Oil and The Changing World Order

U.S. oil inventories have fallen every week for two months yet WTI has averaged less than $40 per barrel since the end of August. That is because oil has been re-priced and markets are unwilling to pay more for it.

Those who expect a return to 2019 price levels acknowledge that the oil-demand recovery has stalled. They believe that this is because of Covid-19 and that things will return to normal once there is a vaccine.

Perspective

“I don’t think the severity of this downturn has been well understood yet.”

Sophia Koropeckyj, Moody’s Analytics

What is happening to oil markets and to the global economy is not because of a virus. The virus greatly accelerated what was already happening. Things won’t go back to normal when the virus ends. I wrote that a month ago and nothing has happened since then to change my mind.

The world is in a debt cycle that began fifty years ago. World orders change when debt cycles approach their end. Ray Dalio has studied how and why world orders have changed over the last 1500 years. These are the requisites that changing world orders have in common:

- High levels of indebtedness.

- Low interest rates that limit the ability of central banks to stimulate the economy.

- Large wealth gaps and political divisions that lead to social an political conflicts.

- A rising world power that challenges the over-extended leading power.

These criteria have clear relevance to the present world order as China challenges U.S. hegemony. Discord created by debt, interest rates and income inequality have been aggravated by the Covid-19 pandemic but will not be resolved when the virus is controlled.

What Recovery?

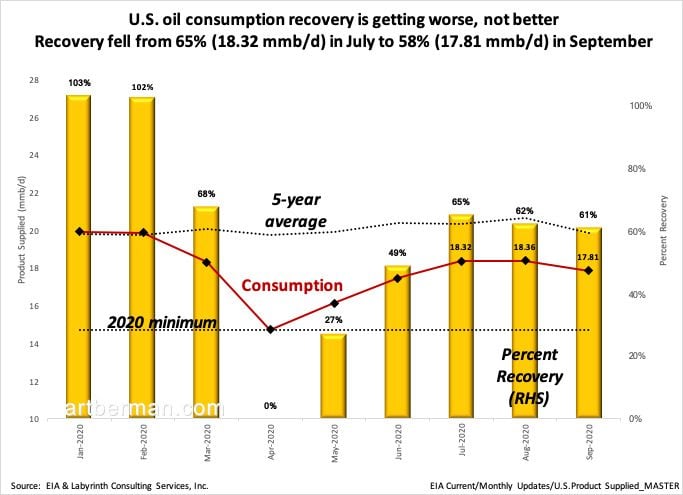

The U.S. oil consumption recovery is getting worse, not better. U.S. oil consumption recovered to 65% of normal in July and has since decreased to 61% (Figure 1).

Recovery fell from 65% (18.32 mmb/d) in July to 58% (17.81 mmb/d) in September.

Source: EIA and Labyrinth Consulting Services, Inc.

Some analysts report a much more optimistic recovery of about 90%.

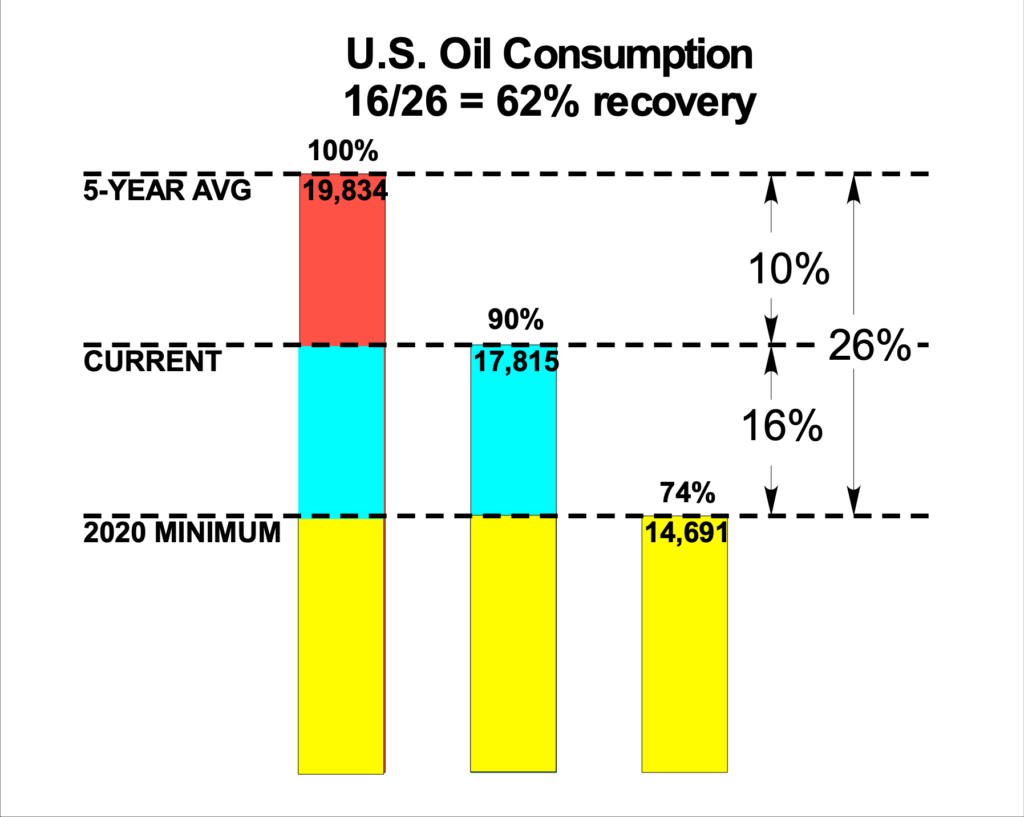

Figure 2 shows EIA consumption data for September. September consumption of 17,815 mmb is 90% of the 5-year average of 19,834 but that is not a measure of recovery. Recovery must be measured between two datums.

Recovery is determined by comparing the current level (90%) with the 2020 minimum (74%) and the 5-year average (100%). The current level is 16% of the 26% gap between the April minimum and the average. Sixteen divided by twenty-six is sixty-two so recovery is 62%, not 90% (These are rounded to an even percent so the true recovery is 61% as shown in Figure 1).

Source: Labyrinth Consulting Services, Inc.

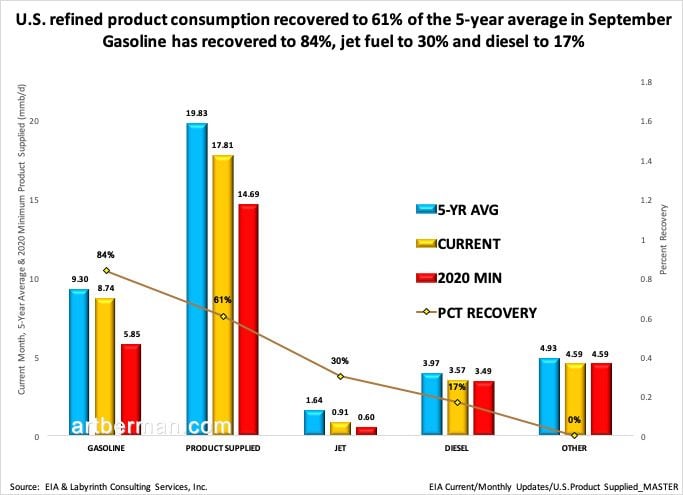

The consumption recovery continues to be dominated by gasoline which was 8.74 mmb/d in September or 84% between its minimum and five-year average (Figure 3). That is not surprising since gasoline accounts for about 45% of refined products produced from every barrel of oil. Jet fuel’s recovery is only 30% and diesel’s is only 17%.

Gasoline has recovered to 84%, jet fuel to 30% and diesel to 17%.

Source: EIA and Labyrinth Consulting Services, Inc.

Gasoline use is important but driving around to see friends and make small purchases contributes little to economic activity.

Diesel is the barometer of the economy and its use is normally fairly insensitive to price. As long as there are orders, trucks, trains and ships run. When diesel use is down, it is because there are few orders. With recovery at 17%, it is difficult to be very optimistic about the state of the economy.

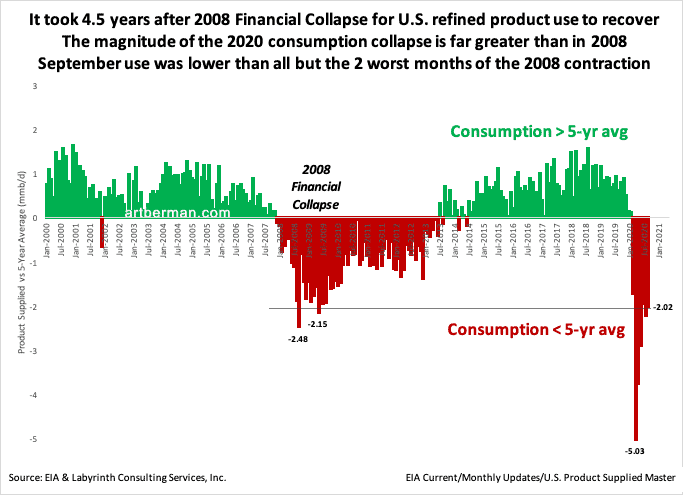

It took 4 1/2 years for oil consumption to return to the five-year average after the 2008 Financial Collapse (Figure 4). The present collapse is far greater and September use was lower than all but the worst two months of the last recovery from 2009 to 2013.

This is very significant. Why should we expect this recovery to proceed any faster than the last one?

The magnitude of the 2020 consumption collapse is far greater than in 2008.

September use was lower than all but the 2 worst months of the 2008 contraction.

Source: EIA and Labyrinth Consulting Services, Inc.

Paradigm Change

Much of the thinking about oil markets and the economy assumes that what is happening now is a temporary anomaly and that things will return to the previous state at some time.

We are in a depression—not a recession, but a depression. And I think the dynamics of a depression are different than they are in a recession because depressions invoke a secular change in behavior. Classic business cycle recessions are forgotten about within a year after they end—the scars from this one will take years to heal.

David Rosenberg, Rosenberg Research

We should pay attention to what David Rosenberg says but even his stern message suggests a return to normal after a number of years. Return is never a useful or valid assumption for the future but particularly not now. A new paradigm is needed.

A paradigm is a model that for a time seems to explain the state of the world better than competing theories (Thomas Kuhn, The Structure of Scientific Revolutions). Economic growth has been the ruling paradigm since the end of World War II. Technological innovation, capitalism and democracy have evolved as possible causes for the growth paradigm. The problem is that they were hardly unique to the second half of the twentieth century.

Energy is the economy. Money is a call on energy. Debt is a lien on future energy.

The extraordinary growth after 1945 was because of the widespread shift to petroleum as the primary energy source for the world. Because a barrel of oil contains the equivalent of about 4 1/2 years of human work, the resulting increase in productivity was the true cause for economic growth.

Early empires rose by enslaving conquered populations and capturing their work, and by taking their gold—a claim on work. World War I was fought initially over coal. Germany challenged England’s energy dominance by sinking ships like the Lusitania that was carrying coal. World War II was fought largely over oil. Germany’s first attacked Poland because it produced oil. Japan took Indonesia for its oil and then attacked the United States for denying it oil exports.

The United States rose initially on the backs of negro slaves. It became a major power first on the back of coal and then petroleum, the most productive slave in human history.

Great states fall when they reach the limits of their resources or they are defeated in wars trying to obtain more. The rise and fall of world powers is closely related to their access to credit which, in turn, is a call on future energy resources.

The world order has changed. U.S. dominance is declining and China’s is rising. Producing countries largely determined oil prices until 2014. Since then, consuming countries led by China have begun to assert their power.

Many people tell me, “I agree with everything you say but the difference between you and me is that you’re a pessimist and I’m an optimist.”

I am neither an optimist or a pessimist. I am a scientist. I use data to best describe the present state of things. If someone prefers a different story, I understand. Stories are good for entertainment but rarely lead to a clear view of what the future may bring much less good investment decisions.

The growth paradigm is dead or dying. Most future energy scenarios do not acknowledge slow growth. They imagine that technology will allow the world to simply switch from fossil to renewable energy without sacrificing living standards. The physics of that simply don’t work.

Most analysts incorrectly assume that slowing oil demand signals the end of the oil age. They don’t understand that all growth is slowing because of unmanageable debt and a weakening economy. Covid-19 brought that grim future to us a decade or so earlier than expected.

The world order is changing. The world will need oil more than ever because of its unparalleled productivity. Oil was responsible for the singular economic growth after World War II. It is the only thing that can prevent slow growth from becoming negative growth in that new world order.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts

Thank you for being honest, it is a treasure to read something like this on the internet for free.

My country, Brazil, discovered in 2008 the largest oil reserve the so called PRÉ-SAL. Then, the company invested in technology and refineries to extract and refine the oil. The idea was to use this potential to develop our country.

The Brazil was booming, The Economist puts the Christ flying on the first page.

At that time US intelligence spy on us. We discovered later on Wikileaks and Snowden revelations.

Some analysts say that in 2013 we suffered a hybrid attack. The color revolution started and throw the country in a chaotic situation. The goal was to let Brazil “Free” from corruption. Our idiot middle and upper class bought the idea sold by the media aligned with the financial sector and later the elected president, Dilma, was impeached. After that, our country entered into our worst recession ever and we didn’t recover yet by the way.

The next government elected, Bolsonaro, is 100% aligned with US. Our major Civil construction companies were destroyed in the process, we lost all our business in Africa and Latin America.

The supply chain was disrupted and privatization of our companies started.

PETROBRAS’s current president said that his “dream” is to see Petrobras Privatized. The case continues. The company started selling the refineries and oil reserve from PRÉ-SAL. We started to export crude oil to the US and buy refined oil from US in dollars lol.

The international financial interest has been like a vampire drinking Brazilian blood since 1500.

One more time my country will be serving the Masters, selling our food because we are the biggest “farm” of the world and while here the police and government will repress our population and sell fake dreams to an uneducated and poor population.

Could you tell if my narrative about PETROBRAS is wrong?

US companies lobbied a bunch of academics in the last century telling that in Brazil we didn’t have oil lol. But Getúlio Vargas founded PETROBRAS and it was a success. Later he himself puts a bullet in his heart leaving a letter informing about foreign interest in our oil. He said in the letter “I will leave life entering into history”.

Igor,

Petrobras was among the finest oil companies in the world not many years ago. The corruption of Brazil’s government and its willingness to take loans from China weakened Petrobras.

The political situation that you describe in Brazil is beyond my expertise. I suspect, however, that the problem is less one-sided than what you believe. Every country deserves the government it has. No country can be exploited to the degree that you suggest without willing participation from that country’s government.

Best,

Art

Art,

I had no idea up to now, reading your articles, that GDP and energy are that closely connected.

People tend to think it is their ingenuity and diligence mainly, leading to increasing GDP.

What a deception. You need both.

Keep up your work, thank you

Best Frank

Thanks, Frank. GDP itself can be somewhat misleading because it includes debt-driven expenditures and investments which are liens against future energy surpluses.

Best,

Art

Thank you Art. Now I understand how you are deriving the 17%. However, I still don’t find the small recovery in diesel usage very meaningful or worrisome given the impact of Covid on many businesses and people’s current behavior.

Diesel consumption is important because it is a measure of economic activity.

Art, Like some others, I don’t understand the percentages you are using. The graph shows diesel at 3.57 for 2020 vs 3.97 for 5 year average. That means diesel use is ~90% of pre-covid use. I interpret you to mean diesel use is 17% of pre-covid demand and THAT would be meaningful. But current diesel use of 90% versus 2019 usage would seem pretty intuitive and not all that surprising (or worrisome)

Tom,

If all you want to know is what percent of the 5-yr average diesel consumption is, you’re right it’s 90%. But if you want to know how much diesel use has RECOVERED, you have to have a starting point to measure that progress from and a reference level to compare it to.

The simple 90% has a starting point of zero. Interesting and somewhat useful but not a measure of recovery.

If the starting point was 3.492 mmb and the 5 year average (better than pre-Covid b/c consumption varies monthly/seasonally) is 3.968 mmb, the from-to difference is 0.476 mmb. The current level is 3.573 mmb which is 0.081 mmb more than the starting level of 3.492. The recovery progress is 0.081 of 0.476. That is 17%.

Think of it as money. I had $100,000 in my investment portfolio and lost $30,000 when the stock market fell in March and only had $70,000. Now I’ve recovered $25,000 of the $30,000 that I lost so I’m 95% of where I was before March which sounds pretty good. The truth, however, is that I’ve only gotten back 83% (25,000/30,000) of what I lost. That’s not bad but it’s not nearly as rosy as 95%.

Much of what happens in markets is not as simple as people would like. If you want the simple answer, great. If you want to understand things more fully, it’s not as simple.

Best,

Art

Tom,

The difference between the two approaches is essentially the arithmetic vs geometric average. They are both correct but the geometric average is more applicable to measuring portfolio returns.

Thanks for your excellent analyses. I am confused about the recovery in diesel usage. I notice the Baltic Dry index has almost fully recovered. Orders for class 8 trucks are surging. I live near the main northern east/west rail line, and traffic appears to be double from a year ago, mostly oil cars, Burlington was recently criticized for not providing sufficient cars, forcing more freight to trucks.

Can you help me understand?

Robert,

Consumption is as reported. The fact that it does not correspond to other observations does not change that.

Orders are not consumption. Casual rail observation is not quantitative. Baltic Dry is a measure of refined product leaving Europe and the US imports 0.01% of the diesel consumed.

I hope that this helps,

Art

Alan and Earl,

That is a false argument. If my bank account is down by 83%, that is not changed because the maximum money in that account is small compared with a rich person’s account. I still have a lot less money than before.

Percent is a useful measure because it allows comparison between disparate quantities.

Best,

Art

Energy Mix,

This is a place for comments on my posts, not a platform for posts by others. If you have a comment or question about my post, I will be glad to approve it. I will not, however, approve this lengthy speech. Use your own website for that, please.

Best,

Art

Earl – the relatively low recovery in diesel demand is consistent with the high levels in activity because diesel fuel production did not fall that much in the first place , at least compared with Gasoline and especially jet fuel

The data is available at the EIA website in their weekly petroleum status report – https://www.eia.gov/petroleum/supply/weekly/ – production data is available in the first set of tables – Petroleum balance sheet – both as a weekly total and a four week trailing average – excel file is called psw01

Distillate fuel oil – ’15-19 average = 3957 KBOPD, lowest point in late April = 2718 BOPD , 2nd October trailing average = 3572 BOPD

Distillate production is a lot more “jagged” than that for gasoline – any reasons ??

If the assumptions you make in this article are accurate, what are the effects on the US oil industry and in particular MLPs?

I don’t give financial advice. You may contact my business manager if there is some specific research you would like me to do.

https://www.artberman.com/contact-two/

Best,

Art

Art

as always very informative

one observation is oil & gas can only deliver if the industry makes decisions to extract more

if they don’t then negative growth with mass famines seems inevitable

John

John,

At some moment, society will have to learn what can realistically be delivered by renewable energy. Humans rarely learn without trauma. If fossil energy is abandoned, billions will die of starvation. That may be traumatic enough but I don’t know.

Best,

Art

Art

I’m retired and have large investment in EPD oil pipeline.

I heard you on George Gammon’s utube video and was very impressed with your knowledge and insights.

This current article is so compelling and comprehensive….I wish your ideas were wrong but sounds spot on.

Thanks for sharing your thoughts and analysis. I wish you were in politics. 🙂

Then something might actually happen.

Thanks, Brian.

I could never be in politics because honesty doesn’t get you elected.

Best,

Art

I am having trouble reconciling the minimal recovery in diesel fuel consumption with apparently booming trucking and rail transport and high levels of online shipment delivery. The latest (August) Cass Freight Index of Shipments (Chart 1) does not seem to comport with 17% recovery in diesel.

Earl,

Consumption is what it is. You may not think that it is consistent with class of data that you are looking at. If it is not, it is likely that what you are looking at is not very representative of the market.

Online trucking is a small portion of miles traveled for all trucking. Diesel is used by trains and ships in addition to trucks.

Perhaps your view is too narrow or you place to much emphasis on its effect on total consumption.

Best,

Art

I understand what you are saying, and I have a question. The current price reflects current and future demand unless there is growth? If there is significant growth causing more demand won’t price follow?

James,

The current price reflects what the market is willing to pay. It also reflects the dynamics of supply, demand, storage an sentiment. You cannot look at one component, growth in this case, and say what is going to happen.

Growth of what? Demand? Price? Please explain.

Best,

Art