because the Chinese economy has hit the same point as Japan in the early 1990s. It was exhausted after one of the biggest investment and credit booms of mankind…So, my guess is at least 10 years to get over this restructuring of the economy. It took Japan 20 years, and the excess is real small.

“So, I think, China you can forget as a locomotive for the world economy. And it has been the locomotive for the world economy in the last 15 years.”

Felix Zulauf

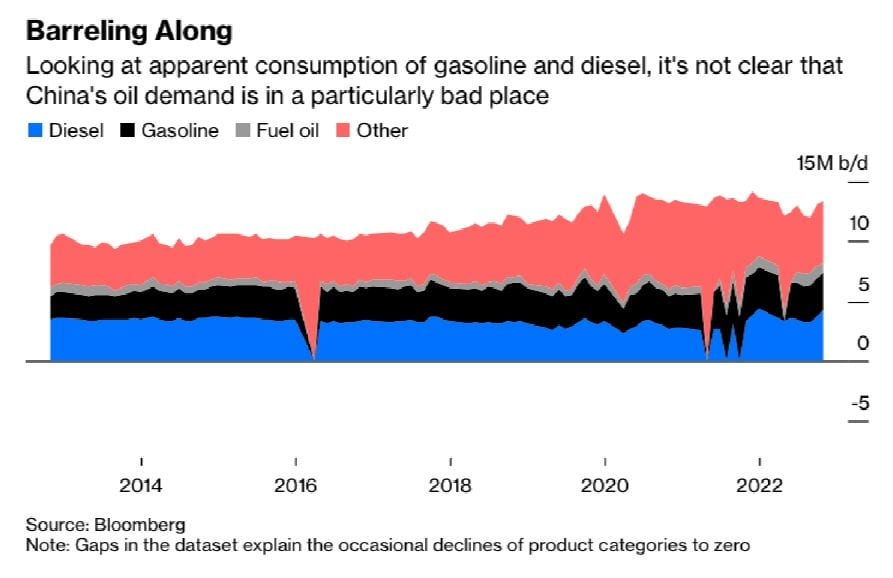

Bloomberg’s David Fickling wrote an article on December 18 that seems to support some of Zulauf’s views about China’s economy. He points out that a smaller percentage of China’s oil consumption is used for transport than in other major economies. Although gasoline and jet fuel use have declined substantially because of 2022 lockdowns, total refined product consumption is only marginally lower (Figure 4).

He states that,

“In fact, the only factor that’s prevented China’s crude oil consumption from hitting a fresh record this year has been a precipitous collapse in asphalt production….

“That parallels the bust in the country’s real estate sector: bitumen is mainly used for surfacing the roads that connect new property developments to towns, as well building materials such as roofing.”

–David Fickling, Bloomberg

His concluding observation sounds very similar to Zulauf’s comment cited above.

“It’s a sign China’s long period as a driver of oil growth is near its end.”

For most of 2022, analyst forecasts were based largely on supply and demand. If there was an expected supply-demand deficit, that meant “tight markets” which, in turn indicated higher prices. As projected deficits got larger, so did the correlative oil price forecasts.

A simple look-back at the correlation of supply-demand balance and oil prices was either not done or was disregarded.

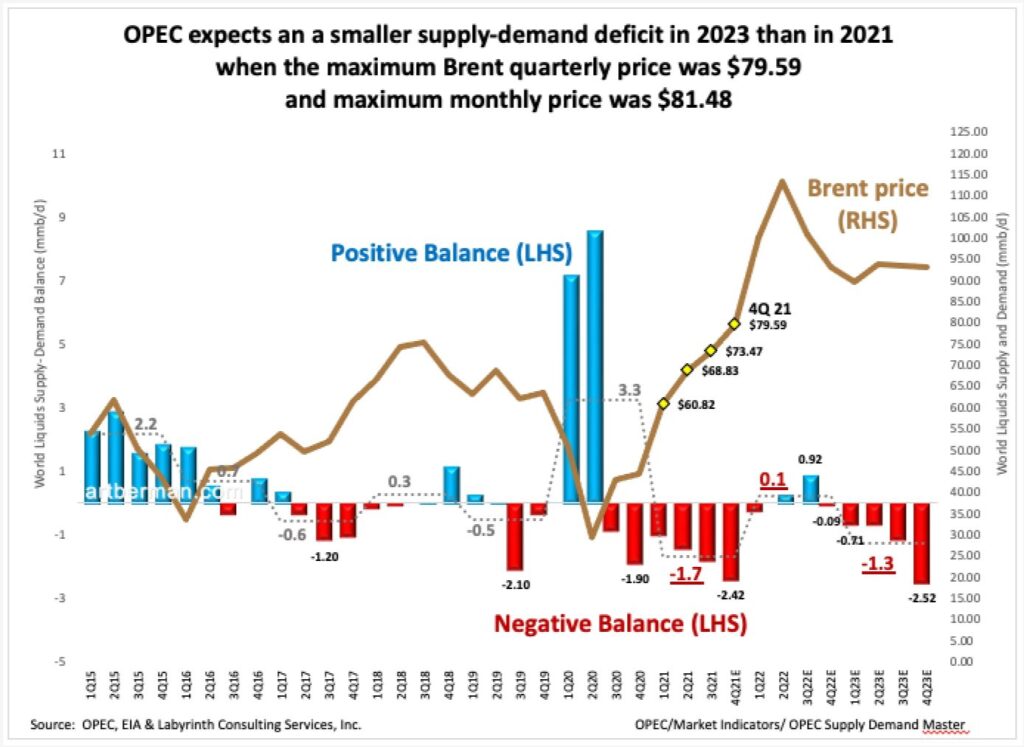

OPEC expects an a smaller supply-demand deficit in 2023 than in 2021 when the maximum Brent quarterly price was $79.59 and the maximum monthly price was $81.48 (Figure 5). Why would supply-demand considerations lead to substantially higher prices for 2023?

I expect low-to-mid $90 Brent prices in 2023 but if comparative inventory continues to increase as it has since early June, prices will continue to fall. In order to reach $90/barrel, C.I. must decrease about 40 mmb. That is feasible now that U.S. strategic petroleum releases are finished but first C.I.needs to stop increasing.

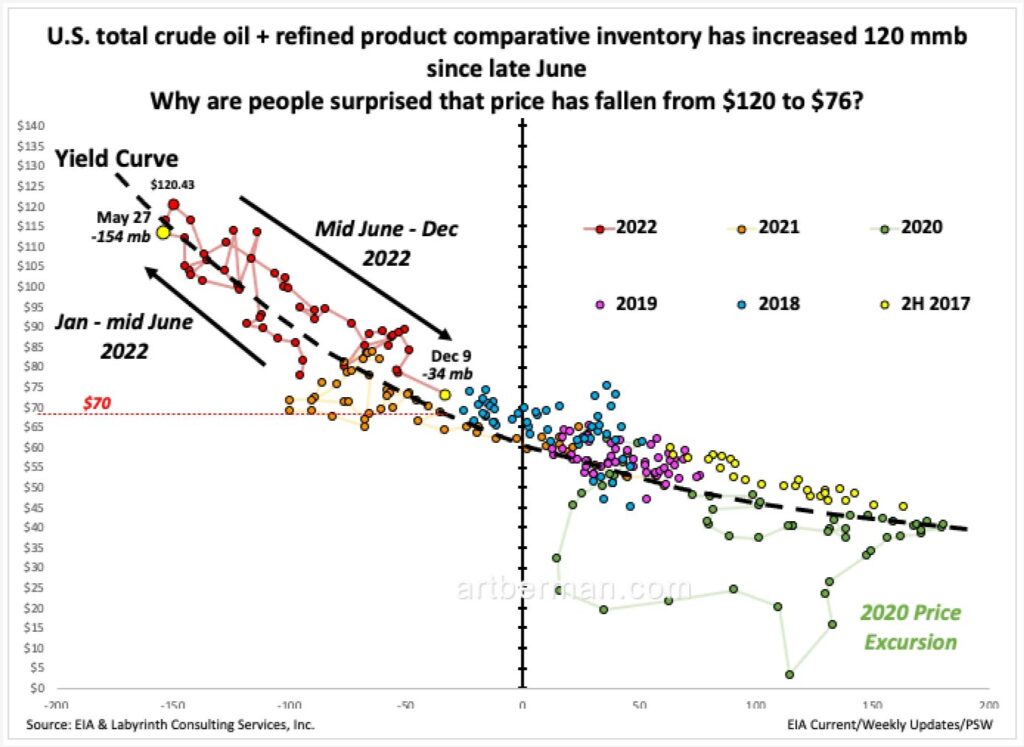

Throughout the second half of 2022, the analyst chorus proclaimed that inventories were at record lows when in fact, comparative inventory was increasing since June. U.S. total crude oil + refined product comparative inventory has increased 120 mmb since late June (Figure 6). Based on the dashed black yield curve, the current, implied market-clearing price for WTI is about $70. Why are people surprised that price has fallen from $120 to $76?

If we disregard Zulauf’s and Fickling’s views on structural problems with China’s economy, it is still unlikely that its demand for oil demand will recover quickly.

First of all, the changes to China’s zero-Covid policies are not a full reopening, and the most optimistic rebound forecast is for second quarter 2023. The latest models suggest more than 1 million deaths through 2023 with virus cases peaking around April 1. Nomura Holdings warns “We continue to caution that the road to a full reopening may still be painful and bumpy.”

It is also worth noting that U.S. transport fuel consumption has not recovered from the effects of Covid after almost three years.

A lot of what passes for oil-market analysis is just a re-shuffling of popular memes to headline simplistic reasons for daily price movements. Once these stories are repeated enough, they become embedded in our thinking with more weight than they deserve.

Rather than disagree with oil prices or try to fit them into some pre-existing framework, I try to pause and ask, What does the market know?

The spectacular price collapse in November and December was because the market knew something that analysts did not. Oil supply was no longer tight and markets were risking Chinese demand differently. Instead of anticipating China’s re-opening as the best case for higher oil prices, the market was pricing in the more-likely case that China’s long period as a driver of oil growth is near its end.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

[…] shown in previous posts that supply-demand balance is a terrible indicator of oil price and that comparative inventory does […]

[…] has consistently missed its price forecasts to the low side by at least 20% since June 2022. My point is not to criticize but to try to understand why analysts have been […]

Another astute analysis!

Thanks, Vince!

All the best,

Art

Great post. Thanks so much

Great overview there.However,with China not being the major of global oil prices and it having reached oil use tipping point and therefore slowing down demand,where then does focus shift to in the oil demand in the world? Africa?