Art Berman Newsletter: February 2021 (2021-1)

I made a lot of calls about market trends and prices in 2020. It’s time to look back and see how they turned out.

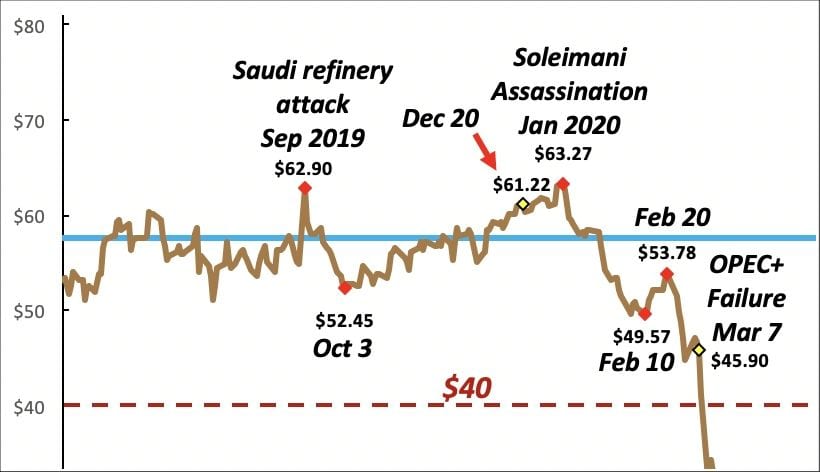

Prices fell after the Saudi refinery attack in September 2019 but then increased steadily and reached $61.22 by late December as shown in Figure 1. On December 20, I wrote:

WTI prices began increasing in early October from a low of $52.45 and reached $61.22 on December 19. I expect that this rally will continue into the new year. WTI prices of $63 or somewhat higher would not surprise me. It will last as long as someone can be found on the other side of the trade. When those counter-parties realize that nothing in the world has fundamentally changed, prices will fall to $51 or $52 as they have with the last three failed rallies of 2019.

Futures price increased to $63.27 on January 6, 2020 so that call was accurate. Prices fell to below $50/barrel by early February so my estimate was close.

WTI futures fell to $49.57 by February 11 amid concerns about Chinese oil demand because of Coronavirus. At the time, Covid was strictly a Chinese problem and the death toll there had just surpassed 1,000. It was not widely seen as a global problem.

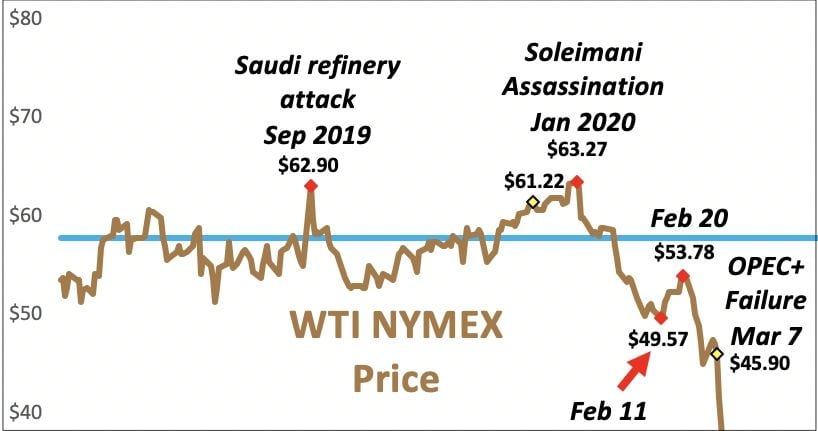

Prices rallied to $53.78 by February 20 and analysts were optimistic that the virus in China would peak soon (Figure 2).

“It’s way to early to definitely state that the virus is in place, but optimism is growing. Prices will mildly recover in the meantime, as the virus slowly eases,” one analyst wrote.

On February 11, I published an article called “Coronavirus Will Crush Oil Prices.”

Markets seem to be assuming that Coronavirus is an Asian phenomenon. It is not and will unavoidably become a global problem. I have a hard time imagining an outcome that will not crush oil prices.

WTI fell to $45.90 by the March 7 OPEC+ meeting that ended with no agreement. Saudi Arabia and Russia began a market-share and price war that caused prices to collapse to $20.11 when OPEC+ announced the largest production cut in history on April 14 (Figure 3).

On April 6, I wrote:

Almost everyone says that we will get through this. I wonder what things will be like when we do. It seems likely that oil markets and, therefore, the world economy will be quite different. Shale plays will continue to supply more than half of U.S. oil but total output may be lower. Many companies will disappear. I doubt that oil production or prices will return to 2018 levels for many years.

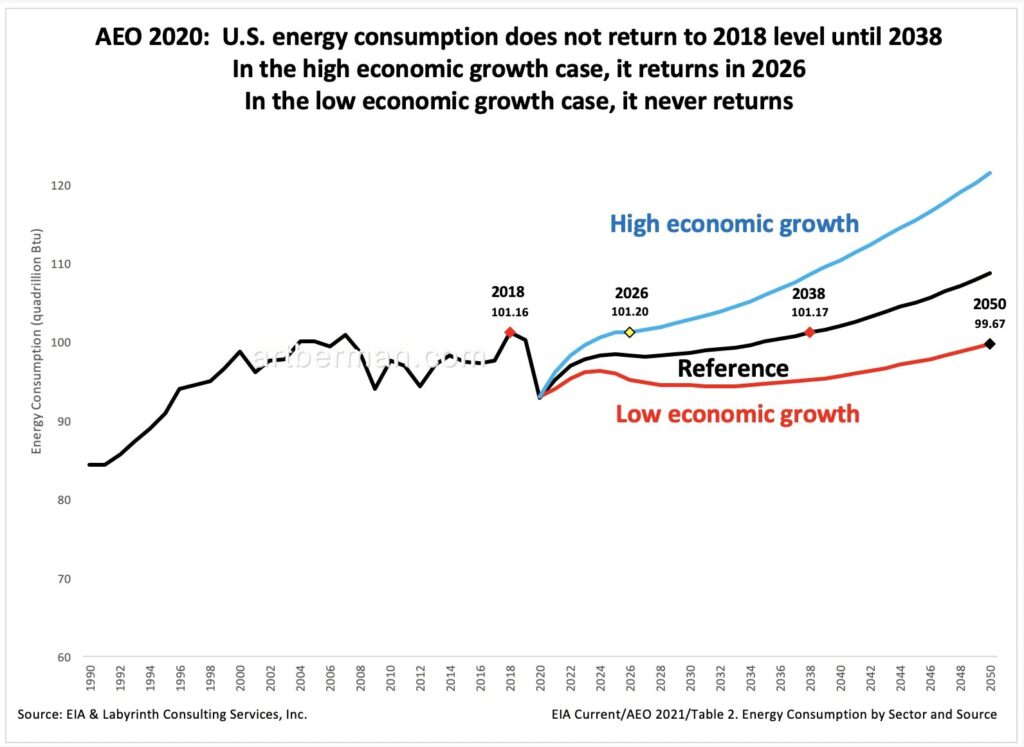

My point was that the Covid pandemic and economic closure would have long-term effects on how the world does business and on the economy beyond what many were anticipating in early April 2020. Many still imagine a return to normal once the virus is brought under control. I suspect that the global economy has been permanently damaged and that many things will never return to normal simply because people will not have the money to do what they did before.

EIA’s recently released Annual Energy Outlook 2021 seems to agree with me. Its projections do not anticipate a return to 2018 energy consumption levels until 2038 in the reference case (Figure 4). Consumption returns to 2018 levels by 2026 in the high economic growth case but in the low economic growth case, it never returns.

On May 6, I wrote:

Despite the present optimism about prices, there is still no place to store oil, the world economy is a disaster and Coronavirus is not going away. That means that oil prices will probably crash again sooner than later. Many independent oil companies will declare bankruptcy in coming months.

That was a week-and-a-half after WTI fell to -$37.63. Oil price had increased to $23.99 but there was no storage for oil. I was, perhaps understandably, overly pessimistic. I was, nonetheless, wrong about that call.

The following month on June 4, I wrote:

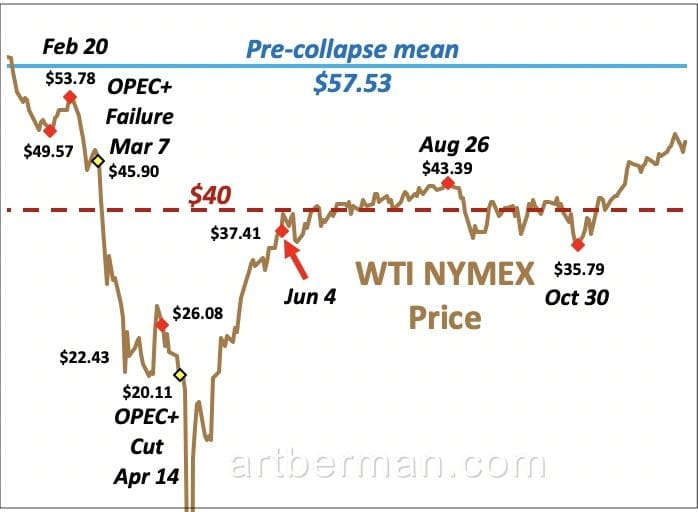

Last month I said that the current oil-price rally would end in tears. It hasn’t yet so let’s talk about why it hasn’t and why it still probably will. The current oil-price rally has room to continue to $40 or a little higher but I suspect it will weaken before then.

Prices did not weaken but I correctly called the $40 threshold that would be the average WTI futures price from that date June 4 through the end of November (Figure 5).

On July 6, I said,

This supports my expectation that WTI prices should average $40 to $45/barrel in coming weeks and possibly months. When C.I. decreases enough to persuade markets that a secular change has occurred, rig counts will increase and prices should move back to the blue yield curve and average $50 to $60 per barrel.

The following month, I wrote:

The trajectory of prices since February reflects a 4-month price discovery process that is finally stabilizing in the low $40 range. The flat slope of all three yield curves shown in Figure 4 means that price is unlikely to increase much until C.I. is reduced by about 50% of its present level of almost 140 mmb more than the five-year average.

Figure 6 is from that July Newsletter. It shows the extreme price-discovery excursion from February through June and validated my earlier call that WTI would stabilize in the $40 price range.

I wrote in early September:

Things are looking bleak for oil markets in early September 2020. WTI fell below $40 today and Brent is not far behind at a little more than $42. What concerns me most is what will happen when markets realize that U.S. oil production will fall to levels not seen since the early 2000s.

That is where I made the case that rig counts had fallen to levels that could not maintain production at 11 mmb/d and that this would have profound implications going forward.

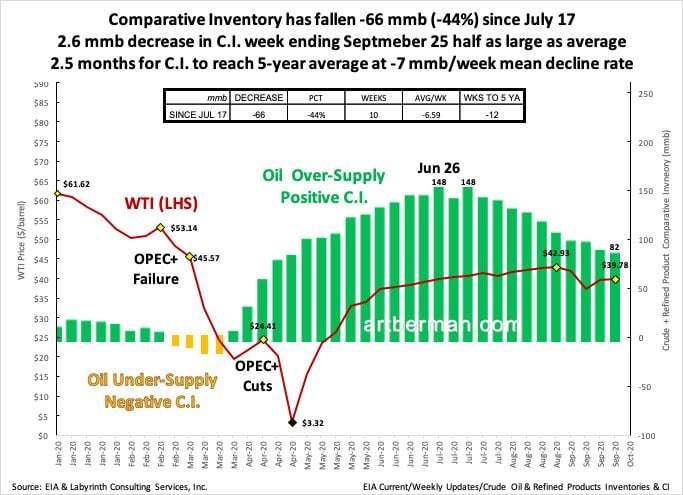

Oil prices remained capped in early October despite falling inventories because markets were focused on weak demand and not on impending supply problems (Figure 7).

By early November, I explained that WTI prices were under-priced by at least $4 or $5 based on comparative inventory. Market sentiment was still focused on weak demand but I suggested that supply urgency was the next phase for price formation.

What the yield curve tells me is that there is little likelihood that oil prices will increase to much above $45 on a sustained basis until the market changes its sense of supply urgency. Until that happens, the yield curve provides good opportunities to play the excursions. For the last six weeks, for example, WTI has been consistently $4 or $5 under-priced. It will revert and that could convert into profits for knowledgeable investors.

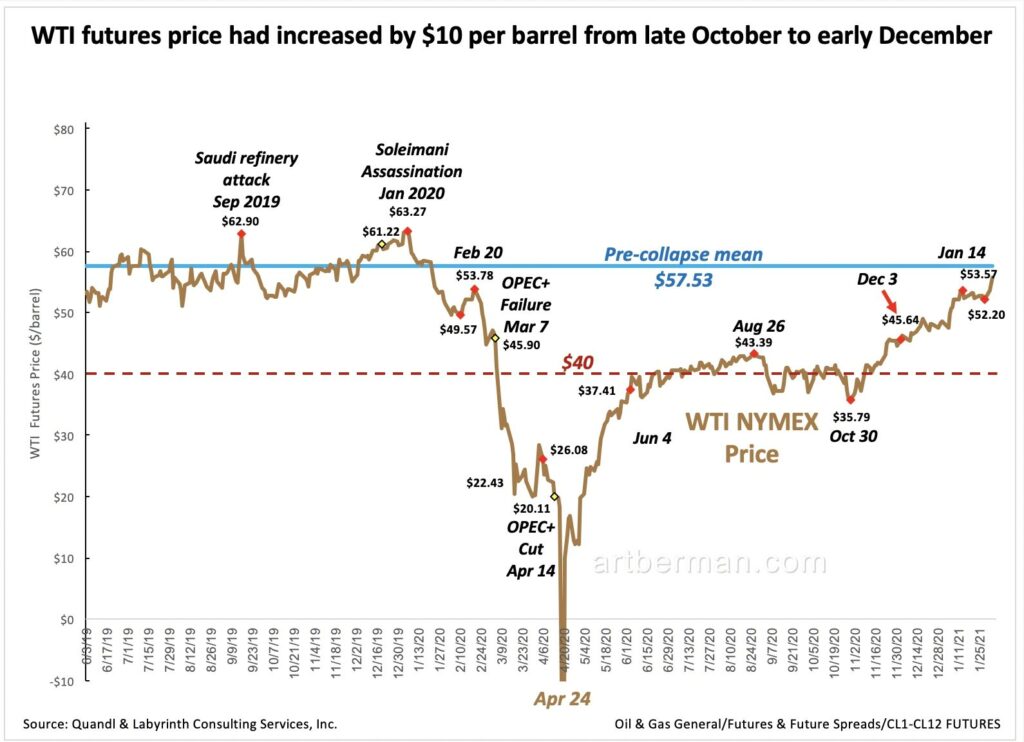

Successful Covid vaccine trials proved to be the trigger for that sense of supply urgency. I wrote on December 3.

The market is sending a price signal to producers to drill more wells. That is the reason that oil prices have increased to $45 per barrel. Once the market realizes how wrong the EIA forecast is, the price should go higher.

WTI price had increased about $10 per barrel from $35.79 on October 30 to $45.64 when I wrote that.

A month later in last month’s newsletter:

Whatever the magnitude of production decline or its precise timing, it is important to recognize what is coming. The lower-for-longer ruling paradigm has been accurate and useful since the oil-price collapse in 2014. What is happening now is different.

Most do not see WTI prices in the $60 to $70 range as likely in 2021 but I do.

Discussion

Today, WTI spot and futures prices are at $56 yesterday and Brent is at almost $59. My friend Bjarne Schieldrop at SEB in Oslo said, “The market is “close to a frenzy” and Goldman Sachs is calling for $65 Brent by summer.

After languishing in the low $50-range since early January, WTI prices have made a strong move upward this week. Analysts who are obsessed with demand focus on Covid variants and the specter of long-term low prices. Perhaps markets have turned the corner and are acknowledging that supply is the critical factor.

I use all the tools and information that other analysts use. There are two key reasons that my work and calls are different from theirs. First, I am a 40-year veteran of the oil and gas business and few of them have ever worked in that business. Second, I use comparative inventory. It is not a solution but it is an unequaled calibration technique that often makes sense of confusing and seemingly conflicting information.

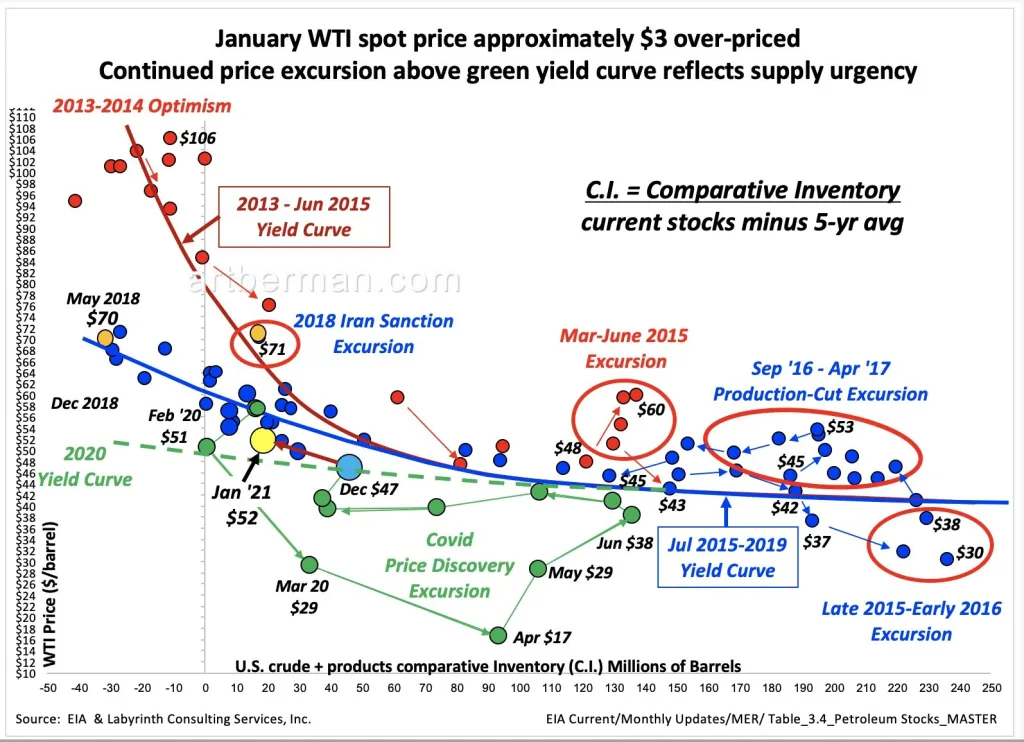

C.I. and the price-volume yield curve allowed me to establish the 2020 green yield curve in Figure 8 when WTI was still in the $20 range.

Current data (yellow circle) plots above the yield curve for the first time since February 2020. That departure from the trend reflects the market’s sense of supply urgency that I have been writing about for several months. I expect it to continue until rig counts reach levels needed to adequately supply the market.

2020 has been the most tumultuous year for oil markets and prices of my career. Despite that, my calls have been quite accurate. I appreciate your support as subscribers and hope to continue providing you with meaningful guidance in 2021.

Like Art's Work?

Share this Post:

{kind=link}

Read More Posts